A contractor lands a solid job, opens the subcontract, and gets hit with the same paragraph that shows up on so many projects: indemnify, defend, hold harmless. The scope looks manageable. The schedule is tight but doable. The insurance requirements look familiar. Then that one clause changes the whole risk of the deal.

That's the starting point for what is contractual liability. It isn't an abstract legal term. It's the moment a contractor agrees, in writing, to take on liability that might not have existed without the contract. On a busy construction job, that can mean a framing sub, roofer, plumber, or electrician gets pulled into a claim because of what the contract says, not just because of what happened in the field.

Most generic explainers stop too early. They define contractual liability in broad terms, but they don't answer the question contractors ask at bid time: Will the General Liability policy respond if this indemnity clause gets triggered? That answer usually turns on one phrase inside the policy: insured contract.

Table of Contents

- The Contract Clause That Can Sink Your Business

- What Contractual Liability Actually Means on the Job

- How Your Insurance Policy Responds to a Contract

- Contractual Liability Claims in the Real World

- Your Checklist for Reviewing Any Contractor Agreement

- Common Questions About Contractual Liability Insurance

The Contract Clause That Can Sink Your Business

A framing subcontractor reviews a GC agreement after winning a school addition project. The price is acceptable. The scope is clear enough. Then the indemnity section shows up, packed with legal wording that sounds like standard paperwork until someone reads it closely.

The clause says the framer will defend and indemnify the GC for claims arising out of the work. That sounds routine. Then the wording gets broader and starts reaching toward losses connected to the site, the project, or the acts of others. That's where a profitable job can turn into a risk transfer trap.

Contractors don't need to become lawyers, but they do need to know when a contract stops being administrative and starts moving real liability onto their balance sheet. That's why some firms use outside references to understand how commercial agreements are built before sending them for legal review. A practical primer on mercantile contract insights can help a contractor see how obligations, payment terms, and risk transfer language fit together before the signing rush takes over.

A second problem usually appears at the same time. The same contract that demands indemnity also demands insurance support for the other party. That often includes additional insured status, which is related to contractual risk transfer but isn't the same thing. Contractors who need a plain-English refresher on that issue usually benefit from a guide to additional insured endorsement requirements.

A bad indemnity clause doesn't feel expensive on bid day. It feels expensive after the claim arrives.

For a framing sub, the danger isn't just a fall, a property damage claim, or a suit involving another trade. The danger is signing a clause broad enough that the GC tenders the whole mess downstream. At that point, the contractor isn't just defending workmanship. The contractor is defending a promise.

