A contractor lands the job, signs the subcontract, and then the paperwork starts fighting back. The contract says the GC, owner, or property manager must be added as an additional insured. The certificate gets requested fast. The project manager wants to mobilize. Everyone assumes the COI will handle it.

That assumption is where a lot of expensive problems start.

On a real jobsite, an additional insured endorsement isn't clerical cleanup. It's a risk-transfer tool that decides who gets a defense, whose policy pays first, and whether a claim gets pushed upstream or lands back on the trade contractor who thought the file was complete. The gap between what a COI seems to show and what the policy endorses can leave both sides exposed right when a claim hits.

Table of Contents

- The Contract Requirement That Trips Up Most Contractors

- What Is an Additional Insured Endorsement Really

- Decoding Common Endorsement Forms and Language

- Why Your COI Is Not a Substitute for an Endorsement

- How Vague Wording Can Make Your Coverage Useless

- A Contractor's Process for Requesting and Verifying Coverage

- Get Your Contracts and Coverage Right

The Contract Requirement That Trips Up Most Contractors

A GC issues a subcontract, gets a COI the same afternoon, and releases the sub to start work. The certificate lists the owner and GC as additional insureds, so the file looks complete. Then a claim hits six months later, counsel asks for the endorsement, and nobody can produce language that matches the contract. That is the point where a routine admin task turns into an uninsured cost.

This problem shows up early, usually before anyone steps on site. The contract requires additional insured status, primary and noncontributory wording, waiver of subrogation, and sometimes completed operations. The certificate may reference some or all of that, but the job risk sits in the actual policy wording. If the endorsement does not grant what the contract requires, the COI does not fix the gap.

For GCs, this belongs in prequalification, right alongside license checks, safety history, and scope review. Contractors building a tighter intake process for subs often start with practical guidance on general contractor insurance requirements. Contract language matters too, especially where indemnity and insurance obligations have to work together. Contractors reviewing that side of the deal should understand how Washington contract indemnity provisions affect risk transfer before work starts.

Confusion often starts on bid day

A lot of contractors get tripped up because the request sounds simple. Add the upstream party as an additional insured. Done.

Then the rider or exhibit adds conditions that change the result of a claim:

- Additional insured status for the owner, GC, and sometimes other upstream parties

- Primary and noncontributory wording so the downstream policy responds first

- Waiver of subrogation to limit recovery actions after a loss

- Completed operations protection that stays in place after the work is finished

Those are not clerical details. They decide whose carrier responds, whose deductible gets hit, and whether the GC has to fund its own defense while everyone argues over the wording.

Practical rule: If the contract asks for specific insurance terms, ask for the endorsement itself and verify that the language matches before work begins.

On a busy project, the usual failure point is easy to spot. Someone treats the COI as proof of coverage, files it, and moves on. The safer approach is slower up front but cheaper later. Match the contract requirement to the endorsement, confirm any limits on ongoing or completed operations, and clear up vague wording before the first delivery hits the site.

