A contractor wins the job, lines up the crew, orders materials, and then gets stuck on a one-page insurance form. The property manager kicks back the paperwork with notes like “AI required,” “waiver needed,” and “primary non-contributory wording missing.” Nobody on the site earns a dollar until that gets fixed.

That's why a certificate of insurance for vendors matters far more than most contractors expect. It isn't office paperwork for the sake of office paperwork. It's often the document standing between a signed contract and a live job, between smooth billing and a payment hold, between a subcontractor's mistake and a claim hitting the wrong policy.

For trade businesses trying to win better work, this matters on both sides. A contractor has to provide a clean COI to owners, GCs, and landlords. That same contractor also has to collect and review COIs from subs, haulers, equipment vendors, and specialty trades before they walk onto the site.

Table of Contents

- Why Your Vendor COI Can Make or Break a Job

- What Is a Vendor Certificate of Insurance

- Decoding Required Coverages and Limits

- The Three Critical Endorsements Explained

- Your Practical COI Verification Checklist

- Common COI Mistakes That Cost Contractors Jobs

- Get Compliant Fast with Coverage Axis

Why Your Vendor COI Can Make or Break a Job

Monday morning, your crew is loaded out, the lift is scheduled, and the owner's rep sends a one-line email: insurance rejected. No site access until the certificate matches the contract.

That is how jobs get delayed before a single tool comes off the truck.

A vendor COI can decide whether work starts on time, whether pay apps keep moving, and whether you look buttoned-up during bid review or like a subcontractor who creates admin problems. For contractors, this is not clerical busywork. It is part of pre-job risk control and part of sales.

The practical issue is simple. A signed contract does not get you through the gate if the insurance paperwork is wrong. Owners, GCs, lenders, and property managers use the COI review to screen for two things at once. First, can this vendor meet the project requirements? Second, if something goes sideways, is the risk being pushed where the contract says it belongs?

That second point is where contractors lose time. A certificate may show active coverage and still fail review because the named insured is off, the certificate holder is wrong, an endorsement is missing, or the policy dates do not line up with the job. On a busy project, nobody wants to debate insurance wording while rough-in is supposed to start. The reviewer just kicks it back.

I see the same pattern across trades. A concrete sub gets held at the gate because the GC is not properly reflected in the COI package. An electrical contractor is told to revise the certificate before mobilizing because auto liability or workers' comp details do not match the contract requirements. A roofer gets approval delayed because the asset manager wants confirmation that the underlying policy wording, not just the ACORD form, supports the transfer of risk.

The contractors who win more work usually treat COI compliance as part of operations, not an afterthought. They know what their carrier can issue, they catch gaps before the customer does, and they respond fast when a project manager asks for revisions. That makes estimating cleaner, onboarding faster, and your company easier to hire again.

It also protects margin. Every avoidable delay creates labor reshuffling, schedule compression, and office time nobody priced into the job.

If you are still sorting out the bigger insurance picture behind these requests, start with this guide to insurance contractors often need. The sections that follow will get into the part many articles skip. The endorsements that usually decide whether your COI is accepted or sent back.

