A bid package lands in the inbox on Monday morning. The scope fits the crew, the schedule works, and the margins look solid. Then the insurance exhibit shows up. Suddenly the job that looked ready to price turns into a puzzle of liability limits, additional insured wording, workers' compensation, auto coverage, and umbrella requirements that don't match what the company carries now.

That's where many contractors get stuck. They assume insurance is just a licensing box to check, only to find out the contract is the gatekeeper. The contractor who understands that difference gets the bid out faster, avoids last-minute scrambling, and looks more professional to owners and upstream GCs.

That's why general contractor insurance requirements matter far beyond compliance. They affect who can bid, who can sign, who gets on site, and who gets pushed out before the first mobilization meeting. A contractor can do great work and still lose opportunities because the paperwork, limits, or endorsements aren't lined up.

The good news is that this problem is manageable. Once the moving parts are clear, insurance becomes less of a recurring headache and more of a job-winning tool. Contractors dealing with larger projects, multiple trades, or higher-risk scopes can also benefit from reviewing the operational side of exposure, especially the day-to-day issues covered in this guide to contractor risk factors.

Table of Contents

- Introduction Why Insurance Requirements Are Your Key to Bigger Jobs

- The Core Four Coverages Every GC Must Understand

- Decoding Policy Limits From State Minimums to Project Demands

- Beyond the Basics When to Add Umbrella Coverage and Surety Bonds

- The Paper Trail That Wins Jobs COIs and Additional Insureds

- Managing Subcontractor Risk A GC's Guide to Compliance

- Get Compliant Get Bidding Your Next Steps

Introduction Why Insurance Requirements Are Your Key to Bigger Jobs

A general contractor bidding a school addition or municipal renovation usually doesn't lose the job over carpentry knowledge or scheduling software. The loss often happens much earlier, when the insurance requirement sheet gets handed to accounting or a broker at the last minute and nobody can confirm whether the current program matches the contract.

That frustration is real. Many contractors carry what their state or license board requires and assume that's enough until an owner, university, or public agency asks for more. Then the scramble starts. Endorsements have to be requested, limits have to be increased, subcontractor requirements have to be tightened, and the start date gets closer while everyone waits on paperwork.

Practical rule: The coverage that keeps a license active is not always the coverage that wins the next job.

Insurance works differently on bigger projects because the owner isn't just checking whether a contractor exists legally. The owner is trying to push risk away from the project and onto the firms doing the work. That changes everything. It changes limits, endorsements, timing, documentation, and how subcontractors are managed.

Take a roofing GC moving from residential tear-offs into institutional work. On a house, the owner may never ask for a certificate or completed operations wording. On a university or public project, the bid package can require a much more structured insurance program before the contractor is even allowed on site. The contractor who treats insurance as a growth tool usually moves through that process faster than the contractor who sees it as pure overhead.

