An electrician leaves early for a service call. The van is loaded with conduit, testers, ladders, and the crew's core tools. On the highway, traffic stops fast, the van can't avoid the chain reaction, and now there are several damaged cars, injured drivers, a missed job, and a customer waiting for power to be restored. That's when a contractor finds out whether the auto policy was built for real work or just bought to satisfy a registration requirement.

For contractors, a vehicle isn't just transportation. It's a rolling part of the business. It carries employees, equipment, materials, and the company name into neighborhoods, job sites, apartment complexes, and commercial properties every day. One crash can trigger medical claims, property damage claims, legal costs, schedule delays, contract problems, and lost revenue all at once. Commercial auto liability insurance is the coverage that stands between that accident and the business assets the owner has spent years building.

Table of Contents

- Your Work Van Is Your Biggest Liability

- What Commercial Auto Liability Actually Covers

- Required Limits vs The Right Limits for Your Trade

- Essential Endorsements and Policy Add-Ons

- How Your Premiums Are Calculated and Controlled

- Comparing Policies and Choosing the Right Carrier

- Putting the Right Vehicle Protection in Place

Your Work Van Is Your Biggest Liability

An electrical contractor with three vans usually worries about payroll, backlog, permits, and whether materials will arrive on time. The bigger exposure often sits in the parking lot. A company vehicle can injure several people in a single accident, damage multiple cars, and bring a workday to a halt before the crew even reaches the site.

That's why commercial auto liability isn't just for tractor-trailers and large fleets. It matters for the lone plumber in a pickup, the HVAC company with install vans, the roofer towing debris trailers, and the lawn care specialist moving crews between properties. If the vehicle is used for business, the liability exposure belongs to the business too.

Milliman reported that commercial auto liability direct written premium rose to just over $43 billion in 2024, up 12.3% from 2023, and that the weighted average calendar-year loss and defense and cost containment expense ratio reached about 86%, the highest in the prior five years, which helps explain why insurers keep a close eye on contractor vehicles and driving records in this market (Milliman's 2024 commercial auto liability statutory financial results).

Why this hits contractors harder

A contractor's accident rarely stays an auto problem only. It can also become:

- A scheduling problem because the crew misses a tenant improvement, inspection, or service window.

- A contract problem because the owner or general contractor wants proof of coverage immediately.

- A reputation problem because the company logo is on the side of the van.

- A cash flow problem if the claim blows through a thin liability limit.

Practical rule: If losing one vehicle for a week would disrupt jobs, billing, or manpower, the auto policy deserves the same attention as general liability and workers compensation.

There's also the human side. When another driver gets hurt in a collision involving a work vehicle, legal and insurance issues move quickly. For readers trying to understand the other side of that event, this plain-English guide on your rights after a delivery vehicle collision shows why these claims become serious so fast.

