A lot of plumbing business owners are dealing with the same tension right now. Jobs are booked, trucks are moving, payroll has to clear, and insurance feels like one more bill that only matters when someone asks for a certificate or the state wants proof for a license renewal.

Then a routine job turns into a serious claim long after the crew has left. A water heater install in a finished basement looks clean on day one. Months later, a hidden leak ruins flooring, drywall, and cabinetry, and the homeowner's carrier starts asking hard questions. That's when plumbing business insurance stops being paperwork and starts looking like one of the few things standing between a bad day and a business-threatening loss.

The right approach isn't buying a random stack of policies and hoping it all fits. A residential service plumber, a small shop with two vans, and a contractor bidding bonded municipal work don't need the same setup. They need a program that matches how they work, what they drive, what they carry, who they hire, and what can come back on them after the job is done.

Table of Contents

- Beyond the Wrench Why Your Insurance Matters

- The Plumber's Essential Insurance Toolkit

- Insuring Your Tools Projects and Reputation

- What Drives Your Plumbing Insurance Premiums

- Staying Compliant with State and Client Demands

- Advanced Risk Scenarios for Plumbing Contractors

- How to Get the Right Plumbing Insurance Step-by-Step

Beyond the Wrench Why Your Insurance Matters

A plumbing company can do everything right on the visible part of a job and still get hit later by the part no one sees. A slow leak behind a finished wall, a failed connection under a slab, or water migration from a second-floor bathroom remodel can trigger damage long after final payment clears.

That's why insurance has to do more than satisfy a license board. It has to protect the business from delayed property damage claims, injury claims, vehicle losses, payroll-related obligations, and contract demands that show up in normal plumbing work.

The job isn't over when the crew leaves

A drain cleaning crew can leave a slick floor at a residence. A service tech can back a van into a customer's fence. An apprentice can throw out a back hauling cast iron. A small mistake can become a legal problem, a medical bill, or a property loss that has to be paid by someone.

Practical rule: The most expensive plumbing claims often come from ordinary work done on an ordinary day.

Insurance also affects growth. Commercial customers commonly want proof of general liability, commercial auto liability, and workers' compensation before work starts, and many states require plumbers to carry liability insurance and a license bond as part of licensing or renewal, as outlined in plumber insurance cost guidance for common policy types.

Insurance is a business tool, not a box to check

A solid insurance program does three jobs at once:

- Protects cash flow: Covered claims don't have to come straight out of operating funds.

- Supports better jobs: The right certificates and endorsements help a contractor qualify for stronger commercial opportunities.

- Keeps one mistake from ending the business: A single hidden defect or jobsite injury shouldn't erase years of work.

For plumbers, that matters because the trade carries long-tail exposure. Water doesn't need much time to do expensive damage. And when a customer, property manager, or general contractor starts looking for who's responsible, they'll start with the contractor who touched the piping.

The Plumber's Essential Insurance Toolkit

A lot of plumbing owners buy insurance one policy at a time, usually because a customer asks for a certificate, a state board asks for proof, or a broker sends over a quote. That approach leaves holes. A better approach is to build the core of the program around how the business works: occupied homes, service vans, employees in the field, and jobs that can come back months later if a fitting fails or a line leaks.

Start with four policies that carry most of the load for a plumbing contractor.

The four policies most plumbers can't skip

General liability handles claims from other people who say your work or your crew caused bodily injury or property damage. If a customer slips on a wet bathroom floor during a service call, or a tech chips a stone countertop while resetting a fixture, this is usually the first policy in play. It also matters for completed work. If a problem tied to your work shows up after the job is finished, that claim often lands here, assuming the policy is set up correctly and the operations are classified properly. Contractors who want the plain-English version can review this guide to general liability insurance for contractors.

Workers' compensation pays for employee job injuries, subject to state law and policy terms. Plumbing is hard on backs, shoulders, knees, and hands. Water heater installs, trench work, ladder work, demo, and moving cast iron all create exposure. Owners sometimes get caught here when they use part-time helpers or assume a 1099 label solves the problem. It usually does not if the state or carrier views that person as an employee.

Commercial auto covers liability arising from business vehicles, with physical damage added if you choose it. A plumbing company runs through its vans and trucks. Personal auto coverage is not designed for a lettered service van carrying fittings, machines, and inventory from stop to stop all day. If your driver rear-ends another vehicle on the way to a repipe, this is the coverage that should respond.

