A lot of window cleaners start shopping insurance when a client asks for a certificate, a landlord wants to be added to the policy, or a larger commercial bid lands on the desk and suddenly the paperwork matters as much as the price. That's usually when the confusion starts. One policy says liability. Another says auto. Another says property. Then a quote comes back higher than expected because the carrier cares how high the crew works, what equipment they use, and whether they're on ladders, poles, scaffolds, or rope.

That's where window washing insurance stops being a box-checking exercise and becomes an operating decision. A storefront route, a residential crew using water-fed poles, and a high-rise contractor on suspended access don't present the same risk. They shouldn't carry the same insurance program either.

Table of Contents

- The Four Essential Policies for Every Window Washing Business

- Decoding General Liability Your Most Important Coverage

- How Jobsite Risks and Work Types Affect Your Premiums

- Advanced Coverage to Help You Win Bigger Contracts

- Mastering COIs Additional Insureds and Contract Requirements

- Get the Right Window Washing Insurance Without Overpaying

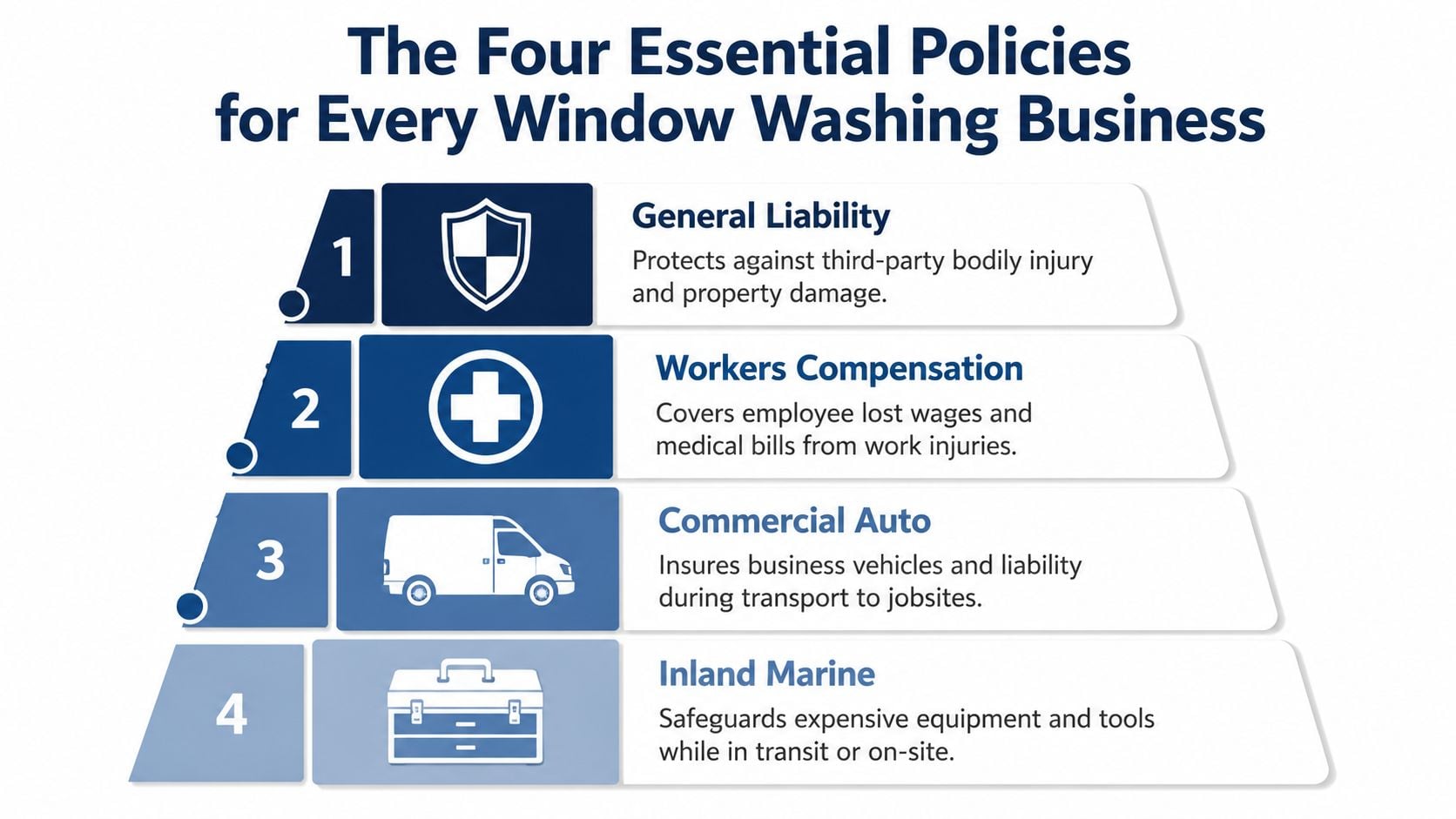

The Four Essential Policies for Every Window Washing Business

A property manager approves your bid, then sends over the insurance requirements. They want general liability, workers' compensation, and auto coverage on file before your crew sets one ladder. If your policy setup does not match how you work, that job can stall before the first pane gets touched.

For a window washing business, the core insurance program usually comes down to four policies. The right mix depends on three things: how high you work, whether you use employees or subs, and what equipment and vehicles move from site to site.

What each policy does on a real job

General liability handles third-party injury and third-party property damage claims tied to your operations. Industry cost data for window cleaners puts a typical general liability policy with $1 million per occurrence and $2 million aggregate limits at about $60 per month, or $719 per year, based on window cleaner liability cost data. On a real job, this is the policy that comes into play if water gets tracked across a storefront entrance and a customer slips, or if a tool drops from ladder height and injures someone below.

Workers' compensation pays for employee injury claims, including medical bills and lost wages, when a crew member gets hurt on the job. Earlier cost data in this article put workers' comp at a higher monthly cost than general liability, which fits the exposure. Ladder work, roof access, repetitive pole use, and carrying gear in and out of buildings all raise the chance of injury. If a helper twists a knee stepping off a ladder rung or strains a shoulder handling long water-fed poles, this is the policy built for that loss.

