A lot of contractors run into the same problem at the same stage of growth. The crew is solid, the project is a good fit, and the numbers work. Then the insurance requirements page shows up and the job asks for liability limits that sit well above the contractor's current program.

That's usually the moment commercial umbrella insurance stops sounding optional.

For construction businesses, this coverage isn't just about buying “more insurance.” It's about keeping a bad claim from reaching company assets, keeping a certificate from holding up a contract, and keeping a promising bid from dying in the office instead of on the jobsite.

Table of Contents

- Your Next Big Job Requires More Than Standard Insurance

- What Commercial Umbrella Insurance Actually Is

- Real Claims That Exhaust Contractor Liability Limits

- Meeting Contract Demands with Umbrella Coverage

- Umbrella Policy Costs Limits and Common Exclusions

- How Much Umbrella Coverage Does Your Business Need

- Get the Right Umbrella Policy for Your Trade

Your Next Big Job Requires More Than Standard Insurance

The bid package is sitting open on the desk. A concrete contractor has the manpower, equipment, and field supervision to take on a larger commercial site package. Then the insurance section shows a liability requirement that's higher than the current program.

That gap blocks more jobs than many owners expect.

A standard liability setup often starts with $1 million per occurrence on the underlying policy, and commercial umbrella insurance is commonly used to add another layer above it rather than rebuilding the whole program from scratch, as explained in this overview of general contractor insurance requirements. For contractors trying to move from smaller private jobs into larger commercial work or public work, that extra layer often becomes a practical business tool instead of a back-office purchase.

A framing contractor, for example, might be fine on small tenant improvements and light residential work. The same company can get screened out fast when a school project or mixed-use development asks for limits that exceed the current certificate. The crew's capability didn't change. The contract threshold did.

Practical rule: If the insurance requirement is stopping a qualified contractor from bidding, the insurance program has become a growth issue, not just a protection issue.

The same logic applies to risk control on active jobsites. A contractor can do a lot right and still get hit by a severe third-party injury claim, a major vehicle loss, or a subcontractor-related lawsuit that puts pressure on the primary liability limit. Contractors already working on mastering project risk in construction know that paperwork, site controls, traffic flow, and subcontractor oversight all matter. Umbrella coverage sits on the financing side of that same conversation. It's what helps when prevention fails.

For many trade businesses, the question isn't whether bigger jobs carry bigger exposure. It's whether the current insurance program is built to survive that exposure and satisfy the contracts tied to it.

