A contractor can do excellent work, sharpen pricing, and still lose a job before the first truck rolls out. It happens in the insurance requirements page of the contract.

A skilled electrical contractor bidding a commercial renovation often sees the same pattern. The scope looks solid. The timeline is manageable. Then the bid package asks for a certificate of insurance template with specific wording, exact holder details, listed limits, and endorsements that must be in place before mobilization. At that point, the COI stops being office paperwork and becomes part of the deal itself.

For contractors, the certificate of insurance template is the last visible step in a contract negotiation. It tells the owner or GC whether the insurance program behind the bid can support the promises in the contract. If the certificate is wrong, incomplete, or backed by the wrong policy terms, the contractor can get delayed, rejected, or pulled into a claim that should have been transferred elsewhere.

Table of Contents

- Why Your Certificate of Insurance Is More Than Just Paperwork

- Breaking Down the Certificate of Insurance Template Field by Field

- How to Fill Out Your COI to Meet Contract Requirements

- Adding Additional Insured, Waivers, and Other Key Endorsements

- What Insurance Limits Do You Actually Need

- Avoid These Common COI Mistakes

Why Your Certificate of Insurance Is More Than Just Paperwork

An electrician bidding a tenant improvement project might think the hard part is pricing conduit runs, panel upgrades, and labor. The harder part sometimes shows up in a few contract lines that require primary coverage, additional insured status, waiver language, and proof before any work starts.

That's why the certificate of insurance template matters so much. It gives the project owner a fast way to check whether the contractor's insurance setup matches the risk transfer terms in the contract. If the template doesn't support those terms, the bid can look noncompliant even when the workmanship and pricing are strong.

The COI is part of pre-job risk transfer

The historical role of the certificate of insurance template is tied to risk-transfer requirements that expanded as third parties increasingly asked contractors to document coverage before work started. Institutional checklists now show how specific acceptance standards can be. For example, the insurer is typically expected to be licensed and admitted in the state, carry an A- or better AM Best rating, and issue primary, not excess or contributory, coverage, according to this university risk management COI checklist.

That sounds technical, but the business meaning is simple. The owner wants to know who pays first if there's a loss, whether the carrier is acceptable, and whether the contractor can satisfy the contract without arguments after an incident.

A framing contractor or electrical subcontractor that works through lower-tier subs has even more at stake. If a sub causes an injury or property damage event, weak documentation can unravel the intended transfer of liability. That's why many contractors build a separate review process around subcontractor liability exposure, not just their own outgoing certificates.

Practical rule: A clean-looking COI doesn't win the job by itself. A COI that accurately reflects contract-ready coverage does.

Why owners care about speed and precision

Most owners and GCs don't want a stack of full policy forms during bid review. They want a one-page snapshot they can scan quickly. The certificate became important because construction procurement moves fast. Vendor onboarding, public work compliance, and jobsite access often depend on whether the right certificate lands in the inbox with the right names, dates, limits, and wording.

A contractor who treats the certificate of insurance template as an afterthought usually finds out too late that the insurance requirement wasn't a clerical item. It was a bid qualification issue.