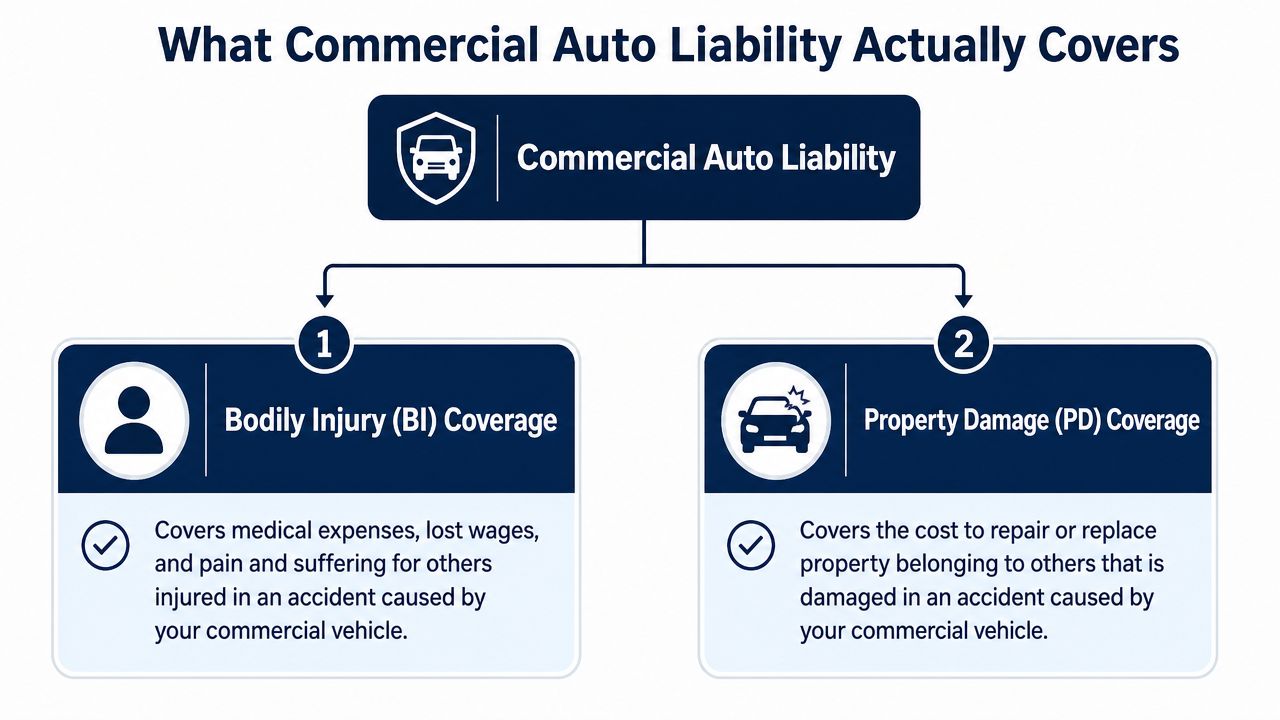

What Commercial Auto Liability Actually Covers

Commercial auto liability insurance pays when a business vehicle causes injury or damage to other people and their property. The easiest way to think about it is this. It acts like a financial firewall between a road accident and the contractor's business assets.

A plumbing van backing down a tight residential driveway clips a parked luxury car. The owner is stepping out, gets knocked off balance, and later claims an injury. The van driver was working. The vehicle was being used for business. That's a classic commercial auto liability situation.

The two parts that matter most

Bodily Injury coverage handles harm to other people when the company vehicle is at fault. In the plumbing example, that can mean the other person's medical bills, claimed lost income, and the legal defense costs tied to the injury claim, subject to the policy terms and limits.

Property Damage coverage handles damage to other people's property. In that same driveway claim, it would respond to the parked car that was hit, and in other scenarios it can involve fences, garage doors, storefront glass, gates, or job site structures.

A contractor doesn't need legal jargon to understand the practical issue. If the company vehicle injures someone else or breaks someone else's property, this is the part of the policy built to respond.

Why personal auto usually fails here

Many owners start with the wrong assumption. They assume a personal policy will somehow stretch to cover a truck or van used for service calls, deliveries, estimates, or hauling materials. That's where claims get denied or disputed.

A vehicle used in the business should be listed and rated on a commercial policy. That matters because the use is different, the exposure is different, and the insurer is pricing for business activity, not family errands.

A work vehicle that carries tools, signage, employees, and materials creates a different risk than a personal car driven to the grocery store.

For trade businesses, the distinction is important on ordinary days too. A plumbing van may enter narrow alleys, customer driveways, and active construction areas repeatedly in one week. An electrical contractor's truck may park roadside near active traffic. A flooring crew may load and unload in congested retail lots. The pattern of use itself is why commercial auto liability insurance exists.

Required Limits vs The Right Limits for Your Trade

The minimum limit required by law and the limit a contractor needs are usually not the same thing. State minimums are there to establish a legal floor. They aren't designed around a contractor towing equipment, carrying employees, parking on active job sites, or driving under commercial contract requirements.

Major market guidance reflects that reality. Nationwide notes that businesses often need more than the minimum and commonly recommends $500,000 to $1 million, while Maryland's commercial insurance guide notes that commercial auto policies may carry a typical $1 million liability limit (Nationwide's commercial auto liability guidance).

