A contractor lands a solid job, opens the contract, and gets stopped cold by the insurance requirements. The client wants proof of commercial auto coverage before work starts. The trucks are already on the road, the crew is ready, and now the policy quote becomes the bottleneck.

That's where a lot of trade businesses lose time and make bad decisions. They rush, grab the cheapest number, and hope it satisfies the contract. Sometimes it does. Then a claim shows up and the policy turns out to be built for a delivery van, not a contractor hauling tools, rotating crews, and bouncing between jobsites.

A smart commercial auto policy quote does more than check a box. It protects cash flow, keeps jobs moving, and helps the business qualify for better work. The spread in pricing proves the point. Insureon reports annual commercial auto premiums can range from under $375 to over $16,000. That kind of range means the quote can change hard based on vehicles, state, and risk profile.

Contractors already juggle enough. A clear quoting process helps prevent the insurance side from becoming another avoidable mess. It also matters when a contract ties vehicle coverage into broader general contractor insurance requirements, which is common on better-run projects.

Table of Contents

- Your Quote Starts Before the Phone Call

- Assemble Your Contractor's Quote Kit

- How Underwriters Price Your Fleet and Your Trade

- Building a Policy That Actually Protects You

- How to Compare Quotes Beyond the Price Tag

- Binding Coverage and Getting Your COI

Your Quote Starts Before the Phone Call

A plumbing contractor with two vans and one pickup gets a call on a Monday morning. Good client. Good scope. Fast start. Then the contract arrives and says no work begins without proof of commercial auto coverage that matches the job requirements. Suddenly, the issue isn't whether the business has vehicles. The issue is whether the policy quote is built right and can be documented fast.

That's the reality for contractors. Vehicle insurance isn't just an expense line. It's a gatekeeper to revenue. If the quote is sloppy, the certificate gets delayed. If the coverage is thin, the job may start with a hidden liability problem attached to it.

Practical rule: A rushed quote usually creates one of two problems. It either misses a contract requirement, or it misses an exposure from the way the crew actually drives.

A contractor should treat the quote process like pre-job planning. The better the information going in, the better the result coming out. That matters even more for a trade business with mixed vehicle use. One truck may be owned by the company, another may be leased, and a lead tech may use a personal pickup for supply runs. Generic quote forms often miss that.

A painting contractor is a simple example. One van might carry sprayers and ladders. Another worker might drive a personal vehicle between jobsites. The risk isn't just the van itself. The risk includes what's being transported, who's driving, how often stops happen, and whether the business gets dragged into a claim from a non-owned vehicle situation.

The quote starts before the phone call because the quality of the answer depends on the quality of the story the business gives the underwriter. Contractors who understand that move faster and buy better coverage.

Assemble Your Contractor's Quote Kit

Walking into a quote without your information ready is the insurance version of showing up to a remodel without a tape measure. It wastes time, creates bad assumptions, and usually produces a quote that needs to be redone.

A contractor should build a Quote Kit before talking to any advisor or carrier. That kit doesn't need to be fancy. It needs to be complete.

A plumbing company is a good example. If the business does service work during the week and small new construction jobs on the side, that needs to be said clearly. If one van stays local but another runs material across county lines, that matters too. Underwriters don't like blanks, guesses, or vague descriptions.

For contractors working under written agreements, this is also where broader contract language matters. Vehicle obligations often overlap with indemnity language and risk transfer terms, so it helps to understand what contractual liability means for contractors.

Know what the underwriter is trying to understand

An underwriter is trying to answer a simple question. How does this business use vehicles in its operations?

That answer goes beyond make and model. The underwriter wants to know whether the business sends one tech to a single call, rotates several employees through the same truck, tows equipment, stores tools inside vehicles overnight, or relies on personal autos when the schedule gets busy.

A contractor who gives clean, specific information usually gets a cleaner quote with fewer surprises.

What belongs in the kit

The strongest quote kits usually include these items:

Business details: Legal business name, operating address, and basic company information. If the business has multiple locations or yards, that should be clear from the start.

Full vehicle schedule: Every truck, van, pickup, and trailer should be listed with VIN, year, make, and model. If a landscaping company has one dump trailer and one utility trailer, both need to be discussed because towing changes exposure.

Driver list: Include full names, dates of birth, and license details for anyone who may drive. That includes owners, foremen, service techs, and the “occasional” employee who grabs keys when things get hectic.

Current insurance information: If there's an existing policy, have it ready. That helps identify coverage gaps, missing endorsements, and changes the business needs before renewal.