One practical rule applies here. If someone works under your business name and climbs, lifts, drives, or handles equipment for the job, review workers' comp before the next project starts.

Commercial auto covers vehicles used in the business and the liability tied to driving between jobs. A personal auto policy may not respond the way you expect if the vehicle is being used for work. If your van is loaded with ladders, poles, towels, and pure water equipment and it rear-ends another car on the way to a site, commercial auto is the coverage meant for that claim.

Inland marine covers mobile tools and equipment while they are in transit, stored in a vehicle, or being used at a jobsite. This is the policy many window cleaners miss until a theft or breakage happens. Water-fed poles, extension poles, pumps, ladders, and other gear move constantly. General liability is not designed to pay for your own stolen or damaged equipment.

Core Insurance Coverages for Window Cleaners

| Insurance Type | What It Covers | Typical Jobsite Claim Example |

|---|---|---|

| General Liability | Third-party bodily injury and third-party property damage | A pedestrian slips near a wet storefront entrance during service |

| Workers Compensation | Employee medical bills and lost wages after a work injury | A helper falls from a ladder and needs treatment and time off |

| Commercial Auto | Business vehicle damage and liability from road use | A work van loaded with ladders hits another vehicle between jobs |

| Inland Marine | Tools and mobile equipment while in transit or at a site | Water-fed poles and squeegees are stolen from a vehicle or damaged on site |

Some businesses also add a business owner's policy or professional liability, especially if they lease space, store inventory, or sign contracts with broader insurance language. Those can make sense, but they are not the starting point for most window washers.

The starting point is matching these four policies to the way the work gets done. A solo storefront cleaner with one van has a different insurance setup than a crew handling mid-rise routes, lifts, and large commercial accounts. That difference affects not just coverage, but price, contract eligibility, and whether a claim gets paid cleanly when something goes wrong.

Decoding General Liability Your Most Important Coverage

General liability is the backbone of most window washing insurance programs, but it gets misunderstood more than any other policy. Contractors often assume it covers any damage that happens while they're working. It doesn't.

A clean example is a crew doing interior glass in an office. A technician puts too much pressure on an older pane seated in a fragile sash. The glass cracks. The client expects the cleaner's liability policy to pay. In many cases, the carrier points to the exclusion and denies the claim.

What general liability actually handles

General liability is built for damage or injury to others arising from business operations. In window cleaning, that usually means events around the work, not always the surface being worked on.

