A bid gets accepted. The schedule is tight. The subcontractor looks solid on price, crew size, and references. Then the insurance exhibit shows up and stalls everything.

That's where many contractors lose time and take on risk they didn't mean to assume. The insurance page isn't just paperwork from legal or a box for the office to check. It decides who pays when a ladder falls into a parked truck, when a plumber floods finished space, or when an uninsured worker gets hurt and everyone starts pointing fingers.

For contractors and trade business owners, subcontractor insurance requirements matter long before a claim happens. They affect bid eligibility, contract approval, jobsite access, payment timing, and whether a project problem stays with the subcontractor that caused it or lands back on the general contractor.

Table of Contents

- Why Subcontractor Insurance Is Your First Line of Defense

- The Four Core Policies Every Subcontractor Needs

- Decoding Limits and Critical Endorsements

- Contractual Requirements vs Statutory Minimums

- How Job Risk Changes Insurance Requirements by Trade

- Mastering the Certificate of Insurance COI

- Your Subcontractor Compliance Checklist and Next Steps

Why Subcontractor Insurance Is Your First Line of Defense

A subcontractor can be excellent at the trade and still be a bad risk transfer partner. That's the mistake busy contractors make when they focus only on price, manpower, and production speed.

A general contractor might hire a painting sub because the finish work is clean and the bid is competitive. Then a crew member oversprays a client vehicle, a passerby trips over materials, or a helper gets dropped off in a truck that isn't properly insured for business use. If the subcontractor's coverage is thin, expired, or missing key endorsements, the claim doesn't stay neat and contained. It spreads into the project.

That's why subcontractor insurance requirements should be treated the same way a contractor treats safety procedures or scope review. They aren't an afterthought. They're part of the front-end job filter.

Insurance screening is part of subcontractor vetting

The best subcontractors usually expect insurance scrutiny. They can produce current certificates, understand the contract language, and get corrections made quickly when an owner or GC asks for changes.

The weaker ones often create the same pattern:

- Late paperwork: Coverage documents arrive after the start date is already scheduled.

- Wrong named insured: The COI shows a trade name, not the legal entity signing the contract.

- Missing endorsements: The certificate says one thing, but the policy setup doesn't support it.

- Coverage gaps: Auto, workers comp, or completed operations details don't line up with the scope.

Practical rule: Vetting a subcontractor's insurance is really vetting whether that company runs a professional operation.

For contractors reviewing indemnity language, contractual liability coverage in plain English helps connect the subcontract language to the insurance program behind it.

The real issue is who gets stuck with the bill

A loss on a jobsite doesn't just damage property. It burns time, relationships, margin, and reputation. Owners remember who brought a problem onto the site. Carriers remember who had to absorb it.

That's why the insurance exhibit exists. It's there to decide, before work begins, whether the subcontractor has the financial backing to stand behind the work and the risk that comes with it.

The Four Core Policies Every Subcontractor Needs

A subcontractor's insurance program should stand like a four-legged stool. If one leg is weak, the whole thing wobbles. For a roofing subcontractor, that shows up fast because roofing work combines height exposure, material handling, vehicles, and schedule pressure on nearly every project.

In major construction markets, subcontractor insurance requirements often start with $1,000,000 per occurrence for Commercial General Liability and $1,000,000 for commercial auto liability, which has become a common baseline contractors are expected to meet according to Arkansas construction insurance requirements.

Contractors that want a broader overview of policy structure can review what insurance contractors typically need before matching those requirements to each trade.

For owners trying to secure your contracting business, the right starting point is a policy set built around actual jobsite exposures, not just the cheapest certificate that satisfies a bid portal.

General liability handles the damage you cause others

For a roofer, general liability is the policy that responds when the work harms someone else or damages someone else's property. Think about a bundle of shingles sliding off a roof edge and crushing the hood of a parked vehicle below. That's the kind of third-party property damage this policy is built for.

General liability is also where many contract disputes start, because the sub may have the policy but not the right form, not the right endorsement, or not enough limit for the project.

Workers comp protects the crew and the contract

Roofing is labor-heavy and injury-sensitive work. A worker can slip on a ladder, strain a back carrying material, or get hurt moving across a wet roof surface.

Workers comp exists to take care of job-related injury obligations tied to the employee. It also keeps that injury from becoming a direct financial problem for the hiring contractor. When a subcontractor doesn't carry workers comp correctly, the risk doesn't disappear. It shifts uphill.

Commercial auto follows the work off the jobsite

Many subcontractors think of vehicle claims as separate from project risk. In reality, auto exposure is part of the job. A roofing crew hauls ladders, compressors, dump trailers, and materials from yard to site and back again.

If a truck loaded with roofing material causes a road accident on the way to the project, commercial auto is what should answer the claim. Personal auto policies often aren't built for business-use construction exposure.

