A contractor opens an email at 6:12 a.m. The project looks solid. Scope fits the crew. Margins are workable. Then the insurance requirements show up. Additional insured wording is tighter than usual. Primary and noncontributory is required. There's a waiver of subrogation. The GC wants a certificate fast, and the current agent says, “That policy doesn't include that,” or worse, “We'll have to ask underwriting.”

That's when many contractors learn the hard way that the cheapest policy on last year's renewal wasn't the best deal. The actual cost shows up when a job can't be bid, a contract can't be signed, or a claim lands in a gap nobody explained in plain English.

For a contractor, an independent insurance broker isn't just someone who sells a policy. The right broker protects revenue, keeps jobs moving, and helps prevent one bad claim from turning into a payroll crisis.

Table of Contents

- Why Your Current Insurance Agent Might Cost You the Next Big Job

- Independent Broker vs Captive Agent What Contractors Must Know

- Five Key Advantages of an Independent Broker for Your Trade

- Real-World Scenarios from the Job Site

- Your Checklist for Choosing the Right Broker

- Understanding Licensing and Legal Details

- Quick FAQs for Contractors

Why Your Current Insurance Agent Might Cost You the Next Big Job

A general contractor bids a tenant improvement project. The number is competitive. The superintendent is ready. Then the owner's rep rejects the insurance package because the contractor's policy language doesn't match the contract requirements. The agent who handled the renewal last year sold a standard package, collected the premium, and disappeared until audit season.

That isn't a paperwork problem. It's a broker problem.

The bid doesn't die on the job site

Most contractors don't lose jobs because they can't swing a hammer. They lose jobs because their insurance setup can't support the contract. A framing contractor might need higher limits. A plumbing subcontractor might need completed operations language cleaned up. A remodeler might need faster certificate turnaround to get through onboarding before the work starts.

A contractor dealing with general contractor insurance requirements doesn't need a generic seller. The contractor needs someone who reads the agreement, spots the problem before bid day, and fixes it with the right carrier and endorsements.

A low premium won't help when the certificate gets rejected and the crew sits idle.

Why independent brokers are taking a larger role

The independent brokerage model keeps growing. The number of firms in the United States reached over 435,000 in 2026, and these brokers operate in all 50 states with broader market access than captive agents who are limited to one company's products, according to IBISWorld data on insurance brokers and agencies.

That matters in construction because one carrier's appetite doesn't define a contractor's business. An electrical contractor doing tenant build-outs, service work, and low-voltage installs may fit one market. The same contractor adding traffic signal work or utility-related jobs may need another. A captive agent can only sell what one company wants to write. A contractor's operations rarely fit inside that box for long.

A trade example that shows the difference

Take a concrete subcontractor chasing a larger commercial slab package. The project requires tighter contract transfer language and fast proof of coverage for the owner, GC, and lender. The old agent can't move quickly and doesn't have alternatives. The contractor misses the window.

An independent insurance broker works differently. The broker shops the account, matches the work class correctly, and builds the policy around the actual exposure. For a contractor, that changes insurance from an annual bill into a job-winning tool.

