A contractor is ready to bid a solid commercial job. The crew is lined up, the pricing is tight, and the scope makes sense. Then the insurance section of the bid package stops everything. It calls for $1,000,000 Combined Single Limit on commercial auto, but the current policy shows 100/300/100 split limits.

That's the moment this stops being insurance jargon.

For a contractor, combined single limit can decide whether a bid goes out on time, whether a certificate gets approved, and whether one fleet accident becomes a bad claim or a business-threatening event. This matters most for trades that live on the road: HVAC, electrical, plumbing, landscaping, roofing, concrete, restoration, and any operation hauling tools, trailers, materials, or crews every day.

Table of Contents

- Why Your Commercial Auto Limit Matters

- What Is a Combined Single Limit

- CSL vs Split Limits The Contractor's Comparison

- How CSL Affects Your Bids and Insurance Certificates

- Real-World Scenarios A Landscaper's Crash

- Choosing Your CSL Amount What Contractors Need

- Get the Right Limit for Your Next Job

Why Your Commercial Auto Limit Matters

An HVAC contractor bidding a maintenance contract for a retail portfolio might have everything ready except one line in the insurance requirements. The owner wants $1,000,000 combined single limit for auto liability. The contractor's renewal shows split limits instead. Same coverage? Close enough? Usually not.

That gap matters because bid compliance is black and white. Either the insurance requirement matches the contract, or it doesn't. If the policy form doesn't fit, the certificate can't accurately state that it does. Contractors lose time trying to patch coverage at the last minute, and sometimes they lose the job entirely.

Commercial auto is easy to overlook because the trucks are already insured and the decals are already on the doors. But for a contractor, the vehicle schedule is tied directly to revenue. If a crew can't drive, materials don't move. If a certificate doesn't clear, work doesn't start. Contractors that want to tighten operations should also learn fleet management from T1A Auto, because safer fleet habits and cleaner vehicle oversight reduce the odds that insurance becomes a problem in the first place.

A contractor reviewing commercial auto coverage for contractors should treat the liability limit structure as a business decision, not an admin detail.

Practical rule: If the bid package asks for combined single limit, don't assume a split-limit policy will satisfy it just because the total premium looks similar.

What this changes on the job side

A plumbing company with two service vans faces a different auto exposure than a paving contractor running heavier units and trailers, but both face the same basic problem. One crash can involve injured people, damaged vehicles, a fence, a storefront, or a highway barrier. The insurance structure controls how those claims get paid.

For contractors trying to grow, combined single limit often becomes the dividing line between small local work and better-paying accounts with formal insurance requirements.

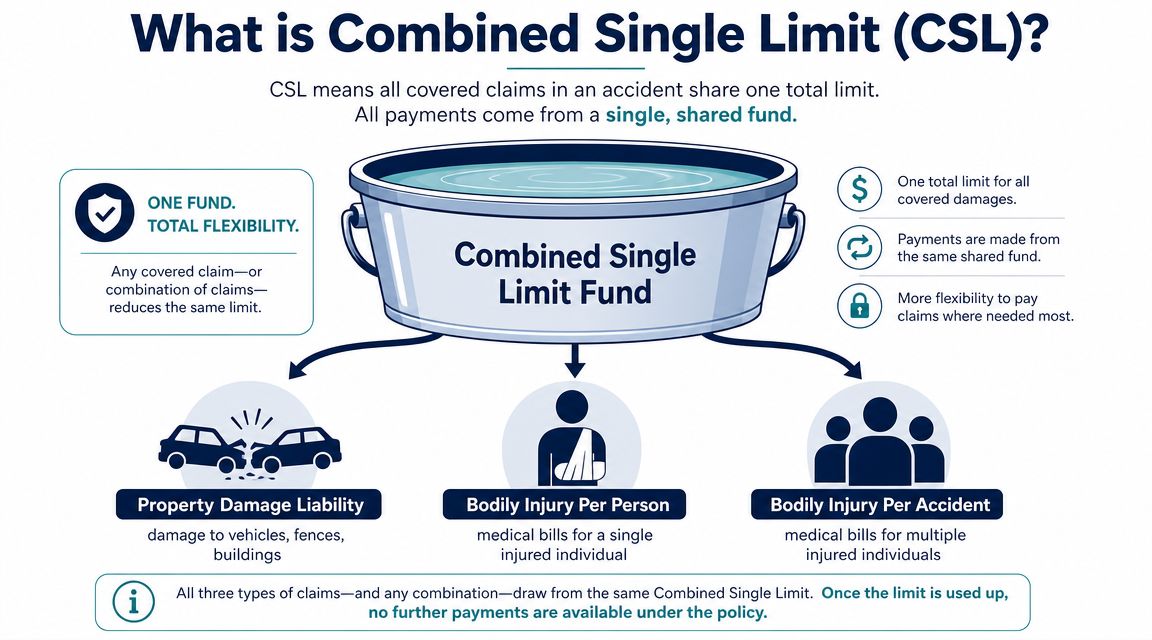

What Is a Combined Single Limit

Combined single limit means the policy uses one pooled dollar limit for liability claims from a single accident. Bodily injury and property damage both draw from that same pool.