Surety backs up performance and payment obligations

Insurance covers accidents and liability. Surety is different. It supports the promise that the subcontractor will perform the work and meet certain financial obligations tied to the job.

Not every small subcontract needs a bond on every project. But when the owner, lender, or general contractor requires one, it becomes a test of financial strength and operating discipline. A roofer who can't qualify for required bonding may still be skilled in the field, but the project team may see that business as a reliability concern.

A subcontractor with all four core coverages in place usually moves through contract review faster, starts work faster, and creates fewer surprises when the risk team reviews paperwork.

Decoding Limits and Critical Endorsements

A policy limit sounds simple until a claim happens. Then the wording matters.

An electrician gives a good example. Faulty wiring can remain behind walls until a failure leads to fire, smoke damage, shutdown, and a completed-operations dispute long after the crew has left the site. In that kind of claim, the limit structure and endorsements decide whether the subcontractor's insurance really protects the hiring contractor or only looks adequate on paper.

How per occurrence and aggregate limits really work

Think of the policy as a set of buckets.

The per occurrence limit is the amount available for one claim event. The general aggregate is the total amount the policy can pay across covered claims during the policy term. A subcontractor can have a per occurrence limit that looks acceptable, but if earlier claims have already eaten into the aggregate, the remaining protection may be far less than the certificate suggests at first glance.

That's why project teams ask for both numbers and not just one.

Why endorsements matter more than many subs realize

The two endorsements that cause the most friction in subcontractor insurance requirements are Additional Insured and Waiver of Subrogation.

An Additional Insured endorsement is what extends certain liability protection to the general contractor or owner for claims arising out of the subcontractor's work. If an electrician's completed wiring work later causes a loss allegation, the GC doesn't want to rely only on the electrician's promise to indemnify. The GC wants status under the electrician's liability policy.

A Waiver of Subrogation helps stop the subcontractor's carrier from paying a claim and then turning around to pursue recovery against the GC or owner in situations governed by the contract.

For a clearer breakdown of that status, this guide to an additional insured endorsement is useful for both field leadership and office staff reviewing subcontracts.

If the endorsement isn't actually attached or available under the policy terms, the COI language alone won't rescue the claim.

Workers comp deserves close attention here too. Workers' Compensation is a statutory requirement in nearly every state, and Employers' Liability is commonly required at $1,000,000 per accident, as reflected in Indiana University insurance requirements. That matters because employee injury disputes are one of the fastest ways for uninsured subcontractor problems to climb back up to the general contractor.

Contractual Requirements vs Statutory Minimums

Many subcontractors confuse what the state requires with what the contract requires. Those are not the same thing.

A sole proprietor grounds care specialist is a good example. In some situations, that business owner may believe an exemption or minimum legal requirement is enough to get on site. From the GC's side, that assumption creates a gap. If the grounds care specialist is hurt operating equipment on the project and the insurance setup isn't what the contract required, the claim pressure may move straight into the hiring contractor's program.

The law sets the floor

Statutory minimums exist so businesses meet legal compliance. They are a floor, not a complete risk transfer strategy.

That floor may be too low for a commercial job, a public contract, a lender requirement, or a site with multiple trades working at once. State law might permit a thinner insurance setup than the owner, GC, or risk manager is willing to accept.

For contractors checking state-specific obligations, workers comp rules by state help identify where legal requirements stop and contract requirements need to take over.

The contract builds the firewall

Contract language should close the gaps the law leaves open. That's why project requirements usually scale upward with project value.

For example, projects exceeding $1 million in value often require $2 million per occurrence and $4 million general aggregate, while projects under $1 million may require $1 million per occurrence, according to Sonoma County insurance requirements. The point isn't to overcomplicate the subcontract. It's to match the protection to the financial exposure.

A grounds maintenance professional doing light site work on a small project doesn't create the same loss potential as a subcontractor working inside a large occupied structure. Contracts should reflect that difference.

A weak approach is copying state minimums into every subcontract template and assuming that solves risk transfer. A stronger approach is matching insurance requirements to project size, trade hazard, and who would absorb the damage if the subcontractor's policy fails.

How Job Risk Changes Insurance Requirements by Trade

The fastest way to create a coverage gap is to use the same insurance template for every trade. A painter, plumber, demolition crew, and crane operator don't bring the same hazard to a site, so they shouldn't be asked for the same limit structure.

A painter and a plumber don't bring the same exposure

A painting subcontractor usually presents lower catastrophic property damage exposure than a plumbing subcontractor. Paint mistakes can still be costly, especially in finished or occupied space, but plumbing failures can damage multiple units, mechanical systems, flooring, drywall, and contents all at once.

