A lot of Pennsylvania contractors hit the same wall at the same moment. The phone rings, a solid commercial opportunity lands in the inbox, the scope looks profitable, and then the insurance requirements page shows up. That's where many bids stall.

The problem usually isn't craftsmanship. It's that the business is carrying just enough insurance to stay active, not enough insurance to qualify for the jobs that drive revenue and margins. In practical terms, contractor insurance in PA isn't just about staying legal. It's part of the bid package, part of risk control, and part of how a contractor gets taken seriously by owners, municipalities, and general contractors.

A general contractor trying to move from kitchen remodels into light commercial tenant improvements sees this fast. The crew can do the work. The schedule works. The numbers pencil out. But if the COI can't show the required limits, the bid is dead before anyone talks about workmanship.

Table of Contents

- Your Insurance Is Your Ticket to Bigger Jobs

- PA General Liability The Real vs The Required

- Pennsylvania Workers Compensation A Non-Negotiable Rule

- Insuring Your Trucks Tools and Equipment in PA

- Winning Bids with Bonds COIs and E&O Coverage

- How to Lower Your Pennsylvania Insurance Premiums

- Get the Right PA Contractor Coverage Today

Your Insurance Is Your Ticket to Bigger Jobs

The fastest way to look small on a commercial job is to submit a bid and then ask whether the insurance requirements are negotiable. Most project owners assume they aren't. They use insurance to screen out contractors before the first truck rolls onto the site.

A Pennsylvania GC moving into restaurant buildouts sees this in real time. The owner wants proof that if a passerby gets hurt, a delivery truck causes a crash, or a subcontractor creates downstream damage, the contractor has the backing to respond. Insurance becomes a business credential.

What better coverage really buys

It buys access.

A stronger insurance program helps a contractor bid on projects with tighter contract language, larger owners, and more demanding general contractors. It also helps when the work itself changes. A remodeler taking on mixed-use property upgrades has different exposures than a crew handling single-room residential jobs. The policy stack has to match that shift.

Practical rule: If a contractor wants better jobs, the insurance program has to be built for the jobs they want next, not just the jobs they finished last year.

That applies beyond insurance too. Contractors who are tightening up operations, proposal flow, and client handoff often also invest in tools and solutions for contractors that help them look organized before a contract ever gets signed.

Where growth stalls

It usually stalls on paperwork and limits.

A contractor may have active coverage, but the limits, endorsements, and documentation don't line up with the contract. The same thing happens with bonding. A company may be qualified to build the project, but if it hasn't planned for the financial guarantee side of the bid, it loses position late. Contractors trying to understand that side of prequalification usually benefit from a plain-English breakdown of how much bonding costs.

A masonry contractor is a good example. The crew may be excellent on schools, municipal walls, or retail facades. But if the insurance setup was built for small private jobs, the business can't make the jump. That's why the right coverage program should be viewed as part compliance, part asset protection, and part sales tool.

PA General Liability The Real vs The Required

General liability is the coverage that responds when a contractor's work or operations allegedly cause third-party bodily injury or property damage. In plain language, it's the policy that helps when someone outside the company says the contractor caused a loss.

For a roofer, that can mean falling debris cracking a customer's windshield. For a remodeler, it can mean a visitor slipping on dust protection near an active work area. For a tile contractor, it can mean water escaping during a fixture reset and damaging finished flooring below.

Why the minimum doesn't win the job

Pennsylvania sets a floor for certain residential contractors, but that floor isn't what wins commercial work. Pennsylvania's HICPA registration system mandates that contractors doing over $500 in annual residential work carry liability insurance, with the Bureau of Consumer Protection expecting at least $50K/$300K/$50K. However, nearly every general contractor sub-agreement and municipal license requires $1,000,000 per occurrence / $2,000,000 aggregate as the practical baseline, meaning contractors with minimum coverage are disqualified from over 95% of commercial and municipal work (Pennsylvania general liability requirements and commercial standards).

That's the gap many contractors miss. They assume legal compliance equals market readiness. It doesn't.

A contractor can be perfectly compliant for registration purposes and still be unqualified for the projects that pay better. That's why general liability should be bought around target jobs, not just minimum state thresholds. Contractors comparing options often start with a clearer overview of general liability insurance for contractors.

What that gap looks like on paper

| Coverage | HICPA State Minimum | Typical Commercial Contract Requirement |

|---|---|---|

| Bodily injury per person | $50,000 | Usually addressed within broader $1,000,000 per occurrence requirement |

| Bodily injury per occurrence | $300,000 | $1,000,000 per occurrence |

| Property damage | $50,000 | Typically included within $1,000,000 per occurrence structure |

| Aggregate limit | Not the practical commercial benchmark | $2,000,000 aggregate |

A roofer is a good trade example here. One bad debris event can involve a person on the ground, a damaged vehicle, and legal costs if the claimant hires counsel. State-minimum-style thinking breaks down fast in that scenario. Commercial owners know it, which is why they ask for stronger limits before they issue a notice to proceed.