Loss history: Prior claims matter. A contractor should gather loss runs and be ready to explain what happened and what changed afterward. If there was a backing accident in a yard, say what process was added to prevent a repeat.

Operations summary: This is where a lot of contractors undershare. A short, plain-English description works best. For example: residential service plumbing, light commercial tenant work, local travel, tools carried daily, occasional material pickup, no long-haul work.

A short operations summary often improves a quote more than contractors expect. It tells the underwriter whether the exposure is controlled or chaotic.

A roofing company, for example, should mention if crews travel in company trucks, haul compressors or ladders, and move between several jobsites in a day. That profile looks different from a cabinet installer with fewer stops and lighter cargo. Same road. Different risk.

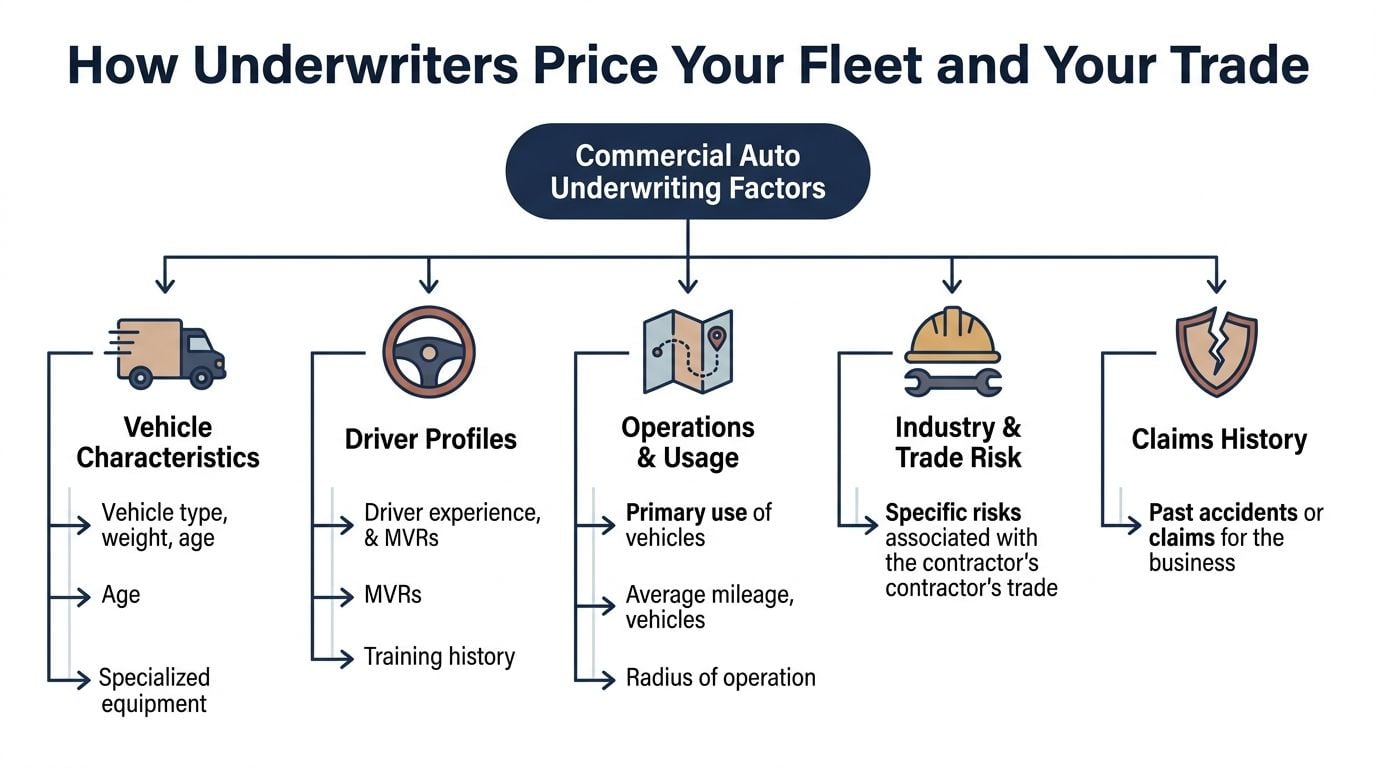

How Underwriters Price Your Fleet and Your Trade

Commercial auto pricing isn't random. Contractors sometimes treat it like a mystery because the premiums can swing hard from one quote to the next. But the logic is usually there. The underwriter is pricing the vehicles, the drivers, and the way the trade uses both.

For contractor classes such as carpenters, electricians, and painters, Progressive Commercial reports a median commercial auto cost of $212 per month. That doesn't mean every contractor should expect that number. It does show that pricing follows patterns when the information is accurate and the operation is understood.