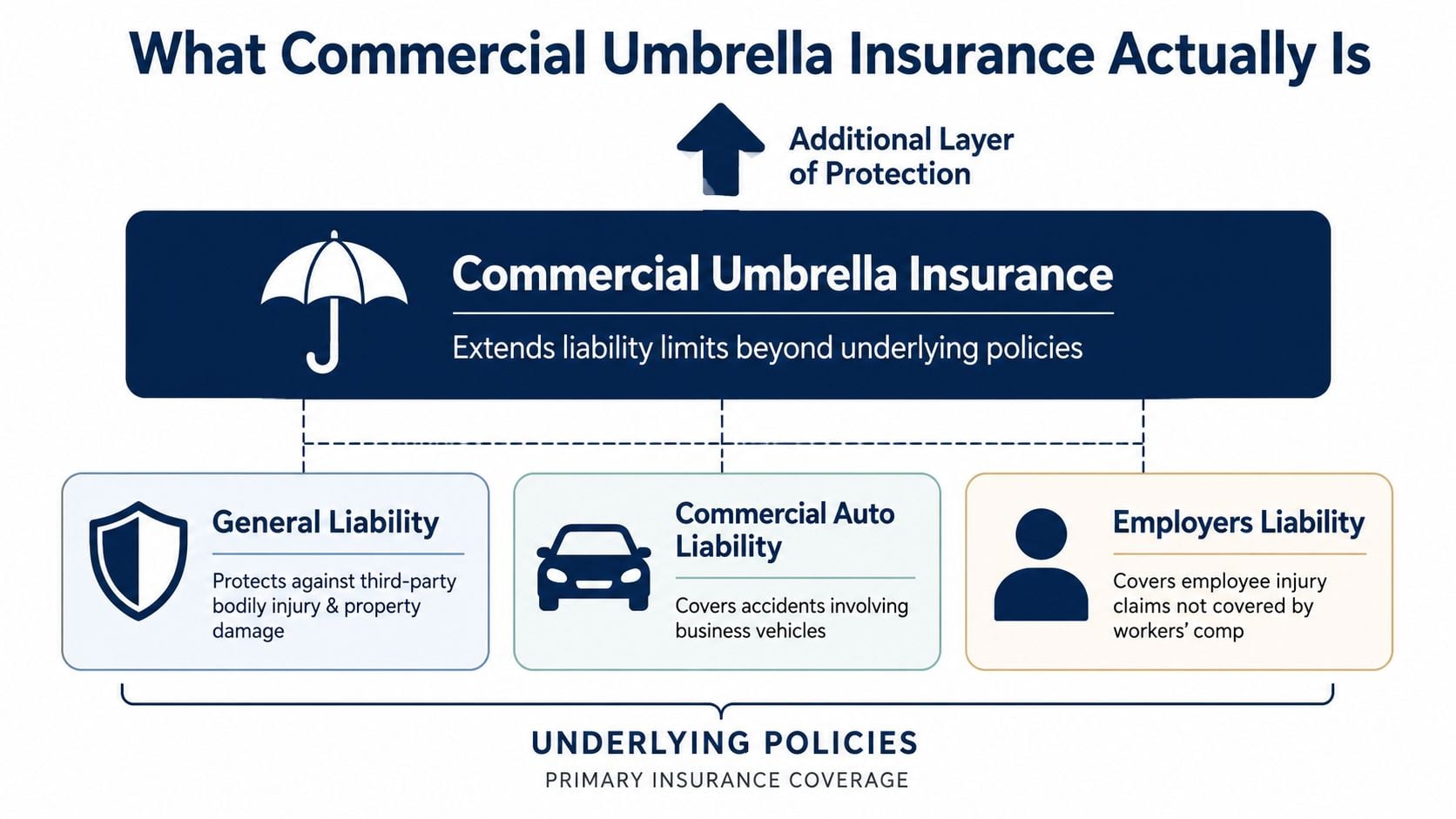

What Commercial Umbrella Insurance Actually Is

Commercial umbrella insurance is best understood as a second liability roof built over key parts of a contractor's existing insurance program. It doesn't replace the foundation. It sits above it.

According to this commercial umbrella explanation, the base liability layer for contractors usually starts with general liability. From there, umbrella coverage can extend over the scheduled underlying policies in the program.

The simple way to think about it

For contractors, the core idea is straightforward. The primary policy pays first. The umbrella layer doesn't come into play until that underlying limit has been used up.

Commercial umbrella insurance is described as an excess liability layer that sits above scheduled underlying policies, typically general liability, commercial auto, and employer's liability, and it activates only after the primary policy's limit is exhausted, according to Travelers' overview of commercial umbrella coverage.

That structure matters in construction because many severe claims are low-frequency events. A company can go years without a catastrophic loss, then have one bad accident that puts immediate pressure on the primary liability limit.

The policy structure is easier to understand visually:

A plumbing contractor offers a good trade example. If one of the company trucks causes a severe road accident while hauling material to a site, the commercial auto liability policy responds first. If the covered loss pushes beyond that underlying limit, the umbrella layer is built to respond above it.

Where contractors get tripped up

Many buyers make the wrong assumption. They hear “umbrella” and think it means broad backup coverage for anything liability-related.

It doesn't work that way.

Some policies are true umbrella forms and may be broader in certain situations. Others operate more like follow-form excess. In practical terms, contractors should assume the umbrella follows the structure of the underlying program unless the policy language says otherwise. If the underlying policy excludes the claim, is missing a needed exposure, or wasn't set up properly, the umbrella may not respond the way the contractor expected.

Umbrella coverage is only as useful as the policies underneath it and the way those policies were structured.