A business owner's policy, or BOP, packages general liability with commercial property coverage for small businesses that have an office, shop, or stored contents. That can be a good fit for a plumbing company with a small premises, office furniture, computers, parts inventory, or fixtures stored off the shelf. It is often a cleaner base than buying liability and property separately, but only when the property side matches what is at the location.

Core plumbing insurance policies at a glance

| Policy Type | What It Covers | Real-World Plumbing Scenario |

|---|---|---|

| General Liability | Third-party bodily injury and property damage, including many claims tied to completed work | A homeowner slips on water tracked onto a tile floor during a drain clearing visit |

| Workers' Compensation | Employee job-related injuries and related costs | A tech injures a shoulder lifting a heavy water heater into place |

| Commercial Auto | Liability tied to business vehicles, with vehicle damage options depending on policy setup | A service van hits another car while carrying tools and materials to a job |

| Business Owner's Policy | General liability plus commercial property for qualifying small business premises | A small plumbing office suffers a covered property loss that damages office contents |

The key is how these policies work together.

General liability addresses damage or injury to others. Workers' comp addresses injuries to your own employees. Commercial auto addresses road exposure. A BOP can protect the small office or shop that keeps the operation running. Put those together and you have a usable foundation for a residential service company, a small remodel crew, or a light commercial plumber.

But the right answer still depends on the work mix. A one-van service plumber has a different risk profile than a contractor bidding tenant improvement jobs, public work, or municipal projects that require bonds, higher limits, and tighter contract terms. Owners who want to boost profitability with loss prevention usually do better when they pair insurance with tighter hiring, vehicle controls, tool tracking, and water-damage prevention procedures.

What works in practice

Match the policy setup to the operation, not the label on the form.

- Residential service plumbers usually need clean coordination between liability, commercial auto, and workers' comp if they have staff.

- Plumbers with a shop or office often benefit from a BOP, but only if the property values are realistic and the location is listed.

- Contractors using helpers, apprentices, or family labor need to get clear on workers' comp status before an injury turns into a coverage dispute.

- Plumbers doing larger commercial or public work should treat these four policies as the base, not the whole program.

The mistake I see most often is assuming the first policy purchased is doing more than it really does. General liability does not replace workers' comp. A BOP does not insure road risk. Commercial auto does not protect the office. And none of these policies, by themselves, guarantee that post-job liability exposure is handled the way a plumbing contractor expects. That is why the toolkit matters. It is the start of a coordinated insurance program, not the finish line.

Insuring Your Tools Projects and Reputation

A plumber finishes a water heater swap on Friday, gets paid, and moves on. On Monday, the customer calls because a fitting in the wall let go overnight and water ran for hours. The tools in the van are another concern. So is the building owner asking for proof of coverage before your crew can start the next job. Those are different problems, and they do not all fall under the same policy.

This part of the insurance program is where plumbing businesses either stay protected or find out, too late, that they bought a policy instead of a plan.

What core coverage leaves out

General liability usually handles third-party bodily injury or property damage claims. It does not usually pay to replace your press tools, sewer camera, threader, or locator if they are stolen from a truck, job site, or storage unit. Owned mobile equipment needs its own coverage, often written as an equipment floater or inland marine form.

That detail matters because plumbing tools rarely stay in one place. They move from shop to van, van to driveway, driveway to job site, then back again. If the schedule includes emergency calls, they may sit in a vehicle overnight. Coverage has to follow that movement, or the loss lands on your balance sheet.

Completed operations is another gap owners miss. It is the part of liability coverage that responds after the job is done, not while your crew is still on site. If a drain line starts leaking a week later, a failed solder joint damages cabinets, or a gas connection issue causes a claim after sign-off, completed operations is the piece that often decides whether you have a defense and indemnity or an ugly dispute with the carrier.

I pay close attention to this on plumbing accounts because the loss often shows up after everyone thinks the job is over.

The add-ons that start to matter as the work gets larger

Higher-limit liability is one example. A bad water loss in a commercial space, a serious auto accident involving a marked van, or a claim tied to multiple units can burn through base limits faster than many small contractors expect. Umbrella liability can add another layer above certain underlying policies, but only if the underlying limits, classifications, and policy structure are set correctly in the first place.

Then there are bonds. A surety bond does not protect your company the way insurance does. It protects the project owner or public entity if you fail to meet the contract terms. That distinction matters on municipal work, public bid jobs, utility connections, and larger commercial contracts where bond language is part of the gatekeeping.

