A drywall subcontractor opens a bid package on a Sunday night, ready to price a school renovation. The scope looks fine. Then the insurance page shows up. The general contractor wants a certificate of insurance, additional insured status, waiver language, completed operations, and limits that have to match the contract exactly. The sub already has general liability. But that doesn't mean the paperwork will pass, and it doesn't mean the policy fits the job.

That's where most contractors get burned. They treat general liability insurance for contractors like a license requirement or a line item to keep the office moving. It's not. It's the policy that keeps a trade business eligible for serious work and standing after a lawsuit. A cheap policy that fails contract review is wasted money. A policy that only sort of matches the operation is worse.

An electrician, roofer, plumber, or painter doesn't need more insurance jargon. The business needs a straight answer on what the policy does, what it doesn't do, and which contract details matter before mobilization starts.

Table of Contents

- Why Your General Liability Policy Is Your Most Important Tool

- What General Liability Actually Covers on the Jobsite

- The Paperwork That Wins Jobs Certificates and Additional Insureds

- Decoding Your Policy Limits and Completed Operations

- What Drives the Price of Your Contractor GL Policy

- The Contractor's Checklist for Getting the Right GL Quote

Why Your General Liability Policy Is Your Most Important Tool

A painting contractor lands a chance to work on a regional office buildout. The pricing is competitive. The schedule works. Then the owner's insurance requirements stop the job before it starts. The contractor has a policy, but the carrier can't produce the right paperwork fast enough, and the wording doesn't line up with the contract.

That's not an insurance problem. That's an operations problem.

General liability insurance for contractors is the tool that lets a business bid, start, invoice, and stay alive when something goes wrong. Without it, a contractor can't get through most serious prequalification reviews. With the wrong version of it, a contractor can still lose the job after winning the bid.

For a concrete subcontractor, that can mean missing a larger commercial opportunity because the certificate doesn't reflect the required endorsements. For an electrician, it can mean getting pulled into a property damage claim after work hours because a third party alleges the installation caused the loss. Either way, the policy isn't just back-office paperwork. It protects the business from lawsuits that can otherwise hit retained earnings, future contracts, and sometimes the owner's personal financial stability.

Practical rule: If a policy can't satisfy the contract and respond to real third-party claims tied to the trade's work, it's not good coverage, no matter how cheap it looked on the quote.

The smart approach is simple. Contractors should judge a GL policy the same way they judge a lift, panel schedule, or roofing membrane. Does it fit the work? Does it meet spec? Will it hold when pressure hits?

That's the standard.

What General Liability Actually Covers on the Jobsite

A plumbing contractor opens a wall in a tenant improvement project. A worker hits the wrong line. Water runs into an adjacent suite, damages flooring and cabinets, and the neighboring tenant demands repairs. That's the kind of event general liability is built to address.

For contractors, general liability is built around third-party risk transfer. It responds to claims for bodily injury, property damage, and personal or advertising injury caused by the contractor's operations, while excluding employee injuries and the contractor's own tools, vehicles, and project property, as explained in this contractor GL coverage overview.

The core jobsite claims

For an electrician, the easiest way to understand GL is to ask one question. Did the contractor's work allegedly injure someone else or damage someone else's property?

If the answer is yes, GL is the first place to look.

A few common examples make it clear:

- Bodily injury: An HVAC contractor leaves cords across a walkway in a mechanical room, and a visiting property manager trips and gets hurt.

- Property damage: A tile contractor drops material that cracks a finished glass panel owned by the client.

- Personal or advertising injury: A remodeling company uses marketing content that creates a dispute over advertising-related injury.

This is why GL is the backbone of a contractor insurance program. It handles the outside-party allegations that can turn an ordinary day into a lawsuit.

A contractor also has to think beyond insurance when managing the site itself. For larger projects, jobsite controls such as fencing, access logs, and expert security for construction sites can reduce the kinds of third-party incidents that trigger claims in the first place.

What the policy does not pick up

A lot of contractors overestimate GL because agents and online summaries often stop at “slip and fall” language. That's not enough.

For a roofing contractor, these gaps matter:

| Exposure | Where it usually belongs |

|---|---|

| Injury to a roofer on payroll | Workers' compensation |

| Damage to a company truck | Commercial auto |

| Loss of company tools or mobile equipment | Inland marine |

| Pollution-related job loss | contractors pollution liability coverage |

That split matters because one event can trigger several policies at once. A masonry contractor could have a visitor injury, a hurt employee, and damaged equipment tied to the same incident. GL doesn't replace those other policies. It works beside them.