That's the simplest way to think about it. One bucket. Not three.

If a contractor's driver causes a wreck that injures people and damages other vehicles or property, the insurer pays from one shared limit until that limit is used up. That gives the claim more flexibility because the loss doesn't have to fit into separate property damage and bodily injury compartments.

Why that structure is real, not marketing language

Combined single limit isn't a catchy phrase invented for sales brochures. It's a recognized liability structure that regulators address directly. In New York, the Department of Financial Services explained that state minimum auto liability protections are $25,000 for bodily injury to one person, $50,000 for bodily injury to two or more persons, and $10,000 for property damage, and that a CSL motor vehicle liability policy with a single liability limit of less than $160,000 still has to be structured so those minimum protections are available.

That point matters because it shows how combined single limit has to be built to satisfy underlying legal requirements. It's not separate from liability law. It's one way a policy is designed to respond to it.

Contractors should think of CSL as flexible money inside a hard ceiling. It gives the claim handler room to allocate payments where the damage actually is, but once the limit is exhausted, the insurer stops paying.

Why contractors care more than ordinary drivers

A painter driving a van to a residential repaint has one level of exposure. A groundskeeper towing a trailer loaded with machines through dense traffic has another. A restoration crew rushing to a water loss after hours adds fatigue, urgency, and equipment weight to the equation.

For contractors, accidents are rarely clean and simple. They often involve multiple people, multiple vehicles, and cargo or attached equipment. Combined single limit can handle that mess more naturally than a policy that separates everything into smaller buckets.

CSL vs Split Limits The Contractor's Comparison

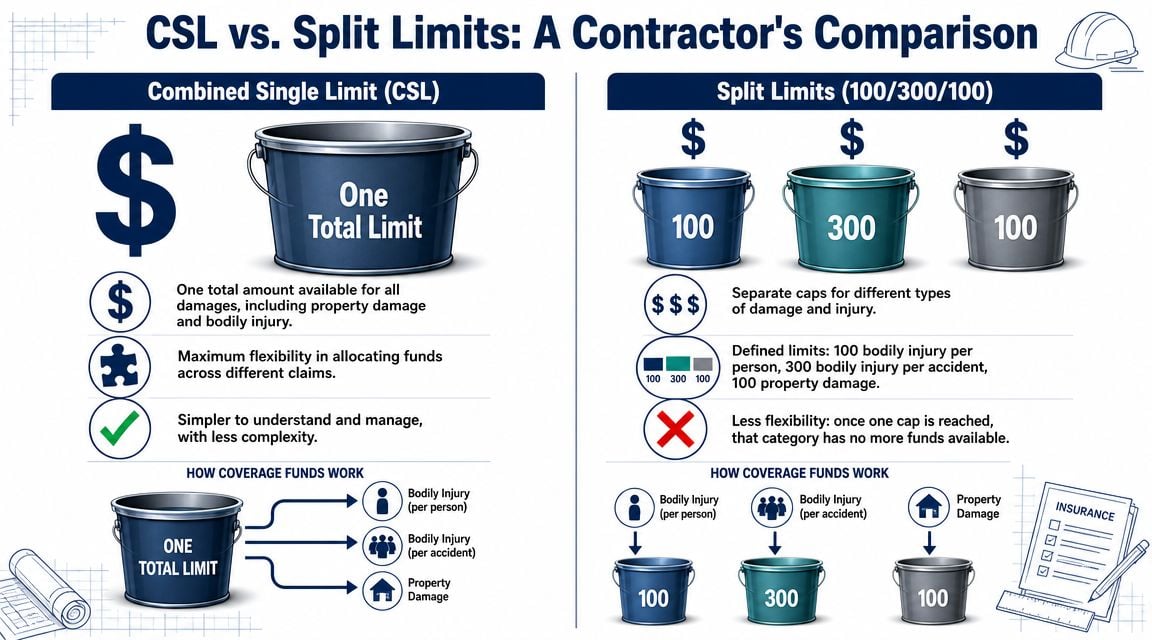

Split limits and combined single limit both provide liability coverage. The difference is how the money is divided before the accident ever happens.

