A lot of contractors don't start by asking, “What insurance do contractors need?” They start with a problem.

A bid package lands in the inbox. A property manager asks for a certificate before work starts. A general contractor sends over a subcontract agreement filled with terms like Additional Insured, Waiver of Subrogation, ongoing operations, completed operations, and liability limits that look higher than anything the contractor currently carries. A plumber trying to land a commercial tenant improvement job or a roofer moving from residential work into managed properties usually hits this wall fast.

That's where insurance stops being a background expense and becomes a business filter. The contractor with the right setup gets on the job. The contractor with the wrong setup loses time, scrambles for endorsements, or gets disqualified before pricing even matters.

Table of Contents

- The Insurance Wall Every Contractor Hits

- The Foundation General Liability and Workers Compensation

- Protecting Your Tools Trucks and Equipment

- How Contracts and COIs Dictate Your Coverage

- Advanced Coverage for Growth and Bigger Bids

- Specialty Insurance Most Contractors Overlook

- How to Build Your Custom Insurance Program

The Insurance Wall Every Contractor Hits

A small electrical contractor wins mostly service calls and tenant work, then decides to bid a larger office remodel. The pricing is manageable. The labor plan makes sense. Then the insurance requirements page shows up and slows everything down.

The contract asks for general liability with specific limits, additional insured status, completed operations wording, workers compensation, auto, and proof before mobilization. A fire sprinkler installer or plumbing subcontractor sees the same thing on bigger jobs. The work itself may be familiar, but the paperwork feels like a separate trade.

Why the confusion costs real jobs

Insurance language is technical, but the consequences are practical. If the contractor can't produce the right certificate, can't add the required endorsement, or carries the wrong policy type, the job may not start. Even when the contractor eventually gets compliant, delays can hurt credibility with the client or GC.

A lot of owners first think insurance is only about licensing. On actual projects, it's also about risk transfer. The client wants the contractor's policy to respond first when the contractor's work creates a loss. That's why contract requirements usually go beyond whatever a state minimum might be.

Contractors don't usually lose bigger jobs because they can't do the work. They lose them because their paperwork and coverage don't match the contract.

A roofer moving into commercial maintenance runs into this quickly. A residential setup that felt adequate on home jobs may not satisfy a property manager with strict vendor requirements. A mason stepping onto a university project faces the same issue. The contract often expects a more formal insurance program than a small crew has carried in the past.

Insurance becomes a growth tool

The contractors who handle this well usually treat insurance as part of operations, not as a last-minute purchase. They review requirements before signing. They understand what their certificate can show. They know which endorsements need to be requested from the carrier in advance.

For contractors trying to sort out bid-driven requirements, this guide to general contractor insurance requirements is a useful starting point because it frames insurance the way jobs are awarded.

A plumber bidding a mixed-use buildout, an electrician taking on school work, and a concrete contractor moving into municipal jobs don't all need the exact same program. But they do need a way to connect real business milestones to the right coverage at the right time. That's the part that usually clears up the confusion.