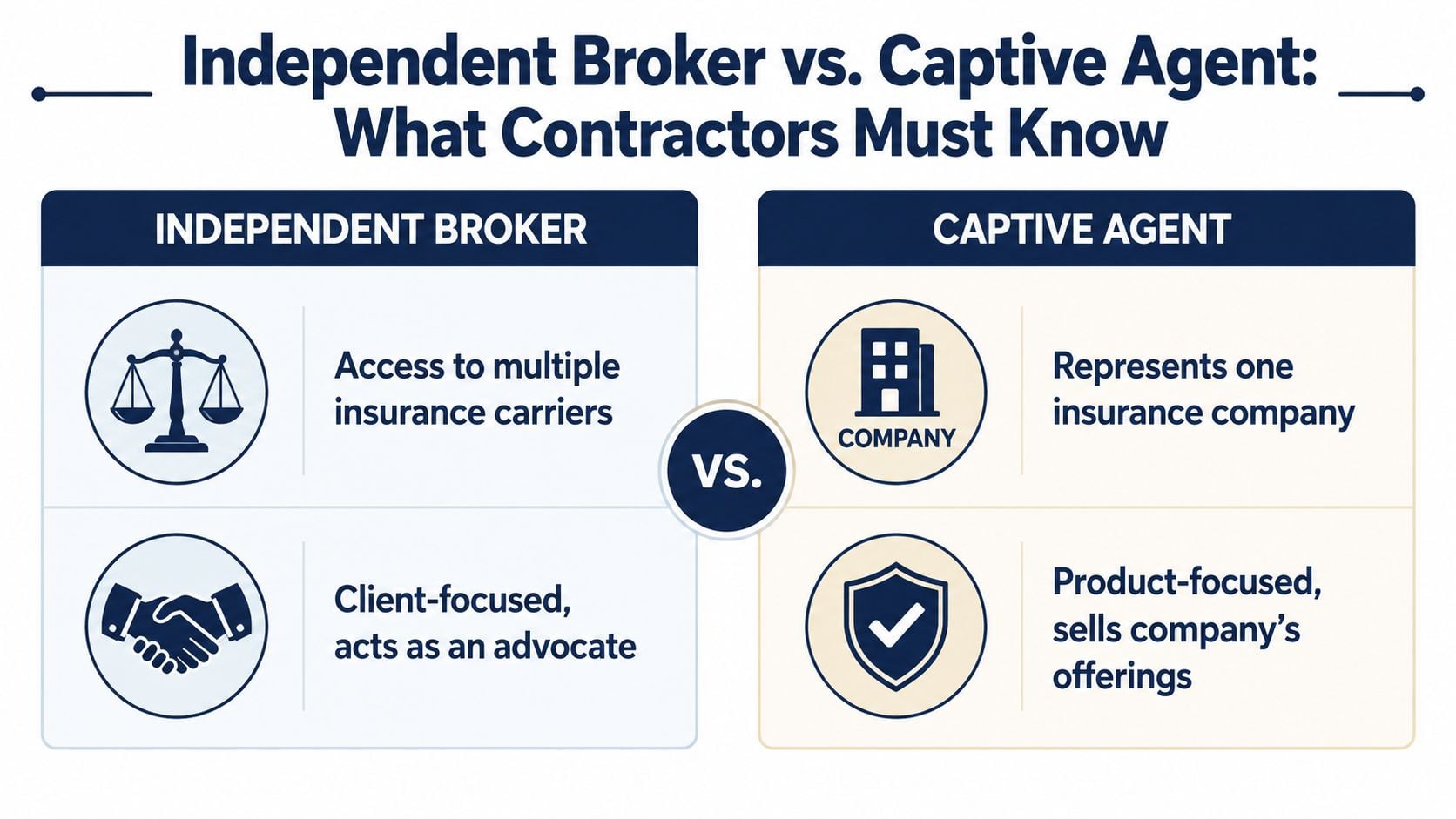

Independent Broker vs Captive Agent What Contractors Must Know

Contractors hear “agent” and “broker” used like they mean the same thing. They don't.

An independent insurance broker is like a general contractor building a custom project. The broker sources from multiple suppliers, compares options, and assembles a fit for the job. A captive agent is closer to a sales rep for one factory. If that factory doesn't make what the project needs, the answer is still whatever the factory has on the shelf.

Who works for whom

Here's the plain-English breakdown contractors should keep in mind when asking what insurance contractors need.

| Role | What they do | Why it matters to a contractor |

|---|---|---|

| Independent broker | Shops multiple carriers and structures coverage around the contractor's operations | Better fit for mixed trades, changing scope, and contract requirements |

| Captive agent | Sells one insurance company's products | Fewer options when that carrier doesn't like roofing, hauling, restoration, or multi-state work |

| Wholesaler | Accesses specialty or hard-to-place markets through retail brokers | Useful when a trade has unusual exposures or standard markets won't quote |

A wholesaler usually isn't the person a contractor works with day to day. The contractor's retail broker uses that wholesale access when needed. That's common in tougher trades, unusual losses, or specialty work.

What this looks like on a real project

A roofing contractor takes on residential reroof, small commercial flat roof jobs, and occasional sheet metal work. One carrier might like residential but avoid certain commercial roof exposures. Another carrier may be better with the commercial side. A captive agent has one answer. An independent broker has options.

Practical rule: If a contractor's business changes faster than one carrier's appetite, that contractor needs a broker, not a single-company salesperson.

The fastest test

Ask one question. “If this carrier declines the account or won't add the endorsement, what's the next market?” If the answer is silence, delay, or “there isn't one,” the contractor doesn't have meaningful market access.

That distinction matters even more for growing firms. New equipment, hired autos, subcontractor use, design-build responsibilities, and public work requirements all create pressure points. The wrong insurance relationship turns each one into a scramble. The right broker handles them as part of normal account management.

Five Key Advantages of an Independent Broker for Your Trade

A contractor shouldn't hire a broker for a nice presentation. A broker should produce outcomes. Better fit. Better paperwork. Better positioning before a claim. Better help when one hits.

Broader market access changes what can be insured

Some trades don't fit neat boxes. Restoration firms, concrete cutters, demolition contractors, artisan electricians doing service and small industrial work, and outdoor services contractors with snow exposure often need more than a standard package.

An independent broker can move beyond one-company limitations and, when needed, place tougher exposures through excess and surplus insurance options for contractors. That's how a contractor keeps growing instead of hearing “sorry, that class won't fit.”