How split limits work

Split limits are usually written as three numbers. A common example is 25/50/25, which means $25,000 per injured person, $50,000 per accident for all bodily injury, and $25,000 for property damage. Industry guidance also points to CSL examples like $300,000 or $500,000 per accident, and notes that CSL often costs more because it provides broader protection through one pooled limit, especially where one type of damage can burn through a smaller sublimit too fast, as explained in this split limits and CSL overview.

A contractor looking at 100/300/100 has the same structure, just with higher separate caps. One cap applies to one person's injury, one applies to all injuries in the accident, and one applies to property damage.

That structure can work fine until an actual loss shows up in the wrong bucket.

Side-by-side comparison

A contractor dealing with subcontracted drivers, borrowed trailers, or mixed crews should also understand how auto exposure can spill into broader jobsite risk. This is why many firms review subcontractor liability in commercial auto alongside the policy form itself.

| Feature | Split Limit (100/300/100) | Combined Single Limit ($1,000,000) |

|---|---|---|

| How limits are written | Three separate caps | One shared cap |

| Bodily injury payment | Restricted by per-person and per-accident injury limits | Paid from the single accident limit |

| Property damage payment | Restricted by its own property damage cap | Paid from the same single accident limit |

| Flexibility in a mixed-loss crash | Lower | Higher |

| Certificate match for a bid requiring CSL | Often a problem | Usually cleaner |

| Best fit | Lower-tier coverage situations | Contractors needing higher per-accident protection |

Consider an electrical contractor's van that rear-ends a newer SUV at a traffic light. Two occupants report injuries. The SUV is badly damaged. Under split limits, the property damage claim is boxed into its own sublimit, even if unused bodily injury capacity still exists elsewhere on the policy. Under combined single limit, the claim can draw from one larger pool based on what the accident costs.

A split-limit policy can look strong on paper and still fail in a real claim if the damage lands heavily in one category.

That's why contractors with service fleets, trailers, and higher-value equipment often prefer combined single limit when they move beyond basic coverage.

How CSL Affects Your Bids and Insurance Certificates

Combined single limit affects more than claims. It affects whether the contractor is ready to bid and ready to start.

A general contractor or property owner asks for CSL because it simplifies their risk review. They want to know there is one substantial auto liability limit available for a single accident, not a set of smaller sublimits that might break down under pressure. That matters when subcontractors bring vans, pickup trucks, flatbeds, and trailers onto active sites every day.

Why project owners ask for it

A certificate of insurance is only a summary. It doesn't rewrite the policy. If the contract calls for CSL and the underlying policy is split limits, the certificate can't turn one into the other by wording alone.

That's why many contractors hit a wall right before mobilization. Operations sends over the signed contract. Accounting asks for the COI. The broker reviews the policy and says the form doesn't match the requirement. Then the contractor has to amend coverage, ask for a waiver, or delay the start.

Contractors managing larger site obligations should review commercial auto requirements for general contractors before the bid stage, not after award.

Where contractors get stuck

The biggest mistake is treating auto liability as a back-office item that can be fixed later. That approach works until the first thorough client review.

Common friction points include:

- Bid-day surprises: The estimator sees the insurance exhibit too late and realizes the auto form won't satisfy the submission.

- Certificate rejection: The project administrator rejects the COI because it doesn't show the required combined single limit structure.

- Umbrella coordination issues: The contractor carries excess liability, but the underlying auto form still doesn't align with upstream expectations.

- Growth bottlenecks: The company is operationally ready for bigger accounts, but the insurance program still fits smaller jobs.

Bottom line: CSL can be a competitive advantage because it reduces the odds of losing work over a preventable paperwork mismatch.

For a drywall contractor chasing tenant improvement work, or a mechanical contractor bidding regional service contracts, that advantage is practical. It shortens compliance conversations. It reduces revisions. It makes the company easier to approve.

Real-World Scenarios A Landscaper's Crash

A landscaping company has three crew trucks and a trailer setup moving mowers, trimmers, and hand tools between properties. One truck heads to an early commercial site with a loaded trailer. On the highway, the trailer tire fails. The driver loses control, hits another vehicle, and the crash involves several cars before everything stops against the guardrail.

That's the kind of accident contractors worry about. It's not one dented bumper. It's injuries, damaged vehicles, roadside property, a disabled trailer, lost time, and a phone that won't stop ringing.