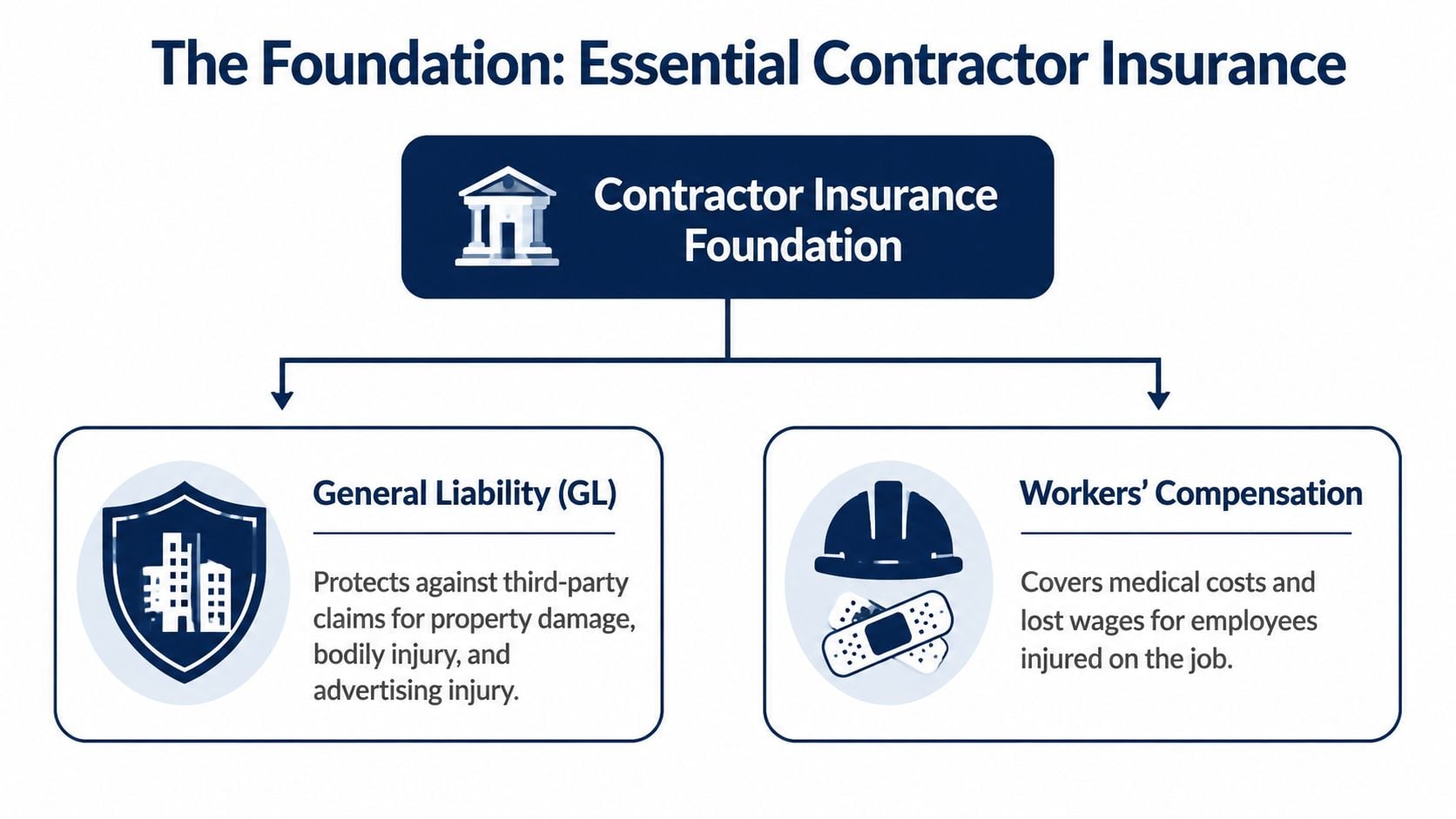

The Foundation General Liability and Workers Compensation

A lot of contractors hit their first real insurance decision at two moments. The contract asks for proof of General Liability, or the owner hires that first employee and now has a workers compensation obligation. A solo plumber doing small residential calls may get by with a basic setup for a while. The minute that same plumber signs a restaurant buildout or adds an apprentice, the insurance program has to change.

Why General Liability is the public-facing policy

General Liability handles claims from other people who say your work or jobsite caused bodily injury or property damage. For many contractors, it is the first policy a client, landlord, or GC expects to see on a certificate.

An electrician working in an occupied retail store is a good example. A customer trips over a cord and gets hurt. A ladder tips and cracks a glass case. A roofer drops debris that dents a tenant's car in the parking lot. A plumber opens a wall for a repair and water damages finished flooring in the unit next door. Those are the day-to-day loss scenarios this policy is built for.

The milestone matters here. A handyman doing small cash jobs may carry General Liability because it is smart risk management. A contractor bidding commercial work usually needs it because the contract requires it, often with specific limits and completed operations coverage. Contractors who are sorting through limit choices can review this explanation of general liability coverage limits to see how per-occurrence and aggregate limits apply in practice.

General Liability also has boundaries. It does not cover defective workmanship in every form, and it does not replace builders risk, commercial auto, or professional liability where those exposures exist. That is where many contractors get tripped up. They buy the policy that gets the certificate issued, then find out later it was never meant to cover every job problem.

Why Workers Compensation changes the conversation once you hire

Workers compensation is tied to payroll, labor, and state law. For a solo roofer or owner-operator electrician with no employees, the question may be whether to carry it voluntarily or whether a GC will require it before allowing site access. Once that contractor hires a helper, apprentice, or office employee, the issue shifts from optional planning to legal compliance in many states.