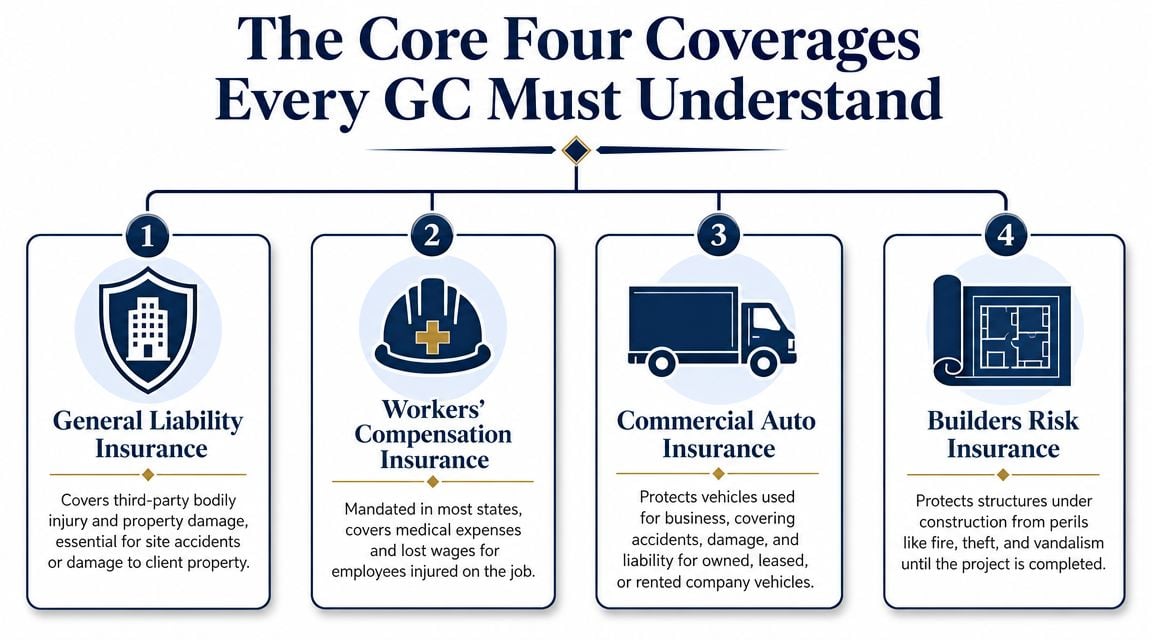

The Core Four Coverages Every GC Must Understand

A GC doesn't need every policy on the market to understand the basics. But four coverages show up again and again because they solve four different jobsite problems. On a residential remodeling project, all four can matter in the same week.

General liability and what it actually does

General liability covers third-party bodily injury and property damage claims tied to the contractor's operations. Think of a remodel where debris falls from a second-story opening and damages a neighbor's parked vehicle, or a visitor trips over materials staged near the front walk. That's the lane where GL usually responds.

On larger commercial and public work, the benchmark GL structure commonly sits at $1,000,000 per occurrence and $2,000,000 aggregate, and California DGS contract requirements explicitly state limits of not less than those amounts in an occurrence-based form requirement context through its public contract insurance requirements guide. Contractors who want a plain-English refresher on the policy itself can review this overview of general liability coverage for contractors.

A framing contractor offers a simple trade example. If stacked lumber tips and breaks a client's glass door, that's a liability issue involving someone else's property. It isn't a workers' comp claim, and it isn't a builders risk issue. It belongs in GL.

Workers compensation commercial auto and builders risk in the real world

Workers' compensation handles employee job injuries. If a crew member falls from scaffolding during the same remodel, GL doesn't pay that worker's medical costs. Workers' compensation is the policy meant for that situation. The legal trigger depends on state rules, but once a contractor has employees, this coverage quickly becomes mandatory in both compliance and contract settings.

Commercial auto applies when a business vehicle causes an accident or creates liability on the road. If the superintendent backs a company pickup into another car while unloading tools, that's an auto loss, not a GL claim. In contractor operations, the line between “work vehicle” and “personal use” gets blurry fast. That's why vehicle use needs to be defined correctly before a claim happens.

Builders risk protects the structure and materials during construction. If a partially completed addition suffers a covered fire loss, theft, or vandalism, builders risk is the policy contractors and owners start looking for. The main mistake isn't misunderstanding what it covers. The main mistake is starting work without confirming who is carrying it.

A practical office issue sits behind all four policies. When a loss happens, job documents, invoices, photos, and incident details need to move quickly and cleanly. Contractors trying to reduce delays often benefit from cleaner admin workflows around insurance claims processing, especially when multiple documents from the field have to be organized fast.

- GL handles outside-party claims: Customer injury, damage to someone else's property, and many routine site liability allegations.

- Workers' compensation handles employee injuries: Medical and wage-related issues tied to employee job injuries.

- Commercial auto handles road exposure: Owned business vehicles and work-related driving need their own treatment.

- Builders risk protects the job itself: Materials and the unfinished structure need a separate answer from liability insurance.

