A lot of Austin contractors are in the same spot right now. A bid is due, a GC wants a certificate before work starts, or a property owner in The Domain pushes over a contract with insurance terms that don't match the policy sitting in the file cabinet.

That's where Contractor Insurance Austin TX stops being a paperwork chore and starts affecting whether a crew gets on site, keeps moving, or gets shut out of better work. Austin isn't a generic market. Tech-driven development, strict municipal requirements, dense traffic, and high-value jobs change what coverage needs to look like.

A small service outfit doing repair work in South Austin doesn't face the same insurance decisions as an electrical contractor trying to qualify for a utility-related project. But both can get burned by the same mistakes. Buying the cheapest policy. Missing completed operations. Letting a sub start before checking additional insured wording. Using a personal truck policy for a work van loaded with materials.

Table of Contents

- The Foundation Your Austin Business Needs

- Navigating Austin's Unique Insurance Rules

- Smart Coverage for Your Specific Trade

- Decoding Your Contractor Insurance Costs in Austin

- Managing Risk with Subcontractors and Additional Insureds

- Get the Right Austin Contractor Insurance in 4 Steps

The Foundation Your Austin Business Needs

You win a job downtown, send over your certificate, and the project manager asks for a revised one before the contract can move. Then one of your vans gets rear-ended on Mopac that same week, and a helper tweaks his back unloading material in East Austin. That is when contractors find out whether their insurance was built for real work or just bought to satisfy a quote request.

For most Austin trade businesses, the base starts with three policies. General Liability, Workers' Compensation, and Commercial Auto. In a market packed with remodels, tenant finish-outs, public work, and high-value commercial jobs, gaps in any one of those policies get expensive fast.

The big three that keep a trade business standing

Take a plumbing company with a few vans running calls from Mueller to South Congress, plus occasional commercial work near The Domain.

General Liability covers third-party bodily injury and property damage. If a pipe connection fails after installation and water runs through cabinets, flooring, or drywall, this is the policy expected to respond. The trade-off is simple. Cheap liability policies can leave out the endorsements or classifications a contractor needs, which becomes a problem when a claim hits or a contract gets reviewed.

Workers' Compensation protects the business when an employee gets hurt on the job. Austin contractors deal with ladders, roofs, trenching, electrical exposure, demo dust, and daily lifting. One injury can mean medical bills, lost time, and a job schedule that starts slipping right away. Even when Texas does not force every contractor to carry workers' comp, many owners buy it because one bad fall can cost far more than the premium.

Commercial Auto covers vehicles used in the business. That matters for Austin contractors who spend half the day moving between jobs, suppliers, and inspections. A truck carrying tools, materials, or crew members is part of operations. A personal auto policy is often the wrong fit for that exposure.

Practical rule: If the vehicle has tools in the back, a wrap on the door, or an employee driving it to a job, put it on a commercial auto policy.

What these policies solve on a real Austin workday

Insurance gets clearer when tied to the kind of claims contractors see every week.

- On a residential service call: General Liability comes into play if completed work later damages a customer's property.

- On a remodel or tenant finish-out: Workers' Compensation matters when an employee slips, strains a shoulder, or gets cut handling material.

- Between jobs on I-35, Mopac, or 183: Commercial Auto matters when a work van is involved in a crash during business use.

That foundation keeps a contractor in business, keeps payroll shocks from turning into cash-flow problems, and keeps routine vehicle claims from landing on a personal policy. For many firms, it also sets the baseline for bidding larger work. If you want a clearer breakdown of how that base policy fits into a broader risk plan, this guide to general contractor insurance is a useful reference.

New contractors often miss this step because they are busy getting equipment, forming the company, and lining up the first jobs. That is common for owners launching niche service lines too. A checklist like these sealcoating startup essentials helps connect those early operating decisions to the insurance choices that follow.

Navigating Austin's Unique Insurance Rules

A contractor can win the bid on a tenant finish-out downtown and still get stalled before the first delivery. The problem is often not price or schedule. It is the insurance review. A certificate comes back with the wrong entity name, the additional insured endorsement is missing, or the liability limits do not match the contract.

