A Virginia contractor lands a commercial buildout, signs the subcontract, and then the paperwork starts hitting the inbox. The owner wants a certificate of insurance. The general contractor wants additional insured status. The surety asks for financials. Someone in accounting realizes the company just outgrew its old license class.

That's where a lot of contractors hit the same wall. They spend weeks getting the class a contractor license va issue handled, then assume the hard part is over. It isn't. The license may let the company pursue bigger work, but it doesn't automatically mean the insurance program, bonding capacity, payroll setup, subcontractor controls, and contract documents are ready for that work.

A roofing company is a good example. A crew may be used to re-roofs and repair contracts, then starts picking up larger multi-building jobs. The owner focuses on the license upgrade, but the actual exposure shows up later when a project requires higher liability limits, tight COI wording, and proof that every sub on site carries proper coverage.

Table of Contents

- Your License Is Approved What Now

- What a Class A License Really Means for Your Business

- Meeting Virginia's Eligibility and Financial Requirements

- The Class A Application Process Deconstructed

- The Insurance and Bonding Nobody Told You About

- Common Application Rejection Reasons to Avoid

- Your Next Steps to Get Licensed and Insured

Your License Is Approved What Now

A license approval feels like a green light. For many contractors, it's really a warning light that the business just entered a different risk category.

A common version looks like this. A general contractor or specialty trade firm has been running solid work under a lower class, then wins a project that pushes contract size, annual volume, or both. The owner handles the licensing step and assumes the existing general liability, workers compensation, and auto policies will stretch to fit the new job mix.

That assumption causes problems. Existing Virginia Class A contractor resources often focus on the $45,000 minimum net worth requirement and say much less about the insurance side. They also note that Class A contractors can take unlimited project sizes, while standard GL and workers comp policies are usually built around the contractor's stated volume and crew size. That gap can leave a contractor legally licensed for work the current insurance program may not fully support, as described in this Virginia Class A licensing FAQ.

Practical rule: A bigger license doesn't upgrade a policy. It only expands what the company is legally allowed to pursue.

A concrete contractor sees this quickly. A firm that used to pour smaller slabs may move into larger commercial foundations or site packages. The work changes. The payroll changes. The equipment mix changes. The hired and non-owned auto exposure often changes too, especially when supervisors, pickups, trailers, and rented equipment start moving between jobs.

Two questions matter right after approval:

- Can the company legally sign the work? The license addresses that.

- Can the company meet the project's insurance and bond requirements without scrambling? That's a separate issue.

Contractors who treat Class A as a business expansion project usually perform better than contractors who treat it like a form-filing exercise. The paperwork matters. The insurance alignment matters more once jobs get larger, owners get stricter, and contract terms get less forgiving.

What a Class A License Really Means for Your Business

Class A is the top contractor license tier in Virginia. In plain language, it's the license built for bigger project values, higher annual volume, and more operational complexity.

The two triggers that matter

Virginia's Class A framework uses a dual trigger. A Class A firm performs or manages construction when a single project is at least $150,000 or when the total value of work in a 12-month period reaches $1,000,000, according to this Virginia Class A threshold summary.

That second trigger catches contractors by surprise. They watch the size of each contract, but they don't always watch how quickly multiple mid-size jobs stack up across the year.

A high-volume roofing contractor is a good example. None of the jobs may look massive on their own. But several apartment reroofs, storm repairs, and commercial maintenance contracts can push the company into Class A territory through total annual work. That matters for licensing, and it also matters for insurance planning because larger backlog usually means more payroll, more subs, more vehicles, and more chance that one claim hits during a busy stretch.

How the license classes work in practice

The easiest way to think about license classes is capacity.

| License class | What it signals in practice |

|---|---|

| Class C | Small-scale work and lower project values |

| Class B | Mid-range work with a ceiling on project size and annual volume |

| Class A | Large-scale or fast-scaling work where the business needs room to take on bigger contracts |

That's why Class A changes business decisions. It affects bidding strategy, staffing, contract review, and how a company presents itself to owners, lenders, and sureties.