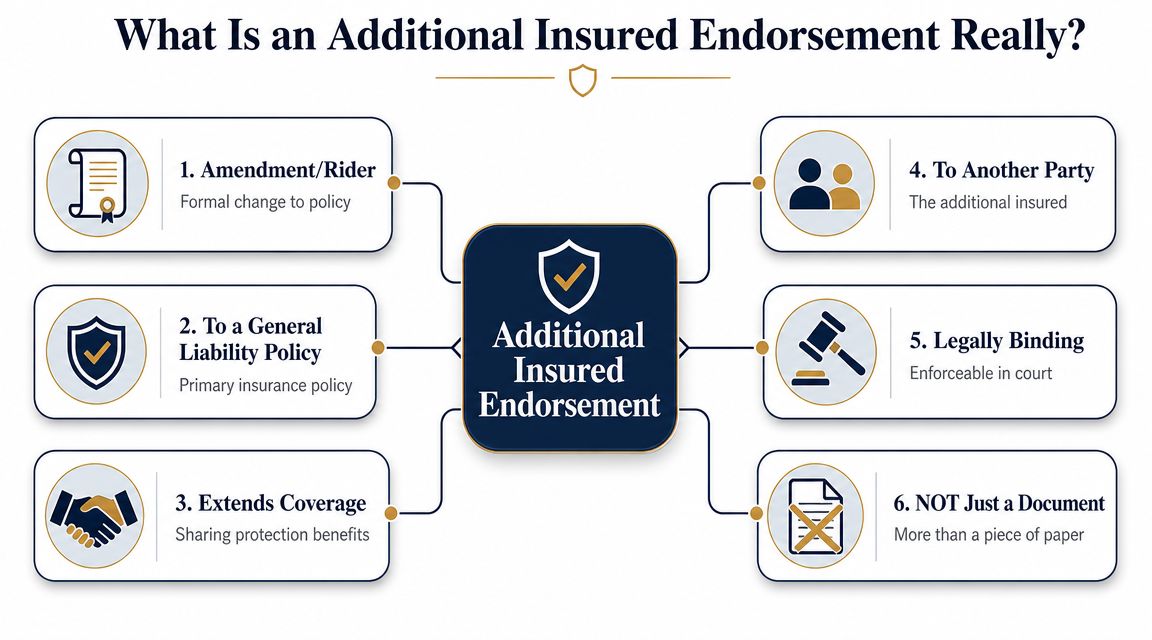

What Is an Additional Insured Endorsement Really

An additional insured endorsement is a policy change. It isn't a courtesy note from an agent, and it isn't the certificate itself. It amends the liability policy and changes who qualifies as an insured for certain claims.

That distinction matters on every construction project because the endorsement controls the actual protection, not the summary page in the file. For contractors who want a plain-language refresher on the base policy underneath all of this, this breakdown of commercial general liability for contractors is useful context. The policy being amended is the same core coverage most contractors carry, but the endorsement narrows who gets protection and under what conditions.

Contractors comparing that base policy to project-specific requirements also need to understand how general liability coverage for contractors is structured before they start agreeing to contract language they haven't verified with their broker.

It changes the policy, not just the paperwork

The easiest way to think about it is this. A COI tells someone what coverage appears to exist. An endorsement is the part that changes the contract between the insurer and the insured.

Vertikal RMS explains that an additional insured endorsement is the policy amendment that changes the insurer's “Who Is An Insured” section, and that endorsements such as CG 20 10 and CG 20 37 separate ongoing operations from completed operations (policy amendment explanation).

A trade example makes this easier to see. An HVAC subcontractor installs rooftop units on a retail buildout. During the install, the owner wants protection if a claim arises out of the HVAC contractor's work. That is one phase of exposure. A different phase begins after turnover, when a leak, vibration issue, or installation defect shows up later. If the endorsement only handles ongoing operations, the owner or GC may have no additional insured protection after the HVAC crew leaves.

Ongoing work and finished work are not the same

Contractors get tripped up here because they think “covered on the project” means covered for the life of the problem. It doesn't.

Two practical questions matter:

- Is the upstream party covered while the trade is still performing work?

- Is that same party covered after the work is complete?

Those are separate issues.

An endorsement can look compliant at mobilization and still leave a hole at closeout.

What works is asking for the endorsement that matches the project phase. What doesn't work is treating additional insured status as one broad label that covers every claim tied to the job.

Decoding Common Endorsement Forms and Language

A drywall sub starts work on Monday. The certificate looks fine, the subcontract says "add the GC and owner as additional insureds," and nobody asks for the actual endorsement until a claim hits. That is when the gap shows up. The form on file may cover only one phase of the job, only parties specifically scheduled, or only contracts with wording that matches the policy trigger.

That is why form language matters. A COI can summarize coverage, but the endorsement decides who gets defense and indemnity, when they get it, and under what conditions.

Subcontractors should tie that review back to their broader subcontractor liability exposure. On a real project, the endorsement issue rarely sits by itself. It usually shows up with contract indemnity language, completed operations obligations, and disputes over whose carrier is supposed to respond first.

Scheduled forms and blanket forms

A scheduled endorsement adds a named party. A blanket endorsement adds status automatically if the written contract requires it and the policy wording is satisfied.

Both can work. Both can also fail.

A scheduled form gives cleaner proof when the contract requires a specific owner, lender, or GC to appear by name. The trade-off is administrative. Every new upstream party may need to be added separately, and mistakes happen when the job changes hands or a second entity appears in the prime contract.

A blanket form reduces that paperwork, which helps subs running many jobs at once. The trade-off is trigger language. If the subcontract says one thing and the endorsement requires something narrower, the carrier may argue that additional insured status never attached in the first place.