What local contracts usually demand

Austin is not a one-template market. A handyman doing small residential repairs in South Austin can often operate with a very different insurance setup than a subcontractor trying to get onto a mixed-use project near The Domain. The city's code environment, the amount of high-value construction, and the contract standards used by larger owners all push insurance requirements higher, especially on commercial and public work.

In practice, the pressure points are usually straightforward:

- Higher general liability limits than a small service contractor carries by default

- Additional insured wording for the owner or GC

- Completed operations coverage that stays in force after the job is done

- Auto liability that matches the contract if trucks, vans, or trailers are part of the work

- Endorsements for trades with underground, structural, or utility exposure

That last point matters more in Austin than many contractors expect. If the job involves trenching, cutting slab, locating utilities, or working around existing infrastructure, contract reviewers often look closely at exclusions and endorsements before they approve a COI.

Why certificates hold up jobs

A Certificate of Insurance, or COI, is usually the first document a project manager sees from your insurance program. It does not change the policy. It shows whether the policy already in force lines up with the contract requirements.

For an electrician bidding a downtown interior build-out, the delay often starts with one of four problems:

- The contract requires higher limits than the current policy

- The certificate lists the wrong business name or entity type

- The owner asks for additional insured or waiver wording that has not been added

- The policy expires before mobilization or before the required completed-operations period

These are fixable issues. They still cost time, and time costs jobs. On a fast-moving Austin schedule, a GC may move to the next qualified sub if certificate review drags on.

A certificate proves coverage. It does not create it.

Where contractors get tripped up in Austin

The biggest mistakes happen when contractors buy insurance for the work they used to do, not the work they are bidding now.

That shows up all over Austin. A remodeler who starts taking larger commercial interiors. A trade contractor hired by a national GC for a project in North Austin. A specialty sub brought onto utility-adjacent work with stricter contract language. The policy may be active and still be wrong for the job.

I see three recurring gaps:

Limits that fit small private jobs but not larger contracts

Austin's larger commercial projects often require more than a basic liability setup.Policy language that does not match how the work is performed

If you hire subs, use leased vehicles, store materials on site, or take on higher-hazard operations, the policy structure needs to reflect that.Late certificate requests

Waiting until the day before a kickoff meeting leaves no room to add endorsements, correct entity details, or raise limits without stress and extra cost.

Contractors who work both private and public jobs need a program built for that mix. A useful starting point is this guide to Texas contractor insurance requirements and coverage options.

Practical habits that prevent contract problems

Read the insurance exhibit before signing the contract. If the job in Austin comes with requirements your current policy cannot meet, find that out before you lock in the price.

Review COI requests as soon as you are shortlisted. That matters on fast-turn tenant work where owners want paperwork cleared before material shows up.

Keep your business name consistent across contracts, W-9s, and policies. A mismatch between “LLC” and an assumed name creates avoidable back-and-forth.

Ask your agent to review the type of work, not just the revenue. Hiring a subcontractor for a retail build at The Domain creates a different exposure than sending one tech to a residential repair call. The insurance should reflect the actual job, the contract language, and the level of owner scrutiny you are stepping into.

Smart Coverage for Your Specific Trade

Required coverage gets a contractor onto the bid list. Smart coverage keeps one bad loss from wiping out equipment, cash flow, or future work capacity.

A lot of policies fail because they're technically active but practically thin. A lawn care professional hauling mowers, a plumber carrying specialized tools, and an HVAC installer storing equipment on site don't have the same exposure. Their insurance shouldn't look identical.

The coverage gap between required and adequate

Consider two jobs.

One is a contractor maintaining commercial properties around North Austin. The biggest insurance pressure may come from trucks, trailers, and equipment moving between sites.

The other is a plumber doing tenant finish-out work in a mixed-use building. The exposure shifts toward completed operations, water damage, and expensive tools riding in vans every day.

That's where extra coverage decisions start to matter:

- Inland Marine protects tools, equipment, and sometimes materials while they're in transit or on site. This is the coverage many contractors realize they need only after a theft from a truck or a job box.

- Umbrella Liability adds extra liability protection above underlying policies. It becomes more important on high-value projects where owners and GCs push for higher limits.

- Surety Bonds aren't the same thing as insurance, but they often matter for public work qualification and contract compliance.