Your vehicles tell part of the story

A painter's van and an excavation truck don't belong in the same mental bucket. Vehicle type changes the severity potential, repair profile, and operating pattern. Heavier units, specialized bodies, and vehicles that tow or haul equipment usually create a different underwriting conversation than a light service van.

A contractor should expect close attention on:

| Factor | Why it affects the quote |

|---|---|

| Vehicle type | A dump truck, service van, and pickup create different road risks |

| Weight and equipment | Heavier vehicles and specialized setups can increase claim severity |

| Trailer use | Towing changes handling, accident exposure, and endorsement needs |

| Cargo carried | Tools, materials, and equipment change the practical risk of each trip |

A landscaping business is a good example. The truck may not look exotic, but once it's towing, carrying equipment, and moving between several stops, the use becomes more complex than many owners assume.

Your drivers and habits tell the rest

Driver quality can help or hurt a quote fast. If a contractor has clean records, a written vehicle policy, and actual oversight of who drives what, underwriters notice. If vehicles are passed around casually and nobody checks records until renewal, underwriters notice that too.

The broader market is also under pressure. Milliman estimated the 2024 commercial auto liability accident-year loss ratio at 80.3% and the countrywide 2024 weighted average calendar-year loss ratio at about 86%, the highest in five years. That's one reason underwriters put real weight on loss-control evidence such as continuous MVR monitoring, telematics, and documented driver training when they decide quote terms.

Clean vehicles don't impress an underwriter if the driving culture is loose.

A contractor doesn't need a complicated safety department to improve results. What matters is consistency. Vehicle inspections, driver screening, training records, and a clear rule on who can use company vehicles all help the account present better.

For businesses that run heavier vehicles or longer routes, practical upkeep matters too. A crew leader reviewing semi truck maintenance tips may not be running over-the-road freight, but the underlying lesson still applies. Documented maintenance supports safer operation, and safer operation supports a better underwriting story.

Trade class changes everything

Contractors often miss how strongly trade class affects the quote. The vehicle isn't evaluated in a vacuum. The carrier asks what the business does.

A roofer often has frequent local travel, tool transport, and crew movement. An electrician may run many short service calls in dense traffic. A concrete contractor may use heavier vehicles with tougher stopping and backing exposures. A painter may have lighter vehicles but higher stop frequency.

That's why generic quote forms fall short. They may ask for a vehicle count, but they don't always capture the practical risk pattern. A strong commercial auto policy quote for a contractor should reflect trade-specific use, not just a registration card and a driver list.

Building a Policy That Actually Protects You

A legal minimum policy and a useful contractor policy are not the same thing. The first one may satisfy a registration requirement. The second one protects the business when the jobsite, the crew, and the road all collide in the same week.

The dangerous move is assuming the cheapest quote is “good enough” because it includes liability, collision, and other physical damage coverage. For many contractors, that leaves obvious gaps. If employees drive personal vehicles for business, if the company leases or borrows vehicles, or if tools move in and out of vehicles all day, the basic form may not reflect the operation.

The cheap quote problem

A cheap quote often wins by cutting where the contractor can't afford a cut. It may leave out Hired and Non-Owned Auto exposure. It may ignore trailer issues. It may insure the truck but leave the business exposed for what happens around the truck.

A simple example makes the point. An HVAC company sends a tech to pick up parts in his own pickup because the service van is tied up. On the way back, he causes an accident while running a work errand. If the business didn't address non-owned auto exposure, the owner may discover too late that the cheapest quote wasn't the cheapest outcome.

The wrong quote saves money only until the first real claim.

This issue shows up in other service businesses too. Operational discipline matters whether a company is dispatching plumbers or managing your moving company. Once employees, schedules, borrowed vehicles, and customer deadlines get involved, auto risk spreads beyond the title on the registration.

The endorsements contractors usually need

Contractors should push past the base policy and ask direct questions about the gaps. The right answer depends on the trade, but several coverage decisions come up again and again.

Hired and Non-Owned Auto liability: This matters when employees use personal vehicles for business, or when the company rents, hires, or borrows vehicles. Contractors with rotating crews and supply-house runs should pay close attention here.

Trailer treatment: A roofer, flooring contractor, or similar trade professional may treat the trailer like an afterthought. That's a mistake. The quote should clearly address how trailers are scheduled or endorsed.

Physical damage choices: Collision and comprehensive protect the vehicle itself. A contractor should decide these based on the unit's value, replacement pressure, and how painful downtime would be.

