A contractor can run tight jobs, keep crews moving, and still get blindsided at renewal when the workers comp premium jumps. Then the estimator starts working the next round of bids and realizes the problem isn't just insurance cost. It's margin, prequalification, and whether the company still looks attractive to a general contractor reviewing subs.

That's where workers comp experience modification becomes more than an insurance term. For trade businesses, it functions like a score attached to payroll, claims handling, and the day-to-day discipline of running crews safely and documenting work correctly. A roofing company with repeated small strain claims, a plumbing contractor with frequent back injuries, or an electrical shop with a run of minor hand injuries can all feel the impact long after the jobs are closed.

Table of Contents

- What Is a Workers Comp Experience Modification?

- How Your Experience Mod Is Calculated

- The Financial Impact on Premiums and Profit

- Why Your Mod Matters for Bids and Audits

- Strategies to Improve and Control Your Mod

- Common Pitfalls and State-Specific Rules

- Take Control of Your Workers Comp Costs

What Is a Workers Comp Experience Modification?

A roofing contractor loses a school re-roof bid by a fraction of a point. The crew is solid, the estimate was tight, and the schedule worked. The problem was not workmanship. It was the workers comp experience modification sitting on the bid form, signaling higher insurance cost and higher perceived risk before anyone walked the roof.

A workers comp experience modification, often called an E-Mod or X-Mod, is the rating factor applied to a business's workers compensation policy based on its loss experience. It works like a performance score inside the insurance system. A mod of 1.00 represents expected loss experience for an employer of similar type and size. Above 1.00 means a higher-than-expected result and usually higher premium. Below 1.00 means better-than-expected experience and usually lower premium.

For contractors, that number reaches further than insurance accounting. It affects labor cost, bid math, and how a GC or project owner reads your operation. A low mod can give an electrical contractor more room to price a tenant improvement job aggressively. A high mod can force a plumbing company to protect margin on every hour of field payroll, even if the foremen and techs are doing good work today.

Why contractors should care

The mod affects three business decisions every contractor feels in real time:

- Insurance cost: It changes what the company pays for workers comp.

- Bid competitiveness: It can tighten or expand the room you have to price work and still protect margin.

- Market perception: Owners, GCs, and risk managers often use it as a quick indicator of jobsite control.

The trade-off is straightforward. A contractor can be excellent in the field and still carry a costly mod because of prior claims, poor claim follow-up, or payroll reporting problems. I have seen companies improve operations on the jobsite but still lose pricing flexibility because the mod kept insurance expense too high for another cycle.

Owners should understand how their workers compensation coverage performs in practice, not just whether the policy is active.

A mod is not just a safety label. It is a cost driver tied directly to whether a contractor can win work at the right price and keep profit after the crew is paid.