What Contractual Liability Actually Means on the Job

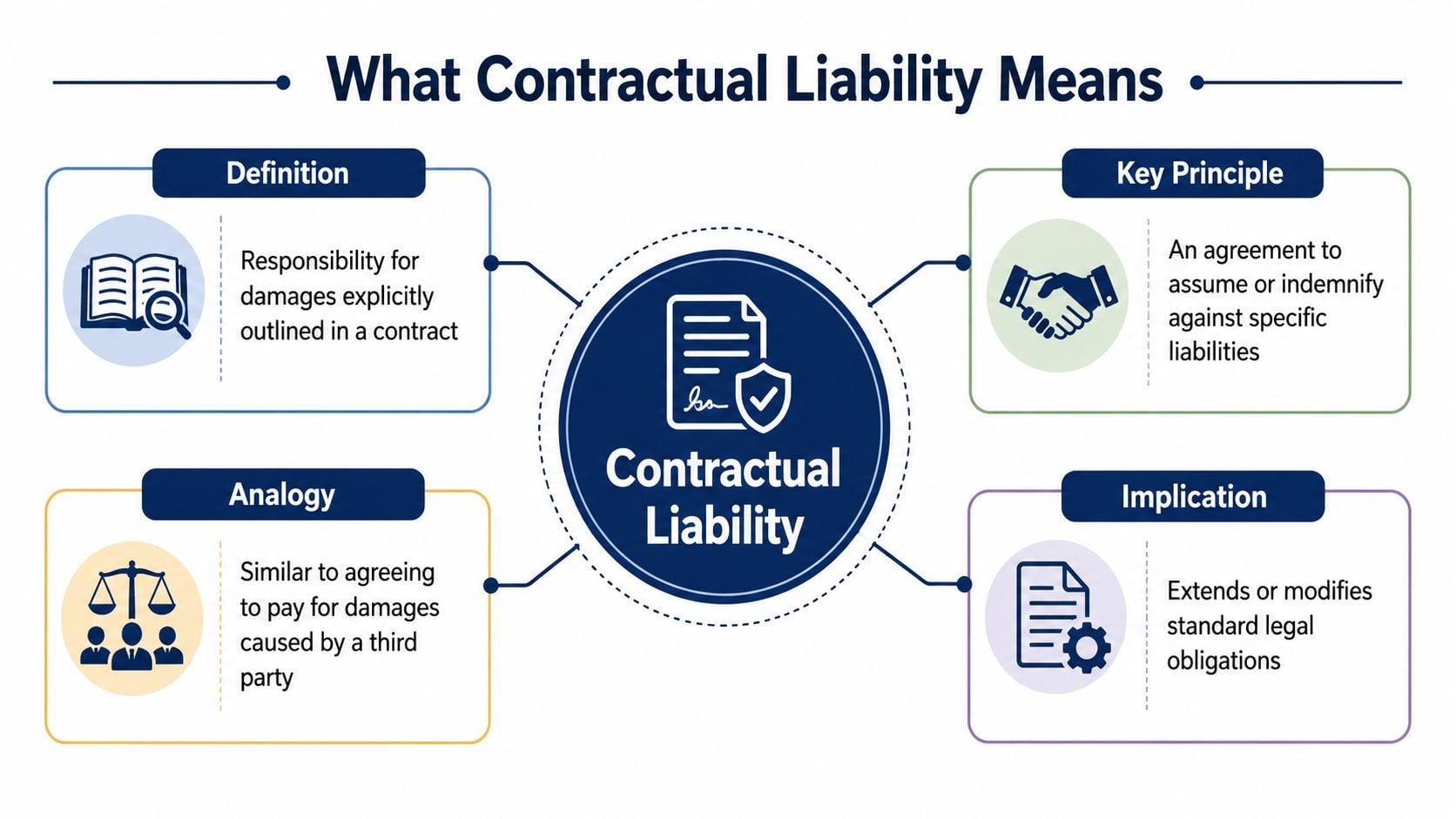

Contractual liability means a business assumes liability through a contract. In plain language, a contractor agrees to be responsible for certain claims because the contract says so.

That's why this coverage topic confuses so many owners. They know General Liability covers bodily injury and property damage claims in a broad sense, but they don't always realize a signed agreement can expand who gets pulled into the claim and why.

The promise matters more than the label

A simple way to think about contractual liability is co-signing risk. A contractor may not have caused the whole loss, but the contract says the contractor will step in and protect someone else against certain claims tied to the job.

For an electrician, that can show up in a subcontract with a broad hold harmless provision. If an electrical fire claim develops and multiple trades get named, the contract may let the GC push part of the defense and indemnity burden back to the electrical contractor. The key point is that the contract can change the liability map.

This doesn't mean every sentence in a contract becomes insured. It means certain assumed liabilities may fit within the policy framework, while others won't.

Where the General Liability policy fits

In U.S. Commercial General Liability forms, contractual liability has been a built-in coverage feature since 1986, and the current structure uses a contractual-liability exclusion with an exception for insured contracts, as explained in IRMI's discussion of contractual liability and the CGL policy. That same discussion notes this protection is generally blanket, which means contractors typically don't have to schedule each contract one by one or buy a separate contractual-liability premium just to access that built-in feature.

That's the part contractors need most. The question usually isn't, “Did the contractor sign a contract?” The question is, “Does this assumed liability fall inside the policy's insured-contract exception?”

Practical rule: Signing a contract doesn't create automatic coverage. It creates a coverage question.

A contractor also has to think about limits. Even when a contract fits the policy structure, low limits can still leave the business exposed. That's why contractors comparing programs should understand general liability coverage limits before agreeing to aggressive indemnity wording in a subcontract or site-access agreement.

The cleanest way to explain what is contractual liability is this: it's liability a contractor takes on by agreement, and the General Liability policy may respond if that obligation fits the policy's insured-contract language. If it doesn't, the signature still binds the contractor even when the policy doesn't.