That's especially important for trades with hired or non-owned vehicle exposure, subcontractor-heavy operations, or employer's liability concerns tied to labor-intensive work. A drywall contractor with a busy fleet and multiple subcontract crews may think the umbrella solves every gap. It won't. It adds limit above covered underlying exposures. It does not cure a poorly assembled liability program.

Real Claims That Exhaust Contractor Liability Limits

A liability limit looks large until a real loss starts stacking medical bills, legal costs, property damage, and multiple injured parties into one file. Construction claims don't have to be common to be dangerous. They only have to be severe once.

For contractors reviewing their program, it helps to compare those scenarios against typical general liability coverage limits, then ask where a major loss could break through the primary layer.

HVAC water damage on a tenant build-out

An HVAC contractor finishes work in a commercial space. The job closes out. Weeks later, a slow leak tied to the installation causes hidden water intrusion behind finished walls and above a drop ceiling.

The claim gets worse before anyone catches it. Building materials are damaged, neighboring suites are affected, and mold remediation drives the dispute into a much larger loss than the contractor expected. This is the kind of claim that teaches a hard lesson about severity. The original issue may look small. The resulting third-party property damage can become large fast.

A mechanical contractor can manage quality control well and still face this kind of allegation. Umbrella coverage matters when the claim grows beyond what the base liability layer was built to absorb.

Roofing debris and a street-level crash

A roofing crew is working several stories up on a commercial building. Weather shifts. Materials that were staged but not secured properly get pulled toward the edge.

What happens next turns a site issue into an auto liability event. Debris hits the street, drivers react, vehicles collide, and several people are injured. The roofing company is now dealing with bodily injury claims, property damage, and a lawsuit built around one chaotic sequence.

On urban jobs, a contractor's risk doesn't stop at the roof edge. It drops to the sidewalk, the roadway, and anyone passing below.

This is one reason contractors with vehicle exposure and public-facing jobsites often buy umbrella coverage even when they haven't had a major loss before. A severe claim doesn't need a pattern. It only needs a bad day.

Excavation work and a utility strike

An excavation subcontractor starts trenching on a busy site. A line is struck. The incident causes a violent chain of damage that reaches beyond the immediate dig area.

Now the claim isn't just about repair costs. Third-party injuries are involved. Adjacent property damage becomes part of the file. Project delay allegations may follow, even if those elements fall into different coverage discussions. The liability piece alone can put serious pressure on the underlying limits.

An excavation contractor, utility contractor, or sitework firm faces this kind of severity because so much of the work happens around unseen hazards. The loss can be rare and still be business-changing.

Here's the practical point. Commercial umbrella insurance earns its keep on these ugly claims. Not the routine slip, not the minor fender bender, not the everyday complaint. It's built for the catastrophic file that threatens retained earnings, future payroll, and the company's ability to keep operating after the dust settles.

Meeting Contract Demands with Umbrella Coverage

A contractor can have a clean loss history, solid safety meetings, and a bid that pencils out. Then the contract lands on the desk and requires higher liability limits than the current program can show.

That is often the point where umbrella coverage moves from optional to practical.

On larger commercial work, owners and general contractors are not only buying labor and materials. They are buying financial backstop. If a major injury, vehicle loss, or completed-operations claim hits the project, they want every trade on site to bring enough liability capacity to stand behind its work. For many contractors, the fastest way to meet that requirement is adding an umbrella over the policies already in place instead of rebuilding every underlying limit from scratch.

That matters when a contractor is trying to move up in job size. A framing contractor that has done custom homes may want school, multifamily, or light commercial work next. A concrete subcontractor may be ready to bid municipal projects. In both cases, the insurance requirement can become the gatekeeper before price, schedule, or experience even get full consideration.

Why contract compliance is more than a higher number on the certificate

A lot of contractors focus on the certificate first. I understand why. The certificate is what gets requested in the pre-award scramble. But certificate review is where weak policy structure gets exposed.

The question is whether the umbrella lines up with the underlying liability policies and the contract terms.