That's why trade-specific subcontractor insurance requirements matter. High-risk trades such as electrical and plumbing often must carry $2 million per occurrence in general liability, while lower-risk trades such as carpentry often stay at the $1 million standard. Extreme risks such as crane operations can require $5 million per occurrence, as outlined in this trade-specific subcontractor insurance guide.

The same logic applies to demolition and waste-related work. Debris, dust, disposal, and contamination concerns create exposures that ordinary general liability may not address fully.

High hazard trades need a different insurance template

For demolition or waste management work, Professional Pollution Liability may be required at $1 million per incident and $2 million aggregate, including cleanup-related exposures and non-owned disposal sites, based on subcontractor insurance requirements used by a major builder.

For crane work, lifting operations change the picture again. The load itself, the rigging, the drop zone, and nearby structures all raise severity potential.

Typical General Liability Limits by Subcontractor Trade

| Trade | Typical Per Occurrence Limit | Typical General Aggregate Limit | Primary Risk Factor |

|---|---|---|---|

| Painting | $1 million | $2 million | Overspray, slip hazards, property damage in finished space |

| Carpentry | $1 million | $2 million | Tool injuries, material handling, site property damage |

| Plumbing | $2 million | Higher limits often required by contract | Water damage, mold, concealed system failure |

| Electrical | $2 million | Higher limits often required by contract | Fire risk, power loss, completed operations exposure |

| Demolition or waste management | Varies by contract and pollution requirements | Varies by contract | Environmental damage, debris, cleanup costs |

| Crane operations | $5 million | Higher limits often required by contract | Lifting operations, rigging, load damage |

A contractor that estimates roofing and exterior work across multiple scopes may also benefit from operational systems that keep scope, documentation, and subcontractor review organized. For teams managing those moving pieces, Exayard roofing contractor software can be a practical workflow resource.

The safest insurance template is not the most detailed one. It's the one that matches the actual trade hazard on the site.

Mastering the Certificate of Insurance COI

The Certificate of Insurance, or COI, is the document organizations commonly use to clear a subcontractor for work. It helps, but it isn't the policy itself. It's closer to an insurance ID card than a guarantee of full compliance.

An HVAC subcontractor shows why this matters. The crew may be driving service vans, cutting roof penetrations, setting units with rented equipment, and working around occupied interiors. If the COI is wrong, the administrative mistake can hold up mobilization even when the field team is ready.

For teams that need a quick reference, this walkthrough on how to read a COI pairs well with an internal certificate of insurance template used to standardize reviews.