How Your Insurance Policy Responds to a Contract

The policy response starts with a basic distinction. A contractor's CGL policy may help with certain assumed liabilities in a contract, but it doesn't turn the policy into a catch-all warranty for every contractual promise.

That distinction matters because many owners blend together three different ideas: contractual liability coverage, additional insured status, and waiver of subrogation. They often travel together in construction agreements, but they solve different problems.

Blanket coverage does not mean unlimited coverage

One of the most misunderstood points in construction insurance is the idea of blanket contractual liability. Blanket doesn't mean every clause is covered. It means the contractor usually isn't required to list every subcontract, lease, or access agreement separately for the built-in insured-contract feature to exist.

The real review happens at the claim stage and often starts with the indemnity language itself. As explained in this analysis of insured contracts and contractual liability issues, CGL protection tied to assumed liability does not simply cover every breach-of-contract claim. For contractors, the recurring issue is whether a hold harmless clause qualifies as an insured contract, especially where state anti-indemnity laws can void language that tries to transfer liability for another party's sole negligence.

That's why a roofing subcontractor can't rely on the certificate request alone. The GC may ask for broad indemnity, but if the clause overreaches under state law or falls outside the policy's insured-contract framework, the roofer may still have signed a promise the insurer won't fully support.

Three tools that get mixed together

A roofer on a commercial re-roof often sees all three in one subcontract:

- indemnity language in the contract

- additional insured requirements

- waiver of subrogation requirements

Those aren't duplicates.

| Insurance Tool | What It Does for the Other Party (e.g., GC) | How It Affects You (the Subcontractor) |

|---|---|---|

| Contractual liability within the CGL insured-contract framework | May support certain indemnity obligations you assumed in the contract | Your policy may respond to covered assumed liability, but only if the contract and claim fit the policy |

| Additional Insured endorsement | Gives the other party direct status under your policy for qualifying claims | Your policy may have to defend or protect that party for covered job-related claims |

| Waiver of Subrogation | Limits your insurer's ability to pursue the other party after a paid loss | You give up a recovery path that might otherwise shift money back from the other party |

A contractor who sees all three should read them as a package, not as isolated paperwork. The indemnity clause shifts liability by contract. The additional insured endorsement opens the door for the other party to seek protection under the subcontractor's policy. The waiver changes post-loss recovery rights.

On a certificate request, the insurance language looks routine. In a claim, each requirement does a separate job.

This is also where limits matter again. A subcontractor with thin limits may satisfy the contract on paper and still be underinsured for the obligation assumed. Contractors evaluating whether one limit structure is enough should understand combined single limit considerations when the project brings together auto, site access, and third-party injury exposures that can stack around the same loss.

Contractual Liability Claims in the Real World

The claim usually doesn't start with someone saying “contractual liability.” It starts with a lawsuit, a tender letter, or a demand from the upstream party saying the subcontractor agreed to defend and indemnify them.

Recent underwriting attention has moved beyond prime contracts alone. Businesses take on contractual liability every time they sign agreements with clients, landlords, or independent contractors, and that exposure is growing through vendor and project-site agreements, as outlined in this overview of contractual liability insurance for business agreements.

Landscaping contract at a commercial property

A landscaping contractor maintains sidewalks and entrances at a shopping center. The property manager's agreement includes an indemnity clause tied to slip-and-fall claims arising from the contractor's services.

A visitor slips on an icy walkway after a winter event. The suit names the property manager first because that's who controls the premises from the visitor's point of view. The manager then tenders the claim to the groundskeeping contractor based on the signed contract.

The contractor may have expected to answer for negligent snow or ice work. What catches many owners off guard is how quickly the upstream party uses the contract to shift defense and claim costs downstream.

HVAC water damage after turnover

An HVAC contractor installs a unit in a mixed-use building. Months later, a leak damages flooring and finished space below. The owner, GC, maintenance vendor, and HVAC firm all get named in the dispute.

The HVAC subcontract contains broad indemnity language. Even if the final fault picture is messy, the contractor may still be dragged into defending broader damage allegations because of the contract wording.

That's why this issue can't be treated as just another CGL checkbox. It sits right at the intersection of contract drafting, claim handling, and project risk transfer.

Concrete work and the equipment rental agreement

A concrete contractor rents specialty equipment for a pour. The rental agreement includes hold harmless language and site-use obligations that barely get reviewed because the crew needs the machine that morning.