Two phrases show up over and over in construction agreements:

- Additional insured means the owner, GC, or another upstream party is added to parts of your liability protection. This guide to the additional insured endorsement explains how that status works in construction contracts.

- Primary and non-contributory usually means your policy is expected to respond first before the other party's insurance is asked to contribute.

Those requirements sound administrative. They are not. They affect how the claim is supposed to be handled after a loss, and they can decide whether your insurance package satisfies the contract review in the first place.

A paving contractor is a good example. The company may buy extra umbrella limit to hit the required total. But if the underlying general liability policy does not carry the right additional insured wording, or if the umbrella does not follow the underlying structure the way the contract expects, the submission can still get kicked back by the GC or project owner.

Where contractors get tripped up

Umbrella insurance helps meet contract demands, but it does not fix bad paperwork or policy mismatches by itself.

Common problems include underlying limits that are lower than the umbrella requires, endorsements that do not match the contract, excluded exposures that matter to the trade, and auto liability that is too light for a contractor with trucks on the road every day. I see this most often when a business grows faster than its insurance program. The company starts chasing bigger work, but the policy structure still looks like it was built for smaller private jobs.

That gap can cost real opportunities. Some contractors lose time in bid review. Others get asked for revised insurance terms after award. In the worst case, they sign a contract they cannot fully support with the coverage they bought.

A certificate does not create coverage. It only reflects what the policies and endorsements already provide.

That is why umbrella coverage should be treated as part of a bidding strategy. Contractors use it to satisfy contract limits, support indemnity obligations that are being pushed downstream, and show they are ready for larger, more loss-sensitive work. The right umbrella limit is not only about surviving a catastrophic claim. It can also be what gets a contractor through prequalification and onto a better class of projects.

Umbrella Policy Costs Limits and Common Exclusions

A contractor pricing umbrella coverage is usually weighing two job decisions at once. One is risk. The other is growth.

If a $5 million umbrella helps the company qualify for a school project, satisfy the GC's insurance schedule, and protect the balance sheet from a severe auto or jobsite injury claim, the premium has to be judged against that opportunity. Looking only at the annual cost misses the point.

What drives umbrella cost and available limits

Umbrella pricing is usually efficient compared with trying to stack much higher limits into every underlying policy. But there is no flat contractor rate that applies across the board.

Underwriters price this coverage based on the exposures most likely to burn through the primary layers. Fleet size matters. Driver quality matters. Payroll, subcontracted work, claim history, territory, and trade class matter. A concrete contractor with multiple trucks, pump operations, and public road exposure presents a different risk than a drywall contractor working mostly on interiors.

The structure of the underlying program matters too. If the carrier sees weak primary limits, loss-heavy autos, or policy terms that do not line up cleanly under the umbrella, pricing can climb and capacity can tighten.

Many contractors also miss a basic point on auto. The umbrella does not replace the primary auto liability setup. It sits over it. If you are reviewing how the auto base limit is written, this guide to combined single limit on a business auto policy helps clarify what the umbrella is sitting on top of.

Available umbrella limits often start at $1 million and go up from there, but the practical ceiling depends on the account. A smaller specialty trade with clean losses may be able to add capacity without much friction. A contractor with severe auto claims, difficult operations, or prior losses may find that each added layer gets more expensive and harder to place.

Where umbrella coverage stops

Umbrella insurance is extra liability capacity. It is not a repair kit for gaps lower down in the program.

If the underlying policy does not cover the exposure, the umbrella may not respond the way the contractor expects. In some situations, the umbrella can require the insured to absorb a retention before it pays on a claim that is not covered by the underlying policy. That is one reason I tell contractors to read the exclusions before they focus on the limit.

The exclusions that cause the most trouble in construction are usually predictable:

- Defective work and damage to your own work: Umbrella coverage does not turn poor workmanship into an insured loss.

- Professional liability exposures: Design-build responsibility, layout errors, engineering advice, and trade-specific consulting work often need separate coverage.

- Uninsured or misaligned underlying policies: If the umbrella is scheduled over general liability, auto, and employer's liability, those policies need to exist and carry the required limits.