Here is where contractors usually get caught:

| ISO Form Number | Coverage Type | Common Use | Main Risk |

|---|---|---|---|

| CG 20 10 04 13 | Ongoing operations | Protecting an upstream party while work is in progress | Does not address completed operations by itself |

| CG 20 37 04 13 | Completed operations | Protecting an upstream party after the work is finished | Leaves a gap during active work if used alone |

| CG 20 33 | Blanket ongoing operations | Jobs where written contracts are supposed to trigger AI status automatically | Bad or inconsistent contract wording can defeat the trigger |

| CG 20 38 | Blanket completed operations | Projects requiring automatic post-completion AI status | Same contract-trigger problem, but after closeout |

| CG 20 12 04 13 | Governmental agency form | Public work where the agency asks for a specific form | Often too narrow for private project requirements |

| CG 20 26 04 13 | Designated person or organization | Situations where a named party approach is needed | Must still match the contract and claim facts |

Form numbers matter, but the operative wording matters more.

Take a sitework contractor hired to regrade a retail pad. The subcontract requires additional insured status for the owner and GC, primary and noncontributory coverage, and completed operations protection. If the policy only includes a blanket ongoing operations form, the paperwork may look acceptable at the start of the job. Months later, a drainage problem leads to property damage after turnover, and the owner tenders the claim. That tender can fail because the endorsement on file never extended completed operations coverage.

Plain English for the contract wording

Three phrases drive most disputes.

- Primary and noncontributory addresses whose policy should respond first. If this wording is required in the contract but not supported by the policy, the upstream party may still push the claim back on your carrier, and your broker will be sorting out a problem that should have been fixed before mobilization.

- Waiver of subrogation limits the carrier's ability to pursue recovery against the protected party after paying a loss. Contractors often request it with additional insured status, but it is a separate requirement and should be verified separately.

- Completed operations deals with claims that arise after the crew leaves. Roofing, waterproofing, concrete, HVAC, framing, and electrical work all generate losses that may not show up until well after substantial completion.

The practical mistake is treating "additional insured" as if it answers all three issues. It does not.

Field takeaway: If the subcontract is precise and the endorsement is narrower, the policy language controls the claim. Review the endorsement line by line before the job starts, especially when the COI makes the coverage look broader than it really is.

Why Your COI Is Not a Substitute for an Endorsement

Friday afternoon, the owner tenders a claim to the GC after a visitor is hurt near a temporary access route. The project team pulls the file and finds a clean-looking COI that says the GC is additional insured. Then the carrier asks for the endorsement itself, and the room gets quiet.

That is the gap that creates real financial risk. A Certificate of Insurance shows what someone summarized on a form at one point in time. The endorsement is the policy change that controls whether the carrier owes a defense or indemnity. If those two documents do not match, the endorsement wins.

That mismatch shows up all the time on jobs with several tiers of subs and fast mobilization. Contractors that rely on downstream insurance usually tighten their subcontractor liability controls because paperwork drift is common once the schedule gets tight.

The COI can match the contract summary and still fail at claim time

Take an electrical subcontractor on a tenant improvement project. The GC gets a COI showing active general liability coverage, policy dates, and a note that the GC is included as additional insured. Work starts. Weeks later, a claim comes in from a temporary power setup, and the GC tenders the loss.

Now the carrier wants the endorsement. If no endorsement was issued, if the wrong form was attached, or if the endorsement only applies when very specific contract conditions are met, the COI does not solve any of it. It never changed the policy.

I tell contractors to treat the COI as an intake document, not as proof that the risk transfer requirement is done.

A certificate can confirm that coverage was represented. The endorsement determines what coverage was actually granted.

What to collect before the sub starts work

A busy project team needs a repeatable file review, not a long legal memo.

- Get the actual endorsement form. If the subcontract requires additional insured status, ask for the endorsement page or pages, not just the certificate.

- Confirm who is covered. If the endorsement is scheduled, check that the owner, GC, and any other required party are identified correctly.

- Match the endorsement to the contract requirement. A blanket endorsement may still contain conditions tied to a written contract, the scope of work, or the timing of the loss.

- Check the policy period and attachment. The form should be issued and attached to the policy in force for the job, not sent as a sample form from another account file.

- Review limits with realistic expectations. Additional insured status usually gives access to the named insured's policy limits. It does not create a separate pot of money for the GC or owner, as noted earlier in the article.

The practical fix is simple. Store the endorsement with the signed subcontract before mobilization, and compare the two documents while there is still time to correct a problem.

What goes right is straightforward. The endorsement matches the contract, the tender goes in cleanly, and the carrier can evaluate the claim without a side fight over whether coverage was ever granted. What goes wrong is expensive. The COI looked fine, the job moved ahead, and the first real review happened after a loss, when your options were already gone.

How Vague Wording Can Make Your Coverage Useless

A claim gets tendered after a loss, the certificate looked clean, and everyone assumes the additional insured issue is handled. Then coverage counsel asks for the endorsement and the subcontract. That is the moment vague wording turns into a real cost.