Later, property damage happens during loading or use near an adjacent structure. The rental company points to the signed agreement. Now the concrete contractor is not just dealing with operations risk on the site. The contractor is dealing with liability created in a vendor agreement.

Some losses in these situations may also involve environmental or cleanup allegations that a standard General Liability form handles differently. Contractors with fuel, runoff, or material release exposure around jobsite incidents should understand when contractors pollution liability insurance becomes part of the bigger risk conversation.

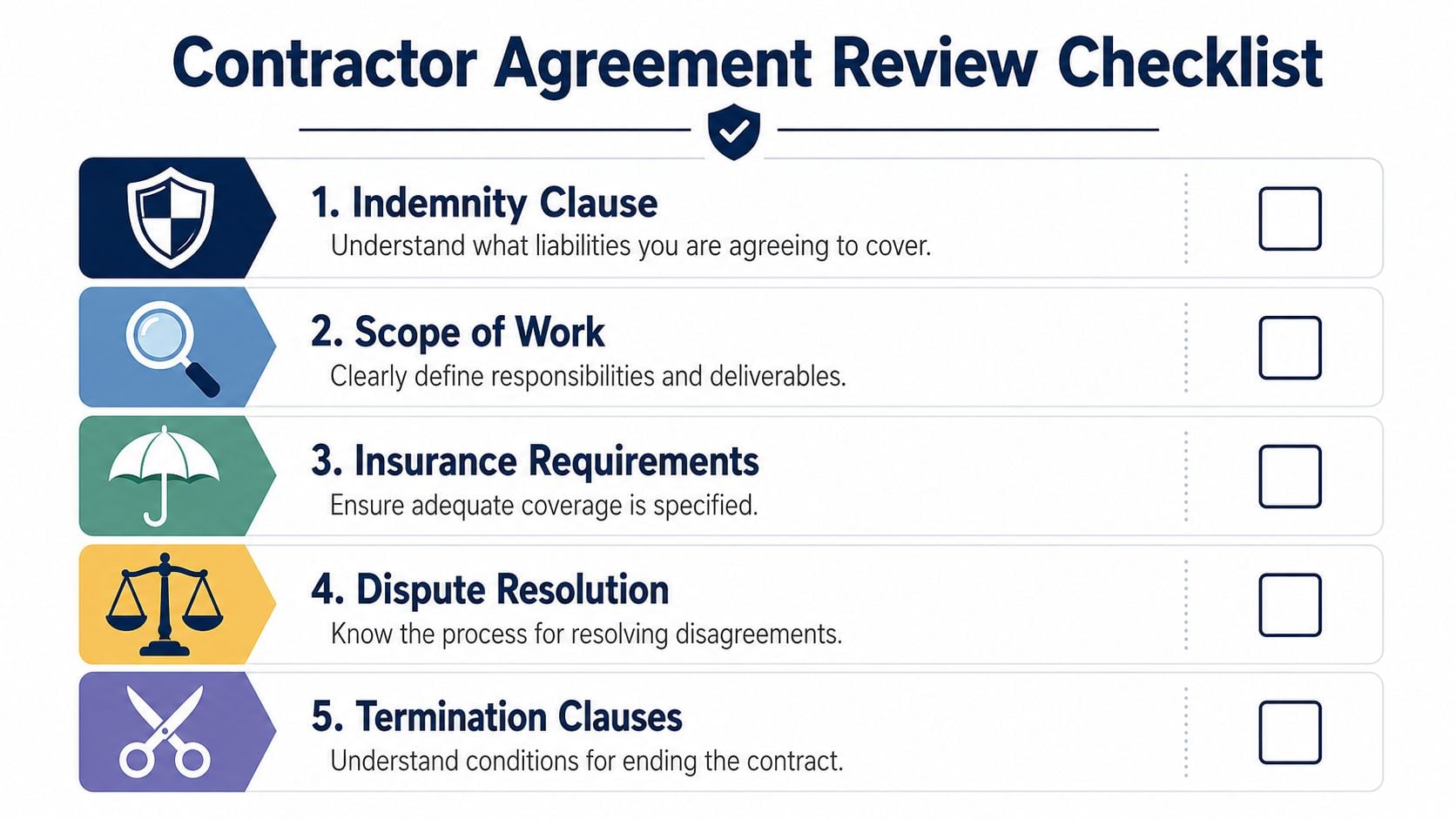

Your Checklist for Reviewing Any Contractor Agreement

Most bad contract outcomes happen because the contractor moved too fast, trusted that the wording was “standard,” or assumed the certificate request matched the actual policy response. A short review process catches a lot of those problems before the signature goes out.