A framing contractor sees this change fast. One worker falls from a short scaffold and breaks a wrist. An HVAC helper strains a back carrying equipment into a mechanical room. Those are employee injury claims. General Liability does not respond to them because they are not third-party claims.

This is also a business milestone, not just an insurance purchase. Hiring the first employee often triggers payroll reporting, audits, classification issues, and contract requirements from upstream parties. A mason adding a laborer for summer work and a plumbing company building out a three-person field crew may both need workers compensation, but the cost and setup depend heavily on trade class, payroll, and loss history.

Driving adds another layer. If a carpenter's employee causes an accident in a company truck between jobs, the injury and liability pieces may involve more than one policy depending on who was hurt and how the vehicle is insured. For a plain-English explanation of road liability concepts, this guide to essential liability coverage for drivers is a useful companion to the contractor side of the discussion.

The practical point is simple. General Liability protects the business from many public-facing claims. Workers compensation addresses injuries to employees. A contractor who has both in place at the right time is in a far better position to sign contracts, add staff, and keep jobs moving when something goes wrong.

Protecting Your Tools Trucks and Equipment

A contractor can have liability covered and still be exposed where daily operations hurt most. The truck gets wrecked on the way to a site. The trailer disappears overnight. The laser, saws, and testing tools go missing from a locked job box. None of that is fixed by General Liability alone.

Commercial Auto covers road exposure tied to the business

A landscaping contractor might have a pickup, a dump trailer, and a crew heading between properties all day. If that truck causes an accident, a personal auto policy may not be the right answer for a business-use claim. The same issue hits HVAC contractors whose vans carry refrigerant, tools, and replacement parts from call to call.

Commercial Auto is the policy built for business vehicles and business driving exposure. It matters even more once employees drive company vehicles, haul materials, or move from one site to another on a tight schedule.

A good way to think about it is this:

| Scenario | Policy that usually responds |

|---|---|

| HVAC van causes a traffic accident on the way to a service call | Commercial Auto |

| Tree crew truck backs into a customer's fence at a jobsite | Commercial Auto |

| Pickup used daily for business is damaged in a covered roadway loss | Commercial Auto |

A contractor comparing vehicle options can look at a commercial auto policy quote with the same seriousness as a liability quote, because one severe vehicle claim can disrupt cash flow and contract eligibility fast.

Inland Marine covers the gear that moves from site to site

The name confuses almost everyone at first. For contractors, Inland Marine usually means movable tools, equipment, and materials that travel, sit in transit, or live on jobsites rather than at a fixed office.

A plumber has drain machines, inspection cameras, press tools, and stocked fittings in the truck. An electrician carries meters, benders, threaders, and specialty cordless tools. A theft from the site or from the vehicle can shut down work the next morning. General Liability doesn't solve that. Commercial Auto doesn't automatically solve that either.

Practical rule: If the item earns money by moving from truck to trailer to jobsite, it usually needs equipment-focused coverage, not just liability coverage.

For many smaller contractors, the difference between being insured and being operational becomes apparent. Liability policies protect the business from claims. Equipment coverage helps the business keep working. A flooring contractor who loses moisture meters, saws, and jobsite tools doesn't just lose property. The contractor loses schedule, labor efficiency, and the ability to finish the scope on time.