A general liability policy isn't just a claims tool. On larger jobs, it's an admission ticket.

There's also a contract language problem. Many commercial agreements don't just ask for higher limits. They ask for additional insured status and waiver-of-subrogation wording. A cheap policy that can't be endorsed cleanly often creates more friction than it saves in premium.

Pennsylvania Workers Compensation A Non-Negotiable Rule

Workers compensation is where Pennsylvania gets very strict, very quickly. Once a contractor has even one employee, the conversation changes from optional planning to legal obligation.

An electrical contractor hiring a first apprentice for service upgrades is a clean example. The owner may think the apprentice is only helping for a small stretch of work. Pennsylvania doesn't care whether that employee is full-time, part-time, seasonal, or temporary.

What workers comp actually does

Under the Pennsylvania Workers' Compensation Act, every employer with at least one employee, including part-time, seasonal, or temporary workers, must carry workers' compensation coverage. Failure to comply can result in fines up to $15,000 and criminal prosecution, and the state does not permit sole proprietors to exempt themselves once any employee is on board (Pennsylvania contractor insurance requirements).

This coverage is built for employee injuries arising out of work. In practical terms, it can help with medical bills and lost wages after a jobsite injury. For a framing crew, that might mean a fall. For an electrician, it might mean a shock injury. For a concrete contractor, it could be a crush or strain loss.

Contractors who want a legal overview of how injury liability can get complicated on construction sites can review insights on Pennsylvania construction accidents, especially when multiple parties are stacked on one project. For policy details and quoting, many owners start by reviewing workers compensation insurance in PA.

Where contractors get into trouble

A lot of trouble starts with misclassification.

Some contractors try to call workers subcontractors when they function like employees. That can look fine until an injury happens or an audit starts. Then payroll gets pulled back in, premium gets recalculated, and the legal exposure gets much worse.

A drywall contractor using day labor is a common pressure point. If those workers take direction, use company tools, work company hours, and operate inside the contractor's process, calling them independent subs won't magically fix the risk. If one of them gets hurt carrying board upstairs, the lack of proper workers comp can become the most expensive decision the business made all year.

The cheapest workers comp policy is the one that's correctly structured before the first injury, not the one that looked cheapest on the invoice.

Insuring Your Trucks Tools and Equipment in PA

For many contractors, the rolling shop is the business. The truck, van, trailer, and equipment inside it are what make revenue possible each morning. That's why this part of contractor insurance in PA has to be treated as operational infrastructure, not as an afterthought.

A groundskeeping contractor with a pickup, trailer, blowers, and mowers is the clearest example. If the truck is in a crash on the way to a site or the trailer gets stolen overnight, the loss isn't just physical property. It can stop crews from working.

Why personal auto coverage falls apart on work vehicles

Pennsylvania's baseline auto requirement is too low for serious contracting work. Pennsylvania's minimum commercial auto insurance requirement is $15,000/$30,000/$5,000, but this is insufficient for contractors. Municipal licenses in Philadelphia and Pittsburgh require $300,000 auto liability policies, and nearly all commercial contracts demand these higher limits, making them a primary screening criterion for project owners (Pennsylvania commercial auto requirements for contractors).

That means a contractor using state-minimum thinking on vehicles is likely cutting off municipal and commercial opportunities before the bid starts. Owners read auto limits as a sign of how a contractor handles risk. If a plumbing van rear-ends another vehicle on company time, the claim has nothing to do with whether the plumbing work was good. But it still threatens the contract relationship.

Contractors comparing fleet and vehicle coverage can get a more focused breakdown through commercial auto liability insurance.

Tools and equipment need their own protection

General liability protects against damage to others. Commercial auto protects the vehicle exposure. Neither one is designed to fully solve the problem of a stolen laser level, missing saws, damaged compact equipment, or a trailer full of trade gear disappearing from a hotel lot.

That's where inland marine usually comes in. Most contractors call it tool and equipment coverage, which is easier and more accurate for day-to-day use. It follows mobile equipment where it lives, in transit, on-site, and between locations.

A finish carpenter is a good trade example. If specialty saws and fastening equipment disappear from a locked trailer, the replacement cost hurts. The schedule hit often hurts more. Good equipment coverage helps keep a theft from turning into missed deadlines, rushed rentals, and strained client relationships.