Typical examples include:

- Slip claims: Water drips into a lobby and someone walking through loses footing.

- Falling object claims: A tool or bucket drops from a ladder area and causes injury below.

- Incidental damage nearby: Equipment bumps trim, flooring, or another area not considered the direct work surface.

That's why the policy is still essential. It protects against exactly the sort of third-party claim that can turn into a lawsuit.

The cracked pane problem

The major trap is the care, custody, and control issue tied to property damage exclusions in the standard form. As explained in Dan Wagner's breakdown of the CGL damage to property exclusion, standard Commercial General Liability forms include exclusion j(6), which bars coverage for “that particular part of real property on which you…are performing operations.” In plain language, if the window cleaner's technique cracks the glass they're actively cleaning, the damaged pane often falls into a category the policy doesn't cover.

A lot of contractors only learn this after the first denied glass claim.

That matters because commercial glass replacement isn't a minor nuisance loss. Some insurers offer proprietary endorsements designed to soften that gap, often with limited protection for property under the contractor's control. The right move is to ask about a care, custody, and control endorsement during quoting, especially for interior work, route service on older buildings, or projects where fragile glass is part of the risk.

A standard liability policy is still the first policy to buy. It just shouldn't be treated like a cure-all.

Before binding coverage, a window washing contractor should ask three direct questions:

- Does the policy include any endorsement for property in the contractor's care?

- Are there sublimits that apply to glass or workmanship-related damage?

- Does the carrier treat interior and exterior work differently based on the operation described in the application?

If those answers are vague, the contractor probably doesn't have enough clarity yet.

How Jobsite Risks and Work Types Affect Your Premiums

A window washing company can keep revenue steady and still watch insurance costs jump after one change in operations. The usual trigger is not paperwork. It is the kind of work being taken on, how crews access the glass, and what can go wrong if something slips.

A contractor cleaning storefront glass from the ground faces a different claim pattern than a crew working from ladders, lifts, or suspended equipment. Underwriters price that difference because the severity changes fast with height, pedestrian traffic, and the type of buildings on the schedule.

Height changes pricing fast

Height is one of the first details a carrier looks at. The question is not only how high the crew can work. It is how they get there, how often they do it, and what sits below them while they work.

A dropped scraper from a six-foot ladder can damage a window ledge or startle someone below. The same tool dropped from several stories up can lead to a severe injury claim, street closure, or a lawsuit involving the property owner and the contractor. That single exposure changes how an insurer views the account.

Access method matters just as much. Water-fed poles for low-rise exterior work usually present a different risk than repeated ladder use. Boom lifts, scaffolds, and rope or suspended access draw more underwriting attention because they bring fall exposure, equipment exposure, and larger third-party injury potential.

Applications get better results when the operation is described plainly. State the maximum working height. List the access methods used in the field. Explain whether high-rise work is occasional or part of the normal book of business. Vague descriptions often lead to higher pricing, tighter terms, or a request for more information before the quote can move.

Classification and service mix affect what you pay

Premium is also shaped by how the operation is classified. Carriers usually separate lower-hazard cleaning work from operations that involve more ladder use, exterior elevation, or specialized access equipment. If the business description lumps everything together, the insurer may assume the broader and more expensive exposure.

That becomes a real business decision. If ladder work is rare and limited, say so clearly. If upper-story work is a core service, the policy needs to reflect that up front. I have seen contractors create problems for themselves by describing the business as basic window cleaning, then adding lift work, gutter cleaning, or pressure washing during the policy term without telling the carrier. The audit arrives later, the premium increases, and claim handling gets harder if the operation on the ground does not match the application.

Side services change the risk profile too. Gutter cleaning adds roof exposure. Pressure washing adds slip hazards and a greater chance of damaging surrounding surfaces. Solar panel cleaning may involve delicate property and different access issues. Those are not small details on an insurance application. They affect class code, eligibility, and final price.

What underwriters want to see

Good underwriting submissions usually share the same traits:

- A clear maximum working height: not a vague statement like "some commercial work"

- Accurate access methods: ladders, poles, lifts, scaffolds, and suspended access listed separately

- A clean service description: window cleaning separated from gutters, pressure washing, or other trades

- Payroll or revenue broken out by operation: especially if one part of the business carries more hazard than another

- Basic safety controls documented: fall protection practices, equipment inspection routines, and crew training records

Those details help the carrier price the work you do instead of pricing the worst version of it.