General liability should be treated like the liability foundation of the insurance program, not the whole program.

A framing contractor that buys GL and ignores the rest is underinsured, not efficient. The right move is to build coverage around the trade's actual exposure, crew setup, vehicles, equipment, and contract obligations.

The Paperwork That Wins Jobs Certificates and Additional Insureds

A commercial roofer gets a notice to proceed, but the GC won't release the start date until insurance documents are approved. The roofer sends a certificate. The GC rejects it. Then comes the email chain: missing additional insured wording, wrong certificate holder, no evidence of waiver language, and a delay that puts the mobilization schedule at risk.

Jobs are won or stalled at this point.

What a COI really is

A certificate of insurance, or COI, is proof that a policy exists. It is not the policy itself, and it does not rewrite coverage. For a siding contractor, that means the certificate can show the carrier, policy dates, and listed coverages, but it can't magically add language the underlying policy doesn't contain.

That distinction matters because many contractors think the office can “just issue a COI” to solve any contract requirement. It can't. If the subcontract requires endorsements, the policy has to support them first.

A practical way to think about the COI is this:

- It proves coverage is in force: Useful when a GC screens subs before work begins.

- It reflects requested parties: Often includes the certificate holder and sometimes notes required status.

- It doesn't grant coverage by itself: If the endorsement isn't on the policy, the COI won't save the contractor in a dispute.

Contractors working through formal compliance systems often benefit from understanding broader prequalification workflows. A Cm3 contractor management guide gives helpful context on how documentation review fits into contractor approval.

Why additional insured status matters

For an electrical subcontractor, additional insured status usually means the client or GC wants access to protection under the sub's liability policy for claims arising out of the sub's work. That's the practical reason the request shows up on so many contracts.

If a tenant sues after an alleged loss tied to the electrician's installation, the GC doesn't want to rely only on its own policy. It wants the electrician's policy involved too, where the contract allows it. That's why contractors need to understand additional insured endorsement requirements before signing.

A contractor that ignores additional insured wording can win the bid and still fail compliance.

This is not optional on larger work. Institutional owners and many contractor agreements require Commercial General Liability with broad-form wording and minimum limits of $1,000,000 per occurrence / $3,000,000 aggregate, often including completed operations and contractual liability, as outlined in this summary of contractor CGL requirements.

Where waiver language fits

A waiver of subrogation is another contract term that frustrates trade contractors because it sounds more complicated than it is. In plain language, it usually means one insurer gives up certain recovery rights against the other party after paying a loss, when the contract requires that waiver.

For a flooring contractor working under a GC, that clause is part of the risk allocation on the project. If the contract demands it, the contractor should check whether the policy can support it before signing. Waiting until the owner's rep rejects the insurance package is too late.

The contractors who scale into better work don't just carry insurance. They manage insurance documents like job-critical submittals.