A contractor who knows which policy should respond can spot coverage gaps before the owner, adjuster, or attorney does.

Decoding Policy Limits From State Minimums to Project Demands

Most confusion around general contractor insurance requirements starts with one false assumption. Contractors think the state minimum is the practical standard. In practice, it often isn't.

Why state minimums and contract limits don't match

State rules vary widely. Arkansas requires commercial general liability at $1,000,000 per occurrence and $2,000,000 aggregate, while contractor guidance for Minnesota cites a much lower $50,000 per occurrence general liability minimum under state guidance, as shown in the Arkansas rule discussion and state comparison reference.

That gap explains why contractors get caught off guard. State licensing exists to set a legal floor. Project contracts exist to shift project-specific risk. Those are different jobs, so the numbers often don't match.

A small drywall contractor in a low-minimum state might be fully legal and still be unqualified for a medical office build-out because the owner requires higher limits, a broader package, and cleaner documentation. The contractor didn't do anything wrong on the licensing side. The problem is that licensure and bid qualification aren't the same test.

Low state minimums can keep a business legal. They rarely guarantee that business is contract-ready.

What contractors should expect by project type

The exact requirement comes from the contract. Still, contractors can think in tiers.

| Project Type | Typical Project Value | Typical GL Limit (Per Occurrence / Aggregate) |

|---|---|---|

| Residential remodel | Varies by owner and contract | Often lower or less formal, depending on owner requirements |

| Small commercial build-out | Varies by owner and occupancy | Often moves toward the common commercial baseline |

| New commercial or public construction | Varies by project and owner | Often aligns with $1,000,000 / $2,000,000 or higher contract structures |

That table is intentionally qualitative in the first two columns because project values and owner demands vary too much to treat them as universal. The useful takeaway is simpler. As project complexity rises, insurance review gets stricter.

Contractors should also watch for excess requirements layered above base liability. Public and institutional contracts may require additional liability sitting above the GL and auto program, which is where umbrella and excess liability coverage becomes part of bid strategy rather than an optional add-on.

A plumbing GC is a good trade example here. The state may allow operation with a lower threshold, but a hospital renovation contract may demand higher GL, auto, workers' compensation compliance, and a structured certificate package before a wrench ever comes off the truck. The contract sets the standard.

Beyond the Basics When to Add Umbrella Coverage and Surety Bonds

A contractor can meet the basic requirements for a smaller job and still be badly exposed on a larger one. That's where umbrella coverage and surety bonds stop looking like extras and start functioning like growth tools.

When umbrella stops being optional

Umbrella or excess liability adds another layer above underlying policies such as GL or commercial auto. It matters when one serious claim burns through the base limit faster than expected.

Use a fleet example. An electrical contractor sends a foreman and a loaded service truck across town to a school project. A major crash injures multiple people and creates property damage. Even with a solid primary auto policy, the total exposure can outrun the base layer. That's exactly the kind of event that turns a limit decision into a business survival issue.

Public and university contracts often build this into the requirement itself. Tufts requires not only $1,000,000 per occurrence and $2,000,000 aggregate in general liability, but also umbrella or excess liability of not less than $5,000,000 per occurrence and aggregate in its vendor and contractor insurance requirements. Contractors pursuing federal or public opportunities also need to pay attention to contract language and procurement rules. For teams working in that lane, this primer on mastering FAR compliance helps explain why documentation standards tighten as project oversight increases.

Why bonds matter even though they aren't insurance

A surety bond is different from insurance. Insurance protects the contractor against covered loss. A bond guarantees to the project owner that the contractor will perform as promised under the contract terms.

That difference matters because some contractors buy the right insurance and still can't bid the job. Public work and larger private projects may require bid bonds, performance bonds, or payment bonds before the owner will award the contract. Those documents signal financial credibility and execution capacity, not just liability protection.

- Umbrella protects against severity: It sits above the primary layer when the underlying limit isn't enough.

- Bonds support qualification: They help owners trust that the job will be completed according to the agreement.