How Contracts and COIs Dictate Your Coverage

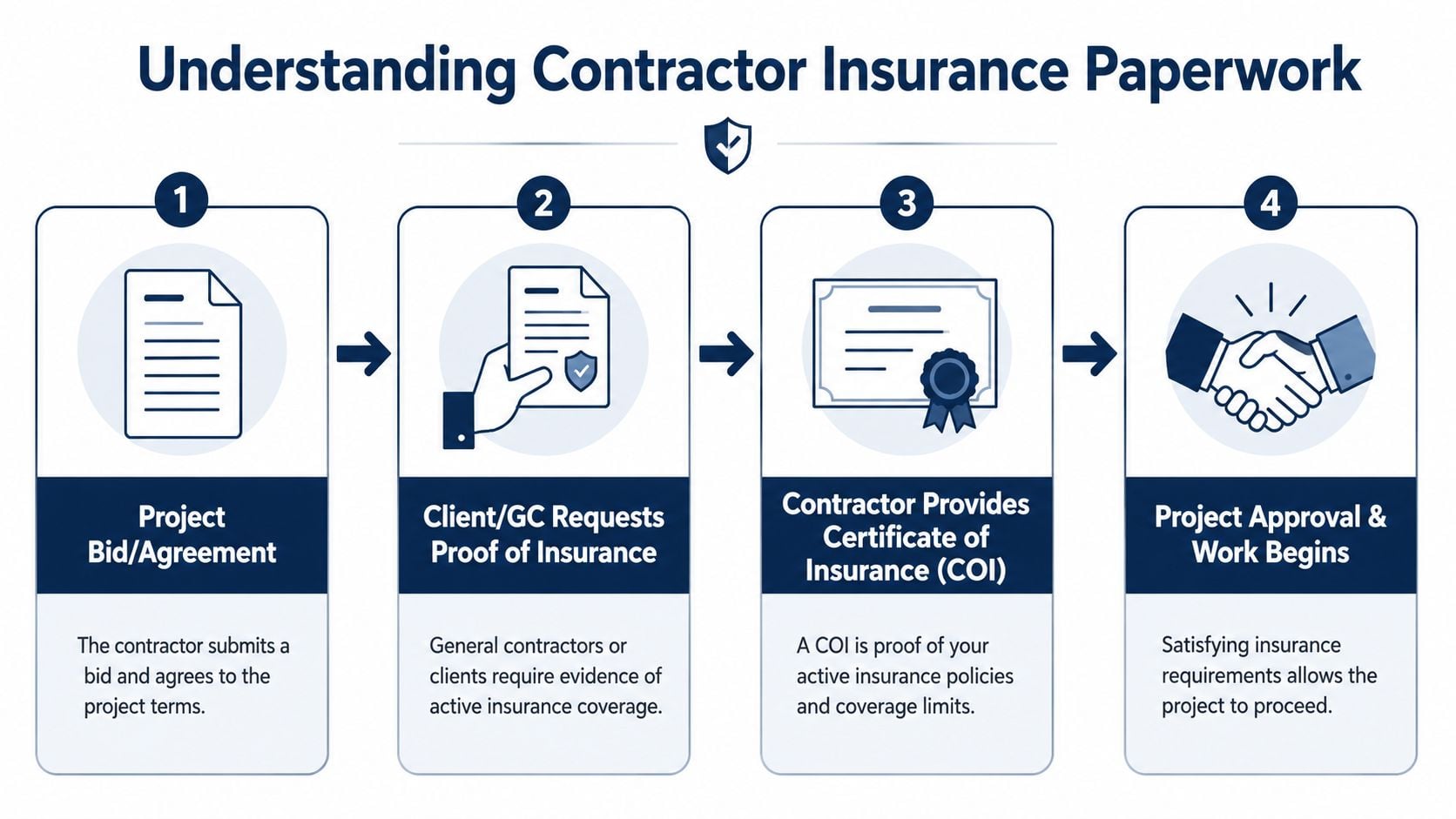

A lot of contractors find out what coverage they need when a job is ready to start and the paperwork gets rejected.

A roofer wins a commercial reroof. The contract looks fine at first glance. Then the owner asks for a COI, additional insured status, waiver of subrogation, and primary and noncontributory wording. If the policy setup does not match the contract, the problem is immediate. Work gets delayed, payroll keeps running, and the first impression with the GC goes sideways.

A Certificate of Insurance, or COI, is the proof clients ask for before they let a contractor on site. It shows the policies in force, the limits, and the effective dates. It does not change the policy, broaden coverage, or add endorsements that were never issued.

A COI confirms what already exists

This is one of the biggest misunderstandings I see with contractors moving from small residential jobs into commercial work. They assume the certificate request is administrative. It is usually a contract compliance check.

An electrician on a tenant improvement project may have General Liability in force, but the lease build-out contract can require specific endorsements tied to that owner and that job. If those endorsements are missing, the COI cannot solve it. The agent has to issue the right forms, and sometimes the carrier has to approve them first.

That timing matters. A concrete sub can lose a start date over paperwork even when the premium is paid and the policy is active.

Contracts often decide your next coverage change

Insurance needs change at business milestones, and contracts are one of the clearest triggers. A plumber doing small service calls may get by with a basic liability setup for a while. The minute that same plumber signs a subcontract with a retail developer or school district, the insurance requirement section starts dictating policy changes.