- Pollution, mold, and similar specialty exposures: These are common problem areas for restoration, remediation, HVAC, and certain civil contractors.

- Employment-related claims and intentional acts: Large claim size does not change the exclusion.

Here is the field version of that problem. A restoration contractor buys more umbrella because the company is taking on larger water-loss jobs. One project turns into a mold dispute with allegations of bad drying protocol and professional judgment errors. If the base program does not properly address mold, pollution, or professional services, the umbrella limit sitting above it may do very little. The contractor paid for more headroom, but the hole is in the floor, not the ceiling.

That is why cost and exclusions have to be reviewed together. A cheap umbrella that does not track the contractor's real exposures can satisfy a certificate request and still leave the business exposed where severe claims happen.

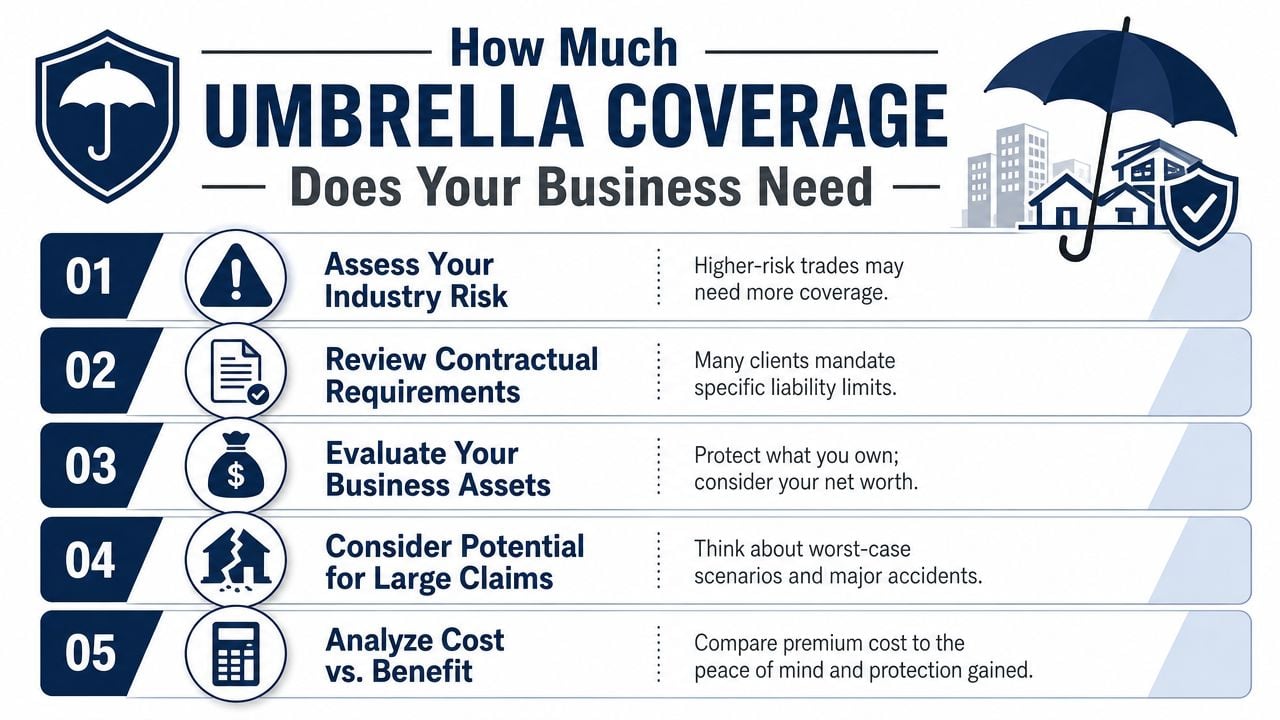

How Much Umbrella Coverage Does Your Business Need

The right umbrella limit is a business decision tied to exposure, contract demands, and how the company operates. Company size alone doesn't answer it.

Market guidance often notes that small to mid-sized businesses commonly carry $1 million to $5 million in umbrella coverage, but the more useful question is whether that limit matches fleet size, project type, and contract terms, as described in Chubb's discussion of commercial umbrella liability.