A city sewer tie-in is a good example. You may have valid liability coverage, workers' comp, and commercial auto, but still lose the job because the bid requires a bond, additional insured wording, waiver of subrogation, or specific certificate language. This overview of a certificate of insurance for vendors explains why those document requests show up before materials hit the site and why small errors can stall the job.

Reputation belongs in this section too. Plumbing claims are messy, visible, and expensive. One avoidable theft loss, one unsecured van, or one preventable water incident can cost money twice. First in the claim itself, then in tougher renewals and harder conversations with property managers and GCs. Owners who want to boost profitability with loss prevention usually do better when they treat security, tool control, and jobsite procedures as part of the insurance strategy, not separate from it.

The practical takeaway is simple. Tools, completed work, contract paperwork, and bond requirements need to be built into the program from the start. If your insurance only fits the day you bought it, it will not fit the jobs you are trying to win next quarter.

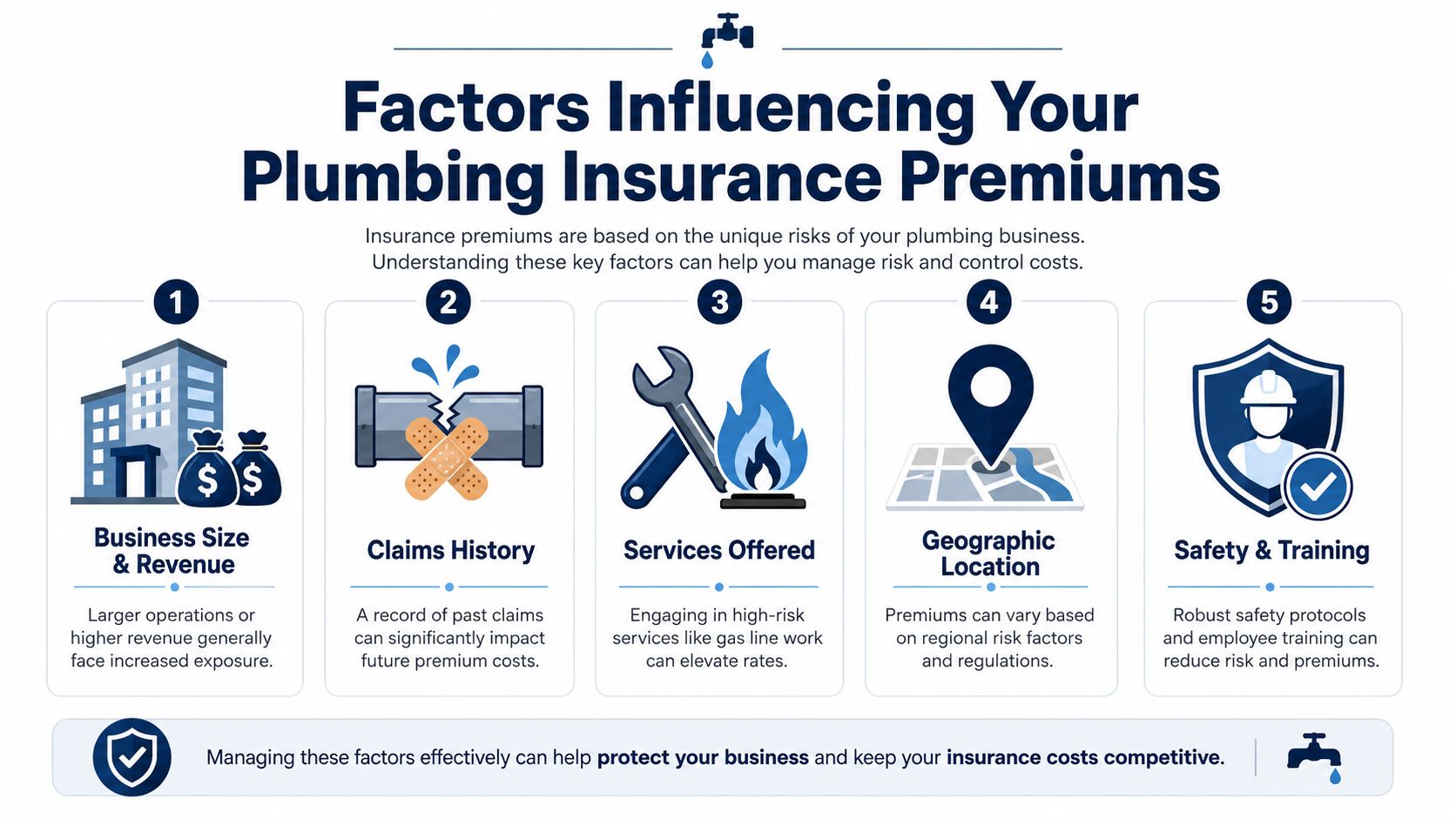

What Drives Your Plumbing Insurance Premiums

Insurance pricing isn't random. Underwriters look at a plumbing business and ask a simple question. How likely is this operation to produce claims, and how severe could those claims be?