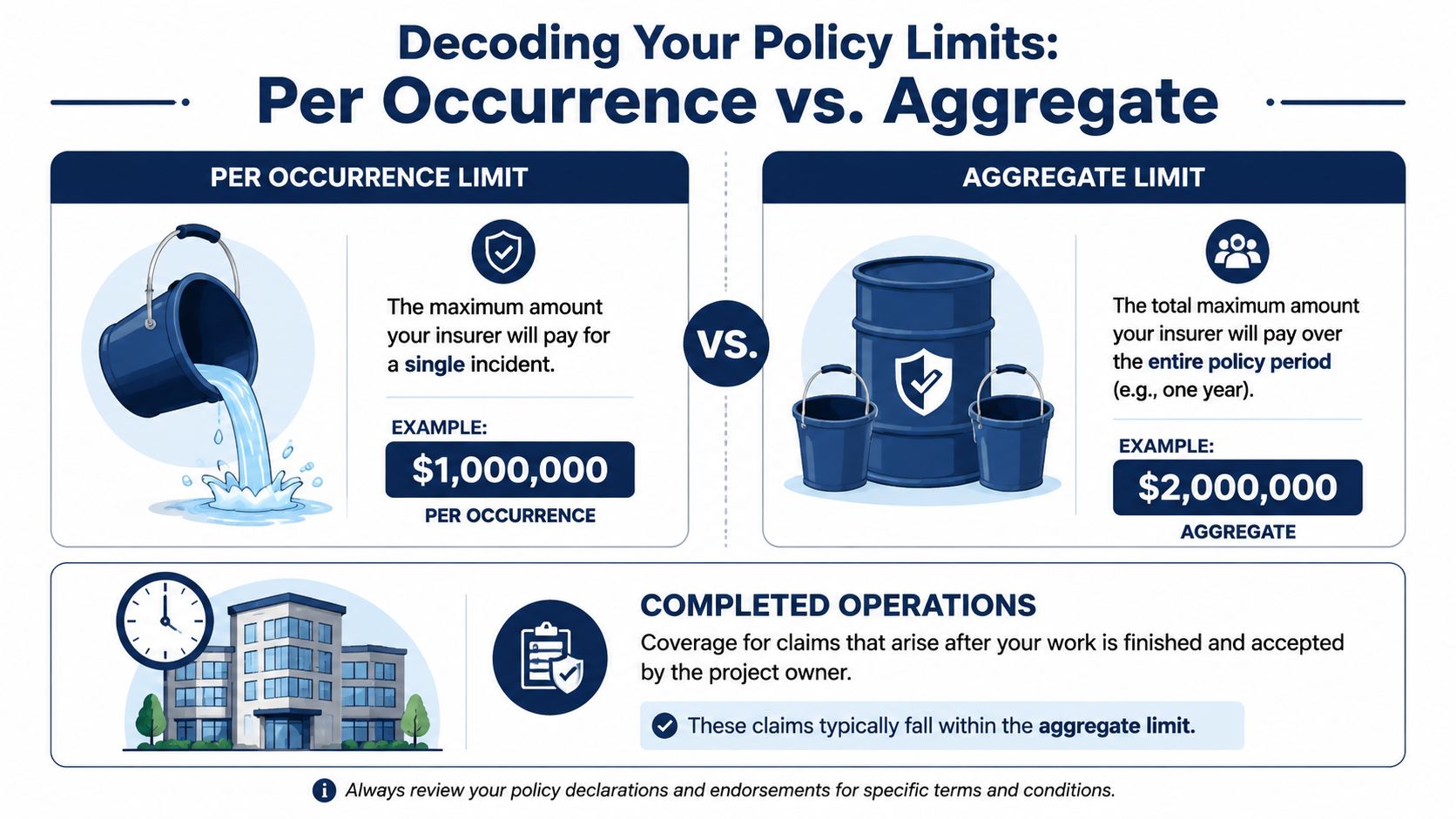

Decoding Your Policy Limits and Completed Operations

A roofer finishes a commercial tear-off and replacement in June. In October, water shows up inside the building after a storm. The owner blames the roof system, the GC demands the roofer's insurance, and the payment dispute starts fast. At that point, the contractor does not need a generic promise that “GL is in place.” The contractor needs the right limits, the right completed-operations coverage, and paperwork that holds up under the contract.

How to read per occurrence and aggregate

Contractors lose time on this because policies use insurance language and contracts use compliance language. You need to read both together.

The per occurrence limit is the most the policy pays for one covered loss. The aggregate limit is the most the policy pays for all covered losses during the policy period. For an electrician, one fire claim tied to a bad connection can burn through the per occurrence limit by itself. A string of smaller property damage claims across several jobs can eat into the aggregate and leave the contractor exposed before the year is over.

That matters on real jobs because owners and GCs do not review your policy like an insurance class exercise. They review it against the contract and against the size of the loss they think your trade can cause.

| Limit type | What it controls | Trade example |

|---|---|---|

| Per occurrence | Maximum available for one covered incident | One major fire or property damage claim tied to an electrician's installation |

| Aggregate | Total available during the policy period | Several separate claims during the year across multiple roofing projects |

Ask the right question. Do the limits fit the work, the contract, and the downside of a bad claim?

A contractor chasing schools, multifamily, or municipal work should expect closer scrutiny here. If you want a plain-English breakdown, review these general liability coverage limits for contractors before you sign the job, not after the owner rejects your insurance package.

Why completed operations deserves real attention

Completed operations is where many trade contractors get hit hardest because the job looks finished until somebody claims it was not done right. For a plumber, that can mean a slow leak behind a wall months after turnover. For a roofer, it can mean water intrusion after the first serious weather event. For an electrician, it can mean a later allegation that installed work caused property damage after occupancy.

This exposure decides more than lawsuits. It affects whether your insurance package satisfies the contract, whether the GC can keep you on the job, and whether a payment dispute turns into a backcharge fight.

Owners focus on completed operations for a reason. A trip-and-fall during active work is obvious. Finished-work claims are more expensive, more disputed, and more likely to pull contracts, endorsements, and certificates into the argument. That is the operational reality contractors need to understand.

Read the policy and the contract together. If the contract requires completed operations for a set period after the work is done, confirm your GL structure supports that requirement. If it does not, fix it before the job starts.