For a GC, this often means moving from local light commercial jobs into work that carries tougher downstream contract requirements. For a specialty subcontractor, it can mean finally qualifying for larger projects that demand stronger documentation. Contractors working in that lane can compare operational considerations with this guide for general contractors and their risk profile.

On paper, Class A is a license class. In the field, it's permission to operate at a scale where small administrative mistakes become expensive problems.

That's the meaning behind the class a contractor license va search. It isn't just about obtaining a certificate. It's about deciding whether the business is ready to handle bigger contractual obligations without creating preventable risk.

Meeting Virginia's Eligibility and Financial Requirements

You win a larger commercial job, then the owner asks for your license details, financials, and proof of coverage before issuing the notice to proceed. That is when Class A eligibility stops being paperwork and starts affecting cash flow.

Virginia expects a Class A contractor to show more than ambition. The business needs a qualifying individual with the right level of experience and completed testing, and the company needs financial backing that supports work at a larger scale. A general licensing overview from Virginia Class A, B, and C contractor licensing requirements outlines the higher threshold compared with lower license classes.

What Virginia is really checking

The state is trying to answer a practical question. Can this company take on larger contracts without failing on the business side?

That is why the file centers on three things:

- A qualified designated employee with enough relevant experience to support the classification

- Required education and exam completion before the application is approved

- Financial capacity shown through net worth documentation or another accepted method

Those items are easy to treat as boxes to check. They are really early screening for risk.

Experience matters because bigger jobs create problems that do not show up on small residential or light commercial work. Schedule compression, change order disputes, equipment lead times, supervision across multiple crews, and downstream warranty obligations all put pressure on the company at once. A designated employee who has already worked through those issues is less likely to make an expensive mistake when the project gets tight.

The financial piece matters for the same reason. A contractor can be profitable on paper and still get squeezed in the field. Material deposits go out before draws come in. Payroll hits every week whether the owner has paid or not. One backcharge, one delayed inspection, or one job running long can put real strain on operating cash.

Why net worth matters after the application is approved

A lot of contractors focus on net worth only long enough to submit the license file. That is usually a mistake.

The same financial condition that helps support the application also affects how the business is viewed by underwriters, bond producers, lenders, and project owners. If you are stepping up into larger work, those parties want to know whether the company can carry payroll, absorb a delay, and fix a problem without falling apart. The license may let you bid the job. It does not guarantee anyone will trust you with it.

Insurance starts to change here too. If your headcount grows after getting Class A status, the policy setup that fit a smaller operation can become inaccurate fast. Payroll estimates, class codes, subcontractor handling, and audit exposure all need a second look. Contractors adding crews or moving into broader GC work usually benefit from reviewing how workers compensation for general contractors is structured before an audit or claim exposes the gap.

What a clean eligibility file usually looks like

The strongest applications tend to have the same traits:

- Clear experience records for the designated employee, tied to the type of work the business will perform

- Financial statements that are readable and consistent, not pieced together at the last minute

- Education and exam records completed early, before a pending bid creates deadline pressure

- Matching business information across the application, entity records, insurance documents, and tax filings

That last point causes more trouble than contractors expect. If the entity name on the application does not match the name on your insurance or corporate records, reviewers start asking questions. So do underwriters. Small inconsistencies make the file look unstable, even when the work itself is solid.

A strong license file does more than satisfy the board. It shows that the business can support larger contracts without creating preventable insurance, bonding, or cash-flow problems.

The pre-license course helps get the application over the line. It usually does not prepare contractors for what comes right after approval. Once you start bidding larger jobs, owners and upstream contractors often ask for coverage terms, additional insured wording, waiver language, and bond capacity that the state did not explain. That gap is where many contractors learn that getting the Class A license was only the first step.