Minimum legal limit and workable business limit are different

A trade business usually runs into three separate limit questions at once:

- What the state requires: This gets the vehicle legal.

- What the contract requires: This gets the company on the job.

- What a serious accident can cost: This determines whether the business survives the claim.

Here's the cleanest way to frame it.

| State | Bodily Injury / Property Damage Minimum | Typical Contractor Requirement (CSL) |

|---|---|---|

| Varies by state | State minimums vary | $1,000,000 CSL is commonly required by project owners, general contractors, and commercial clients |

Contractors bidding commercial work already know this problem. A certificate request may look routine until the auto limit is too low. Then the award stalls, the subcontract gets revised, or the company has to scramble for higher limits at the last minute. For owners reviewing auto structures, it helps to understand how Combined Single Limit coverage works because many contractor contracts are written around CSL rather than split limits.

A landscaping claim gets expensive fast

A landscaping crew is towing a loaded trailer in wet conditions. The trailer starts to sway, the truck jackknifes, and several vehicles are involved. That single event can create multiple injury claims, multiple repair bills, and legal expenses at the same time.

A basic limit may satisfy the DMV and still fail the business. A stronger limit gives the contractor room to absorb a bad day without putting receivables, equipment, or future growth at risk.

What works in practice is matching limits to the actual exposure:

- Crew-carrying vans need more attention than many owners give them.

- Towing operations raise severity. Trailers change braking, turning, and accident dynamics.

- Urban driving increases the chance of multi-party claims.

- Commercial contracts often force the issue before a claim ever happens.

Contractors don't usually regret buying a stronger limit after a serious accident. They regret trying to save money with a limit built for a smaller risk than the one they actually run.

Essential Endorsements and Policy Add-Ons

A base liability policy covers an important piece of the risk, but it doesn't close every gap a contractor has on the road. Contractors often assume the auto policy follows every vehicle use and every item inside the vehicle. It doesn't.

That gap shows up quickly in real work. A roofing foreman drives his own pickup to grab ridge cap and fasteners. Another crew member rents a vehicle or piece of mobile equipment for a rush job. The company may still face liability even though it doesn't own those vehicles.

Where the basic auto policy stops

Hired and Non-Owned Auto liability matters when the business uses vehicles it doesn't own.

- Non-owned auto exposure: An employee uses a personal vehicle for a business errand. If there's an at-fault accident, the employee's personal auto policy may respond first, but the business can still be brought into the claim.

- Hired auto exposure: The business rents or borrows a vehicle for temporary use. Liability doesn't disappear just because the title belongs to someone else.

For contractors with even occasional off-book vehicle use, HNOA is often a basic need, not an optional extra.

The second common gap is inside the vehicle. GEICO states that unattached tools and materials transported in a vehicle are not covered by commercial auto insurance, which is why contractors often need separate inland marine or equipment coverage for what they carry to and from the job.

A stolen pipe threader, laser level, spool of wire, or box of fittings is not automatically an auto claim just because it was inside the van.

Contract language matters too

The paperwork side creates its own headaches. Many contractors need endorsements that support project requirements, not just road exposure.

That often includes:

- Additional insured requests: Common in broader insurance programs tied to contracts and upstream risk transfer. Contractors reviewing that requirement can see how an additional insured endorsement works and where it fits in the full coverage package.

- Waiver of subrogation requirements: Often included in job contracts and should be reviewed before binding or renewing.

- Umbrella coordination: Auto claims can exceed the primary layer, especially where injuries are involved.

A contractor dealing with a severe loss should also understand how excess layers affect recovery and litigation strategy. This overview on how excess liability can maximize accident claim compensation is useful for seeing why higher-layer liability coverage becomes part of major claims.

The mistake isn't buying a basic auto policy. The mistake is treating it like a complete vehicle risk solution when the business also relies on employee cars, rentals, trailers, and mobile tools.