The practical rule is simple. A contractor should treat completed operations as part of job qualification, not as fine print buried in the policy.

What Drives the Price of Your Contractor GL Policy

A painter and a roofer can have the same revenue, the same number of workers, and the same city on the mailing address. They still won't get priced the same. The trade itself changes how underwriters look at the account.

That's where contractors should start when reviewing a quote.

Trade class drives the quote first

A roofer works at height, deals with water intrusion exposure, and can create severe downstream losses if installation fails. A painter usually presents a different risk profile. That doesn't mean one trade is “good” and the other is “bad.” It means insurers classify exposure based on how losses tend to develop.

For an excavation contractor, one mistake can affect underground utilities, neighboring structures, or public areas. For a handyman doing light punch-list work, the exposure tends to look different. So the premium changes.

When a contractor thinks the quote is too high, the first thing to check is whether the business was classified correctly. Misclassified operations create bad pricing and bad coverage.

The rest of the pricing picture

After trade class, underwriters usually focus on the operational facts that show how much exposure the insurer is taking on. For a landscaping contractor or plumber, these are the big levers:

- Revenue and payroll: Higher activity usually means more jobs, more site presence, and more chances for a claim.

- Project type: Residential service work doesn't look the same as public or large commercial construction.

- Loss history: Prior claims affect how the account is viewed.

- Geography: Venue, project environment, and local claim conditions matter.

- Requested limits and endorsements: More contractual requirements usually mean a more complex policy build.

A short comparison makes the point:

| Contractor profile | Likely pricing pressure |

|---|---|

| Roofer doing larger commercial re-roofs | Higher due to height and completed-work exposure |

| Interior painter on occupied tenant improvements | Moderate, depending on job conditions and client requirements |

| Demolition contractor | Higher because the work itself creates more severe loss potential |

A contractor can't control every factor, but the business can improve how it presents risk. Clear scope descriptions, accurate payroll splits, tight subcontractor controls, and organized claim records make underwriting easier and cleaner.

For contractors that are also managing workers' comp costs, understanding experience rating helps explain why labor and claims data matter across the whole insurance program. This guide to workers comp experience modification is useful context when preparing for a broader insurance review.

The fastest way to overpay is to give incomplete or sloppy operational details. The fastest way to buy the wrong policy is to shop on premium alone.

The right quote isn't just the cheapest one. It's the quote built on an accurate picture of the trade.

