A contractor is ready to land a bigger job. The crew is lined up, the schedule works, and the bid is sharp. Then the project owner kicks back the certificate of insurance and says the standard liability policy won't do. They want excess and surplus insurance.

That moment catches a lot of contractors off guard, especially roofers, demo crews, and specialty subs moving into larger or more hazardous work. A high-rise roofing contractor sees it often. The work is above grade, wind exposure is real, pedestrian injury potential is higher, and the owner wants broader protection or higher limits than the standard market is willing to offer.

For a contractor trying to keep jobs moving, this doesn't feel like an insurance lesson. It feels like a roadblock to revenue. That's why it helps to understand where excess and surplus insurance fits, what it solves, and where it creates extra risk that needs careful review. Contractors sorting through broader insurance requirements can also get context from this overview of what insurance contractors need.

Table of Contents

- Your First Encounter with E&S Insurance

- What Exactly Is Excess and Surplus Insurance

- Admitted vs E&S Markets A Clear Comparison for Contractors

- Why Contractors Get Sent to the E&S Market

- How to Secure an E&S Insurance Policy

- Key E&S Policy Terms Contractors Must Understand

- Your Checklist for Reviewing an E&S Policy

Your First Encounter with E&S Insurance

A roofing contractor bidding on a downtown high-rise usually thinks about staging, crane access, fall protection, weather delays, and crew coordination. Insurance often feels routine until the owner's risk manager says the job needs coverage from the excess and surplus market or needs terms that only that market will provide.

That request usually sounds vague at first. The contractor hears “non-admitted,” “specialty market,” or “hard-to-place risk,” and none of that helps when a contract is waiting for signatures. What matters is simpler. The project has risk characteristics that standard insurance carriers either won't take or won't take on terms the owner requires.

For a high-rise roofer, that can mean height, hot work, waterproofing exposures, or limit requirements tied to a large commercial project. The contractor hasn't necessarily done anything wrong. The job is just outside the comfortable lane of the standard market.

The first surprise for most contractors isn't the premium. It's finding out that bigger jobs often come with insurance requirements that operate by a different set of rules.

A second surprise is timing. E&S placement can take more explanation, more underwriting detail, and more review of exclusions than a routine renewal for a small retail tenant build-out. If a contractor waits until the owner rejects the COI, the schedule gets tight fast.

That's why excess and surplus insurance matters to growing contractors. It isn't niche trivia. It's often the bridge between smaller, predictable jobs and larger, more demanding work.

What Exactly Is Excess and Surplus Insurance

Excess and surplus insurance sits in the nonadmitted market. It's used when admitted carriers can't or won't write a risk, especially for nonstandard, unique, or capacity-driven exposures such as high-hazard contractors, adverse loss histories, or risks needing higher limits than the standard market will provide, according to AgentSync's explanation of excess and surplus lines insurance.

Think specialty supply house, not big-box store

The easiest way to understand it is through a construction buying analogy.

An admitted carrier is like a big-box supplier. It carries standard materials for common jobs. The pricing structure is more fixed, the product shelf is more standardized, and it's built for predictable demand.

An E&S carrier is more like a specialty supply house. It handles unusual specs, tougher applications, and one-off needs that don't fit normal inventory. That flexibility is exactly why contractors use it, but it also means the buyer has to read the order sheet more carefully.

A demolition contractor using explosives is a clean example. Standard carriers may refuse the exposure entirely. An E&S carrier may consider it, structure a policy around it, and price it according to the actual risk instead of forcing it into a standard template.

Why contractors end up here

The E&S market exists because real jobs don't always fit standard underwriting boxes. Roofing on occupied high-rises, wildfire mitigation, environmental remediation, heavy structural retrofit work, and large limit demands can all push a contractor outside the standard lane.

That doesn't make the contractor uninsurable. It means the risk needs a carrier willing to write custom terms.

For trade businesses trying to tighten their broader liability program, this article on how to protect your plumbing business from claims is a useful reminder that trade-specific liability issues rarely fit generic policy assumptions.

Practical rule: If the job, the trade, the claims history, or the required limits look unusual, expect a closer look from underwriters and a higher chance the placement moves into the E&S market.

Contractors reviewing general liability options alongside E&S placements should also understand the basics of general liability insurance for contractors.