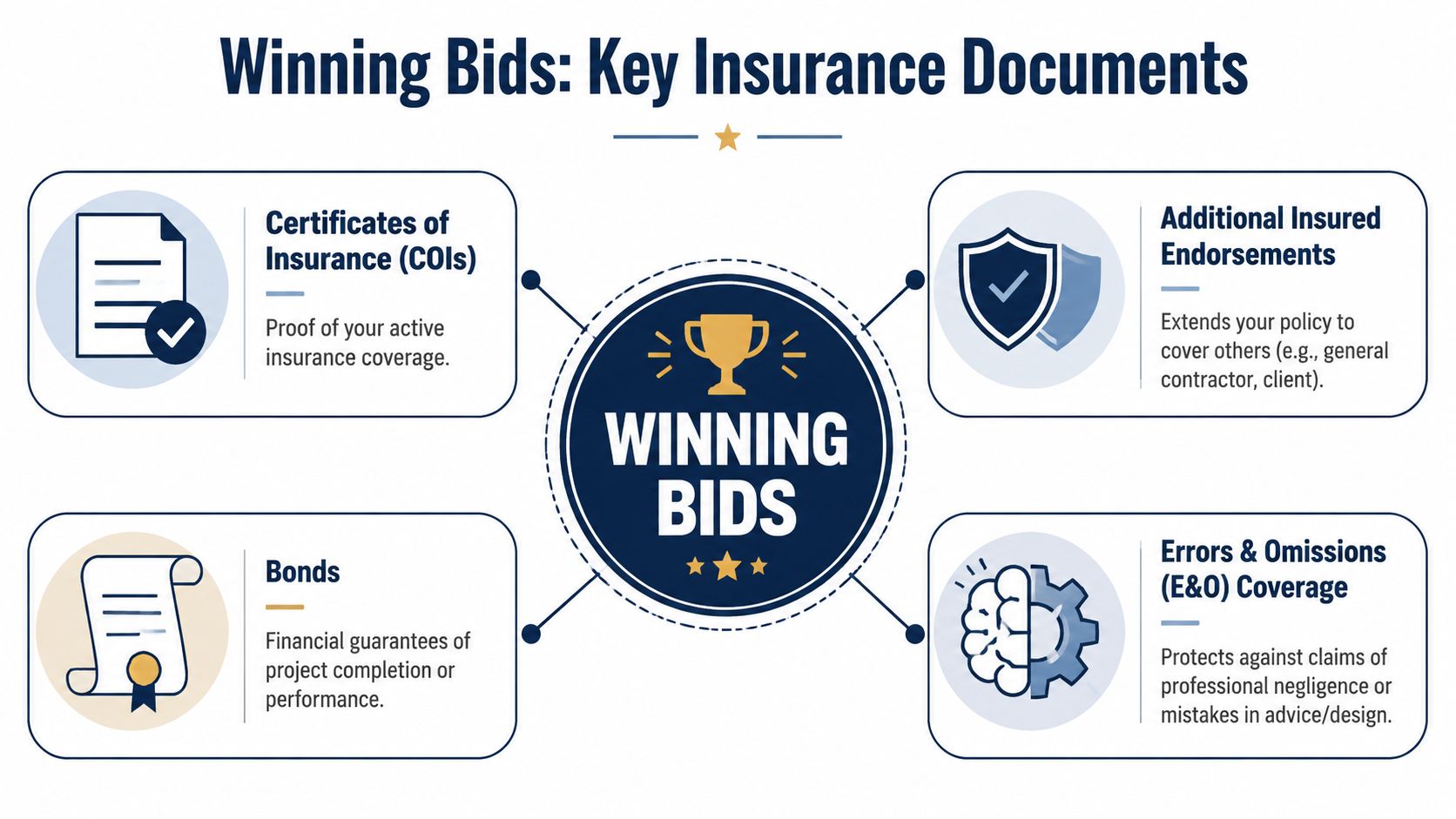

Winning Bids with Bonds COIs and E&O Coverage

A lot of contractors lose work after they've technically won it. The number is accepted, the owner is interested, and then the paperwork review starts. During this review, COIs, endorsements, bonds, and E&O become part of commercial viability.

An HVAC subcontractor on a school retrofit is a strong example. The GC may not care only about price. The GC wants proof that the sub can produce a clean certificate, add the right parties when required, and carry coverage for the kind of mistakes that create expensive callbacks or litigation.

The paperwork owners actually care about

A certificate of insurance, or COI, is the proof document. It tells the owner or GC what policies are active, what limits are carried, and whether the contractor appears ready to step on site. It doesn't replace the policy, but it often decides whether accounting, legal, or project management clears the contractor to begin.

Additional insured endorsements matter because many upstream parties want protection under the contractor's policy for claims tied to the contractor's work. That request shows up constantly on commercial contracts. Contractors that treat COIs as simple admin tasks usually run into delays. Contractors that plan for endorsement language before bidding move faster.

For a simpler explanation of how these documents function in vendor and contractor settings, this guide to a certificate of insurance for vendors is useful.