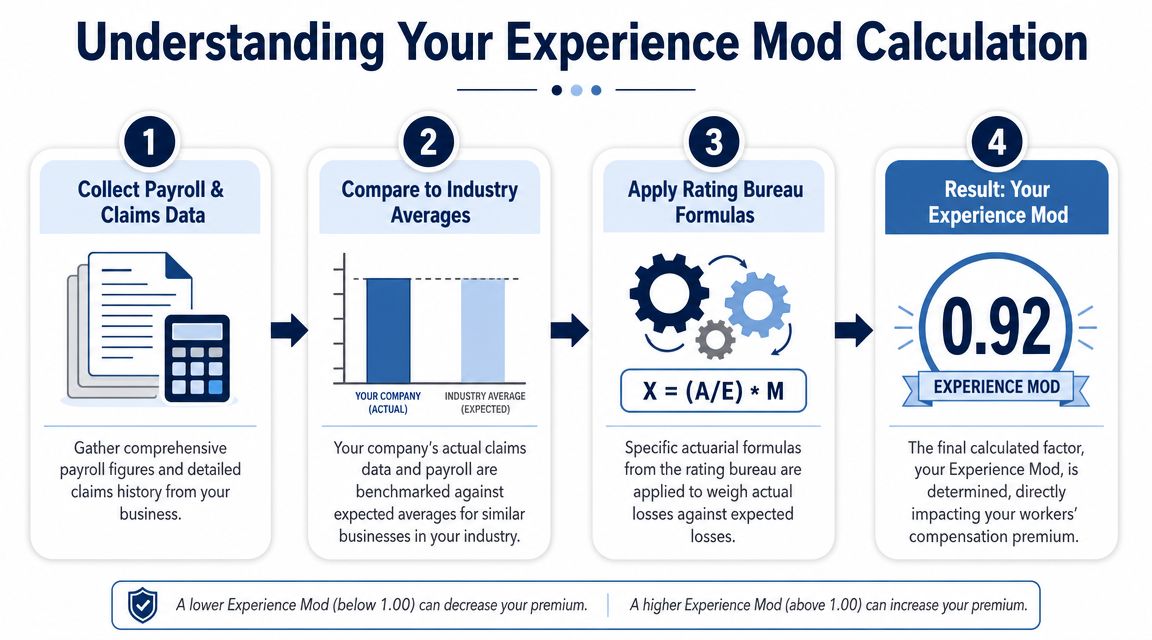

How Your Experience Mod Is Calculated

Most contractors hear that the mod is based on claims history, then stop there. The exact calculation is more specific. The system compares a contractor's actual losses against expected losses for businesses of similar size in the same class codes. Payroll matters. Classification matters. Loss history matters. The formula is built to compare like with like, not just to total up claims.

A contractor that misclassifies payroll, mixes shop labor with field labor incorrectly, or lets claims develop without follow-up can hurt the result from more than one direction.

The time window catches many owners off guard

The mod usually isn't built on only the most recent year. NCCI explains in its experience rating guide that the experience period is generally based on three years of payroll and loss data, though it can range from less than 12 months up to 45 months depending on timing and eligibility rules. That means current premium can still be affected by older jobsite losses.

For contractors, this explains a common frustration. A roofing company may tighten safety, replace a weak foreman, improve ladder practices, and report fewer incidents this year, yet still carry the drag from prior policy years. The system is designed to smooth volatility, not erase a bad stretch overnight.

Why small claims can hurt more than expected

The formula also splits losses into primary and excess components. In plain language, it gives more weight to claim frequency than many owners realize. NCCI-style rating uses that structure so frequent smaller losses hit harder than a single isolated large one, a point summarized in this plain-English explanation of workers comp experience modification.

An electrical contractor is a good example. If a company has a recurring pattern of cut fingers, minor burns, and hand-tool injuries, that frequency can move the mod in the wrong direction even when no single claim looks catastrophic. The issue isn't just dollars paid. It's the repeated signal that the company generates losses more often than expected for its trade and payroll.

Repeated “small” claims are rarely small in the rating formula. They often show a pattern, and patterns are what the mod reacts to.

What goes into the comparison

A contractor trying to understand the worksheet should focus on a few operating inputs:

- Payroll by class code: Field electrician payroll shouldn't be treated the same as clerical payroll.

- Claims attached to the experience period: Older claims may still be active in the rating window.

- Expected losses for that trade: The system compares the business to similarly classified employers, not to every employer in the market.

- Accuracy of reporting: Payroll mistakes and class code errors can distort the comparison from the start.

Contractors that want a better handle on these pressure points should pay close attention to the operational drivers behind construction insurance risk factors. The mod doesn't come from one dramatic event alone. More often, it reflects repeated breakdowns in supervision, reporting, and administrative accuracy.

The Financial Impact on Premiums and Profit

A plumbing contractor can run a solid crew, keep projects on schedule, and still give away margin because the workers comp mod is too high. The problem shows up long before the renewal meeting. It shows up in labor burden, bid math, and how much room is left when a job gets tight.

The X-mod changes premium directly. If the mod is above 1.00, the employer pays more than average for the same payroll and class mix. If it is below 1.00, the premium comes down. That sounds simple on paper. In practice, it affects every estimate built on field labor.

A simple premium example

The table below shows how the mod changes a sample base premium.

| Experience Mod (X-Mod) | Calculation | Final Premium | Difference from Average |

|---|---|---|---|

| 0.80 | $50,000 × 0.80 | $40,000 | -$10,000 |

| 1.00 | $50,000 × 1.00 | $50,000 | $0 |

| 1.25 | $50,000 × 1.25 | $62,500 | +$12,500 |

Same payroll. Same operation. Different result.