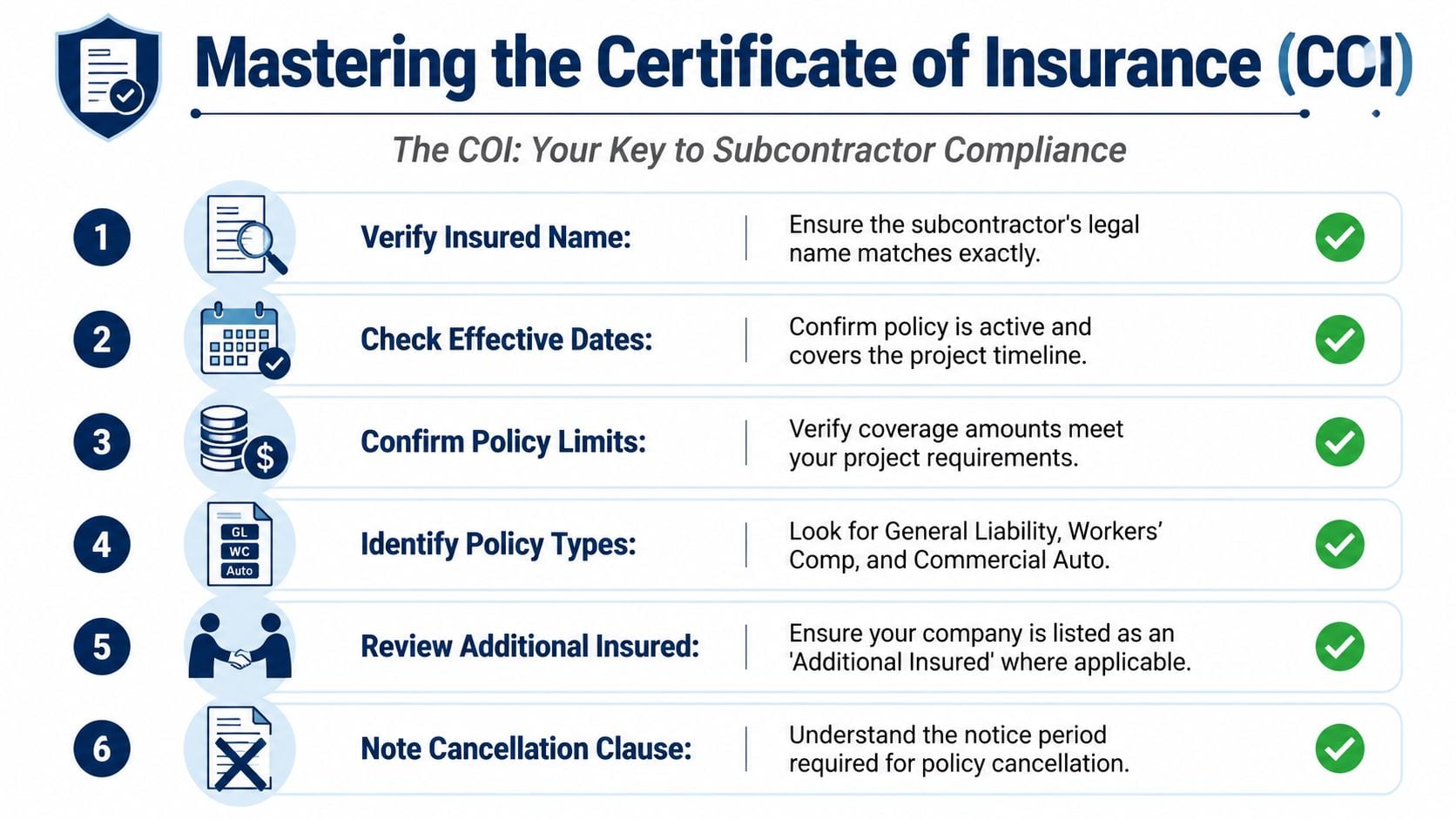

What to check on every COI

The strongest admin teams review COIs in the same order every time:

- Named insured: Match the legal business name to the subcontract exactly.

- Policy dates: Confirm the policies are active through the project timeline.

- Coverage types: Look for general liability, workers comp, and commercial auto at a minimum when the scope calls for them.

- Limits: Make sure the listed limits match the contract, not the subcontractor's assumption.

- Description of operations: Check whether project-specific wording, Additional Insured status, and Waiver of Subrogation language are referenced where required.

A clean COI review process saves field supervisors from the worst kind of delay. A subcontractor on site with people and equipment ready to go, but no approval to start.

Red flags that should stop mobilization

Some COIs look fine until someone reads line by line.

A certificate holder is not the same thing as an additional insured.

Common warning signs include:

- Blank or vague description language: It doesn't identify the project or required status.

- Dates that expire mid-project: Renewal tracking is likely to become a problem.

- Missing auto coverage for a trade that clearly uses vehicles: The paper doesn't fit the actual operation.

- Policy limits below contract requirements: The subcontractor may be trying to use a residential or small-job program on commercial work.

The best practice is simple. Treat the COI as the start of verification, not the end of it.

Your Subcontractor Compliance Checklist and Next Steps

Subcontractor compliance works best when it's built into prequalification, not handled as a scramble after award. Contractors that wait until a start date is looming usually end up accepting weak paperwork, chasing revised certificates, or delaying the project while everyone argues over the insurance exhibit.

A drywall subcontractor may look low-risk compared with a crane company, but even lower-hazard trades can create expensive disputes if the legal entity is wrong, the coverage lapses mid-job, or the endorsements don't match the contract.

A practical prequalification checklist

Use this checklist before work starts, not after a problem appears:

- Check the entity first: The insured name on the certificate should match the company signing the subcontract.

- Match coverage to scope: A sub driving to sites, hauling tools, or transporting materials should show the right auto setup for the operation.

- Compare limits to the contract: Don't accept a certificate just because it looks official.

- Confirm endorsements are addressed: Additional Insured and Waiver of Subrogation issues should be settled before mobilization.

- Track expiration dates: A compliant subcontractor can become non-compliant in the middle of the job if renewals aren't monitored.

- Review specialty exposures: Demolition, design responsibility, pollution risk, and lifting operations need more than a generic template.

- Document exceptions clearly: If an owner or GC accepts a deviation, put that approval in writing and keep it with the subcontract file.

Why compliance helps win better jobs

Insurance compliance does more than prevent claims from leaking uphill. It also helps identify which subcontractors run disciplined businesses.

A subcontractor that understands its own insurance program usually handles contracts better, responds faster to COI corrections, and creates fewer surprises when owner requirements tighten. That kind of subcontractor is easier to schedule, easier to retain, and less likely to create administrative drag when the project is already under pressure.

For trade business owners, the same principle works in reverse. The faster a company can produce compliant coverage, the easier it is to win bids, clear onboarding, and start billing.

Contractors who want a free, no-obligation review of their subcontractor insurance requirements or a fast quote for trade-specific coverage can talk with Coverage Axis. The team helps contractors and specialty trades line up the right policies, limits, COIs, and endorsements so jobs don't stall over paperwork and claims don't turn into business-threatening surprises.