The cheapest policy usually looks fine until someone asks, “Does it cover the tools in the trailer?” or “Can it meet the umbrella requirement on this project?”

A plumbing contractor that's growing into larger commercial jobs may also need a sharper policy structure than a small shop doing mostly service work. This overview of plumbing business insurance is useful for seeing how coverage shifts as job size and project type change.

Typical Insurance Needs by Trade in Austin

| Trade | General Liability | Workers' Comp | Commercial Auto | Inland Marine | Umbrella |

|---|---|---|---|---|---|

| General Contractor | Core policy for third-party injury and property damage, often built to satisfy contract terms | Important when running direct labor crews | Needed for pickups, supervisor vehicles, and business-use trucks | Useful for jobsite equipment and smaller mobile property | Often a smart move on larger commercial jobs |

| Plumber | Important for water damage and completed work exposure | Strong fit for lifting, site injury, and crew protection | Needed for service vans carrying pipe and tools | Strong fit for sewer cameras, press tools, and jobsite equipment | Useful when stepping into larger commercial projects |

| HVAC Tech | Important for property damage tied to installation or service work | Helps protect field crews doing physical installation work | Needed for vans moving equipment and staff | Helpful for gauges, recovery machines, and installed equipment before turnover | Often added when contracts push for higher limits |

| Landscaper | Important for third-party damage on client property | Important when crews use power equipment outdoors | Needed for trucks, trailers, and crew movement between properties | Helpful for mowers, blowers, and mobile equipment | More common on larger commercial maintenance contracts |

The lesson is simple. Buying “a contractor policy” isn't enough. The coverage has to reflect what the crew does, what gets hauled, where work happens, and what the contracts demand.