A simple example is an HVAC contractor that adds crane picks and larger rooftop units. Standard coverage may stop fitting the operation. A broker with broader access can adjust before a claim or contract problem shows up.

Lower premiums only matter when the structure is right

Price matters. Bad structure costs more.

Construction contractors who use independent brokers typically secure 15 to 20 percent lower General Liability premiums compared to single-carrier direct buyers, and broker-led loss control programs can reduce claim frequency by as much as 25 percent, according to construction insurance data from BMB.

That result comes from better classification, trade-specific risk transfer, and policy wording that matches how the contractor operates. A plumbing contractor with service vans, small commercial tenant work, and some new construction exposure shouldn't be rated and packaged like a firm doing large tract developments.

For fleet-heavy trades, premium pressure often starts with the auto side. Contractors trying to make sense of rate drivers can get useful context from this guide on understanding truck insurance premiums, especially when vehicles, driver quality, and hauling exposures are pushing costs up.

Fast paperwork keeps crews moving

A lot of insurance pain in construction has nothing to do with catastrophe claims. It's admin friction.

- Certificates: A slow COI can delay site access.

- Additional insured requests: Wrong wording can trigger rejection by the GC.

- Waivers and contract review: Miss one requirement, and legal risk shifts back onto the subcontractor.

A drywall contractor doesn't get paid for waiting on paperwork. The right broker treats documents as production tools, not back-office chores.

Bonding access opens larger doors

Many contractors hit a ceiling when private owners or public entities require bonds. Bid bonds, performance bonds, and payment bonds aren't side issues. They determine whether a contractor can pursue larger work.

An independent broker who understands both insurance and surety can help a paving contractor prepare financials, explain work history, and present the account properly. That doesn't guarantee approval, but it puts the contractor in position to compete.

Claims advocacy protects cash flow

A claim is where weak brokers disappear.

Take a masonry subcontractor whose skid steer damages a wall during material handling. The contractor needs immediate reporting, clean facts, and someone who can push the claim forward while operations continue. One practical option in the market is Coverage Axis, which shops multiple carriers for contractors and provides plain-English recommendations built around trade type, crew size, and project mix.

Good claims handling isn't only about reimbursement. It's about protecting schedule, reputation, and the next contract.

Real-World Scenarios from the Job Site

Theory doesn't help much when payroll hits Friday and a claim or certificate issue is blocking the job. Real construction insurance problems usually show up as missed time, lost revenue, or a denied claim.

The electrician with the wrong classification

An electrical contractor handles tenant improvements, service upgrades, and low-voltage access control. The current policy treats the business like it performs a heavier class of high-risk electrical work than it does. The premium stays inflated, and nobody can explain why.

A knowledgeable broker reviews operations line by line. The broker separates the actual work performed from the work the carrier assumed was being done. Payroll and class descriptions are cleaned up. Contract requirements are reviewed, and the insurance program gets aligned with reality.

The outcome isn't flashy. It's better. The contractor stops paying for exposure that isn't there and can explain coverage more clearly when bidding commercial projects.

The roofer with a claim problem hidden in the fine print

A roofing company finishes temporary dry-in work before a storm. Water enters the building. The owner files a claim. Then the carrier points to an exclusion the contractor didn't understand when the policy was sold.

Independent advice matters. A broker who works with roofers doesn't stop at “you have General Liability.” The broker asks where materials are stored, how temporary dry-in is handled, whether subs are used, and what project contracts demand. The broker also explains endorsements and exclusions in language the owner can use in the field.

One related issue often appears in contracts and certificates. If a project owner or GC requires specific status, a contractor needs to understand how an additional insured endorsement works on construction jobs. That endorsement can affect who gets protection under the policy and when.

A policy isn't “good coverage” because it has the right name on the declarations page. It's good coverage when the exclusions match the work and the contract.

The restoration firm locked out of better jobs

A fire and water restoration company wants mold remediation work and larger commercial losses. The current insurance setup handled basic drying jobs, but the new contracts require more specialized liability protection tied to the firm's actual operations.

A strong broker doesn't tell the contractor to stay small. The broker identifies the exposure, explains what has to change, and builds a program that supports the next stage of work. That may include more specialized coverage, revised applications, clearer operational descriptions, and better internal documentation.

The practical win is simple. The contractor can pursue better jobs without hoping the old policy somehow stretches far enough.

Your Checklist for Choosing the Right Broker

Most contractors ask the wrong opening question. They ask, “What's the premium?” The better question is, “Can this broker support the way the company operates?”

That's not a minor distinction. Broker mistakes can hurt a contractor long after renewal day.