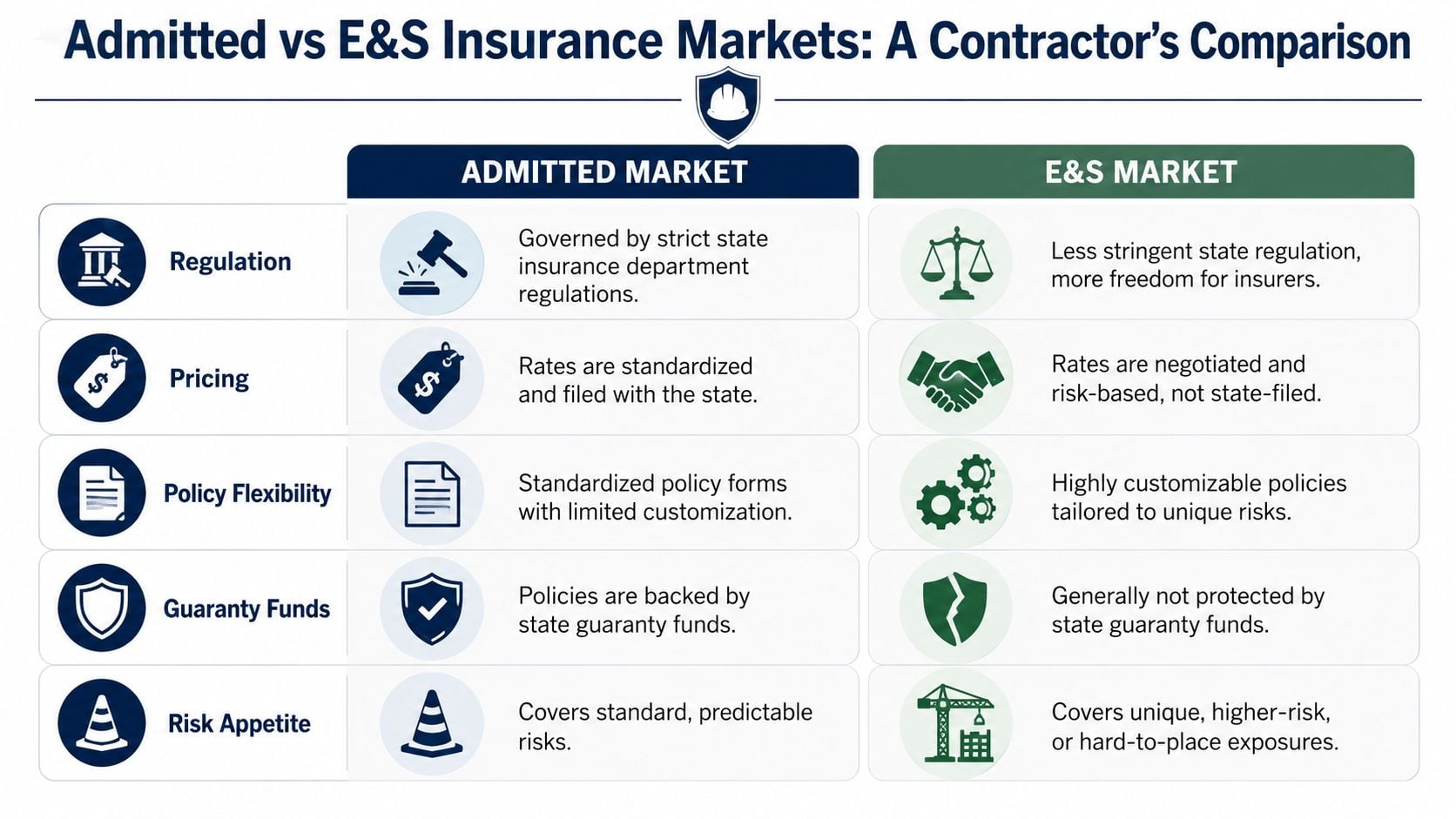

Admitted vs E&S Markets A Clear Comparison for Contractors

A contractor deciding between admitted and E&S coverage shouldn't think in terms of good versus bad. Instead, the question is which market can handle the risk and on what terms.

For an HVAC contractor working on a refrigerated warehouse, the issue might be capacity. The standard market may stop at a lower liability limit than the owner or lender requires. An E&S carrier may be willing to build the limit structure the project needs. That flexibility can keep the job alive.

The trade-off is important. Surplus lines carriers have more latitude in pricing and coverage design, but policies generally don't benefit from state guaranty funds if the insurer becomes insolvent, as explained by IRMI's definition of excess and surplus lines insurance.