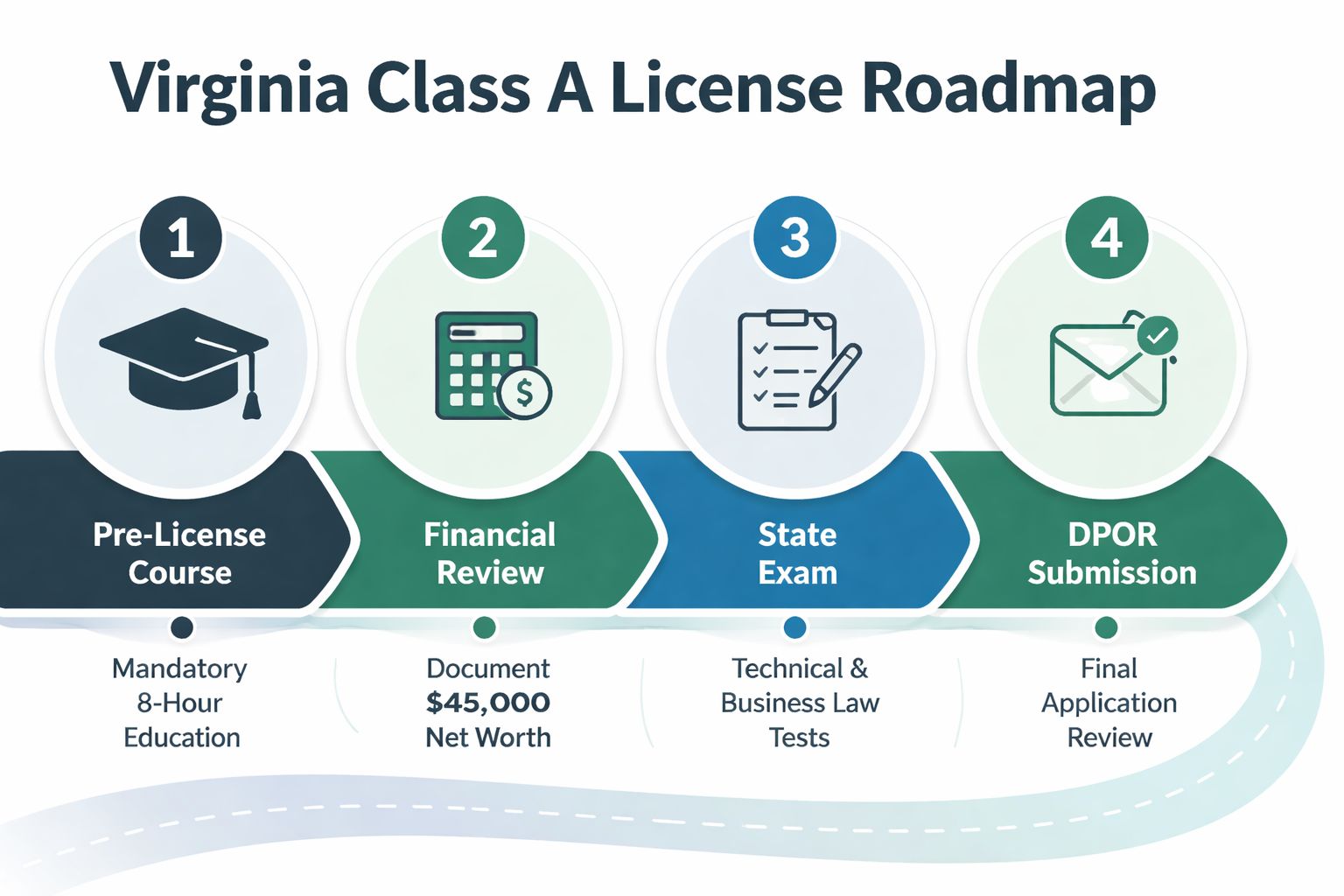

The Class A Application Process Deconstructed

Contractors usually get through the application faster when they treat it like a project schedule instead of a stack of forms. Sequence matters.