Common requests include:

- Additional insured status for the owner, GC, or property manager

- Waiver of subrogation on liability or workers compensation

- Primary and noncontributory wording so your policy responds first

- Per-project aggregate language on General Liability

- Higher limits than the contractor carried for smaller jobs

For a plain-English explanation of what one of the most common requirements means, review how an additional insured endorsement works for contractors.

A framing subcontractor sees this quickly on larger projects. The GC may accept a basic COI for one private remodel, then require scheduled additional insured wording and specific completed operations treatment on the next apartment build. Same trade. Different contract. Different insurance setup.

Read the insurance exhibit before you sign

The key decision point is usually not when the COI is requested. It is when the contract is still negotiable.

A masonry contractor who signs first and reviews insurance later gives up options. If the contract asks for endorsements the current carrier will not provide, the contractor may need to change carriers, pay more, or accept job terms that create claim friction later. A careful review up front gives the contractor a chance to price the requirement into the bid or push back on language that does not fit the work.

Use this check before signing:

- Match the legal entity exactly. The named insured on the policy should match the company signing the contract.

- Compare the contract to the policy forms. A COI should reflect endorsements already attached, not assumptions.

- Watch completed operations requirements. Roofers, electricians, and plumbers often face claims after the job is finished, so post-completion wording matters.

- Confirm lead time. Some endorsements can be issued quickly. Others need underwriter approval and can hold up mobilization.

Contractors do not usually buy these coverages because a textbook says they should. They buy or amend them because a bid package, owner contract, lender requirement, or GC compliance portal forces the issue. That is why contract review is one of the clearest ways to decide what insurance you need now, and what you will need before you chase bigger work.

Advanced Coverage for Growth and Bigger Bids

As a contractor grows, claims can get larger even when the work quality stays strong. More employees, more vehicles, more subcontractors, and larger project owners create more ways for a serious loss to happen. That's when basic coverage often stops being enough for the jobs being pursued.

A general contractor bidding municipal work is a good example. The company may already carry General Liability, Workers Compensation, and Auto, but the bid package asks for higher limits and bonding support before the proposal is even considered.

Umbrella coverage is built for severe losses

Umbrella or excess liability sits above underlying liability policies and provides additional limits when a covered loss blows past the primary layer. The simplest way to think about it is overflow protection for catastrophic claims.

For labor-intensive trades, project owners frequently require Workers' Compensation at statutory limits, Commercial Auto at $1 million combined single limit, and umbrella or excess liability of $5 million on top, according to Loyola University's contractor requirements at insurance requirements for contractors. That package aims at the two loss channels that hit contractors hardest. Jobsite injuries and auto accidents.

A concrete contractor hauling crews and equipment to active sites can see why this matters. One severe roadway claim or one major injury event may exceed the primary policy threshold. The umbrella is there for that upper layer of exposure. Contractors trying to decide whether they've reached that stage can review commercial umbrella insurance in the context of their actual contracts, not just their current revenue.

Bigger limits don't automatically mean better coverage. They mean the contractor is preparing for claim severity that could otherwise break the business.

Surety bonds solve a different problem

Surety bonds aren't insurance in the usual sense. They don't exist to pay the contractor for a loss. They exist to guarantee performance or payment obligations to the project owner or obligee.

That distinction matters on public work. A mid-sized GC building out a park structure or school addition may need a bond to qualify. A site utility contractor can have strong liability coverage and still be unable to bid if the project requires bonding capacity the firm doesn't have.

A roofer almost never needs to think about bonds on small repair jobs. The same roofer bidding institutional re-roofing work may need to think about them immediately. Growth changes the insurance conversation because larger buyers ask different questions.

Specialty Insurance Most Contractors Overlook

A lot of contractors assume a standard liability policy covers anything connected to the job. That assumption causes some of the worst coverage surprises in construction.

A restoration contractor dealing with water damage, an excavation crew disturbing soil, or a design-build electrician making system recommendations all face risks that don't fit neatly inside ordinary General Liability expectations.

Completed work creates a different liability window

Construction guidance often separates ongoing operations from completed operations, and that distinction matters for trades like plumbing and electrical, as noted in this article on contractor insurance coverage distinctions. Work can create one kind of exposure while the crew is onsite and another after the crew has left.