A one-van residential service outfit and a multi-crew contractor doing gas piping, tenant improvement, and utility work don't present the same risk. Their premiums shouldn't look the same either.

The main cost levers underwriters look at

Payroll and crew size matter because more field labor creates more workers' compensation exposure. More people in the field means more lifting, more driving, more jobsite movement, and more chances for injury.

Revenue and job volume also matter. More work generally means more customer locations, more completed jobs, and more opportunities for a third-party claim to happen.

Claims history carries a lot of weight. A business with repeated auto claims, recurring water damage losses, or frequent employee injuries will usually get tougher pricing and tighter underwriting attention than a cleaner account.

Type of work performed can change the whole picture. A residential service plumber doing fixture replacements and drain cleaning doesn't present the same profile as a contractor doing multi-story rough-in, utility connections, or gas line work. The work class affects both frequency and severity potential.

Location changes cost too. Regulation, litigation environment, labor rules, and local loss patterns all affect premium. For example, state-level pricing can vary sharply for plumber liability coverage, and some states set specific workers' comp mechanics.

What actually helps lower cost over time

In Washington, the Department of Labor & Industries sets the base workers' compensation premium rate for residential and small commercial plumbers at approximately $1.78 per hour as of 2023, and employers with strong safety protocols can qualify for experience modification discounts of 25% to 40%, according to Washington plumber workers' compensation rate guidance.

That tells plumbing owners something important. Safety isn't just good culture. It's a pricing lever.

A contractor who wants a better renewal should focus on the pieces under the business's control:

- Clean job classification: Make sure the work being reported matches the work performed.

- Driver management: Screen drivers, address preventable incidents, and set rules for company vehicles.

- Safety documentation: Written procedures matter more when they're followed, reviewed, and documented.

- Tool and vehicle maintenance: Preventable failures often become preventable claims.

- Claim response discipline: Fast reporting and accurate documentation can keep a bad incident from getting worse.

Better pricing usually follows better operations. Underwriters reward businesses that can explain their work clearly and show how they control losses.

Owners who want to understand how claim history affects workers' comp pricing should review how a workers comp experience modification works. That metric can shape renewal cost more than many contractors realize.

Staying Compliant with State and Client Demands

Plumbers don't just buy insurance for loss control. They buy it because licensing boards, property managers, general contractors, and public entities often make it a condition of doing business.

That's where many owners run into trouble. They assume compliance is broad and generic, when it's usually very specific.

Licensing requirements aren't generic

State requirements vary sharply. In Florida, certified plumbing contractors must show proof of at least $100,000 in general liability insurance and $25,000 in property damage insurance before a license is granted. Illinois requires $100,000 general liability, $300,000 bodily injury, and $50,000 property damage for licensing, as detailed in state plumbing insurance requirements for Florida and Illinois.

Those numbers matter because they show a basic truth. There is no universal "plumber policy" that automatically satisfies every state.

Louisiana is another good example of why owners need to read the licensing rules closely. State law requires plumbers to maintain a minimum aggregate limit of $500,000 for general liability and property damage coverage through an authorized insurer, and workers' compensation becomes mandatory upon hiring the first employee. Sole proprietors must file a notarized affidavit of exemption that expires annually on December 31, according to Louisiana plumbing insurance and licensing requirements.

What contract insurance language usually means

Commercial jobs often add another layer. The certificate request or subcontract may ask for terms that sound technical but are manageable once translated.

- Certificate of Insurance or COI: Proof that the contractor carries the required policies and limits.

- Additional Insured: A request to extend certain liability protection to the upstream party, often a general contractor or property owner.

- Waiver of Subrogation: A request limiting the insurer's right to pursue recovery from a specified party after paying a claim.

