A bid looks good until the paperwork shows up.

A general contractor sends over a commercial build-out package. The scope fits the crew, the schedule is workable, and the pricing is close. Then the requirements page lands in the inbox. It asks for a performance bond, general liability with specific limits, workers' compensation, commercial auto, and certificate wording that has to match the contract. That's the point where many contractors stop asking whether they should get bonded and insured and start asking how do I get bonded and insured without losing the job.

The confusion usually starts because those two items get lumped together as if they're one purchase. They aren't. One is about proving that the contractor can meet an obligation. The other is about protecting the business when something goes wrong on or around the jobsite. If a new plumbing contractor is trying to get licensed, the bond question may come first. If a roofing company is hiring more field staff and adding trucks, the insurance side gets more complicated fast.

Contractors who handle this well treat it like two tracks moving at the same time. The bond gets the business through the licensing or contract requirement. The insurance program keeps the company operating when a claim hits, a vehicle is involved in a crash, or a customer asks for proof of coverage before work starts.

Table of Contents

- Why “Bonded and Insured” Is More Than Just a Sticker

- Bonded vs Insured What Contracts and Licenses Really Demand

- Your Step-by-Step Guide to Getting a Surety Bond

- Assembling Your Commercial Insurance Program

- Decoding the Costs Timelines and Underwriting Process

- Your Contractor Checklist for Getting Bonded and Insured

Why “Bonded and Insured” Is More Than Just a Sticker

A van decal that says “bonded and insured” sounds like a trust signal. In practice, it's paperwork that decides whether a contractor can pull a permit, satisfy a license board, or submit a compliant bid.

For a drywall subcontractor on a tenant improvement job, that phrase can mean two separate document requests from two separate decision-makers. The owner or public entity may require a bond tied to the work. The general contractor may also require certificates showing liability, workers' comp, auto, and endorsement wording that matches the subcontract. Contractors who treat those as the same thing usually find out they aren't when a bid gets kicked back.

The paperwork exists for a reason

Bonding and insurance solve different business problems. A bond answers the question, “Will this contractor fulfill the obligation?” Insurance answers the question, “What pays when there's an accident, injury, or covered property loss?”

That's why the first move isn't shopping blindly. It's identifying the exact requirement in the license application, prime contract, subcontract, or public bid package. A contractor reviewing common construction coverage types will usually see quickly that the bond requirement and the insurance requirement sit in different parts of the risk picture.

Practical rule: If the paperwork names an obligee, asks for a bond form, or references statutory or contract compliance, that's a bonding issue. If it asks for a certificate of insurance, additional insured wording, or evidence of workers' comp, that's an insurance issue.

Where contractors lose time

A small electrical contractor often runs into this on municipal work. The license board wants one thing. The project owner wants another. The GC wants certificates before mobilization. None of that gets solved by telling clients the business is “fully covered.”

What works is reading the requirement line by line, then handling the bond track and insurance track in parallel. That approach keeps licensing from stalling and keeps the field crew from waiting on paperwork while a start date slips.