A practical sequence that keeps the file moving

The cleanest path typically follows this order:

Set up the business correctly

The legal entity, ownership records, and business name need to match everywhere. If the entity name on the application differs from the name used on insurance, contracts, or tax records, delays tend to follow.Identify the designated employee early

This person carries a lot of weight in the file. For a plumbing or HVAC company, that means confirming the right individual is tied to the correct classification before anyone schedules exams or gathers signatures.Complete the required education

Virginia requires the pre-license course before the file is complete. Contractors who wait until a bid is already on the table usually create their own timing problem.Pass the required exams

At this stage, classification details matter. A trade contractor may need both the business component and the relevant trade-related requirement. Missing one piece can stall the whole submission.Assemble financial documentation and submit a clean packet

The final package works best when every supporting document lines up with the business entity, designated person, and class level being requested.

Where contractors usually lose time

Most delays don't come from hard questions. They come from mismatched records, vague experience descriptions, or incomplete attachments.

A sheet metal contractor might submit strong field experience but describe it too broadly. “Worked on commercial jobs” isn't nearly as useful as a description tied to scope, responsibility, and supervision. The state wants enough detail to understand what the person did.

A second bottleneck is financial preparation. Contractors often wait too long to organize the net worth documentation or bond alternative, then rush the package. That usually creates preventable back-and-forth.

A third issue appears after submission. Some contractors assume the application process ends with approval, but larger projects often require bonding support soon after. Firms that expect public work, negotiated private work, or owner-required security usually benefit from understanding how surety bonds for general contractors fit into the bigger picture before the first large bid lands.

Contractors who submit a coordinated package usually move faster than contractors who submit the right pieces in the wrong order.

For an electrical contractor, the practical lesson is simple. Line up the company information, the designated employee, the education record, the testing plan, and the financial backup before chasing the next contract. That approach saves time and keeps growth from getting stuck in admin.

The Insurance and Bonding Nobody Told You About

The state's licensing requirements are not the same as a project-ready insurance program. Contractors learn that fast when an owner, GC, or lender asks for documentation the license process never really explained.

License qualification is not project protection

Virginia's Class A qualification stack includes a designated employee with at least five years' experience and a firm that demonstrates minimum net worth of $45,000. Those markers matter beyond licensing because insurance underwriters often read managerial experience and financial strength as signs of operational discipline, which can influence pricing and access to bonded work in higher-risk trades, as reflected in the Virginia administrative code discussion of Class A qualification standards.

That still doesn't mean the business is fully protected.

A contractor can meet the licensing standard and still have:

- A general liability policy built for smaller jobs

- Workers compensation payroll estimates that no longer fit the crew

- Commercial auto limits that don't reflect a larger fleet or more driving

- No umbrella support for bigger claim severity

- No clear process for owner-required additional insured wording

- Weak subcontractor insurance controls

A masonry subcontractor on a larger commercial site is a useful example. Once cranes, forklifts, staged materials, pedestrian exposure, and multiple trades are all in play, one incident can involve far more parties than a small standalone job. The contract may shift defense obligations downstream. The certificate request may include wording the subcontractor has never had to produce before.

How coverage needs change on larger work

General liability is usually the first place contractors feel the mismatch. Larger projects often come with stricter limits, tighter completed operations expectations, and more contractual transfer language. Contractors reviewing that issue often start with a clear understanding of general liability coverage for contractors.

Workers compensation changes too. More jobs usually means more payroll, more classification scrutiny, and more audit pressure. If a contractor adds crews quickly or leans harder on subs, documentation becomes critical. Misclassified labor or uninsured subs can create expensive surprises after the policy period ends.

Commercial auto also gets more serious as operations scale. Supervisors travel farther, materials move more often, and trailers or equipment may end up on the road more frequently. One serious vehicle claim can affect future insurance options as much as a jobsite injury.

Surety is a separate issue. A license-related bond or financial substitute for net worth is not the same thing as a project bond. Owners and GCs care whether the contractor can support job performance and payment obligations on a specific contract. Those are different promises to different parties.

Bigger jobs don't just increase revenue opportunity. They multiply the number of ways a contractor can be contractually right and financially exposed at the same time.