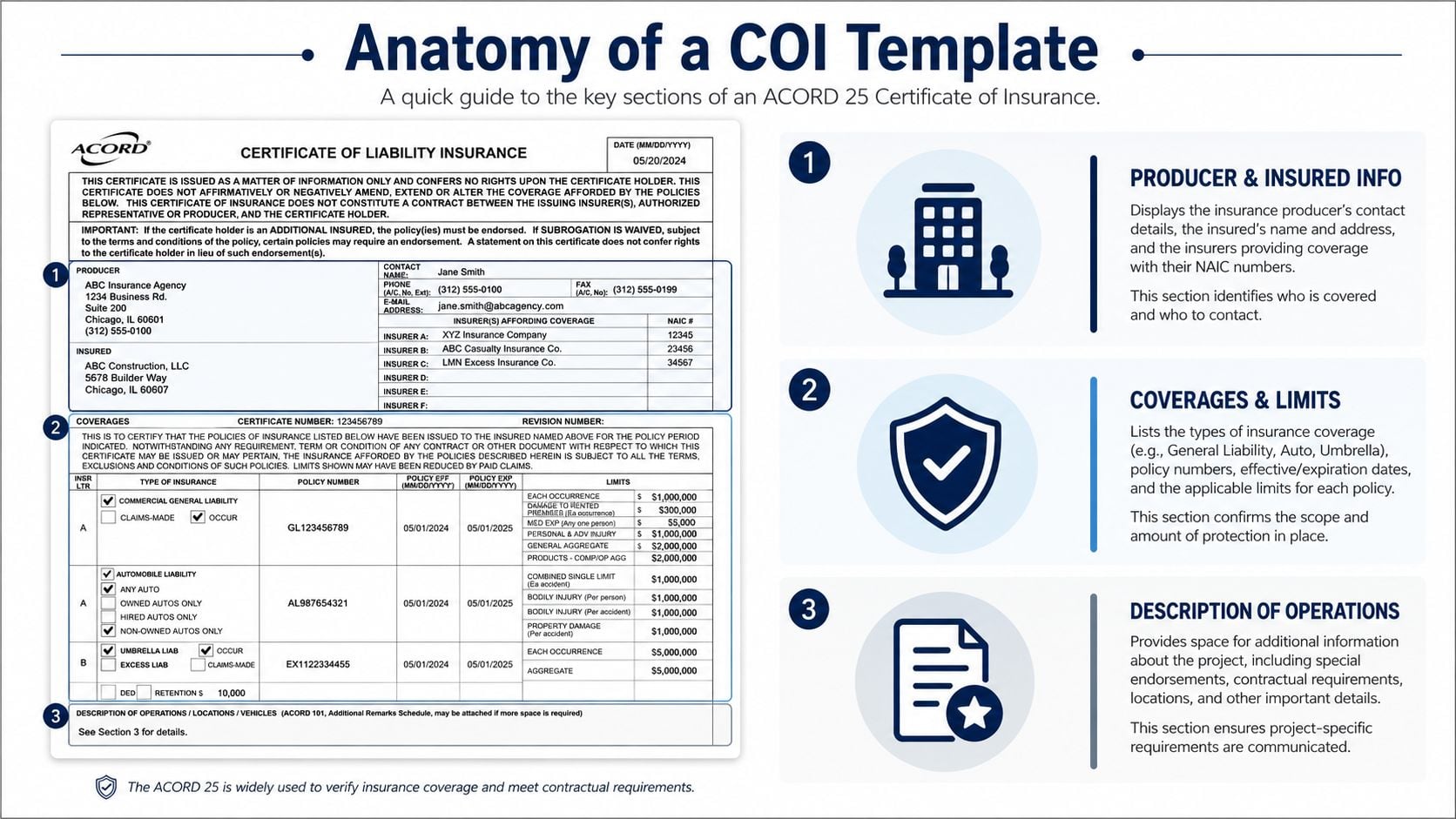

Breaking Down the Certificate of Insurance Template Field by Field

Most contractors run into the same liability certificate format over and over. It's the standard ACORD-style layout recognized across major markets. Once a contractor understands what each box means, the form becomes easier to review and harder to get wrong.

The template is built for speed

Modern COI forms commonly show the insured's name, policy number, policy effective date, policy expiration date, coverage type, limits, and certificate holder on a single page. Guidance also emphasizes that the certificate is only evidence of coverage and doesn't alter the underlying policy terms. For contractors, precise numbers often decide acceptance. A holder may require commercial general liability at $1,000,000 per occurrence and $2,000,000 aggregate, automobile liability at $1,000,000 combined single limit, and workers' compensation with employer's liability at $100,000/$500,000/$100,000, as outlined in this contractor COI requirements reference.

For a contractor trying to bid larger jobs, those fields aren't random blanks. They are the visible proof that the insurance program meets the contract.

What each section means on a real job

Take an electrical contractor on a commercial renovation. The GC asks for a certificate before site access. Here's what the major fields mean in plain language:

- Producer means the insurance agent or broker issuing the certificate. This is the office the GC may contact when something looks off.

- Insured is the contractor's legal business name and address, exactly as shown on the policy. If the LLC name is wrong, the certificate can be rejected.

- Insurers affording coverage lists the carriers behind each coverage line. This matters when a contract requires an acceptable admitted carrier.

- Coverages show what policies are in force, often including general liability, auto, umbrella, and workers' compensation.

- Policy number and dates confirm that coverage exists for the job period shown on the contract.

- Limits show the ceiling the carrier may pay, subject to the actual policy terms.

- Certificate holder is the party asking for proof. On a renovation, that could be the owner, the landlord, the GC, or a combination spelled out in the contract.

- Description of operations is where project-specific wording often appears, including location details or required endorsements.

A contractor reviewing these fields should also understand common terms. Per occurrence refers to the limit for a single covered event. Aggregate refers to the total available for covered claims during the policy period.

For many trade contractors, the quickest way to understand whether those liability lines are reasonable is to compare them against the scope of work and the business's general liability coverage needs.

On a real project, the smallest box on the certificate can create the biggest delay. A missing suite number in the certificate holder name can hold up compliance just as fast as a missing coverage line.