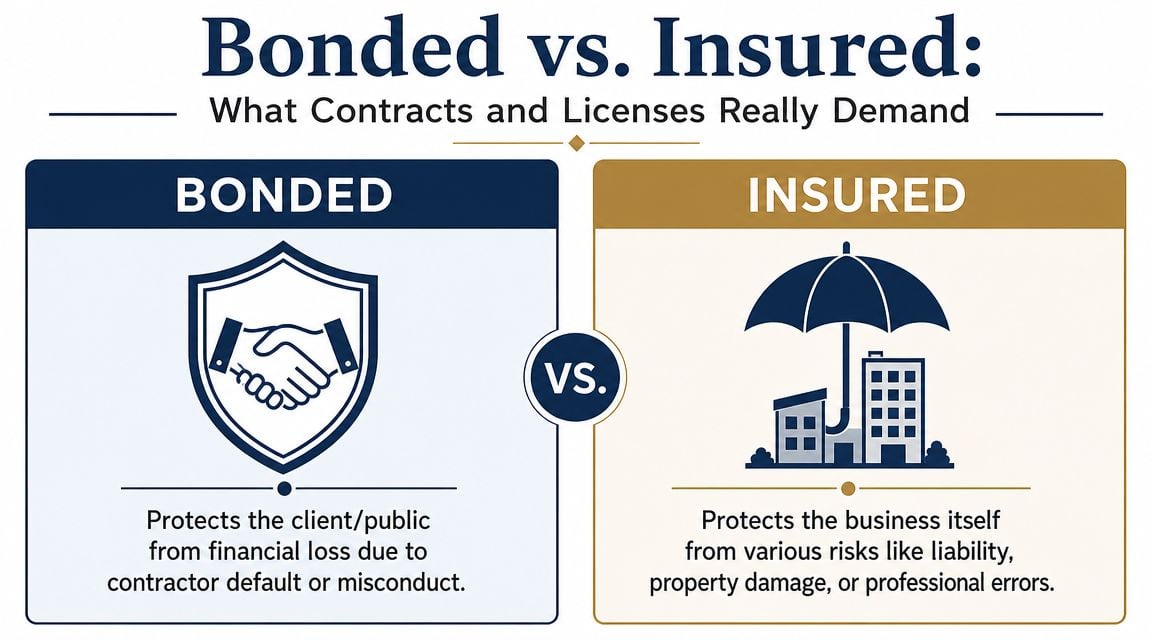

Bonded vs Insured What Contracts and Licenses Really Demand

Surety bonds are not insurance in the normal sense. They're a three-party guarantee among the contractor, the obligee (client or project owner), and the surety. In practice, bonding is often a prequalification step for work, while insurance is the ongoing risk-transfer layer that covers jobsite incidents like injury, vehicle loss, or property damage, as explained in this bonded versus insured overview.

Who each one protects

A bond is primarily there for the party requiring it. If the contractor doesn't meet the obligation, the obligee has a path to recovery under the bond terms. That's why bonds show up in licensing, public work, and customer contracts.

Insurance protects the business against covered losses. If a plumber opens a wall, solders a connection, and a fitting later fails and causes water damage, that's the kind of event contractors look to insurance to handle, subject to policy terms. The bond for that same plumber would usually be tied to a legal or contract obligation, not the water claim itself.

For firms that manage larger scopes, insurance also needs to fit the actual operation. A GC handling remodels, framing, and subcontracted MEP work has different exposures than a solo handyman. Contractors who want a trade-specific view of those exposures often start with this page on insurance for general contractors.

What contracts usually care about

The contract rarely uses “bonded and insured” as a loose phrase. It usually asks for exact items.

| Requirement type | What it usually means in practice |

|---|---|

| License bond | Needed to satisfy a licensing rule for a trade or business activity |

| Bid bond | Tied to submitting a qualifying bid for a project |

| Performance or payment bond | Tied to completing work and meeting contract obligations |

| General liability certificate | Proof of liability coverage for third-party injury or property damage |

| Workers' compensation proof | Evidence the contractor is meeting employee injury coverage requirements |

| Commercial auto certificate | Proof vehicles used in the business are insured |

A common mistake is assuming the bond replaces the insurance. It doesn't. The contract may require both, and they serve different purposes.

A trade example that makes it clear

Take an electrician opening a new shop. The state or locality may require a license bond before the business can legally operate in that trade. Separately, a commercial customer may refuse site access until the electrician provides proof of liability coverage and workers' compensation.

That's why asking “how do I get bonded and insured” as if it's one transaction usually creates delays. The faster question is, “What exact bond is required, and what exact insurance proof does this owner or GC want?”

Your Step-by-Step Guide to Getting a Surety Bond

A surety bond goes smoother when it's treated like a prequalification file instead of a quick online form. The surety wants to see whether the principal can meet the obligation, which is why paperwork quality matters.

For a new HVAC contractor, the bond may be a license or permit bond. For a sitework contractor bidding a public job, it may be a bid bond first, followed by performance and payment bond requirements if the award comes through. Those are different requests, and the surety will evaluate them differently.

Start with the exact bond requirement

Many public and private contracts require bid, performance, and payment bonds, and the SBA's Surety Bond Guarantee program is aimed at helping small businesses qualify. The practical issue isn't just getting bonded. It's identifying which bond fits the job and what contract value, credit, and capacity standard applies, as outlined by the SBA surety bond program.