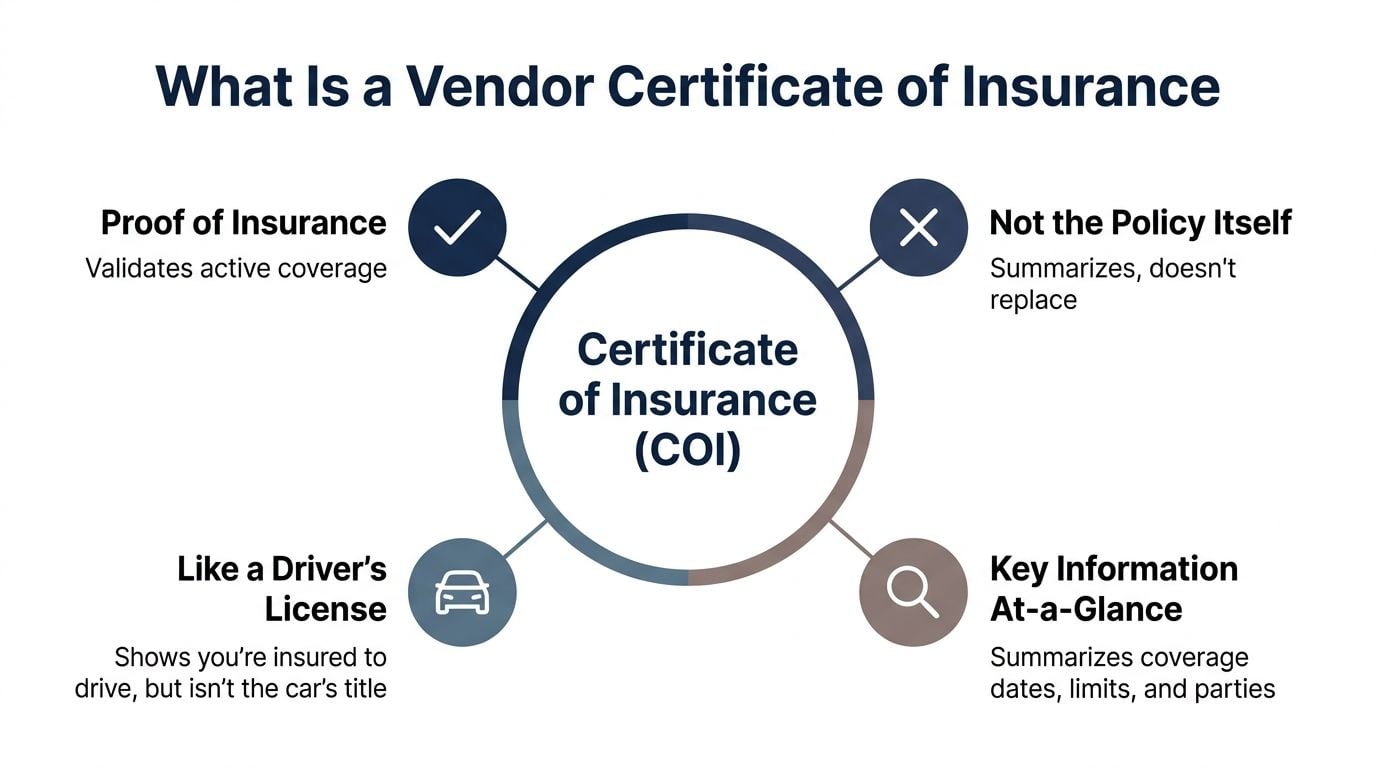

What Is a Vendor Certificate of Insurance

A vendor certificate of insurance is the document that gets your sub, supplier, or service vendor through the insurance checkpoint before work starts. It gives the hiring party a quick read on whether coverage appears to be in place for the job. For a contractor, that matters because this piece of paper often decides whether mobilization stays on schedule or gets pushed back.

The certificate is proof of insurance status, not proof that every contract requirement has been satisfied. That is the part many contractors learn the hard way. A COI can show active general liability and still fail review if the policy does not include the right endorsements, the named insured is wrong, or the dates do not cover the project term.

A vendor COI functions much like a business license check

A vendor certificate of insurance is usually issued on an ACORD 25 form. It is a standardized snapshot of the insured business, the carrier, the coverage types, the limits, and the policy dates. It helps a GC, owner, property manager, or upstream contractor screen whether a vendor appears insurable before letting that company onto the job.

On a real project, this usually comes up fast. A landscaping company is scheduled to start irrigation and planting work for an HOA. Before anyone unloads equipment, the HOA asks for a COI. The form shows the company name, the insurance carrier, general liability, commercial auto, workers' comp, and the active policy period. That gives the reviewer enough information to decide whether the vendor can move into the approval queue or needs revisions first.

What it does not do is replace the policy itself.

That distinction affects risk transfer, and risk transfer affects your balance sheet. If a claim hits the job and the wording behind the certificate does not match what the contract required, the certificate will not fix the problem after the fact.