The practical takeaway is simple. Premium follows exposure. A company that controls where it works, how it accesses the glass, and how clearly it reports those operations usually has more options than a contractor whose application leaves the underwriter guessing.

Advanced Coverage to Help You Win Bigger Contracts

Small residential and storefront work usually doesn't demand a complicated insurance tower. Commercial property managers, multi-site contracts, and public-facing projects are different. At that point, basic liability may get the conversation started, but it won't always get the contract signed.

When umbrella coverage makes sense

Umbrella insurance sits above underlying liability policies and adds extra limits. For window cleaners, that becomes relevant when the work involves larger buildings, denser foot traffic, stricter contract language, or clients that want higher limits than the base policy provides.

A practical example is a contractor bidding on a mid-rise commercial account. The manager wants higher liability limits because the work takes place over an active sidewalk and busy parking area. The contractor's base liability policy may be adequate for smaller jobs, but not enough to satisfy the bid package. In those situations, umbrella coverage isn't just extra expense. It can be the difference between being eligible and being shut out before pricing is even considered.

Some carriers offer umbrella in $1 million increments, which can make it a targeted way to close a contract requirement without rebuilding the entire insurance program. It's especially relevant where dropped-object exposure, height, and public access all collide.

Why bonds matter on certain bids

Surety bonds aren't liability insurance. They function more like a financial guarantee tied to performance or compliance obligations in a contract. Not every window washing contractor needs them, but some public, institutional, or larger facility contracts ask for them.

If a bid package requires a bond, the message is straightforward. The client wants assurance that the contractor can fulfill the contract terms. For a cleaner trying to move from small private jobs into larger formal bids, that requirement can feel unfamiliar. It shouldn't be treated as a red flag. It's often just part of entering a different tier of work.

Contractors usually make better decisions when they treat advanced coverage like a growth tool, not overhead. If a policy or bond opens access to stronger contracts, steadier accounts, and clients with formal purchasing systems, the cost belongs in the bidding strategy from the start.

Mastering COIs Additional Insureds and Contract Requirements

The crew is loaded, the route is full, and the first stop is a commercial account that took weeks to win. Then the property manager rejects the certificate because the ownership entity is wrong, the additional insured endorsement is missing, or the contract asks for limits the policy does not carry. That kind of delay costs real money. It can also make a reliable contractor look disorganized.

A lot of insurance trouble on commercial window cleaning jobs starts before any claim happens. It starts with paperwork, contract wording, and timing.

What clients are really asking for

A certificate of insurance, or COI, is a summary of the policies in force. It usually shows the carrier, policy dates, limits, and named insured. It does not change coverage by itself. It shows what is already on the policy.

Commercial clients often want more than a COI. They may ask for additional insured status, a waiver of subrogation, or wording tied to ongoing and completed operations. In plain terms, they want the insurance program set up to match the contract before your tech steps onto the site.

That matters because window cleaning creates very specific liability concerns for owners and managers. A dropped scraper from a ladder, overspray on a pedestrian walkway, or a cracked pane during detail work can pull multiple parties into a claim. The client wants the insurance structure lined up in advance so there is less argument later about who is protected and how the claim gets tendered.

A retail center is a common example. The contract may require the property owner, management company, and sometimes the landlord entity to be listed correctly. If even one name is off, the certificate can get kicked back.

Where contractors get tripped up

The most common problem is not complicated insurance language. It is mismatch between the job requirements and the policy setup.

A small contractor may carry $1 million per occurrence and $2 million aggregate on general liability because that fits the current book of business. Then a shopping center, medical office, or municipal account requires higher limits, specific additional insured wording, or primary and noncontributory status. At that point, the issue is no longer just price. It is whether the business can satisfy the contract fast enough to keep the start date.

Higher-access work also tends to bring tighter requirements. If the account involves ladder work around public entrances, recurring service on multi-tenant buildings, or work near parked vehicles and storefront traffic, expect closer review of certificates and endorsements. Clients in those settings are usually trying to control transfer of risk, not create busywork.

How to handle contract requirements without slowing down the job

The best time to review insurance requirements is during estimating, not after the work is awarded. By then, your pricing should already reflect any added insurance cost.