Before any application starts, verify these items with the agency, owner, or contract administrator:

- Correct bond type: License bond, bid bond, performance bond, payment bond, or another required form.

- Exact obligee name: The legal entity on the bond has to match the requirement.

- Bond amount and form: A wrong amount or wrong form can trigger rejection.

- Filing instructions: Some obligees want the original executed bond, others have specific filing steps.

Contractors who want a plain-language reference on bond types and costs for contractors often find it useful before sending documents to a surety.

Build the file the underwriter actually needs

The surety usually wants business registration details, EIN information, owner identity, and current financials. On larger contract bonds, the review often gets deeper because the surety is looking at credit strength and capacity to perform.

That's why sloppy submissions create avoidable problems. If the legal name is inconsistent between the license record, W-9, and bond request, the obligee may reject the bond even if the surety approves it.

Field advice: The fastest bond file is the one with matching names, matching addresses, signed forms, and a clear explanation of the work.

A practical sequence often looks like this:

- Confirm the requirement with the agency or project owner.

- Apply through a licensed surety or bond provider.

- Complete underwriting and answer follow-up questions quickly.

- Pay the premium after approval.

- Review the executed bond before filing it.

- Submit it exactly as instructed by the obligee.

What works and what doesn't

What works is sending complete information early, especially when a bid deadline or license issue date matters. What doesn't work is guessing at the bond form, submitting an abbreviated business name, or assuming the surety will fix missing contract details after the fact.

A contractor looking for a direct path to this coverage can review surety bond options for contractors. The main point stays the same. Bonding is paperwork-driven, and precision matters more than speed alone.

Assembling Your Commercial Insurance Program

A drywall crew backs a truck into a client's brick column on Monday. On Wednesday, an employee strains his shoulder unloading sheets. Friday, a miter saw goes missing from the trailer. None of those problems call for a bond claim. They call for the right insurance program, set up before the first certificate request lands in your inbox.

That is the part many newer contractors miss. Bonding and insurance move on parallel tracks. The bond satisfies a license board or project owner. Insurance protects the business when day-to-day field work causes injury, damage, or loss. If the policies do not match the operation, you can still lose a job, fail a certificate requirement, or end up paying out of pocket after a claim.

The core coverages most contractors build around

Most contractor insurance programs start with four policy types, but the right setup depends on what happens on your jobsites.

- General liability: This covers third-party bodily injury and property damage, subject to the policy terms. If a plumber's apprentice cracks a finished tile floor or a visitor trips over extension cords, this is usually the first policy involved. Contractors reviewing limits, exclusions, and common endorsements often start with general liability coverage for trade businesses.

- Workers' compensation: This covers employee injuries under state law. If you have field labor, this is often tied directly to legal compliance, payroll reporting, and certificate requirements from general contractors.

- Commercial auto: Work trucks, vans, and dump vehicles need business auto coverage. A personal policy often will not respond the way a contractor expects once the vehicle is used for hauling tools, towing equipment, or moving crews.

- Inland marine: This covers tools, mobile equipment, and materials in transit or at temporary locations. It matters for trades that move value from site to site, such as electricians, framers, and flooring installers.

The right mix depends on the trade

A one-van handyman operation does not need the same structure as an excavation contractor with multiple drivers, trench exposure, and owned equipment. A painter using sprayers has different underwriting questions than a finish carpenter working mostly indoors. A GC using many subcontractors needs close attention on certificates, additional insured status, and how subcontractor agreements shift risk.

Some contractors also cross into advice, design, or specification work. That exposure does not fit neatly inside standard general liability. If the business recommends systems, prepares plans, or gives technical direction tied to the job, this guide to professional indemnity helps explain where professional liability starts to matter.

Insurance works best when the application matches the work. Describe the actual trade, the tools on the truck, the payroll in the field, the vehicles on the road, and the jobs you subcontract.

Cheap paper can create expensive gaps

I see this problem often with growing trade businesses. A contractor buys the lowest-priced package, then finds out the payroll was understated, the trailer was never scheduled, or the carrier was told there was no subcontracted labor. The certificate looks fine until a claim or contract review exposes the mismatch.

A better approach is to build the program around how the company earns money. Start with payroll, vehicle use, tools and equipment, subcontractor use, and the type of property you touch. Then check those details against the contracts you sign and the certificates you have to issue.