A flooring contractor installs polished concrete in a grocery buildout. After turnover, a customer slips near the entrance during rainy weather and sues the owner, the GC, and the flooring sub. The GC expects the flooring contractor's policy to defend it as an additional insured. The certificate may support that expectation. The endorsement may not.

That gap matters because endorsement wording often narrows coverage in ways a COI never shows. Some forms only protect the additional insured for liability caused, in whole or in part, by the named insured's work. Some are narrower in practice and apply only where the upstream party is being held responsible for the subcontractor's conduct, not for its own separate fault. Shared limits create another pressure point. A serious injury claim can burn through the same policy limits the subcontractor needs for its own defense.

Where vague wording breaks down

The problem usually appears in the allegations.

If the slip-and-fall claim says the flooring sub created a dangerous surface, the GC has a better argument for tendering downstream. If the same complaint says the GC failed to maintain the entrance, ignored water tracking, or kept the area open without proper controls, the carrier may accept only part of the tender or dispute it outright. The GC then lands in an expensive middle ground. It tenders the claim, but still has to use its own policy and its own deductible to deal with the pieces tied to its alleged negligence.

Completed operations is another common failure point. A roofer finishes a warehouse project, months pass, and water intrusion damages stored product. The owner tenders as an additional insured because the certificate from the job file says coverage was in place. If the endorsement only applies to ongoing operations, or the contract did not require completed operations clearly enough, the tender can fail after the work is done. Contractors dealing with both active jobsite risk and post-completion exposure should review a trade-specific view of general liability coverage for roofing contractors before they assume one endorsement handles both.

One phrase can change the result. So can one missing phrase.

The contract and the endorsement have to say the same thing

Vague contract language causes its own problems. If the subcontract says the sub will name the GC as an additional insured "where required," or "for work performed," that sounds acceptable until a claim arrives. Required under what terms. For ongoing operations only. For completed operations too. Primary and noncontributory. Limited to liability caused by the sub. Those details control the tender.

I see this mistake often on busy projects. Operations signs the subcontract, accounting collects the COI, and nobody compares the actual endorsement language to the indemnity and insurance exhibit. Months later, the project team learns the endorsement never matched the risk transfer requirement they thought they bought.

The practical standard is simple. If the contract asks for a certain scope of additional insured coverage, the endorsement needs to grant that scope in words that hold up when a complaint is filed. If those words are missing, soft, or conditional, the coverage can be useless when the job goes bad.

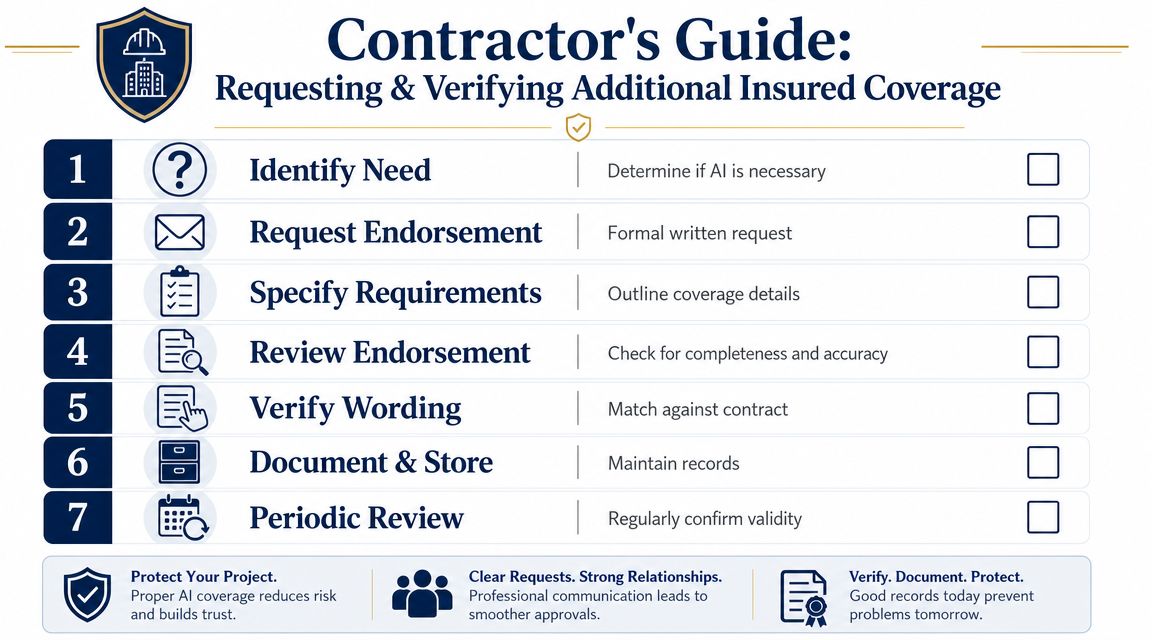

A Contractor's Process for Requesting and Verifying Coverage

A claim does not expose a bad additional insured process. The process usually failed months earlier, when one team collected a certificate, another signed the subcontract, and nobody checked whether the endorsement matched the deal.