How Your Premiums Are Calculated and Controlled

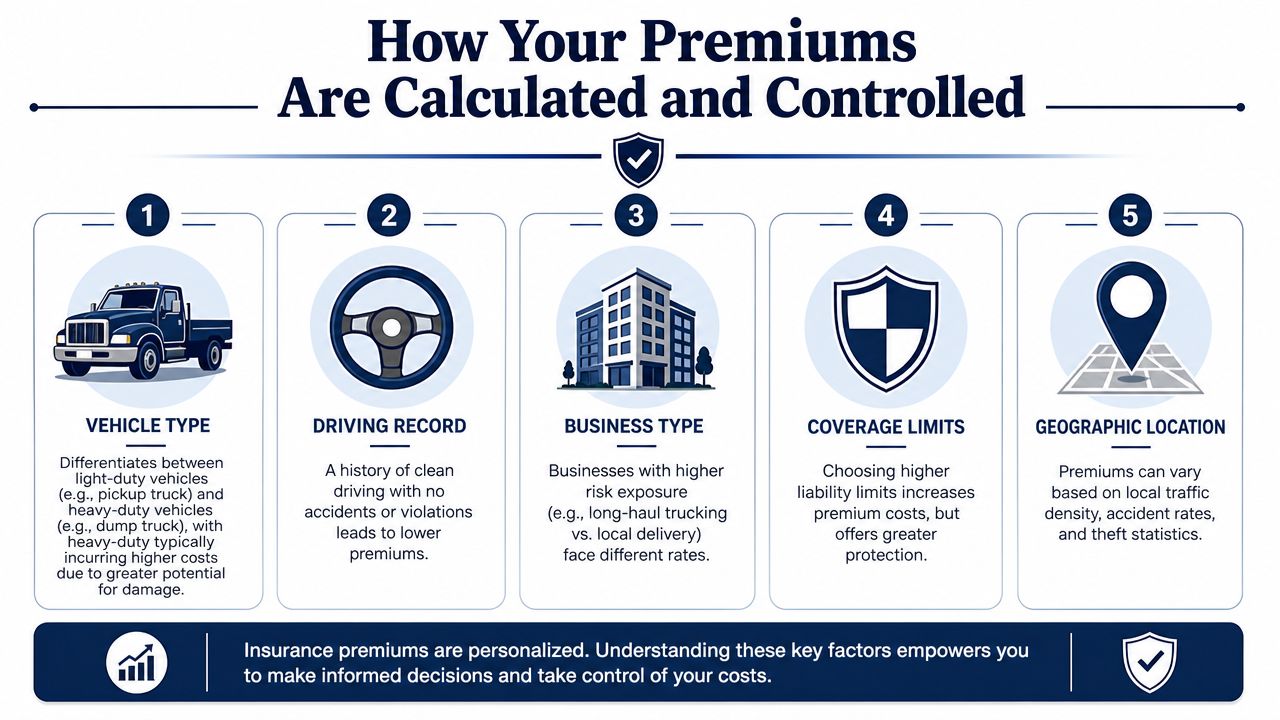

Many contractors think the premium is mostly based on the truck itself. The truck matters, but underwriters are pricing the operation around the vehicle too. They want to know who drives, what gets driven, where those vehicles go, how they're maintained, and what the loss history looks like.

That caution didn't come out of nowhere. Conning reported that commercial auto had 13 consecutive years of underwriting losses, and its market outlook noted combined loss ratios above 100% for 12 of the past 13 years, along with a $30 billion surge in commercial auto claim costs since 2012 and a 39% increase in the average statutory closed claim payment for commercial auto liability cases from 2019 to 2023 (Conning's 2025 commercial auto market update).

What underwriters look at

A general contractor with a small fleet may get hit with a rough renewal after one driver picks up multiple violations and an at-fault accident. Even if the rest of the fleet is clean, one bad driving profile can affect the account.

Underwriters commonly focus on:

- Vehicle type: A light pickup, cargo van, dump truck, and utility body truck don't present the same severity.

- Driver quality: Motor vehicle records matter. Prior violations and accidents change how the entire account is viewed.

- Radius of operation: Local service work and longer-distance driving create different exposures.

- Business type: A contractor hauling debris or towing equipment is different from a consultant driving to meetings.

- Loss history: Frequency matters. So does the story behind each claim.