Tool and equipment gap: The auto policy generally addresses the vehicle, not every tool inside it. Contractors hauling expensive gear should ask how tools and mobile equipment are covered while in transit or at the jobsite.

Acuity's contractor-relevant guidance is useful on this point because it recognizes that commercial auto issues can involve owned, leased, hired, borrowed, and employee-used vehicles. Contractors who skip that discussion end up with a policy built for a simpler business than the one they run.

State rules can change the foundation

Some contractors compare quotes across states as if the baseline should be similar. It isn't. State requirements can change the structure of the quote before the contractor makes a single elective coverage decision.

For example, New York requires specific minimums for bodily injury liability, property damage liability, Personal Injury Protection, and Uninsured Motorist coverage. A contractor quoting there starts from a different foundation than a contractor in a state with fewer mandated coverages.

That matters for interpretation. A business owner shouldn't look at one low number from one state and assume another quote is overpriced. Sometimes the difference is the law. Sometimes it's the trade class. Sometimes it's the endorsement package. Usually it's all three.

For contractors that need a plain-English explanation of the liability side of the form, commercial auto liability insurance basics can help frame the right questions before accepting the proposal.

How to Compare Quotes Beyond the Price Tag

Contractors should collect multiple quotes, then compare them like they'd compare subcontractor bids. Same scope first. Price second. Anything else is a shortcut to a bad decision.

That approach is supported by industry guidance. Insurance.com recommends collecting at least three quotes and targeting about a $1 million combined single limit for liability, while avoiding the mistake of buying state-minimum limits just to lower the premium. That's a practical standard because it forces a real comparison instead of a race to the smallest number.

Use a side-by-side test

A contractor doesn't need a complex spreadsheet. A short checklist works if it's built around the right issues.

| Item to compare | What to look for |

|---|---|

| Liability limit | Are all quotes built on the same limit? |

| Deductibles | Is one quote cheap because the out-of-pocket cost is much higher? |

| Vehicle list | Are all owned units and trailers handled the same way? |

| Hired and non-owned exposure | Included, excluded, or unclear? |

| Physical damage | Same vehicles covered, or different ones dropped? |

| Practical fit | Does the quote match how the trade actually operates? |

A flooring contractor gives a good example. One quote may look cheaper because it ignores the borrowed box truck used during larger installs. Another may look expensive only because it addresses that exposure.

What to challenge before saying yes

Before binding, the contractor should ask direct questions and expect direct answers.

What was excluded to get this price? If the answer is vague, that's a problem.

Does this quote reflect how the crew really drives? A service business with frequent jobsite runs shouldn't accept a quote built like a low-mileage office account.

What happens when employees use personal vehicles for company errands? If the proposal doesn't address it, the contractor should keep pushing.

Will this satisfy contract requirements without last-minute fixes? Cheap quotes often become expensive when endorsements must be added under time pressure.

For contractors who need a quick refresher on limit structure, combined single limit coverage explained helps separate meaningful protection from low-limit window dressing.

A good quote should survive tough questions. If it falls apart under basic scrutiny, it doesn't belong on a working contractor's balance sheet.

Binding Coverage and Getting Your COI

Once the contractor picks the right quote, the next step is binding coverage. That means the application gets finalized, details get confirmed, and the initial payment is handled so the policy can go active.

What binding actually means

At this stage, accuracy matters. The named insured has to be correct. The vehicle schedule has to be correct. Drivers, garaging, business use, and requested coverages should all match reality. Contractors who rush this step sometimes create their next claim problem before the policy even starts.

A straightforward process helps. Some contractors work through a broker or advisor that handles market outreach and placement. Coverage Axis, for example, offers commercial insurance quote support for contractors and handles carrier shopping as part of that workflow. What matters most is that the contractor gets a clear final proposal and confirms the details before binding.

Get the certificate right the first time

After binding, the contractor usually needs proof fast. That proof is the Certificate of Insurance, or COI. The certificate should match the contract requirements, list the correct certificate holder, and reflect any required wording.

A contractor should check the COI before sending it. If the client requires specific language, the request needs to be clear up front. If the wrong entity is listed or a required endorsement is missing, the job can still get delayed even though the policy is active.

For contractors who want to see how certificates are structured, a certificate of insurance template for construction use is a useful reference before the request goes out.

Coverage Axis offers free commercial auto quote help and coverage reviews for contractors who need a policy that matches how the business runs. A quick review can help identify gaps around hired and non-owned exposure, trailers, tool transport, and contract requirements before they become claim problems. Contractors who need a faster quote, cleaner COI process, or a second opinion can request a free review through Coverage Axis.