For a roofing contractor, that extra premium is rarely absorbed unnoticed. It either gets pushed into the bid, which can make the number less competitive, or it comes out of profit. On a job with tight labor margins, even a modest increase in workers comp cost can wipe out the cushion that was supposed to cover rework, weather delays, or a foreman change.

Where margin disappears

Electrical and mechanical contractors feel this quickly because labor drives so much of the job cost. If an estimator carries the wrong workers comp burden into a school remodel or tenant improvement, the company can win the work and still underperform financially. Owners often focus on material escalation and production hours first. The mod belongs in that same conversation because it changes the cost of every payroll dollar.

That is why I tell contractors to treat the mod like an estimating input, not just an insurance result. A debit mod puts pressure on every labor-heavy project. A credit mod creates room. It can help a contractor hold margin without becoming the high number.

For contractors trying to tighten cost structure in a payroll-sensitive state, this guide on how to lower California workers' compensation is a useful reference point for reviewing broader rate pressure and cost controls. The larger point is straightforward. The mod affects profit in the field, not just premium on a policy summary.

A debit mod weakens pricing flexibility. A favorable mod gives a contractor more room to bid aggressively and still protect margin.

That matters even more for firms taking on larger projects or managing multiple crews at once. Workers comp costs sit inside a broader risk structure that affects overhead, contract requirements, and job profitability. Contractors expanding into bigger work should review how workers comp fits within general contractor workers' compensation coverage, because a bad mod rarely stays isolated to one line item.

Why Your Mod Matters for Bids and Audits

Many contractors first notice the mod when the renewal comes in. The market often notices it earlier. Prequalification packages, bid documents, and contractor review forms frequently ask for workers comp details because hiring parties want proof that a subcontractor can manage labor risk on an active site.

For labor-intensive trades like roofing, framing, and concrete, a seemingly modest 1.10 to 1.25 mod can severely erode bid competitiveness when applied to a large payroll base, as discussed in this article on experience mods and contractor costs. That's why mod management belongs in estimating meetings, not just renewal calls.

Bid qualification is where the pain becomes visible

Take an HVAC subcontractor pursuing school work. The company may have the manpower, equipment, and install experience to handle the package. But if the GC's safety review team sees a debit mod and interprets it as evidence of avoidable jobsite issues, the subcontractor can lose the opportunity before price is fully considered.

That's the part many owners underestimate. The mod doesn't only affect what the company pays. It affects whether the company gets invited to play at all.

A lower mod also helps when a contractor needs to reassure a project owner about supervision quality, injury response, and crew discipline across multiple jobs running at once.

Audits become harder when the file already looks messy

Carriers and underwriters look at the whole account, not just one number. A poor mod history can lead to closer review of payroll allocations, claim handling, loss trends, and subcontractor relationships. Even when a formal audit is routine, a contractor with a troubled loss pattern often spends more time defending records and answering follow-up questions.

That creates drag inside the office:

- More documentation work: Payroll records, job descriptions, and classifications need to be cleaner.

- More scrutiny on subcontractor use: Hiring parties often want tighter proof of downstream compliance.

- More pressure on management time: Owners and office staff end up chasing records instead of running jobs.

A high mod can turn routine paperwork into a recurring credibility problem.

This gets more complicated when subcontracted labor is involved. Contractors should understand how workers comp and subcontractor liability issues can affect both audits and upstream project requirements. On many jobs, a weak mod doesn't stay hidden in the insurance file. It becomes part of the contractor's reputation.

Strategies to Improve and Control Your Mod

Contractors can't change the past, but they can control what future rating periods look like. The strongest results usually come from three operating habits working together: preventing avoidable injuries, managing claims aggressively once they happen, and keeping payroll and classification records accurate.

The reason this matters is simple. The formula gives more statistical weight to claim frequency than claim severity. One state fund explanation says ten claims of $3,000 each will generally drive a higher experience modification factor than one $30,000 claim, which is why reducing claim count matters so much for contractors managing long-term workers comp costs, as explained in this overview of experience modification factors.

Build fewer claims in the first place

A company doesn't need a glossy safety binder to improve results. It needs field habits that crews put into practice.