A plumber may have no issue during installation, then face a claim later when a failed connection causes damage after turnover. An electrician may finish a panel or wiring upgrade, only to face an allegation tied to completed work after occupancy. Those aren't the same as an active jobsite slip or a tool dropped during service.

This is why contractors shouldn't treat “liability” as one bucket. The timing of the loss matters. The wording tied to completed operations matters. The contract may care about that distinction even when the contractor hasn't thought about it before.

Pollution and design exposures sit outside standard assumptions

Many contractors assume General Liability is enough, but standard GL policies often exclude pollution-related losses and claims arising from design errors, which creates a gap for restoration, excavation, HVAC, refrigeration, and design-build firms, as explained in this overview of contractor pollution and professional liability needs.

A few trade examples show where that becomes real:

- Restoration contractor: Mold conditions, contaminated water, or cleanup decisions can trigger environmental exposure.

- Excavation contractor: Soil disturbance, runoff, or underground material release can create pollution-related claims.

- HVAC contractor: Refrigerants, fuel-related components, or system performance recommendations can create exposure outside basic GL assumptions.

- Electrical design-build firm: If the contractor also specifies layout, load approach, or performance decisions, that advice can create a professional liability issue.

If the contractor's job includes cleanup, containment, environmental handling, or design judgment, standard GL may leave the most expensive part of the claim outside the fence.

That doesn't mean every roofer, painter, or tile installer needs every specialty policy available. It means the decision should be tied to the actual work performed, not to a generic checklist.

How to Build Your Custom Insurance Program

The right answer to what insurance contractors need depends less on the trade label and more on the business stage. A solo tile setter doing residential work has a different profile than a plumbing company with service vans, apprentices, and commercial contracts. A grounds-care professional with one pickup has a different exposure than a grading contractor running crews and hauling equipment.

Start with the way the business actually operates

A practical review starts with documents and workflow, not with shopping for the cheapest premium.

A solid prep list usually includes:

Current contracts and bid requirements

A commercial client may require more than state licensing rules. Large project owners often expect higher limits. Tufts University, for example, requires contractors and vendors to carry Commercial General Liability insurance of $1,000,000 per occurrence and $2,000,000 aggregate, showing how bid qualification often drives insurance standards in real markets through its published insurance requirements for vendors and contractors.Payroll and crew details

A drywall contractor with employees, helpers, or shifting labor arrangements needs the insurance program to reflect how labor is deployed.Vehicle and equipment schedules

A locksmith with one van and a paving contractor with multiple units have very different auto and equipment exposures.Work type and job conditions

Heights, excavation, water intrusion risk, refrigerants, tenant-occupied spaces, and design input all change what should be reviewed.

A new trade business can also benefit from broader operational planning. For contractors still structuring the company itself, this guide to handyman business startup essentials is useful because insurance decisions usually work better when they're aligned with licensing, entity setup, and service scope from the start.

Compare policies on fit, not just price

Two policies can look similar on the certificate and still perform very differently when a claim or contract issue shows up. A cheap quote that misses key endorsements can cost more than a higher quote that properly fulfills the job.

A useful comparison process looks like this:

- Look at contract fit first: Can the policy satisfy the owner, GC, or property manager requirements without last-minute scrambling?

- Check trade-specific gaps: A roofer, HVAC contractor, and excavation company should not all be reviewed the same way.

- Confirm operational match: Vehicles, tools, employees, and subcontractor use should line up with the policy setup.

- Ask for plain-English explanations: If a contractor can't tell what a policy does in a real claim scenario, the review isn't finished.

Coverage Axis is one option contractors use for this kind of review. It shops multiple carriers and builds construction-focused insurance programs around trade type, crew size, and project requirements rather than forcing a generic package.

The goal isn't to buy every policy available. It's to carry the right ones for the next stage of the business. A residential electrician may need a clean liability-and-auto setup today. The same company may need endorsements, higher limits, and specialty coverage once it starts bidding schools, medical offices, or design-build work.

Contractors who want a practical second look at their current setup can get a free quote or coverage review from Coverage Axis. A licensed advisor can review contracts, current policies, vehicles, crew structure, and trade-specific exposures to help identify what's required now, what can wait, and what might be missing before the next bid goes out.