A blank certificate of insurance template can be useful as a reference, but it shouldn't be treated as a fill-it-yourself exercise unless the contractor is working directly with the issuing insurance professional and the underlying policy documents at the same time.

How to Fill Out Your COI to Meet Contract Requirements

The fastest way to produce a bad certificate is to start with last month's COI and swap names. That shortcut causes rejected certificates every week.

A contractor filling out a certificate request for a new job should work from the contract and the policy declarations page together. For an electrical contractor on a commercial renovation, that means reading the insurance requirements page before asking the office to issue anything.

Start with the contract, not the form

A practical workflow is straightforward. Confirm the certificate holder's exact legal name and project role. Verify the insured's legal entity and mailing address. Match the policy number, effective and expiration dates, and coverage type to the underlying policy. Check that the limits shown meet the contract. Then verify that requested endorsements such as additional insured or waiver of subrogation are attached to the policy, as outlined in this COI workflow guide.

For a renovation project, the electrician's office should pull these details from the contract first:

- Legal name of the holder. If the contract names the ownership entity, that exact entity belongs on the certificate.

- Project identity. If the owner wants the address, building name, or project number listed, it belongs in the operations box.

- Required coverages. General liability, auto, workers' comp, and umbrella are common asks.

- Required wording. Many contracts ask for additional insured, waiver of subrogation, and primary wording.

A GC's requirements for a larger renovation often line up with what many general contractors require from subs, especially when multiple trades are on site and losses can cascade across contracts.

Match the form to the policy

The second half of the job is accuracy. The certificate should never promise coverage that doesn't exist in the policy file.

A contractor's office should verify the following before issuing:

- Business entity match. If the policy is written to “Bright Line Electric LLC,” the certificate can't be issued to a trade name only.

- Active dates. If the policy renews mid-project, the certificate still has to show a current policy period.

- Coverage lines. A pickup truck used for service calls belongs under commercial auto, not under general liability.

- Limits match the contract. If the contract requires higher limits than the policy carries, the certificate won't fix that problem.

A certificate should be the summary of a completed insurance decision, not a substitute for one.

A common field error happens in the certificate holder section. A contractor copies the GC's marketing name from an email signature instead of the legal entity listed in the contract. Another happens when the office uses a prior project description and leaves the wrong address in the form. Both mistakes can trigger rejection even if the policy itself is fine.

The right approach is slow for a few minutes and fast afterward. Pull the contract. Pull the declarations page. Match every line. Then issue.

Adding Additional Insured, Waivers, and Other Key Endorsements

Most COI disputes don't come from the top half of the form. They come from the wording in the lower description box and from the endorsements that wording is supposed to reflect.

A drywall sub, plumber, or electrician can send a certificate that looks complete, but if the policy doesn't include the required endorsement, the contractor may still fail compliance. That's where jobs stall and claims get messy.

The wording box is where deals stall

ACORD-style samples repeatedly state that the certificate is issued “as a matter of information only,” “confers no rights upon the certificate holder,” and “does not amend, extend or alter the coverage afforded by the policies.” That legal distinction matters because the certificate can omit endorsements, exclusions, or additional insured wording that the contract requires, as shown in this sample liability certificate language.

That means typing “additional insured” into the description box doesn't create additional insured status. The policy has to carry the endorsement.

What these endorsements actually do

Contractors hear these phrases constantly. They need plain-English meaning.

- Additional insured. This generally allows the upstream party, such as the GC or owner, to seek protection under the contractor's liability policy for claims arising from the contractor's work.

- Waiver of subrogation. This generally means the insurer gives up certain recovery rights against the party named in the waiver after paying a covered claim, subject to the policy and endorsement terms.

- Primary and noncontributory. This generally means the contractor's policy is intended to respond before the upstream party's policy, again if the policy endorsements support that arrangement.

For a roofing contractor, this can be the difference between a contract that transfers a jobsite water intrusion claim as intended and a contract that leaves everyone fighting about whose insurance should respond first. For a fleet-based specialty contractor, umbrella or excess coverage can become part of that same discussion when the job requirements exceed the primary policy structure. Contractors dealing with larger loss potential usually need to understand how umbrella and excess liability fit above the primary layers before the certificate request arrives.

Field note: If the contract requires an endorsement, the endorsement page matters more than the wording typed into the COI.

The trade-off is practical. Some contractors want to keep policies simple and low-cost. Larger project owners want stronger transfer language. The certificate of insurance template sits at that intersection. It doesn't resolve the negotiation. It reveals whether the negotiation is backed by the insurance program.

What Insurance Limits Do You Actually Need

A lot of contractors carry the same limits for years because those limits worked on smaller jobs. Then they start bidding schools, municipal work, retail buildouts, multifamily rehabs, or fleet-heavy service contracts and find out the market they're entering expects a different insurance profile.