What changes for a contractor

A standard admitted policy tends to be more familiar. Forms are more standardized. Rates are filed through the regulatory system. There's more built-in uniformity.

An E&S policy is different. The carrier often has more room to shape wording, set conditions, add endorsements, and price for the exact exposure in front of it. That can be a major advantage when a contractor needs a solution the standard market won't provide.

But that same flexibility means the contractor can't assume one policy reads like another. The paper matters more.

Admitted vs E&S Insurance at a Glance

| Feature | Admitted Standard Market | Excess & Surplus E&S Market |

|---|---|---|

| Regulation | State-regulated with approved policy and rate structures | More flexibility in form and pricing |

| Policy design | More standardized | More customizable |

| Best fit | Common, predictable risks | Unique, higher-risk, or hard-to-place exposures |

| Financial backstop | Generally includes state guaranty fund protection | Generally no state guaranty fund protection |

| Contractor takeaway | Easier to compare, less tailored | Better problem-solving, needs tighter review |

What works and what doesn't

What works is using the admitted market whenever the contractor's operations fit it cleanly and the project requirements are achievable there. That usually means simpler review, more standard language, and fewer surprises.

What doesn't work is forcing a complicated risk into a standard policy just because the label feels safer. If the form excludes the very operations the contractor performs, the “safer” market doesn't help much.

For contractors, the best policy isn't the one with the familiar label. It's the one that actually matches the work being performed.

For the HVAC warehouse example, the practical question isn't “Which market sounds better?” It's “Which market gives the right limit, the right wording, and a financially sound carrier behind it?”

Why Contractors Get Sent to the E&S Market

Most contractors don't wake up and ask for E&S coverage. They get pushed there by the realities of their work.

A roofing contractor on high-rise projects may have clean operations and still land in the E&S market because the work itself carries a hazard profile standard carriers don't like. A brand-new general contractor may get sent there for the opposite reason. There isn't enough operating history to satisfy standard underwriting.

The trade itself can trigger it

Some classes of work routinely draw more scrutiny.

- Roofing work: Height, water intrusion, and completed operations exposure make underwriters cautious.

- Demolition and structural tear-out: Collapse potential, neighboring property damage, and debris hazards raise the stakes.

- Welding and hot work: Fire exposure changes the risk profile fast.

- Environmental or remediation operations: Pollution-related exposure often pushes standard carriers out of the picture.

A contractor's marketing can influence the kinds of projects that come in, which then affects insurance placement. Firms trying to attract larger or more specialized work often benefit from a stronger digital presence, and this guide to contractor marketing helps explain that side of growth.

The project can be the problem

Sometimes the contractor is fine, but the job isn't standard.

A large build may require higher limits than the current carrier will offer. A steep-slope project, coastal exposure, wildfire-adjacent work, or specialty materials can all make an otherwise insurable contractor harder to place in the admitted market.

An HVAC contractor taking on a cold-storage facility, for example, may face contractual requirements that create a broader liability picture than normal tenant improvement work.

History and business stage matter

Claims history changes the conversation. So does a recent cancellation, lapse, or major operational change.

A new venture often faces the same issue from the opposite side. There's no long track record to review. A new general contractor with no prior completed projects may start in the E&S market because underwriters want more evidence before offering standard terms.

Contractors should also understand where contract language increases exposure. This explanation of contractual liability helps connect insurance placement to indemnity obligations that show up in real agreements.

A move into the E&S market isn't always a red flag. Often, it's just the market's way of pricing uncertainty, unusual operations, or larger exposure.

How to Secure an E&S Insurance Policy

Buying E&S coverage isn't a quick online checkout. It's closer to assembling a custom submittal package for a demanding owner. Better information usually produces better terms.

A landscaping contractor that expands into wildfire fuel reduction is a good example. The operation has changed. The exposure has changed. The broker now has to present the business in a way that makes sense to specialty underwriters.

Who does what

The contractor provides the raw job information. That includes operations, payroll split, subcontracting details, project types, safety controls, prior losses, and upcoming contracts.

The retail agent gathers and organizes that information. Then a wholesale or surplus lines broker accesses the E&S carriers that can underwrite the risk. That extra layer is normal in this market.

The insurer underwrites from there. If the risk is acceptable, the carrier issues terms, endorsements, conditions, and pricing specific to that account.

What the process usually looks like

- Contractor submission: The contractor turns over accurate details about work performed, where it's performed, and how it's controlled.

- Market search: The broker checks whether the standard market can take the account and documents the outcome where required.