- Growth brings both into play: As work gets larger, owners usually want stronger balance-sheet backing and stronger liability structure.

A contractor expanding into bonded work should understand the mechanics before the bid deadline. This overview of surety bonds for contractors lays out the role bonds play in qualification.

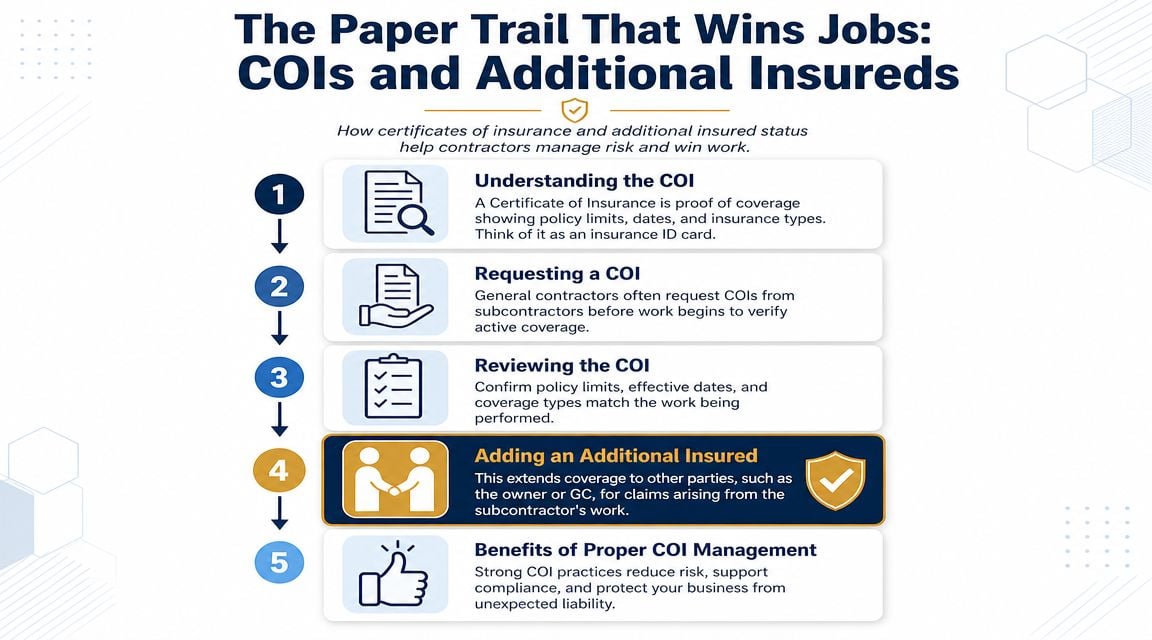

The Paper Trail That Wins Jobs COIs and Additional Insureds

A lot of insurance problems don't start with bad coverage. They start with missing proof.

Once the contract is awarded, owners and upstream GCs usually want paperwork fast. If the contractor can't produce the right certificate, can't show current effective dates, or doesn't have the requested endorsement available, the project may stall before mobilization.

What a COI proves and what it doesn't

A certificate of insurance, or COI, is the summary document that shows what policies are in force, what dates apply, and what limits are listed. It's the insurance ID card for the project file.

For licensed contractors, the paperwork itself can affect compliance. Tennessee requires proof of GL insurance for contractor or home improvement licensing with minimums tied to the contractor's monetary limit, ranging from $100,000 for applicants or licensees up to $500,000, $500,000 for $500,001 to $1.5 million, and $1,000,000 for $1.5 million or more. The certificate must be current and show policy number, effective dates, and limits according to the Tennessee contractor insurance information form.

That's a licensing example, but the same practical lesson applies on projects. A policy that exists but isn't documented correctly can still create a problem.

How additional insured status fits into risk transfer

An additional insured endorsement extends certain protection under one party's policy to another party when the contract requires it. In plain language, it helps formalize risk transfer connected to the work.