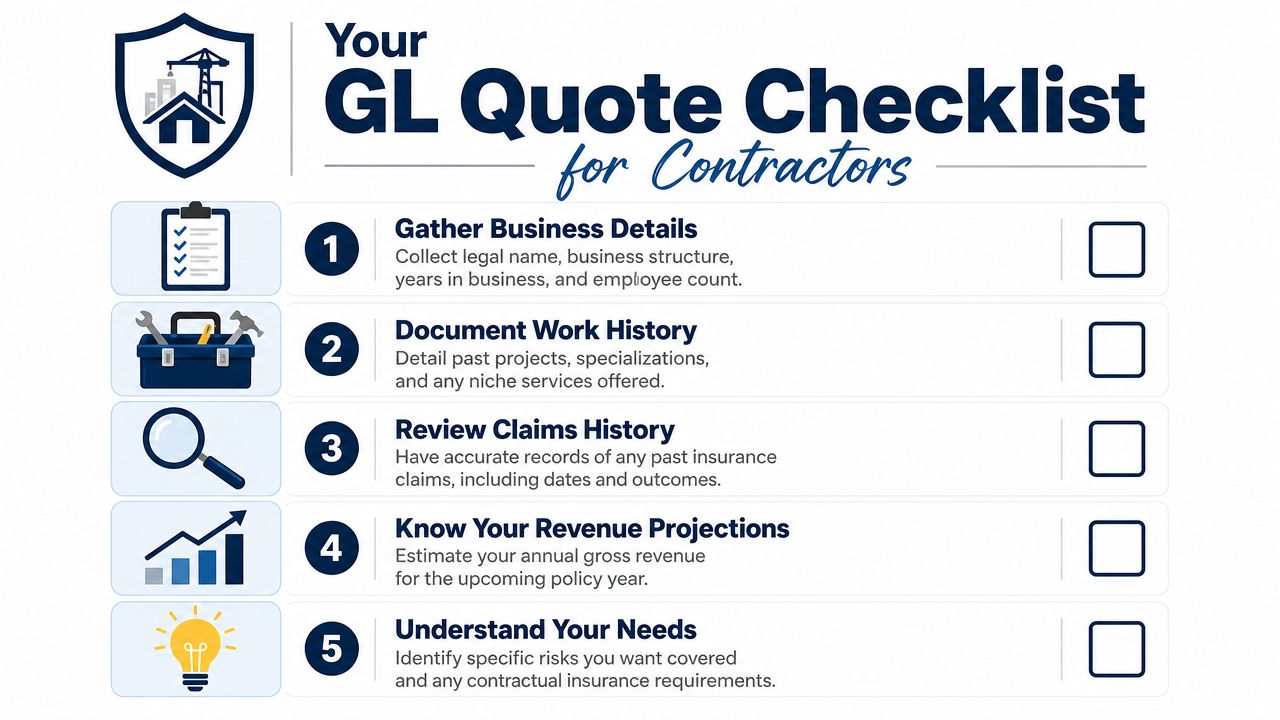

The Contractor's Checklist for Getting the Right GL Quote

A general contractor is ready to issue a subcontract to a finish carpenter on a repeat tenant improvement job. The superintendent asks for the updated COI and Additional Insured wording. The carpenter tells his agent, “Just renew what I had last year.” That is how contractors end up with a cheap quote, the wrong endorsements, and a payment hold before the first delivery hits the site.

General liability quoting is not a shopping exercise. It is a compliance and risk review. If your quote does not match your actual scope, your contract requirements, and the way you deliver certificates on live projects, it is not the right quote.

What to gather before calling

For a plumbing contractor, the right move is to build the file the same way you build a bid package. Clean information gets cleaner terms.

Business details

Give the legal entity, years in business, state(s) of operation, crew count, and who performs the work. If office records, licenses, and prior policies do not match, the quote starts off wrong.Full scope of work

A drywall contractor should spell out metal framing, insulation, acoustical ceilings, patch and repair, tenant improvements, and any specialty work. Vague descriptions create bad classifications, bad pricing, and bad assumptions about what the policy is meant to cover.Revenue projections

Use a realistic estimate based on signed work, current backlog, and expected bidding volume. Underwriters price contractor GL around the work you are going to perform, not a round number picked in a hurry.Claims history

Bring a clear loss summary and be ready to explain what happened and what changed afterward. A roofer with one prior water intrusion claim looks a lot better when the account file shows stronger tarp procedures, documentation, and jobsite controls.Current and target contract requirements

Bring the toughest insurance spec you expect to sign this year. An electrician bidding commercial work should have sample subcontract language in hand, especially if owners or general contractors require Additional Insured status, primary and noncontributory wording, waiver of subrogation, or specific completed-operations language.

If clients regularly ask for proof-of-coverage language in a specific format, review this certificate of insurance template for contractors before you request policy documents. It will help you spot documentation gaps before they slow down mobilization.

What to ask before buying

A lot of contractors ask one question: “What's the premium?” That is the wrong question.

An electrician, HVAC contractor, or concrete sub should ask these instead:

Does the policy match the work we do?

The business name alone is useless. The operations description needs to reflect the trade, the project type, and any higher-risk work you have added since last term.Can the policy support our contract requirements?

If your jobs require Additional Insured endorsements, completed-operations coverage for upstream parties, or fast COI turnaround, confirm that before binding. Do not assume the paperwork will work itself out later.How is completed operations handled?

This matters most for trades where the claim shows up after turnover. A plumber, roofer, or stucco contractor can finish a job cleanly and still face an allegation months later. Your quote needs limits and wording that fit that exposure.Are the limits high enough for the jobs we want, not just the jobs we had last year?

A small-service electrician chasing larger commercial build-outs often outgrows last year's limit structure before he notices it.Who is handling certificates, and how fast can they issue them correctly?

On active projects, slow or inaccurate COIs hold up access, billing, and draws. Speed matters, but accuracy matters more.

Many contractors find out their GL policy was built wrong only after a finished-work claim or a rejected certificate request.

A masonry contractor should ask one blunt question before binding coverage: if an owner alleges property damage after handoff, will this policy respond in a way that matches the subcontract and the project requirements? If the answer is unclear, do not buy the quote.

Disciplined contractors get better results because they treat GL insurance like jobsite planning. They know their scope, they know their paperwork requirements, and they make the policy fit both.

Coverage Axis helps contractors build insurance programs that fit the work they perform, not generic packages built for somebody else's trade. For a free quote or coverage review, visit Coverage Axis and have a licensed advisor review current policies, contract requirements, COIs, additional insured needs, and completed-operations exposure before the next job goes live.