That gap is expensive.

I see it on active projects all the time. The GC believes the subcontractor added the required parties because the COI says so. The subcontractor believes the broker handled it because the request was sent over. Then an injury or property damage claim comes in, defense is tendered, and the carrier points to endorsement wording that is narrower than the contract requirement. The job file looked complete. The risk transfer was not.

Roofing contractors run into this problem often because one job can create both active jobsite exposure and post-completion exposure. A trade-specific view of general liability coverage for roofing contractors helps frame the right questions before the subcontract is signed and before the certificate request goes out.

For subcontractors providing coverage

Subcontractors should treat the additional insured request as a scope item, not a paperwork item.

- Read the insurance exhibit before sending anything to the broker. Confirm who must be added, whether the requirement is blanket or scheduled, and whether it applies to ongoing operations, completed operations, or both.

- Send the broker the contract language itself. Do not send a summary from the project team. Small wording changes can produce the wrong endorsement.

- Review the endorsement after it is issued. Check the named insured, the additional insured entity names, the form number, and the coverage trigger.

- Compare the endorsement against the subcontract requirement line by line. If the contract requires completed operations or primary and noncontributory wording, confirm the policy grants it.

- Send the endorsement with the COI. That saves another round of requests and reduces the chance that the receiving party relies on the certificate alone.

A request to the broker should be specific enough to survive a claim review, not just broad enough to get a certificate issued. For example:

Additional insured status is required for the owner and general contractor for ongoing operations and completed operations, on a primary and noncontributory basis, where required by written contract.

That wording gives the broker something concrete to place. It also gives the subcontractor a clean reference point when the endorsement comes back wrong.

For GCs and owners receiving coverage

GCs and owners need a verification process that assumes the COI may overstate what the policy does.

- Ask for the endorsement, not only the certificate. A COI can say "additional insured" while the endorsement limits coverage in ways the certificate never shows.

- Match legal names exactly. Watch for missing LLCs, related entities left off the form, and project names that do not tie back to the contract.

- Check the trigger language. If the endorsement only applies when required by a written contract, make sure the written contract is signed by the right parties and says the right thing.

- Check the project phase. Coverage for ongoing operations does not solve a completed operations requirement.

- Track policy renewals on longer jobs. The endorsement form can change at renewal even when the certificate looks familiar.

- Store the endorsement where the claims team can find it fast. During a tender, time gets wasted when the only document in the file is the certificate.

One practical rule helps here. No crew starts until one person confirms that the contract requirement, the COI, and the endorsement all line up.

That person needs authority to reject bad paperwork.

On a busy project, this usually works best as an intake step owned by risk management, contract administration, or a designated project lead. What fails is the split process where operations sends the contract, accounting collects the certificate, and no one is responsible for reading the endorsement itself. That is how contractors end up paying their own defense costs on a claim they thought had been transferred.

Get Your Contracts and Coverage Right

The hard part about an additional insured endorsement isn't the definition. It's the false sense of completion that comes with a clean COI file.

Contractors need to separate paperwork from actual coverage. The endorsement changes the policy. The certificate doesn't. The contract wording matters. The project phase matters. The chain of contracts matters. And if a claim hits a shared policy, the available limits aren't magically larger because more parties were added.

A practical checklist looks like this:

- Read the subcontract insurance language before signing

- Ask for the exact endorsement, not only the certificate

- Confirm whether the requirement applies to ongoing work, finished work, or both

- Check whether the contract wording matches the trigger in the endorsement

- Store the endorsement where the claim team can find it fast

Contractors who handle this well usually treat it as part of job costing and risk control, not just admin support. That approach avoids the most common mistake in construction insurance. Assuming a certificate means the risk transfer is done.

If a current policy, subcontract package, or COI process hasn't been reviewed lately, a free coverage review from Coverage Axis can help identify gaps in additional insured wording, contract compliance, and trade-specific liability before the next job starts.