For a concrete subcontractor, this comes up constantly. The GC may require the sub to name the GC and owner as additional insureds before the sub pours a foundation. If a claim later arises out of the sub's operations, that endorsement becomes a key part of the risk transfer framework.

The fastest way to look disorganized on a commercial bid is to treat certificates and endorsements like afterthoughts.

A clean process usually looks like this:

- Review the contract early: Pull insurance exhibits before signing.

- Match the request to the current program: Limits, dates, entities, and endorsements should all be checked.

- Request the certificate package promptly: Don't wait until the day before mobilization.

- Confirm named insureds and project details: Wrong entity names create avoidable rejections.

- Store final documents where operations can access them: PMs, accounting, and field supervision often all need the same file.

A contractor that wants to speed this up can work with any responsive advisor that understands construction paperwork. Coverage Axis, for example, states that it provides contractor-focused program reviews and COI turnaround as part of its construction insurance advisory process.

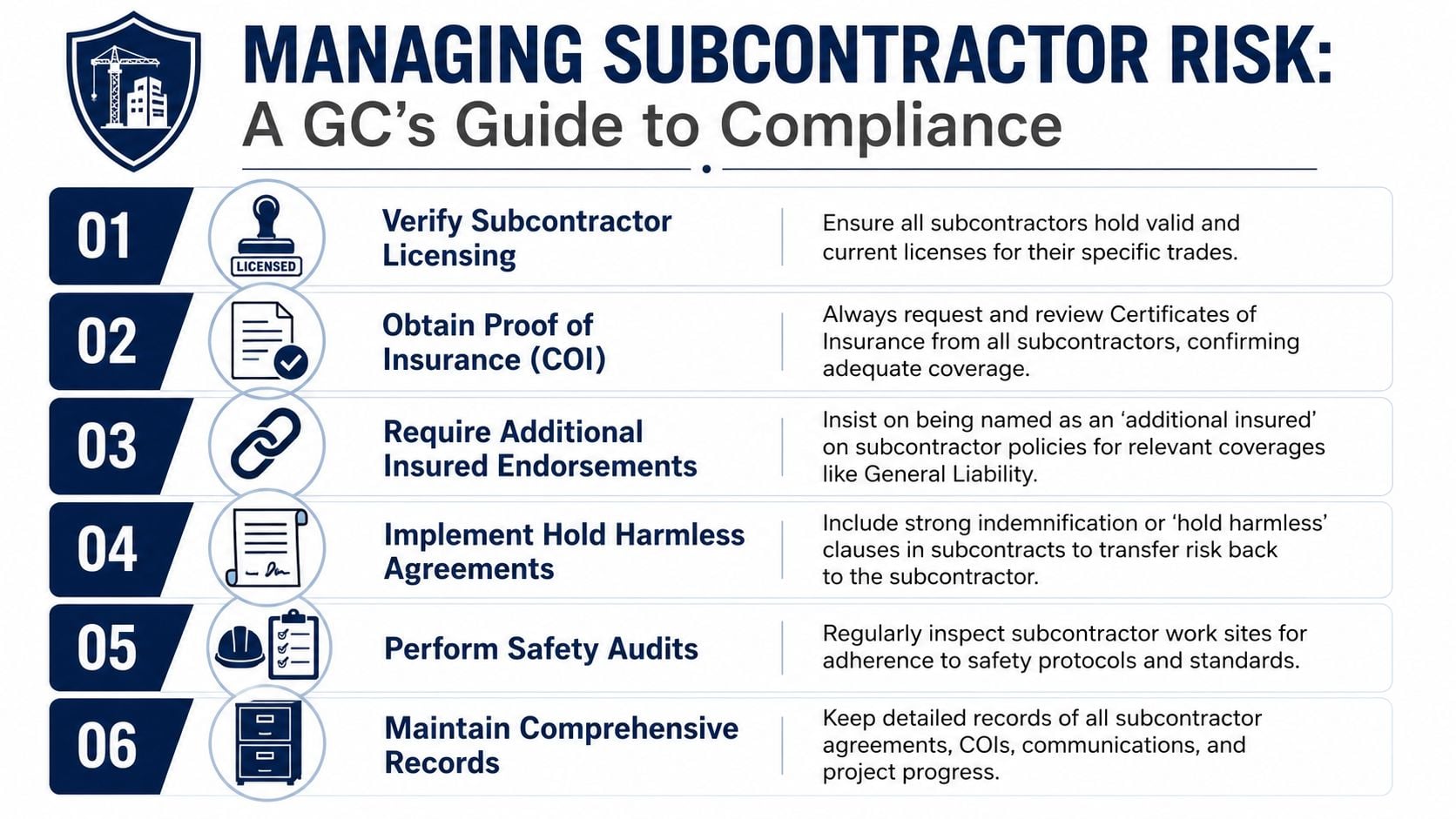

Managing Subcontractor Risk A GC's Guide to Compliance

The biggest insurance leak in many GC operations isn't the GC's own policy. It's the subcontractor file.

If a sub shows up uninsured, underinsured, or with incomplete endorsements, the GC inherits far more risk than expected. That can lead to disputes with the owner, claim friction with the carrier, and expensive finger-pointing after a loss.

A practical firewall around the GC policy

A common breakdown in risk management is failure to verify subcontractor insurance before work begins. Project owners increasingly require GCs to ensure subs carry proper coverage and name the owner as an additional insured. The main issue is having a documented process that verifies and preserves risk transfer before mobilization, as discussed in this write-up on general contractor subcontractor insurance verification.

That's why subcontractor compliance needs to be operational, not occasional. Waiting until after a loss to find out that a sub's policy expired is too late. The GC needs a firewall around its own insurance program, and that firewall is built with contracts, COIs, endorsements, and follow-up.

A masonry trade example shows the point. If a masonry sub damages adjacent property and its coverage was never verified, the owner will still look upstream. The GC then has to fight over who should have paid while the claim is already active.