For contractors, the better question isn't “What number goes on the COI?” It's “What limits and coverage structure let the business bid the jobs it wants without scrambling every time a contract arrives?”

Why the same limits don't fit every trade

An electrician wiring tenant improvements has a different exposure profile than a roofer working at height or a lawn care business sending multiple vehicles and trailers out daily. A plumbing contractor doing ground-up multifamily also faces a different claim pattern than a one-crew finish carpentry shop.

That's why insurance decisions should line up with:

- Type of work performed

- Project size and owner sophistication

- Vehicle use and fleet exposure

- Subcontracted work

- Payroll and workers' comp obligations

Workers' comp is part of this conversation even when owners focus first on liability lines, because payroll growth and crew size can change the whole risk profile. Contractors reviewing limits should also check how workers compensation coverage fits the jobs they're pursuing.

Typical Insurance Limits by Contractor Trade 2026

The table below is a practical planning tool, not a statement of legal requirements. Where a contract sets the requirement, the contract controls. Where a carrier or owner asks for more, the contractor has to decide whether that work justifies the increased insurance cost.

| Trade | General Liability Per Occurrence / Aggregate | Commercial Auto Combined Single Limit | Umbrella/Excess Liability |

|---|---|---|---|

| General Contractor | Often driven by contract requirements | Often required when vehicles are used in operations | Common on larger or higher-risk projects |

| Electrician | Often driven by tenant improvement, commercial, or public work requirements | Often required for service vans and job travel | Frequently considered when moving into larger commercial work |

| Plumber | Often driven by project size and completed operations concern | Often required for vans and tool transport | Often considered for larger residential and commercial jobs |

| Roofer | Often scrutinized closely because of height and property damage exposure | Often required if crews operate company vehicles | Commonly considered because claim severity can be higher |

| Landscaper | Often shaped by premises, equipment, and third-party injury exposure | Often important due to trucks, trailers, and mobile equipment movement | Considered as operations scale or municipal work grows |

A contractor doesn't need the maximum structure for every job. But a contractor who wants smoother bid compliance does need a program built for the level of work being pursued.

Avoid These Common COI Mistakes

Most certificate problems aren't complicated. They're small errors with expensive consequences.

A contractor can lose days waiting on a corrected certificate, miss a mobilization date, or discover after a loss that the policy never matched the wording sent to the project owner. The best practice is a checklist-based review: compare contract-required limits against the COI, then request carrier-issued endorsements before mobilization. Public sample certificates also make clear that the certificate is issued for information only and confers no rights on the holder, which is why the review can't stop at the form itself, as shown in this sample COI and review guidance.

The mistakes that hold up jobs

Some mistakes show up constantly in contractor files:

- Wrong certificate holder name. A legal entity mismatch can trigger immediate rejection.

- Old project details. Reused forms often carry the wrong address, job name, or owner.

- Promised endorsements without policy support. This is one of the biggest gaps between appearance and actual compliance.

- Missing endorsement pages. Some owners don't just want the certificate. They want evidence that the endorsements exist.

- Expired dates or renewal gaps. A certificate tied to an old policy period won't satisfy a current contract.

- Using the certificate as proof of everything. It isn't. The policy and endorsements still control.

A concrete trade example makes this easy to see. A plumbing subcontractor gets approved on a fast-moving apartment renovation. The office sends a certificate listing the GC as additional insured in the description box. A water loss occurs later, and the GC asks for defense under the plumber's policy. If the endorsement was never issued, the certificate wording won't create the protection the GC expected.

Clean formatting does not equal compliant coverage.

Use a review process before anyone mobilizes

Contractors that handle COIs well usually build a short internal review before field crews leave the yard.

That review should include:

- Contract check. Compare the bid award or subcontract insurance exhibit against the certificate request.

- Policy check. Confirm the active policy, dates, entities, and limits.

- Endorsement check. Make sure additional insured, waiver, and primary wording are supported where required.

- Project check. Confirm holder name, address, project number, and operations wording.

- Final issuance check. Send the certificate and any required endorsement evidence together.

Some contractors handle this through their agent, some through an internal admin process, and some use an outside advisor. Coverage Axis is one option for contractors that need coverage review, market shopping, and certificate support built around construction accounts.

A certificate of insurance template should make contract compliance easier. When the underlying insurance program is wrong, the template only exposes the mismatch faster.

Contractors who want fewer rejected certificates, cleaner bid submissions, and insurance that matches the work they're taking on can request a free quote or coverage review from Coverage Axis. A review can help confirm whether current policies, limits, and endorsements are set up to issue compliant COIs when the next job is on the line.