A plumbing subcontractor on a tenant improvement project may get asked for all three. The GC isn't asking for paperwork for the sake of paperwork. The GC wants confirmation that the plumber has coverage and that the GC has some contractual protection under the plumber's policy structure.

The paperwork isn't the job. But if the paperwork is wrong, the job may not start.

A common challenge for many growing shops arises when their policy is active, yet endorsements don't match the contract, or the certificate request arrives too late. For contractors hiring subs or working under another contractor's insurance standards, this guide to subcontractor insurance requirements helps clarify what usually gets requested and why.

Advanced Risk Scenarios for Plumbing Contractors

Most articles stop at the basic policy list. That's fine for a simple service operation. It's not enough for a plumbing contractor whose work can trigger claims long after the trench is backfilled or the wall is closed up.

Completed operations is where many programs break down

Completed operations is one of the most important and most misunderstood parts of plumbing business insurance. It deals with liability that appears after the work is finished.

For a residential plumber, that might mean a slow leak behind a vanity wall. For a contractor doing municipal sewer work, the exposure gets heavier and lasts longer. Utility tie-ins, municipal pipe installations, and underground repair work can create delayed failures that don't show up right away, and policy limitations in this area can leave a dangerous gap.

That gap isn't theoretical. A 2024 data point showed 42% of plumbing contractors who perform utility work experienced a completed operations claim within 18 months, but only 15% had adequate coverage, according to completed operations exposure for utility plumbing contractors.

A contractor who only swaps water heaters in occupied homes has one kind of completed operations risk. A contractor handling sewer line repairs for a municipality has another. Underwriters know the difference, and plumbing owners need to know it too.

A policy that works for basic residential service can fail badly on utility or municipal plumbing work if completed operations needs aren't reviewed carefully.

Other exposures that deserve a closer look

Some plumbing businesses also need to ask tougher questions about specialty exposures.

Pollution liability can matter for septic work, drain cleaning involving contaminated discharge, or operations where sewage release becomes part of the claim. Professional liability can matter when the plumber takes on design-build responsibility, layout decisions, or specification-driven work where the allegation is a professional error rather than straight bodily injury or property damage.

These aren't universal needs. But they become relevant fast when the business expands beyond routine service and repair. The mistake many owners make is assuming "plumbing" is one underwriting class. It isn't. The policy structure should reflect the actual jobs being performed, not the broad trade label on the website or the side of the van.

How to Get the Right Plumbing Insurance Step-by-Step

Buying insurance gets easier when the owner stops trying to shop abstract policy names and instead builds around operations, contracts, and growth plans. A clean process saves time and usually leads to better coverage decisions.

A simple path from quote request to active coverage

Assess operations

Start with what the company does. Residential service, remodel work, new construction, gas piping, utility work, drain cleaning, and municipal projects don't belong in the same risk bucket.Pull together the business details underwriters need

That usually includes business structure, payroll or staffing details, vehicle information, loss history, current insurance, and the type of jobs performed. If bids or contracts require special wording, that should be part of the conversation early.Shop multiple carrier options

A broad market approach matters because one carrier may like small service plumbers while another is more comfortable with contractors doing larger project work. Owners who want a practical overview can review how to get bonded and insured before starting the application process.Compare recommendations in plain English

Price matters, but so do exclusions, completed operations treatment, vehicle coverage details, and endorsement handling. The cheapest option can become the most expensive one if it doesn't match the work.Bind coverage and confirm certificate handling

Once the policy is in force, make sure the business can get COIs, additional insured language, and bond support without delay. That administrative side affects revenue more than many owners expect.

What to have ready before applying

A plumbing contractor can speed up the process by organizing a short file before asking for quotes:

- Operations summary: The types of plumbing work performed and the types avoided

- Employee and payroll details: Enough information to place workers correctly

- Vehicle list: Who drives what, and how the vehicles are used

- Prior insurance and claims information: A clear history helps underwriters evaluate the account accurately

- Upcoming contract requirements: Especially for bonded work, public jobs, or projects with endorsement demands

The best outcome isn't just a policy that binds. It's a coverage program that fits the company's actual risk and keeps pace as the business adds employees, vehicles, tools, and larger contracts.

A plumbing company shouldn't have to guess whether its coverage will hold up after a leak, a vehicle claim, or a contract review. Coverage Axis helps contractors get a free quote or coverage review built around their actual work, crew size, vehicles, and project requirements, with plain-English guidance and fast turnaround on the policies and certificates they need.