For contractors building response plans after an accident, it also helps to understand the repair and downtime side of commercial vehicle collision management, because claim handling and getting units back on the road are separate problems that hit at the same time.

What the claim looks like

Combined single limit is easier to grasp when considering how bodily injury and property damage compete for the same policy pool. If the accident causes both, both categories draw against the same ceiling. That tradeoff is especially important for contractors with trucks, trailers, and crews in dense traffic, as discussed in this contractor-focused auto liability explanation.

The good part is flexibility. The hard part is exhaustion risk.

A practical way to evaluate this crash:

- Multiple injury claimants: More than one injured person means the bodily injury side can escalate fast.

- Several damaged vehicles: Property damage doesn't stop at one bumper if a trailer swings across lanes.

- Roadside structures: Guardrails, signs, and barriers can add another layer of third-party damage.

- Business interruption: Even if the policy pays the liability claim properly, the contractor still has crews and schedules to deal with.

A contractor should also review how commercial auto accident claims affect contractors before the loss happens, because the policy wording and claims process matter most when nobody has time to read them calmly.

Where CSL helps and where it does not

If the company carries split limits, the property damage side can hit its own cap while injury claims are still developing. That leaves the contractor exposed on the property side even if another part of the policy hasn't been fully used. In a trailer-related crash, that's a real concern because damaged vehicles and roadside property can add up quickly.

With combined single limit, the insurer can allocate the available amount across the full accident based on the actual loss pattern. That often fits contractor claims better because these accidents don't stay neatly separated.

CSL helps when the loss is uneven. It does not create unlimited coverage.

That last point matters. A large property damage payment under CSL can still reduce what remains for bodily injury claims. So combined single limit is usually better for flexibility, but the chosen limit still has to be large enough for the contractor's real exposure.

Choosing Your CSL Amount What Contractors Need

The right combined single limit depends on what the contractor drives, hauls, signs, and bids. A one-van electrician doing residential service calls doesn't face the same auto liability pattern as a roofing contractor running multiple trucks, hauling debris, and moving crews between sites.

Industry guidance aimed at contractors notes that CSL is often used for higher liability placements such as $500k and $1M+, while split limits are more common for lower-tier coverage. It also points out that the buying decision depends on fleet composition, project requirements, hauled equipment, and how quickly one serious crash could exceed a single limit, as described in this CSL and split-limit contractor guide.

What should drive the limit decision

The smartest way to choose a limit is to work backward from exposure.

- Contract requirements: If the best jobs in the pipeline require combined single limit, that requirement needs to shape the policy.

- Vehicle use: Service vans usually create a different claim profile than trucks pulling equipment trailers.

- Cargo and attached equipment: Hauling tools, materials, or machinery increases the chance that an accident produces both bodily injury and property damage at once.

- Crew movement: More drivers and more road time create more opportunities for the wrong kind of loss.

- Asset protection: The policy should help protect the business, not just satisfy a state minimum.

Contractors adding higher-limit protection should also look at how the auto layer coordinates with umbrella and excess liability coverage.

A practical way to think about it by trade

A solo electrician may prioritize contract compliance and basic fleet protection. An operator with trailers should focus heavily on mixed-loss accidents. A concrete contractor with heavier vehicles should expect tougher underwriting scrutiny and larger downside from a serious road claim.

A useful decision filter is simple:

- What's the largest contract requirement on the horizon?

- What's the ugliest realistic fleet accident the company could cause?

- Would the current limit protect both the job and the business?

Decision test: The right CSL amount is the one that satisfies the toughest contract the company wants to win and still looks credible for the fleet exposure it actually has.

What doesn't work is choosing the limit only because it's what the company has always carried. Contractors outgrow their insurance faster than they realize.

Get the Right Limit for Your Next Job

Combined single limit matters because contractors don't operate in neat claim categories. A real fleet loss can involve injured people, damaged vehicles, roadside property, delayed crews, and a contract partner asking hard questions by noon. A policy that gives one shared liability limit often fits that reality better than separate smaller buckets.

It also matters before any accident happens. Contractors with the right auto limit structure are easier to approve, easier to certificate, and better positioned for larger accounts that spell out exact insurance requirements. That can make combined single limit a growth tool as much as a protection tool.

If the current policy shows split limits and upcoming work calls for CSL, that gap should be reviewed before the next bid goes out. If the company already carries combined single limit, the next question is whether the amount still matches the fleet, the contracts, and the size of the business.

A contractor that wants a free quote or a no-obligation coverage review can talk with Coverage Axis. The team helps contractors compare combined single limit options, review current auto liability structures, and build a right-sized insurance program that fits the trade, fleet, and bid requirements.