What to look for on the form

The ACORD form has a lot of boxes, but a contractor reviewing a vendor COI usually needs to focus on a few fields first:

- Insured. The legal business name should match the entity signing the contract and performing the work. If the certificate names the wrong LLC, expect questions.

- Insurer. This identifies the carrier issuing the policy.

- Coverages. This section lists the policy types, such as general liability, workers' compensation, and commercial auto.

- Policy dates. These dates need to line up with the project schedule, not just the day the certificate was issued.

- Certificate holder. This should show the company requesting proof of coverage.

A clean-looking COI can still hide problems. I tell contractors to read it the way they read a set of plans. You are not just checking whether the page exists. You are checking whether the details match the job.

If you want a field-by-field reference before you send or review one, this certificate of insurance template guide helps break down what each part of the form is telling you.

Decoding Required Coverages and Limits

A COI review gets real the moment the job changes from office paperwork to field exposure. A janitorial vendor cleaning a finished lobby creates one set of risks. A roofer working over pedestrians, glass, and parked cars creates another. If the coverage on the certificate does not match the actual work, the file gets kicked back, the vendor stalls, and the project schedule starts slipping.

That is why experienced contractors do not read limits as filler on a form. They read them as a preview of who pays first when something goes wrong.

What the main coverages actually do

General Liability handles third-party bodily injury and property damage claims tied to the vendor's operations. On a job site, that can mean cracked storefront glass, damaged flooring, or a delivery driver tripping over materials left in a walkway. For many contractor and vendor agreements, a common starting requirement is $1,000,000 per occurrence and $2,000,000 aggregate. The exact number still depends on the contract, the owner, and the trade.

Workers' Compensation covers employees injured in the course of their work. If a laborer falls from a ladder or strains a back unloading material, this is the policy expected to respond. Contractors usually also look for Employers Liability on the certificate because contracts often call for stated limits there, not just a workers' comp policy in name only.

Commercial Auto applies when owned, hired, or non-owned vehicles are part of the work. A van clipping a parked car, a dump truck backing into a gate, or a driver causing an accident while hauling material creates an auto claim, not a general liability claim. If vehicles touch the project in any meaningful way, auto coverage usually belongs on the COI.

One detail contractors miss all the time is the difference between per occurrence and aggregate. Per occurrence is the most the carrier pays for one covered claim. Aggregate is the cap for covered claims over the policy term. If a trade contractor runs multiple crews across several jobs, prior claims can eat into the aggregate before your project ever has a loss. A COI may show acceptable limits on paper while the available capacity behind those limits is already under pressure.

Insurance limits should match the weight of the work. A low-risk vendor and a high-hazard trade should not be reviewed the same way.

Typical Insurance Limit Requirements for Contractors

The table below gives a practical framework for reviewing COI requests by exposure, not by paperwork alone. The contract always controls, but this helps explain why one vendor clears review quickly while another gets held up for revised limits.

| Trade Type | General Liability (Per Occurrence / Aggregate) | Commercial Auto (Combined Single Limit) |

|---|---|---|

| Office service provider working on-site | Often starts at $1,000,000, with aggregate limits set by contract | Commonly required if employees drive for business operations |

| Construction trade contractor | Often starts at $1,000,000 / $2,000,000 | Frequently required when vehicles are used on or for the project |

| Transportation vendor | May be set by contract based on loading, unloading, and site access exposure | Higher limits are often required because vehicle risk is central to the work |

| Manufacturing vendor | May require higher general liability limits depending on product or operational exposure | Higher auto limits may apply when delivery or transport is part of the job |

This matters most with specialty vendors. A contractor may be used to checking drywall, electrical, or plumbing subs, then bring in a hauler, crane service, or equipment delivery company and review it the same way. That is a mistake. Those vendors often carry the biggest vehicle and jobsite access exposures on the entire project.

If you need a practical benchmark for comparing contract requirements to policy amounts, this guide to general liability coverage limits for contractors and vendors gives more detail on how limits are usually matched to job risk.