One option contractors use for that process is Coverage Axis, which places contractor insurance and surety through a licensed advisory process. The true value is not the logo on the certificate. It is getting paperwork that matches the work you perform every day.

Decoding the Costs Timelines and Underwriting Process

Cost questions are fair. So are timeline questions. The trouble starts when contractors expect bonding and insurance to move at the same speed or price the same way.

Surety bonds are usually priced as a percentage of the bond amount, commonly ranging from 1% to 15% depending on credit and bond type. A $50,000 contract bond may start around $500 annually for a well-qualified applicant, according to this bond cost explanation for small businesses and contractors.

What drives bond pricing

A surety is looking at the applicant's ability to perform and repay if a claim is paid. That's why credit, financial history, and documentation matter so much.

For a small license bond, the process may be fairly light. For a contract bond tied to a meaningful project, the underwriting review can become more detailed because the surety is evaluating capacity, not just identity.

A practical example is a concrete contractor bidding a larger foundation package. The surety isn't only asking whether the business exists. It wants to know whether the contractor has the financial strength, organization, and track record to carry the job.

What drives insurance underwriting

Insurance underwriting focuses on exposure. The carrier wants to understand what the business does every day, what can go wrong, and how severe a claim could be.

That means applications often turn on details such as:

- Trade operations: A painter doing interior brush-and-roll work presents a different profile than one doing exterior spray work at height.

- Payroll and labor mix: Employee count, class of work, and use of subcontractors affect how the risk is viewed.

- Vehicles and drivers: A single pickup is different from a fleet with trailers and multiple operators.

- Loss history: Prior claims shape how the underwriter views current controls.

A fast quote still depends on accurate information. When payroll, vehicle schedules, and job descriptions are incomplete, the process slows down or the quote comes back wrong.

What contractors can control

They can't control every underwriting decision. They can control how complete the submission is.

Financials that are current, applications that match the actual operation, and contract requirements that are sent up front all help. The same is true on the insurance side when the business provides clean vehicle lists, realistic payroll, and a truthful description of work at height, subcontracted labor, or equipment use.

Your Contractor Checklist for Getting Bonded and Insured

Contractors who move through this efficiently don't treat it as one errand. They run the bond requirement and the insurance requirement side by side, then make sure the final documents match the contract language.

The practical workflow is to separate surety from insurance and buy both in parallel. First identify state or industry requirements, purchase the surety bond, then place needed insurance lines like general liability and workers' comp, ensuring all documents match the obligee's wording exactly, as described in this small-business bonding and insurance workflow guide.

The checklist that keeps jobs moving

- Verify the exact requirement first: Read the license board notice, bid package, subcontract, or customer contract carefully. Confirm the bond type, bond amount, obligee name, insurance limits, and certificate wording before applying for anything.

- Gather the business file: Pull together legal business name, entity documents, EIN details, owner information, financials, payroll estimates, vehicle schedules, and prior coverage details if they exist.

- Apply for the bond on its own track: Don't wait for the insurance side if the obligee needs a bond to issue the license or award the work.

- Build the insurance program around the operation: General liability, workers' compensation, commercial auto, and inland marine should reflect what the crew does, what they drive, and what they carry.

- Review every final document for matching details: Bond forms, certificates of insurance, additional insured wording, and named insured information should all line up with the contract and the legal entity.

Common last-minute misses

A flooring contractor can do everything right and still lose a day because the certificate shows the wrong entity name. A mason can get the bond approved but have it rejected because the obligee required a specific form. Those aren't underwriting problems. They're document-control problems.

A BOP can also be part of the conversation for some smaller contractors who need a combined approach to certain business property and liability exposures. For firms evaluating that structure, this page on a business owners policy for general contractors can help frame when it fits and when it doesn't.

Get the documents the job actually asks for, not the documents that are easiest to buy.

For contractors still asking how do I get bonded and insured, the shortest accurate answer is this. Confirm the requirement, separate the bond from the insurance, submit complete information, and review every document before it goes out. That's what keeps the license active, the bid compliant, and the crew working.

If a contractor needs a free quote or a coverage review, Coverage Axis can help review bond requirements, insurance certificates, and trade-specific coverage needs before the paperwork holds up a job.