A speeding violation can seem small when it happens, but insurers don't treat it as a small signal. For anyone trying to understand how traffic violations can affect future rates, this guide on Florida speeding ticket insurance cost increase gives a useful consumer-side look at why carriers react so strongly to MVR issues.

What actually helps control cost

Lower premiums usually come from cleaner risk, not from arguing harder at renewal.

- Screen drivers before handing over keys: Pull MVRs before hire and on a regular schedule afterward.

- Set a written vehicle use policy: Spell out seatbelt rules, phone use, unauthorized drivers, backing procedures, and accident reporting.

- Use telematics if the fleet justifies it: Not every contractor needs it, but vehicle tracking and driver behavior data can help identify repeat problems.

- Maintain vehicles on schedule: Brake issues, tire neglect, and lighting defects hurt both safety and underwriting.

- Limit bad-fit drivers: A marginal driver is often more expensive than a marginal truck.

For trade owners trying to benchmark broader insurance spending across their operations, this breakdown of electrical contractor insurance costs helps show how auto interacts with the rest of the insurance stack.

Better premiums usually follow better fleet discipline. They don't come from hoping an underwriter ignores weak drivers.

Comparing Policies and Choosing the Right Carrier

Two quotes can look similar on the declarations page and behave very differently when there's a claim. That's why shopping commercial auto liability insurance by premium alone usually backfires.

Consider an HVAC contractor reviewing two options. One quote is cheaper. The other costs more but comes from a financially stronger carrier with more comfort insuring trades. The cheaper quote may still lose if its underwriting appetite is shaky, the claim handling is poor, or the policy form leaves more room for disputes.

Cheap paper and usable coverage aren't the same

A contractor should compare more than price:

- Financial strength: The carrier should have the balance sheet to pay serious losses.

- Claim handling reputation: Fast, practical claim handling matters when vehicles are central to daily operations.

- Trade familiarity: Carriers that understand contracting risks usually ask better questions up front.

- Endorsement fit: The right quote should line up with actual contract requirements and vehicle use.

- Service after binding: Certificates, driver changes, and vehicle additions need to move quickly.

A low price can still be expensive if the business can't get vehicles added fast, can't satisfy project requirements, or spends weeks fighting over claim details.

Submission quality affects access

In the current market, getting the account presented well is part of the job. CRC Group noted that underwriters are becoming more selective, asking for more exposure detail and allowing more time for renewals, which makes submission quality and advisor expertise critical to securing terms at all (CRC Group's hard market perspective on commercial auto).

That means contractors should prepare:

- Driver lists that are current

- Vehicle schedules that match reality

- Loss runs with explanations where needed

- Operational detail on towing, hauling, radius, and garaging

Contractors who are also reviewing broader insurance obligations can use this summary of general contractor insurance requirements to make sure the auto quote fits the rest of the compliance picture.

One option in that process is Coverage Axis, an independent commercial insurance advisory that shops multiple A-rated carriers for contractors and can help structure commercial auto alongside general liability, inland marine, and umbrella coverage.

Putting the Right Vehicle Protection in Place

For contractors, commercial auto liability insurance isn't a box to check. It's part of keeping the business alive after the kind of accident that can interrupt jobs, trigger lawsuits, and put contract relationships at risk.

The strongest programs usually have three things in common. They carry limits that reflect real claim severity and contract demands. They add endorsements for the way the business uses vehicles. They treat driver quality as a management issue, not just an insurance issue.

An electrician's van, a plumber's service truck, a roofer's pickup, or a grounds care professional's trailer setup can all create losses that move far beyond a fender-bender. The right policy structure protects more than the vehicle. It protects receivables, payroll continuity, bidding ability, and the owner's long-term plans.

Before renewal, it also helps to review how certificates are issued and what project partners will ask for. This certificate of insurance template guide is a useful reference for understanding what hiring parties expect to see.

If a contractor wants a second look at vehicle limits, endorsements, driver schedules, or contract requirements, Coverage Axis offers free quotes and no-obligation coverage reviews designed for trade businesses. A short review can show whether the current auto policy is built for actual job site exposure or just built to get the vehicles on the road.