- Tight toolbox talks: Short meetings tied to real exposures work better than generic lectures. A roofing crew needs fall protection reminders tied to current site conditions. An electrical crew needs lockout awareness and hand protection tied to the week's tasks.

- Supervisor accountability: The foreman should catch repeat hazards before they become repeat claims. Loose extension cords, poor ladder setup, rushed material handling, and skipped PPE checks often show up in small but frequent losses.

- Near-miss reporting: Contractors that treat close calls seriously usually spot patterns earlier.

Control what happens after the injury

A lot of damage happens after the incident, not at the moment of injury. Delayed reporting, weak communication, and no modified-duty plan allow claims to grow in both cost and duration.

A plumbing contractor offers a useful example. A tech strains a shoulder lifting a water heater. If the company reports the claim immediately, documents job duties, and offers temporary light work such as inventory, warehouse support, safety checklists, or dispatch assistance, the file often stays more controlled than if the employee remains off work with no plan.

Field advice: The faster the contractor reports the injury and coordinates restricted duty, the better the chance of limiting claim development and protecting the future mod.

Contractors should also understand how injury handling affects the broader employee injury claims process. Fast response isn't only about compliance. It affects reserves, return-to-work timing, and whether a minor injury becomes a long-running file.

Clean up the paperwork that quietly drives cost

Administrative errors can undermine a contractor even when the field operation improves.

A practical review should include:

Class code accuracy

Make sure payroll is assigned to the right operations. Electrical service work, office staff, shop support, and field installation don't always belong in the same bucket.Annual worksheet review

Owners should review the mod worksheet for claim entries, payroll figures, and business details that don't look right. Errors left unchallenged can continue hurting future pricing.Claim trend review

Look for repeats by body part, tool type, vehicle type, or crew. Three hand lacerations may point to glove use, saw handling, or rushed cleanup practices rather than bad luck.

Contractors that improve their mod usually do ordinary things consistently. They report fast, keep injured workers connected to the business, and refuse to let recurring “small” incidents pile up.

Common Pitfalls and State-Specific Rules

Many contractors hurt their own mod because they misjudge what matters. The most common mistake is dismissing smaller claims as harmless. In a rating system that reacts strongly to frequency, repeated minor losses can create the exact pattern that drives future cost and weakens bid positioning.

Another mistake is failing to review the worksheet closely. Payroll can be assigned incorrectly. Class codes can be off. Claims can be misunderstood by the owner because nobody compares the rating document to internal records. A contractor doesn't need to become an actuary, but someone inside the business should read the worksheet line by line.

Geography changes the rules

Workers comp rating isn't perfectly uniform across the country. Many states follow NCCI-style rules, while others use independent state systems. Some states operate through state fund structures with their own processes and requirements.

That matters for contractors with crews crossing state lines, multiple entities, or expanding operations. A company that assumes one set of workers comp rules applies everywhere can end up with reporting mistakes, classification issues, or renewal surprises that were avoidable with better guidance.

Mistakes that usually backfire

- Ignoring recurring small claims: Those often matter more than owners think.

- Treating the mod as an insurance-only issue: Estimating, safety, payroll, and HR all affect it.

- Trying to outsmart the process: Informal side payments or sloppy claim handling usually create bigger problems later.

- Using generic insurance advice: Contractors need state-specific and trade-specific guidance.

The safest approach is simple. Match payroll correctly, report claims promptly, and assume every recurring incident will matter more than it seems.

Take Control of Your Workers Comp Costs

A workers comp experience modification isn't a passive label a contractor has to live with forever. It reflects operating decisions. Safety discipline, claim handling, return-to-work planning, payroll accuracy, and worksheet review all shape where the business goes next.

For trade contractors, that matters well beyond the renewal premium. A better mod helps protect margin, supports cleaner prequalification, and gives estimators more room to compete. A worse mod does the opposite.

Contractors dealing with special compliance questions should also pay attention to state-specific rules. For example, businesses sorting out owner status and exemption questions in Florida may find this guide on navigating FL workers comp exemptions useful as part of a broader compliance review.

Contractors that want a second set of eyes on their current program can get a free, no-obligation quote and workers comp review from Coverage Axis. A licensed advisor can review the current experience mod, payroll classifications, claims pressure points, and overall coverage structure to help identify where costs may be trimmed without weakening protection.