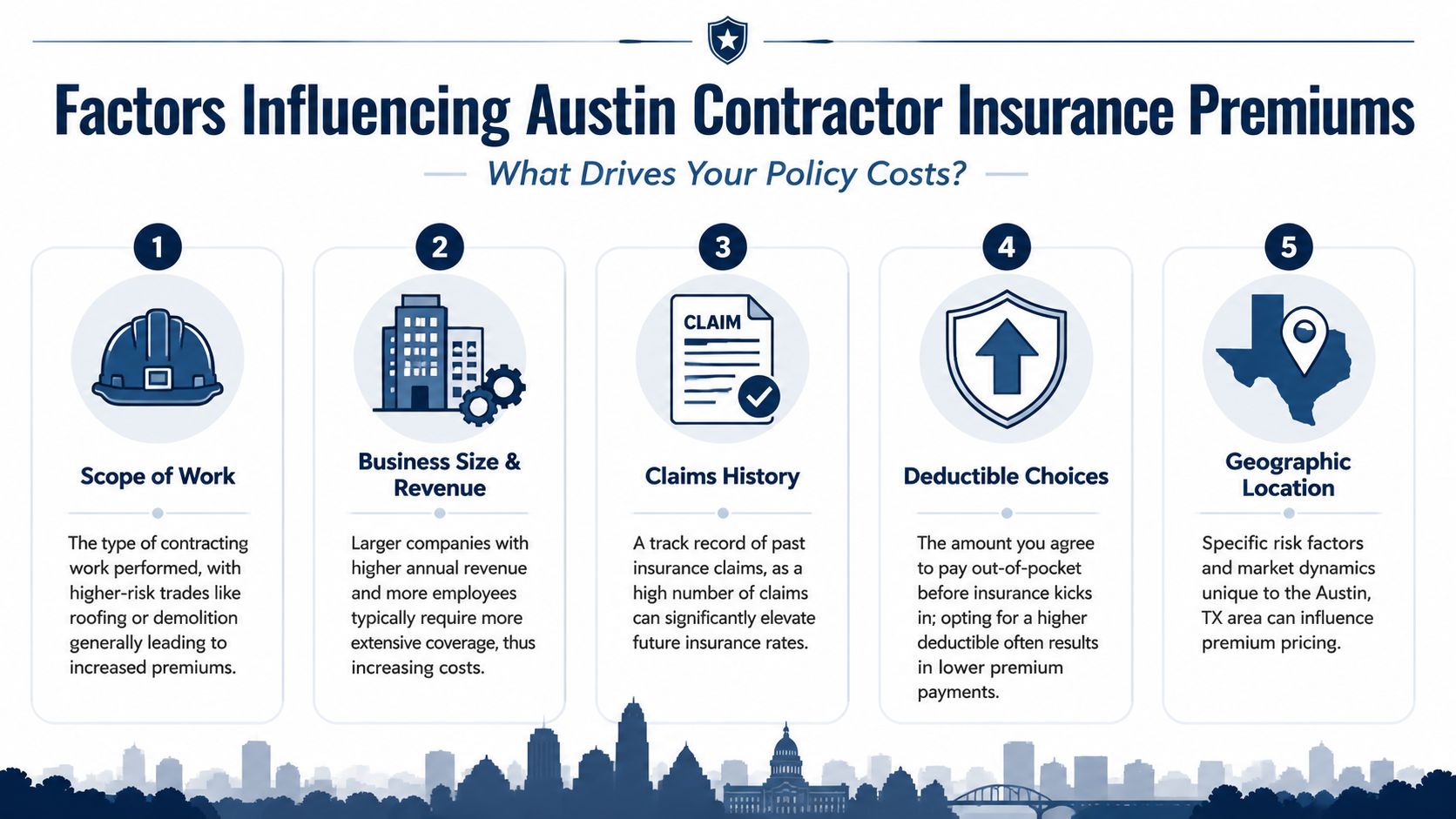

Decoding Your Contractor Insurance Costs in Austin

A contractor bidding a tenant build-out downtown and another running small repair calls in South Austin can both ask for "contractor insurance" and get very different numbers. That is normal. Carriers are pricing the work, the payroll, the vehicles, the claims history, and the contract pressure behind the job, not just the business name on the application.

What the baseline numbers mean

There is no single Austin rate card. A one-crew handyman operation will usually be priced very differently from a general contractor with payroll, pickups on the road every day, and active jobs in tighter urban settings.

That is why rough averages only belong in the budgeting stage. They can help set expectations, but they do not tell you whether a policy will satisfy a downtown project contract, cover a financed truck correctly, or match the trade class the carrier expects.

A cheap premium can become an expensive mistake if the policy does not fit the job.

In Austin, that gap shows up fast. A subcontractor hired for work at The Domain may need higher limits, additional insured wording, or a broader coverage setup than a contractor doing light residential punch-list work in Circle C. The premium changes because the exposure changes.

What pushes premiums up or pulls them down

Underwriters tend to focus on the same few drivers. The difference is how heavily each one matters for your trade.

Type of work performed

Interior finish work is usually viewed differently than ground-up construction, utility work, roofing, or structural trades. Higher injury potential and higher property damage potential usually mean higher pricing.Payroll and labor mix

More field payroll usually means more workers' compensation cost. A business using direct labor is also priced differently from one that mainly supervises subs.Vehicle count and road exposure

Vans, pickups, trailers, and who drives them matter. Austin traffic on I-35, MoPac, and downtown corridors creates real commercial auto exposure, especially for crews making multiple stops a day.Claims history

Repeated water damage claims, backing accidents, or injury losses tell a carrier there may be a supervision, training, or driver management problem.Coverage limits and endorsements

A basic policy with low limits costs less than a policy built to meet commercial contract requirements. The lower number is not always the better buy.

Austin adds its own pressure to the pricing conversation. The city has dense infill work, expensive remodels, strict permitting, and a steady flow of commercial construction tied to population growth and tech expansion. A mistake on a high-value project near downtown or in a mixed-use development can cost far more than the same mistake on a small detached residential job. Carriers know that.

I often tell contractors to look at cost in two buckets. First is fixed insurance overhead. Second is contract-driven cost. If you start landing larger commercial jobs, your insurance program may need to change before the revenue catches up. That is common for electricians, HVAC contractors, and finish trades moving from residential work into office, retail, or multifamily projects.

Contractors who want to keep premiums under control should focus on the items they can influence:

Keep the application accurate

If you install, fabricate, trench, tow trailers, or use subs heavily, say so up front. Misclassified work usually creates trouble at audit or claim time.Control driver quality

One poor MVR can affect the cost of the whole fleet. This matters even more for companies with supervisor trucks and service vans crossing Austin all day.Treat claims prevention like part of production

Documented safety meetings, jobsite housekeeping, and equipment checks help reduce the kind of losses that drive renewals up.Match the policy to the jobs you are pursuing

If your target work includes city jobs, higher-end custom homes, or commercial TI projects, build the coverage for that level now instead of patching it together after award.