What to scan before signing

Find the indemnity paragraph first. Don't start with payment terms. Start where the contract tells one party to defend, indemnify, or hold harmless another party.

Check how broad the trigger is. Language tied to claims “to the extent caused by” the contractor's work is very different from language tied to “any and all claims arising out of the project.”

Look for sole-negligence problems. If the clause tries to make the subcontractor responsible for the other party's sole negligence, that should stop the review immediately.

Match limits to the risk being assumed. One commercial contracting benchmark is to align risk transfer and insurance limits. If a party assumes $2 million in indemnification risk, it should carry at least $2 million in contractual-liability coverage, according to this discussion of contractual liability risk allocation and mediation clauses. That same discussion notes mediation clauses can reduce dispute-resolution costs by 60% to 80% compared with direct litigation.

Review the insurance requirements separately from the indemnity clause. They interact, but they aren't the same thing.

A plumber on a tenant improvement project should be especially careful with broad wording that says the plumber will indemnify the GC for any and all claims arising on the site. That kind of language can reach far past the plumbing scope.

Language that should slow the deal down

Some contract wording is manageable. Some wording needs to be narrowed before signing.

“Arising out of your work” may be negotiable. “Any and all claims connected to the project” should get a harder look.

Useful review habits include:

- Redline instead of accepting boilerplate: Contractors that negotiate consistently often use simple internal procedures so project managers don't miss risky edits. A guide to effective negotiation workflows can help organize that process before counsel or the agent reviews the final version.

- Ask for narrower indemnity wording: A better clause limits responsibility to the contractor's acts or omissions, or to the extent of that contractor's negligence.

- Check the certificate requirements: The contract may demand endorsements, statuses, or evidence that the carrier hasn't actually issued yet. Contractors can avoid last-minute surprises by reviewing a certificate of insurance template against the subcontract requirements before mobilization.

A short checklist won't replace legal review. It will catch the clauses most likely to create uninsured promises, overbroad defense duties, and disputes over what the subcontractor agreed to insure.

Common Questions About Contractual Liability Insurance

Does this cover bad workmanship

Usually, that's the wrong question for contractual liability. This part of the General Liability discussion is about liability assumed in a contract for bodily injury or property damage claims involving third parties. It isn't the same thing as a guarantee that the contractor's own work was done correctly.

A tile contractor who installs defective work may still have a workmanship problem even if the subcontract contains indemnity language. Contractual liability doesn't turn poor performance into a covered loss by itself.

Is contractual liability the same as breach of contract

No. Breach of contract usually means a party failed to perform as promised under the agreement. Contractual liability, in the insurance sense, usually refers to liability the business assumed in the contract, especially through indemnity or hold harmless language.

That difference matters. A contractor can breach a scheduling obligation, a payment clause, or a completion term, and none of that automatically fits the CGL insured-contract framework.

How is this different from professional liability

Professional liability addresses a different category of exposure. It's generally associated with financial harm tied to design, advice, consulting, or professional judgment. Contractual liability under the CGL discussion is usually about assumed liability for bodily injury or property damage claims.

An electrical design-build firm might need both conversations. The field work creates one set of risks. The design responsibility creates another.

What should a contractor do before signing

Three things.

First, read the indemnity clause before looking at the insurance checklist. Second, confirm whether the obligation appears to fit the policy's insured-contract structure and whether the required endorsements match the contract. Third, stop and get review help when the wording reaches beyond the contractor's own work or pushes liability for another party's sole negligence.

The shortest answer to what is contractual liability is this: it's the risk a contractor accepts by contract, and the insurance question is whether that promise fits the policy language that can support it.

Coverage Axis helps contractors review General Liability programs against real contract demands, including indemnity language, additional insured requirements, waiver requests, and limit adequacy. For a free quote or coverage review, visit Coverage Axis.