Bonds serve a different purpose. Insurance transfers certain risks of loss. A bond is a financial guarantee tied to performance or obligations. On public and larger private work, that distinction matters because owners use bonds to assess whether a contractor has the backing to finish what it starts.

Why E&O is becoming a separator

This is the missed coverage that's showing up more often in trade contracts. A common misconception is that General Liability covers faulty work claims, but this often requires a separate Errors & Omissions (E&O) policy. Recent contract trends show 68% of PA commercial GCs now mandate E&O for subcontractors in trades like HVAC and electrical, yet only 22% of these trades carry it, creating a significant compliance and risk gap.

That matters because some losses aren't clean slip-and-fall or property damage claims. They come from alleged professional mistakes, recommendations, layout decisions, or installation decisions that cause a later failure. An HVAC contractor whose system setup contributes to moisture problems or recurring performance issues may find that standard GL doesn't answer the whole claim.

Contractors who can produce COIs, endorsements, and E&O without scrambling look easier to hire. That matters when two bids are otherwise close.

Electrical contractors, HVAC firms, and specialty concrete trades should pay close attention here. The contractor carrying E&O is often in a better position when a GC narrows a sub list to firms that won't create insurance headaches after award.

How to Lower Your Pennsylvania Insurance Premiums

Premiums aren't random, and they aren't fixed. Underwriters price what they think the contractor is likely to cost them. A cleaner operation usually gets a better look than a sloppy one, even when two businesses do similar work.

A plumbing company is a useful example. The company may run service vans, handle remodel work, and keep a few helpers in the field. If claims are frequent, payroll is estimated poorly, and driver issues keep popping up, premium pressure follows. If the operation is documented and disciplined, the insurance spend usually becomes easier to control.

Underwriters reward clean operations

A contractor can usually improve pricing by improving how the business presents risk.

- Build a documented safety process: Tailgate talks, driver rules, ladder procedures, and incident reporting show that the company manages field behavior instead of reacting after losses.

- Keep payroll and classifications accurate: Workers comp problems often start when payroll is guessed, blended incorrectly, or assigned to the wrong type of work.

- Control hiring and driver quality: A commercial auto program gets more expensive when the company puts marginal drivers behind the wheel of loaded vehicles.

- Track subcontractor paperwork: Uninsured or poorly documented subs can create premium problems and claim disputes later.

Field reality: Underwriters don't price intentions. They price records, controls, and past behavior.

Bundling can help too. When general liability, auto, property-related coverages, and equipment protection are structured together, the overall program may become easier to manage and easier to defend during renewals. The main goal isn't chasing the absolute cheapest line item. It's building a stable package that holds up at audit, at claim time, and during contract review.

Cheap insurance usually gets expensive later

The wrong deductible, weak endorsements, and low limits can all make the premium look good upfront. Then the contractor loses a bid, absorbs a claim gap, or pays more during renewal because the account was built badly in the first place.

A painting contractor offers a simple example. The cheapest option might leave out the flexibility needed for larger owner requests or create problems when leased equipment, employee driving, or subcontract labor enters the picture. Saving money on paper only works if the policy still matches the way the business operates.

The best premium strategy is usually boring. Fewer claims. Better records. Cleaner jobsite practices. Correct payroll. Stronger fleet habits. That's what tends to hold pricing down without hollowing out the coverage.

Get the Right PA Contractor Coverage Today

The contractors that win better work in Pennsylvania usually treat insurance as part of operations, not as a separate admin burden. General liability helps qualify the business for serious contracts. Workers comp keeps the company compliant when employees are on payroll. Commercial auto and equipment coverage protect what keeps the field moving. COIs, endorsements, bonds, and E&O help the contractor clear the final gate between a bid and a start date.

For a concrete contractor chasing municipal flatwork, or a cabinet installer trying to move into larger mixed-trade remodels, the takeaway is the same. The right program should match the work the business wants to perform, not just the minimum it can get away with carrying.

A practical next step looks like this:

- Gather current policy documents and recent certificates so the full coverage picture is easy to review.

- Pull insurance requirements from target contracts and compare them to current limits, endorsements, and exclusions.

- Identify where qualification breaks down, especially on general liability limits, workers comp status, vehicle coverage, and paperwork turnaround.

- Get an independent coverage review built around the trade, crew structure, and project types the business is pursuing.

A contractor that handles this before bidding usually has more advantage, fewer surprises, and a much cleaner path into better-paying work.

Coverage Axis offers free quotes and no-obligation coverage reviews for contractors who need a program that fits their trade, crew, vehicles, and target jobs. If the current policy setup is limiting bids, slowing COIs, or leaving gaps in workers comp, auto, liability, or equipment protection, this is the right time to fix it. Get a free review through Coverage Axis and see what a better-structured contractor insurance program can do for the business.