Ask about process before asking about price

In Texas, 1 in 5 agents faces Errors & Omissions claims, which is why contractors should ask about internal procedures, market outreach strategy, and trade experience when evaluating a broker, according to the Independent Insurance Agents of Texas resource on agency operations.

That statistic should change the interview immediately. Contractors shouldn't assume every licensed person handles construction details well.

The questions that actually matter

A contractor can use this checklist when reviewing any broker relationship.

- Trade focus: What share of the broker's book is construction, and how much is the contractor's specific trade?

- Carrier access: Which markets does the broker use for roofing, electrical, plumbing, restoration, or other relevant classes?

- Certificate speed: Can the broker show a sample certificate of insurance template used for contractor requests and explain turnaround expectations?

- Claims handling: What happens on day one of a claim, and who stays involved after reporting?

- Contract review: Does the broker review insurance requirements before bid submission or only after the contract is signed?

Look for operational depth

A broker should also be able to answer these practical questions without wandering into sales talk.

| Question | Why it matters |

|---|---|

| Can they explain exclusions in plain English? | Contractors need field-usable answers, not policy jargon |

| Do they understand subcontractor risk transfer? | Poor transfer language can push losses back onto the hiring contractor |

| Can they support growth plans? | New work types often require policy changes before the first job starts |

Contractors buying or expanding firms should think the same way they would in financing. This guide to SBA loan brokers for business acquisition is useful because it shows the same principle. The advisor matters as much as the product when the transaction carries long-term risk.

The right broker should sound like a construction operator who learned insurance, not a script reader who memorized a few coverage names.

Understanding Licensing and Legal Details

A broker's license isn't a decoration on a website. It means the person met state requirements to sell insurance and passed an exam. For a contractor, that's the floor, not the ceiling, but it still matters.

The profession is growing. The U.S. insurance sales agent workforce is projected to grow by 8 percent from 2022 to 2032, and first-time test takers pass the licensing exam at 57.9 percent, according to insurance agent workforce and licensing data. That tells contractors two things. Entry isn't effortless, and a license reflects a basic level of competency.

What licensing means in plain English

A licensed broker should understand policy forms, state rules, and ethical obligations well enough to advise clients lawfully. That doesn't make every broker good at construction. It does mean the contractor should expect a baseline level of training and accountability.

For a contractor, licensing protects against one kind of risk. It doesn't remove the need to check trade knowledge, responsiveness, and process.

Why E and O insurance matters

Errors and Omissions insurance is the broker's professional liability coverage. If the broker makes a mistake, misses a request, or creates a harmful coverage issue, E and O is one layer of financial protection behind that advice relationship.

A contractor should ask whether the broker carries E and O coverage and how the agency handles documentation, endorsement requests, and market submissions. Those aren't nitpicky questions. They show whether the broker runs a disciplined operation or a loose one.

Quick FAQs for Contractors

Contractors usually have a few questions left once the policy talk settles down. These are the ones that matter most in the field.

What's the difference between a surety bond and an insurance policy

A surety bond and an insurance policy are not the same thing. Insurance protects the insured business from covered losses, subject to the policy terms. A bond is a three-party guarantee tied to performance or obligation. If a bonded contractor fails to meet that obligation, the surety may respond and then seek repayment from the contractor.

That's why bonding capacity says a lot about a contractor's financial credibility, not just insurance placement.

How does an independent broker get paid

In many placements, the broker is compensated through commission built into the premium. That doesn't mean every broker delivers the same value. A weak broker and a strong broker can be paid through the same structure while producing very different outcomes for the contractor.

The contractor should still ask whether any fees apply and what services are included, especially for policy changes, certificates, and claims support.

When should a contractor switch from the current agent

A switch makes sense when the current relationship keeps creating friction. Common warning signs include:

- Slow certificates: Jobs stall because COIs don't arrive when they're needed.

- Unexplained premium jumps: The contractor gets a bigger bill with no clear operational reason.

- Poor trade fit: The agent can't explain roofing, restoration, hauling, subcontractor use, or mixed operations.

- Growth resistance: Every new service line gets treated like a problem instead of a normal business decision.

Contractors focused on growth should treat insurance the same way they treat sales and estimating. Strong lead flow matters, and this guide on effective lead generation for businesses is a useful reminder that operational growth only works when back-end systems, including insurance, can support the jobs being won.

A contractor doesn't need an insurance person who's merely available. The contractor needs one who can keep up with contracts, crews, vehicles, claims, and changing scopes of work.

Contractors who want a free quote or a coverage review can talk with Coverage Axis about General Liability, Workers Compensation, Commercial Auto, Inland Marine, Umbrella, bonds, and trade-specific coverage built around actual job exposures. A short review can uncover contract problems, coverage gaps, classification issues, and paperwork bottlenecks before they cost the next job.