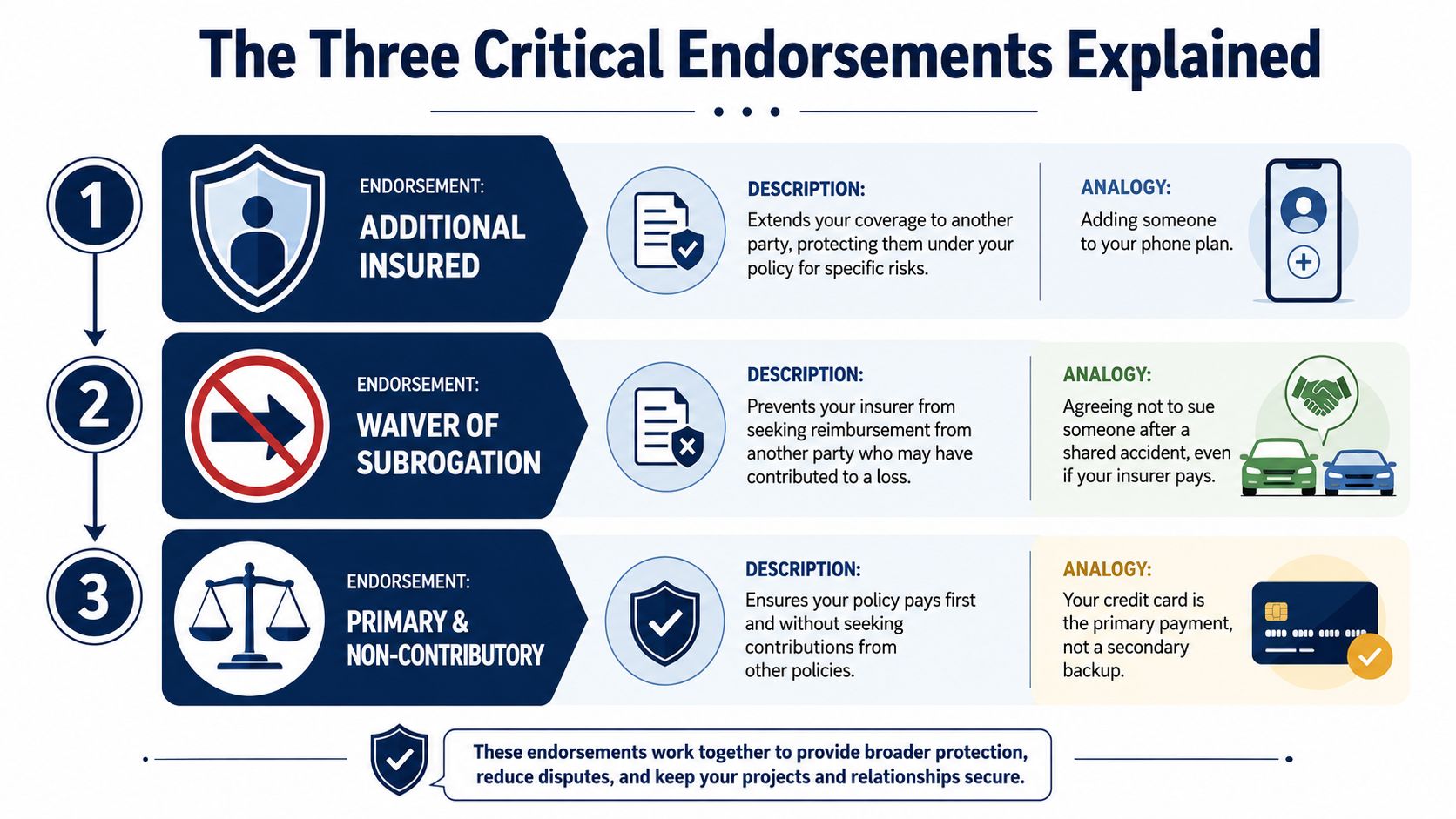

The Three Critical Endorsements Explained

Most COI problems don't come from the top half of the form. They come from the endorsements hiding behind the certificate. In these endorsements, contractors either protect the job properly or assume they're protected when they're not.