The best move is simple. Before bidding larger work, review the insurance program against the actual contract requirements, vehicle use, payroll growth, subcontractor mix, and completed operations exposure. That's what turns a Class A license into a usable business tool instead of a risky piece of paper.

Common Application Rejection Reasons to Avoid

A lot of Class A applications stall for the same reason a job gets red-tagged. The contractor knows how to do the work, but the file in front of the reviewer does not show it clearly enough to approve.

That usually shows up in three places. The business records do not match, the qualifying experience is too vague, or the application is treated like an administrative task instead of a risk screen.

What slows approvals down

Entity details cause more trouble than contractors expect. If the company name is written one way on the application, another way on financial records, and a third way on supporting forms, the reviewer has to stop and figure out whether all of it belongs to the same business. The same problem comes up with addresses, officer names, and license classifications.

Experience write-ups are another weak spot. "Managed installations and service work" is too thin for a Class A file. A reviewer needs to see trade scope, level of supervision, project type, and enough detail to tie that experience to the classification being requested. If the designated employee really ran crews, handled scheduling, oversaw code compliance, or managed subcontractors, say that plainly.

Education causes a different kind of mistake. Contractors complete the pre-license course, check the box, and assume they are ready for bigger work. The course gets you through the licensing requirement. It does not prepare you for the insurance paperwork that starts showing up with larger commercial bids, such as certificate deadlines, additional insured requests, waiver language, or contract insurance limits that exceed the policy a company currently carries.

That gap matters. I see contractors get approved, then lose time on their first serious opportunity because their license is active but their insurance program and documentation process are still built for smaller jobs.

What clean submissions usually have in common

Strong applications are specific and internally consistent. They usually include:

- Detailed work history with trade duties, supervision responsibilities, and project context written in plain language

- Matching business records across the entity filing, financial documents, and application forms

- Financial support that is complete and clear rather than assembled at the last minute

- Straight answers about prior issues instead of partial disclosure that creates follow-up questions

- A real bid-readiness review so the company knows whether its insurance and bonding setup can support the work the license allows it to pursue

That last point gets overlooked.

A contractor can submit a clean application, get the Class A license, and still be unprepared for the first contract that lands on the desk. A restoration firm, for example, may qualify on paper but still run into trouble if it cannot produce current certificates quickly, confirm subcontractor coverage, or meet owner and GC requirements without rewriting parts of its insurance program.

Clean applications answer the reviewer's questions before they have to ask them.

Use one practical test before you submit. Hand the packet to someone who does not know your company. If that person cannot tell who qualifies the business, what that person did in the field, and whether every supporting document points to the same company, the application is not ready.

Your Next Steps to Get Licensed and Insured

A Class A license opens doors, but only if the rest of the business can support the work that comes through them. The right next steps are practical and sequential.

Confirm the company needs Class A

Look at project size and total work volume, then compare that to where the business is headed, not just where it has been.Lock in the designated employee and documentation

Experience should be specific, current, and easy to verify.Finish education and exams before bid pressure builds

Contractors make worse administrative decisions when they're trying to chase a contract and complete licensing tasks at the same time.Prepare financial records carefully

The financial piece affects both the application and how outside parties view the company's stability.Review insurance before taking larger work

The license expands legal capacity. It doesn't confirm that GL, workers comp, auto, umbrella, inland marine, or subcontractor controls match the new job profile.Check fleet exposure as operations grow

Once crews, pickups, vans, and trailers start moving across more jobs, commercial auto for general contractors becomes part of the growth conversation, not just a renewal line item.

For a framing contractor, that checklist can be the difference between profitable growth and a messy first year in larger commercial work. The same license that creates opportunity can also expose weak admin, weak contracts, and weak insurance if the company scales too fast without support.

A Class A license should make the business more capable, not more fragile.

If a Virginia contractor is moving into Class A work or already has the license and wants to know whether the insurance program fits the projects being pursued, Coverage Axis offers a free quote and coverage review. A licensed advisor can review GL, workers comp, commercial auto, umbrella, and bonding needs against the company's trade, crew size, and contract requirements before a larger job exposes a gap.