A subcontractor review checklist that works

The review process doesn't need to be fancy. It does need to be consistent.

- Check the sub's legal entity: The insured name on the certificate should match the subcontracting party.

- Confirm active dates: Coverage needs to be in force before the sub starts and remain active through the work period.

- Review required policy types: If the sub has employees, workers' compensation needs attention. Vehicle use and site exposure also need to match the actual work.

- Compare limits to the contract: A sub doing high-hazard work with thin limits creates obvious problems.

- Require additional insured status where the contract calls for it: The endorsement matters more than verbal assurances.

- Keep records in one place: Contracts, COIs, updated certificates, and correspondence should be easy to retrieve.

- Tie compliance to payment and site access: Subs shouldn't start or continue work with expired paperwork.

Contractors dealing with layered subcontractor exposure can review broader operational issues through this guide to subcontractor liability risk.

A COI collected after the sub starts work is administration. A COI collected before mobilization is risk control.

Get Compliant Get Bidding Your Next Steps

Contractors don't need to memorize every insurance form to get this right. They do need a repeatable process.

The most useful next steps are straightforward:

- Audit the current program: Compare existing policies against the kinds of jobs being pursued now, not the jobs handled two years ago.

- Separate license requirements from bid requirements: State minimums may keep the business legal, but the contract usually decides whether the work can be won.

- Tighten paperwork handling: COIs, endorsements, and named entities should be checked early, not after award.

- Review whether extra layers are needed: Larger jobs often call for umbrella coverage or bonds.

- Formalize subcontractor review: No sub should start without current, verified documentation that matches the subcontract.

For trade business owners trying to grow, insurance becomes practical. Better alignment between policy structure and contract requirements reduces delays, protects the balance sheet, and gives estimators and project managers fewer surprises when a strong opportunity comes in.

If current coverage doesn't match the work being pursued, the next bid can expose the gap fast. Coverage Axis offers free quotes and coverage reviews for contractors who need to check limits, endorsements, subcontractor requirements, or bond readiness before sending out the next proposal.