An HVAC contractor on a commercial retrofit is a good example. The GC asks for three things that sound like legal jargon: additional insured, waiver of subrogation, and primary non-contributory wording. Those three items decide whose policy responds, who can recover against whom, and whether the GC's own insurance gets dragged into the claim.

This visual shows the three endorsements that usually create the most confusion.

The distinction between named insured and additional insured affects policy control and extended coverage, while waiver of subrogation prevents a vendor's insurer from suing the hiring entity for reimbursement after a claim, and primary and non-contributory language ensures the vendor's coverage pays first, according to this industry explanation of vendor insurance requirements and endorsements.

Additional Insured

Additional insured status extends certain liability protection to another party under the vendor's policy. In plain terms, it can help protect the GC or owner when they're pulled into a claim caused by the vendor's work.

Take an HVAC subcontractor installing rooftop units. A rigging mistake damages the roof membrane and water enters tenant space. The building owner sues everyone in the contract chain. If the GC required additional insured status properly, the HVAC sub's policy may help defend the GC for liability tied to that subcontractor's work.

Being listed as certificate holder is not the same thing. Certificate holder tells the insurer who received the form. It doesn't extend coverage by itself.

Contractors dealing with this requirement regularly can benefit from a more detailed breakdown of the additional insured endorsement.

Waiver of Subrogation

Subrogation is the insurer's right to pursue recovery from another party after paying a claim. A waiver of subrogation blocks that recovery route when the contract requires it.

Use a mechanical room fire example. A painter working nearby leaves equipment in a way that contributes to a loss. The painter's carrier pays under the policy. Without a waiver, that insurer may try to recover from the hiring contractor or property owner later. With a waiver in place, that recovery path is cut off as specified by the contract.

A waiver doesn't prevent the claim. It helps prevent the aftershock, where one insurer starts chasing another party on the same job.

Primary and Non-Contributory

Primary and non-contributory wording decides whose insurance responds first. If the vendor's policy is primary, the hiring contractor's policy shouldn't be tapped first for a covered loss tied to that vendor's operations.

Back to the HVAC example. If a lift damages finished glass during equipment placement, the subcontractor's policy should stand in front. Without proper wording, the GC can end up tendering the claim into its own program sooner than expected.

This is why discerning owners and GCs don't just ask for a certificate of insurance for vendors. They ask for proof that the endorsements behind the certificate match the contract.

Your Practical COI Verification Checklist

Friday at 3:30, a vendor sends over a COI so they can start Monday. The certificate looks clean at first glance. Then you notice the named insured does not match the contract, the policy expires mid-project, and no endorsement backup is attached. Catching that on Friday can save a shut-down on Monday.

That is how I tell contractors to treat COI review. It is a pre-mobilization control, just like checking a lift ticket, confirming material delivery, or verifying the right crew showed up for the right scope. A fast review up front protects schedule, billing, and claim position later.

Pre-job review steps

A COI is only a snapshot. It summarizes coverage, carrier, limits, and dates, but it does not override the policy or prove every contract requirement has been met. The practical move is to review it the same way you review submittals. Line by line, against the contract, before the vendor is on site.

Use this checklist:

Match the legal insured name to the contract. If the agreement is with one LLC and the COI shows a different entity, stop and get it corrected. Claims get messy fast when the wrong company is listed.

Check effective and expiration dates against the job schedule. Coverage that is active today may still lapse before rough-in, final install, or punch work is done.

Compare the coverage types to the actual scope. A delivery-only vendor may need different coverage than a trade performing installation, hot work, or hauling. For a stronger intake process, use this guide to subcontractor insurance requirements to align insurance collection with the work being performed.

Review the limits against your contract requirements. A certificate can show general liability and still fail review because the limit is too low for the project or owner requirement.

Confirm your company is listed correctly as certificate holder. Wrong entity names, old addresses, and informal branch names are common reasons a COI gets kicked back.