Use this checklist before signing:

- Match the limits to the contract early: If the job asks for higher liability limits, confirm whether the current policy can meet them or whether excess or umbrella coverage is needed.

- Verify every entity name carefully: The building owner, property manager, and contracting party are often different legal entities.

- Confirm which endorsements are required: Some contracts use broad boilerplate language that goes beyond what the client enforces.

- Check effective dates: A COI with the wrong policy term or a pending renewal can hold up site access.

- Build the cost into the bid: If a contract requires higher limits or special endorsements, treat that as part of job cost, not an afterthought.

- Request documents early: Some endorsements can be issued quickly. Others take underwriting approval.

One good habit is keeping a standard intake process for commercial work. Ask for the insurance requirements with the bid package, not after award. That gives you time to spot problems before your office is chasing revised certificates the night before the first service call.

Fast, accurate COIs help win repeat work. Property managers remember the contractor who sends clean paperwork the first time. On larger accounts, that can matter almost as much as the quoted price.

Get the Right Window Washing Insurance Without Overpaying

A cleaner bids a three-story commercial job as if it were routine storefront work. The price looks good until the certificate request comes in, the carrier asks about maximum height, and the quote changes. That is how window washing insurance gets expensive. The premium usually jumps when the application does not match the actual job.

The best way to control cost is to give underwriters a clear picture of the work before they price it. A carrier is trying to answer a few practical questions. How high are the crews going? Are they using ladders, lifts, or rope access? Are there employees driving between jobs? Is the business cleaning ground-floor retail glass, or working on larger commercial buildings where a dropped scraper, hose, or tool could damage property below?

That detail affects both coverage and price.

What to prepare before requesting quotes

Bring the same information you would want from a subcontractor before sending them onto one of your jobs:

- Payroll records: Needed when employees are on the books and workers' comp is part of the insurance package.

- Vehicle list: Include every van, truck, or other business-use vehicle.

- Equipment schedule: List ladders, water-fed poles, pumps, pressure-related equipment, and other mobile tools.

- Operations summary: Spell out the mix of residential, storefront, low-rise commercial, and any higher-access work.

- Maximum working height: Underwriters ask this early because height changes the risk.

- Safety procedures: Show how crews handle ladder safety, fall protection, training, and jobsite supervision.

Accuracy matters. A business that cleans first-story retail and two-story homes should be described that way. A business taking on suspended work, lift work, or taller commercial properties needs to say that too. If the application understates the operation, the quote may come back cheap and still fail when a claim hits, such as a cracked pane during a ladder transfer or a tool dropped from height onto a parked car.

How to buy smarter

As noted earlier, average pricing for window cleaning insurance can look reasonable on paper. The mistake is treating an average as a buying guide. Insurance for a solo operator doing residential routes is priced differently from insurance for a crew handling commercial properties, driving multiple vehicles, and meeting property manager requirements.

A better process is to quote the business you have, and the one you plan to write next quarter.

- Describe the work with jobsite detail. State the highest work performed, access methods used, and any side services like pressure washing or gutter cleaning.

- Match coverage to the exposure. General liability covers third-party injury and property damage. Workers' comp addresses employee injuries. Commercial auto covers work vehicles. Equipment coverage helps with tools and gear that can be stolen or damaged.

- Read the exclusions and endorsements. A low premium does not help if the policy limits height, excludes certain operations, or leaves a gap in equipment or hired vehicle use.

- Price for contract work early. If the business is pursuing commercial accounts, include the cost of added insured endorsements, higher limits, or umbrella coverage in the estimate.

- Requote after operational changes. New crews, additional vans, taller buildings, and different access methods all change the risk profile.

The cheapest quote is often cheap for a reason. Sometimes the carrier is comfortable because the work is low hazard. Sometimes the application left out the part of the operation that drives claims.

Good insurance buying is closer to job costing than bargain shopping. Set up the policy around how the work gets done, where the crews go, and what can realistically go wrong on site. That is how a window washing business avoids paying for coverage it does not need, while still carrying the limits and endorsements that keep jobs moving.

Coverage Axis helps contractors build right-sized insurance programs for the work they perform, from solo window cleaners to multi-crew operations with vehicles, equipment, and commercial contract requirements. For a free quote or a coverage review, visit Coverage Axis.