A practical decision framework

A contractor doesn't need a complex spreadsheet to start this review. The better approach is a disciplined set of questions.

-

What's the highest limit in the contracts being pursued?

If the goal is to bid municipal work, healthcare projects, or larger negotiated commercial work, the insurance requirement should set the minimum target. -

How much road exposure does the company create?

A trade business with more vehicles, more drivers, and more windshield time usually has more reason to look seriously at higher umbrella limits. -

What kind of projects create the worst-case scenario?

Roofing over occupied buildings, excavation near utilities, electrical work in public facilities, and heavy sitework around traffic all create different severity profiles. -

How dependent is the business on subcontractors?

The more outside parties touching the work, the more important it is to think through transferred risk, upstream liability, and claim complexity. -

What business assets need protection?

A contractor that has built up equipment, working capital, and a valuable reputation has more to lose from one uncovered excess judgment.

The right umbrella limit should match the worst contract requirement and the worst realistic claim scenario, not the owner's comfort level on a quiet day.

A trade example using a growing electrical contractor

Take an electrical contractor moving from small retail jobs into school and light industrial projects. The company now has multiple service vans, larger crews on active sites, and contracts that require higher limits than it carried in earlier years.

If that contractor only looks at office revenue, the umbrella decision may seem easy to postpone. If the contractor looks at fleet exposure, occupied-building work, subcontractor coordination, and the certificate requirements attached to target projects, the answer usually changes.

That's why commercial umbrella insurance should be reviewed anytime a contractor sees one of these shifts:

- Bigger contracts: The company wants work that has stricter insurance language.

- More vehicles: Crews and supervisors are driving more often and farther.

- Higher-hazard jobs: The work moves into schools, hospitals, multifamily, infrastructure, or busy public settings.

- More subs or labor complexity: More parties on the job means more ways a claim can spread.

- More to protect: The company has built real value and can't afford a catastrophic hit.

A contractor can buy too little by guessing. It can also buy too much by chasing a number with no connection to real project demands. The better move is to set the umbrella limit where growth plans and realistic loss exposure meet.

Get the Right Umbrella Policy for Your Trade

A contractor usually figures out whether the umbrella program fits only after a bid gets hung up, a certificate request comes in higher than expected, or a serious loss exposes a gap between the policy and the work. By then, options are tighter.

The better approach is to set up umbrella coverage the same way a superintendent checks a site before concrete is poured. Verify what sits underneath, confirm the dimensions, and catch the problem before it gets buried. For insurance, that means matching the umbrella to the actual liability program, the contracts being signed, and the kind of losses the trade can produce on a bad day.

That review should go past the headline limit. General liability, commercial auto, and employer's liability all need to support the umbrella correctly. The policy form matters too. A cheap quote can fall apart if the underlying limits are wrong, the carrier restricts key exposures, or the contract requires terms the umbrella does not satisfy.

Trade differences matter. A hardscape contractor hauling crews and equipment every day has a different auto and premises exposure than a general contractor running large subcontractor schedules. A roofer working above occupied tenants faces a different severity profile than a finish carpenter wrapping up interior trim in controlled spaces. The umbrella should reflect how claims happen in that trade, not just revenue or payroll.

Contractors are buying more umbrella coverage for practical reasons. Owners and upstream contractors are asking for higher limits. Lawsuits are getting larger. One vehicle loss, one injury with permanent impairment, or one multi-party jobsite claim can push past standard limits faster than many firms expect.

Coverage Axis is one option contractors can use to review underlying liability lines, shop umbrella or excess markets, and compare how different carriers structure contractor programs.

The right limit is the one that keeps the company eligible for the jobs it wants and protected against a loss that could stall growth, drain cash, or change the business in one claim.

If the current insurance program is holding back bids or leaving questions about catastrophic claim protection, a free Coverage Axis quote or coverage review can help identify the right umbrella limit, check for gaps in the underlying policies, and match the program to the trade, fleet, and project types the business is taking on.