For a closer look at how pricing changes with limits, trade class, and risk profile, review this guide to general liability insurance cost for contractors.

Managing Risk with Subcontractors and Additional Insureds

You can bid a clean commercial remodel downtown, line up the schedule, and still watch the job get sideways because a subcontractor's insurance was never set up for that project. I see it happen on Austin jobs where the contract requires additional insured status, completed operations coverage, or higher limits than the sub carries on smaller residential work. The problem usually shows up right before mobilization or right after a claim.

A certificate alone does not solve that.

What additional insured really means on a job

An Additional Insured endorsement gives another party, often the GC, owner, or landlord, access to protection under the subcontractor's liability policy for claims tied to that sub's work. On a project in The Domain, for example, a flooring sub may be working in an occupied retail space with tight delivery windows and expensive finishes nearby. If that crew causes property damage or contributes to an injury claim, the upstream parties want the sub's policy involved first, as the contract intended.

That is why experienced contractors ask for more than a COI. They want the certificate, the actual endorsement when required, and contract wording that matches what the policy can provide. If those three items do not line up, the paper file may look fine while the risk transfer fails when it matters.

Austin raises the stakes because many projects involve stricter owner requirements, higher property values, and tighter contract administration than a small repair job in the suburbs. A sub who is fine for a basic remodel in South Austin may not be properly insured for a Class A office TI downtown or specialty work tied to a utility or public project. As noted earlier, some project types carry much higher insurance requirements. If nobody checks the actual policy terms before work starts, the GC can inherit a claim and a contract dispute at the same time.

A practical subcontractor review checklist

Keep the review process boring and repeatable. That is what works.

Match the legal entity

The named insured on the certificate should be the same company signing the subcontract. If the paperwork says one LLC and the contract names another, fix that before the crew shows up.Check policy dates against the work schedule

A policy that expires halfway through the project creates a gap. This comes up often when a sub is hired late and the job runs longer than expected.Review the coverage lines for the actual exposure

If the sub has employees, drives to sites across Austin, rents equipment, or performs higher-hazard operations, the insurance should reflect that reality.Confirm limits for this project, not their last one

A painter set up for small residential jobs may not meet the requirements for a mixed-use build or a higher-value interior finish package.Verify additional insured and waiver wording

If the subcontract requires ongoing operations, completed operations, primary and noncontributory wording, or waiver of subrogation, confirm each item directly. Do not assume the certificate proves it.Watch for excluded work

Some policies carve out roofing, EIFS, exterior work above certain heights, residential construction, or subcontracted labor. Those exclusions matter more than the premium.

A subcontractor with a current certificate and the wrong endorsement package can still leave the GC holding the bag.

The best contractors in Austin treat subcontractor compliance like part of project setup, not a last-minute admin task. That matters even more as local jobs get larger, contracts get tighter, and owners expect cleaner documentation from day one. For a clearer breakdown of what to request and how to review it, see these subcontractor insurance requirements for contractors and GCs.

Get the Right Austin Contractor Insurance in 4 Steps

Busy contractors don't need a long buying process. They need the right information gathered early, clear recommendations, and a certificate that matches the contract.

Submit the business and project details

Start with the trade, payroll, vehicles, crew setup, and the kinds of jobs the company performs in Austin.Have a licensed advisor shop the market

A good advisor handles outreach across 50+ A-rated carriers and filters out policies that won't work for the trade, crew size, or project demands.Review the recommendation in plain English

The useful version isn't just a premium comparison. It shows what each option does, what it leaves out, and which one fits current and upcoming work.Bind coverage and request the COI

Once the policy is selected, same-day binding is available with 24-hour COI turnaround, which matters when a job is ready to move.

Need a faster way to sort out Contractor Insurance Austin TX without guessing at limits, endorsements, or subcontractor requirements? Coverage Axis shops the market, builds trade-specific coverage, and helps contractors get a free quote or coverage review that matches the work being done.