Read the description of operations. It should match the job. If the certificate references cleaning services and the vendor is cutting concrete, ask questions before work starts.

Request endorsement copies when the contract requires them. The certificate alone is not enough if your agreement calls for specific policy wording.

Keep the process simple enough that your office can repeat it every time. The goal is consistency, not paperwork for its own sake.

When to push back and verify harder

Some certificates deserve extra scrutiny because the downside is bigger.

- Large contract value or tight schedule. If a bad COI can hold up mobilization, inspection, or pay apps, verify details before the vendor shows up.

- Higher-risk trades. Roofing, demolition, hauling, traffic control, and any hot-work exposure justify a closer review.

- Vague or inconsistent wording. If the description of operations is generic, the entity names do not line up, or the form looks altered, call the issuing agent listed on the certificate and confirm it was indeed issued.

- Mid-project renewals. A vendor who starts with acceptable coverage can fall out of compliance during the job. Renewal tracking matters on longer projects.

A clean-looking COI is not the same as a compliant one. If it does not match the contract and the work on site, treat it like an incomplete submittal and send it back for correction.

Common COI Mistakes That Cost Contractors Jobs

The most expensive COI errors are usually the boring ones. The wrong entity name. An expired policy. A missing endorsement. A certificate that looks fine until someone compares it to the contract line by line.

That's why contractors get frustrated by COI review. The form feels simple, but the consequences aren't. A rejected certificate can stop site access, hold billing, delay inspections, and sour the first impression with a new client.

Where contractors get tripped up

A major compliance gap is assuming the certificate itself guarantees protection. It doesn't. 34% of COI reviews fail to identify missing Additional Insured endorsements that are contractually required, and many contractors wrongly believe certificate holder status alone provides liability protection, according to this analysis of common COI misunderstandings and endorsement gaps.

That shows up in several common mistakes:

- Submitting only the certificate summary. If the contract requires endorsement copies, the COI alone may not satisfy review.

- Using the wrong certificate holder name. An electrical contractor can lose time merely because the legal entity on the certificate doesn't exactly match the contract party.

- Sending outdated policy information. A policy that expired before mobilization can stop work immediately.

- Missing trade-specific coverage. A vendor with delivery exposure but no matching auto evidence can create a hard stop.

- Assuming a checked box settles everything. It often doesn't. Reviewers may ask for the actual endorsement form.

Why small errors turn into expensive delays

A contractor doesn't need a denied claim to feel the pain. Admin errors alone can hurt cash flow. Work can't start. Payroll still runs. Materials may already be ordered. The client may wonder whether the contractor is buttoned up enough for the job.

A masonry subcontractor waiting on corrected COI language can miss a sequencing window. A landscaping firm can lose access to a gated community project because the HOA wasn't named correctly. An electrical contractor can have payment held while the office fixes a certificate holder mismatch.

The paperwork problem becomes an operations problem fast.

The contractors who avoid this usually do one thing better than everyone else. They treat insurance compliance as part of project setup, not as a last-minute admin chore.

Get Compliant Fast with Coverage Axis

Contractors don't need more jargon. They need insurance that fits the trade, the crew, and the contract in front of them. They also need COIs that go out correctly the first time, with the right endorsements lined up before the owner, GC, or property manager starts redlining documents.

That's where a specialist matters. Coverage Axis is built for construction, trade, and specialty contractors across the United States. Licensed advisors shop 50+ carriers to help contractors find right-sized coverage for the work they perform. The process is straightforward, and the goal is practical compliance, not generic policy language. When a contractor needs a certificate turned around quickly, speed matters just as much as coverage structure.

For a growing HVAC company, that can mean aligning general liability, workers' comp, auto, and endorsement needs before bidding larger commercial jobs. For an outdoor services provider moving into HOA and municipal work, it can mean getting ahead of COI requests instead of scrambling after award.

Contractors who want a free quote or a no-obligation coverage review can talk with Coverage Axis. A licensed advisor can help review current policies, check contract insurance requirements, and make sure the next certificate of insurance for vendors is built to clear compliance without slowing the job down.