- E&S approach: A wholesale broker markets the risk to eligible surplus lines carriers.

- Quote review: The contractor and broker review exclusions, endorsements, deductibles, and reporting requirements.

- Binding and compliance: The policy is bound, taxes and filing requirements are handled, and certificates are issued.

A contractor should expect surplus lines taxes and stamping-related charges in many placements. Those costs are part of the structure of the market and shouldn't come as a surprise at binding.

What helps and what slows things down

What helps is detail. Clear subcontractor controls, written safety procedures, updated loss runs, and accurate revenue by operation all improve the submission.

What slows things down is vague job descriptions. “General construction” isn't enough if the company does torch-down roofing, structural steel erection, or wildfire mitigation.

Contractors who are also trying to meet owner or licensing requirements should understand the broader process of getting bonded and insured.

The cleaner the submission, the better the broker can negotiate. In the E&S market, missing details often turn into broader exclusions or tougher pricing.

Key E&S Policy Terms Contractors Must Understand

The policy form matters more in E&S than many contractors expect. A roofer may think the hard part was finding a carrier willing to quote. Often the harder part is making sure the quote covers the work.

That's especially true in high-hazard trades where policy wording can differ sharply from one carrier to the next.

Named peril versus all-risk

Many claim disputes start because IRMI data shows that 64% of contractors in high-risk trades misunderstand the named peril limitation in E&S policies, leading to denied claims for unlisted perils like wind-driven rain or acid rain corrosion in situations where standard all-risk forms often respond differently, according to IRMI.

For a commercial roofer, that misunderstanding can get expensive fast. If the policy only covers listed causes of loss and the damaging event isn't listed, the carrier may deny the claim. The contractor may have assumed “storm damage” was enough. The wording may say otherwise.

Claims-made versus occurrence

Contractors also need to know when a policy is triggered.

An occurrence policy generally ties coverage to when the loss-causing event happened. A claims-made policy generally ties coverage to when the claim is made and reported under the policy terms. For long-tail construction liability, that difference can matter years after a project wraps.

A contractor doing envelope work, waterproofing, or specialty coatings should never treat that distinction as technical clutter. It affects whether a future claim lands inside or outside the policy.

“Covered” isn't a feeling. It's a function of trigger language, exclusions, endorsements, and reporting rules.

Exclusions that hit trades hard

Common E&S restrictions often show up in endorsements rather than bold warnings on page one.

- Residential exclusions: A contractor may be covered for commercial work but not apartments, condos, or mixed-use buildings.

- Height limitations: A policy may cap covered operations above a certain number of stories.

- Material or method exclusions: Torch-down roofing, EIFS, exterior waterproofing, or certain remediation methods may be carved out.

- Subcontractor conditions: Coverage may depend on written contracts, additional insured status, or proof that subs carry their own insurance.

Additional insured wording also deserves attention, especially when contracts shift risk downstream. Contractors dealing with owner and GC requirements should understand the role of an additional insured endorsement.

Your Checklist for Reviewing an E&S Policy

Contractors don't need to become underwriters. They do need to ask sharper questions before binding coverage. A short review meeting can prevent a bad surprise after a loss or during contract compliance.

A high-rise roofing contractor should review the policy the same way the crew reviews a roof plan before tear-off. The dangerous part is usually the detail that got skipped.

Questions worth asking before binding

- Carrier strength: Ask for the carrier's financial strength rating and ask what that means in practical terms.

- Coverage trigger: Confirm whether the policy is claims-made or occurrence.

- Top exclusions: Ask the advisor to point out the three exclusions most likely to affect that specific trade.

- Project fit: Verify that the actual operations, heights, materials, and job types are contemplated by the form.

- Cost details: Ask for a breakdown of premium, surplus lines taxes, and other policy fees.

- Claim handling: Ask how claims are reported, who receives notice, and how quickly reporting must happen.

What a good review sounds like

A solid review is direct. It answers plain questions in plain language. It doesn't rely on “that's standard” or “that's probably fine.”

If a contractor asks whether interior water damage from a storm during a roofing job would be covered, the answer should come from the form, not from guesswork.

Bottom line: Excess and surplus insurance can be the right tool for a hard-to-place contractor, but only if the policy is reviewed with the same care given to a high-risk jobsite.

If a contractor needs a free quote or a no-obligation coverage review for a hard-to-place risk, Coverage Axis can help review the current policy, identify trade-specific gaps, and shop options built for the work being performed.