A contractor lands a solid job across the state line. The estimate is accepted, the crew is ready, and the certificate request comes in from the general contractor or property owner. Then the problem starts. The COI gets kicked back because the workers comp setup that worked at home doesn't match the rules where the job will happen.

This is how this issue usually arises in practice. Not as a legal theory, but as a blocked mobilization, a delayed start, or a payroll problem that suddenly turns into a compliance problem. A roofing contractor may have one office employee and think the company is under the threshold in one state, then find out the neighboring state treats coverage much more broadly. An HVAC firm may send a service crew out for a short project and learn that work performed in that state can trigger a separate obligation even when the business is based somewhere else.

For contractors, workers comp requirements by state are tied directly to growth. They affect whether a bid is accepted, whether a project owner approves a subcontractor, and whether a single injury becomes an insured claim or a company-threatening expense. A practical overview of Mitchell-Joseph workers' compensation is useful here because it frames workers comp the way contractors deal with it: as a jobsite, payroll, and contract issue, not just a policy form.

Table of Contents

- Your Guide to Workers Comp Compliance

- The Five Pillars of Workers Comp Compliance

- Quick Reference Table Workers Comp Requirements by State

- When Coverage Kicks In Employee Thresholds

- Owner Exemptions and Officer Rules

- The Subcontractor and 1099 Insurance Trap

- Working Across State Lines A Contractor's Dilemma

- Penalties and Your Next Steps to Full Compliance

Your Guide to Workers Comp Compliance

A concrete crew based in one state can look fully insured on paper and still run into trouble the minute it starts work in another. The owner may have a valid policy, payroll reports may be clean, and the certificate may have satisfied local jobs for years. None of that guarantees the next state will view the business the same way.

That's where contractors get trapped. Many online guides turn workers comp requirements by state into a static checklist. Contractors don't operate in a static world. Crews move, job sites change, subs get added at the last minute, and payroll classifications shift when field staff split time between shop work and site work.

The jobsite version of the problem

A small plumbing contractor wins a tenant improvement project in a neighboring state. The PM asks for a certificate showing workers comp that satisfies the project's state requirements. The contractor assumes the home-state setup carries over. Then someone asks a harder question: who on this crew counts as an employee under that state's rules?

That question can affect all of these at once:

- Bid eligibility: The project may not release the contract without acceptable proof of coverage.

- Mobilization timing: The crew can't start if the insurance requirement isn't right.

- Injury exposure: If someone gets hurt before the coverage issue is fixed, the business may face a direct financial problem.

- Subcontractor management: A subcontractor's missing policy can create a problem for the hiring contractor, not just for the sub.

Practical rule: Contractors shouldn't ask only whether they carry workers comp. They should ask whether the policy, employee count, ownership setup, and state filings match the job they're about to perform.

What actually works

The contractors that handle this well do a few things early. They review state rules before bidding. They check how owners, officers, and part-time staff are counted. They verify subcontractor workers comp instead of relying on a 1099 label. They also clear multi-state exposure with an advisor before the crew crosses the border.

What doesn't work is assuming the home-state rule follows the truck.

A gardening service adding a spring crew, an electrician opening work in a second state, and a restoration contractor chasing storm work all face the same core issue. The legal trigger for workers comp may change faster than the contractor's operations plan. That's why workers comp compliance has to be treated as part of project planning, not something left for renewal season.

The Five Pillars of Workers Comp Compliance

Contractors usually need five answers before they can tell whether they're compliant. Not just “insured,” but compliant for the trade, payroll, ownership structure, and states where the work happens.

Employee thresholds

The first question is simple on the surface. How many employees trigger the requirement? The answer is where many contractors get surprised.

For trade businesses, thresholds vary sharply by jurisdiction. Alabama requires coverage at five or more employees, Wisconsin at three or more employees, while New York and New Jersey are effectively near-universal coverage states for employers according to the state-by-state comparison published by NFIB. A contractor with a small office staff and one field helper may sit below the trigger in one state and still need coverage in another.

Who counts as an employee

Payroll software often gives a false sense of certainty. A worker may be part-time, seasonal, family-related, or paid irregularly, but that doesn't automatically remove them from the count. Construction firms need to compare the legal definition used by the state, not the shorthand used in bookkeeping.

A masonry contractor, for example, may use a mix of yard staff, delivery support, and site labor. If the business only counts full-time bricklayers, the analysis is probably too narrow.

Officers and owners

Owners often assume they're either always excluded or always covered. Neither assumption is safe. Corporate officers, members, partners, and sole proprietors can be treated very differently depending on state and entity type.

That's also where premium planning gets more technical. Businesses that want to understand how payroll, class codes, and claims history can affect cost should also review how a workers comp experience modification factor fits into the bigger picture.

Subcontractor liability

The 1099 label doesn't erase workers comp exposure. If a general contractor hires a framing sub that has no valid workers comp policy, the injury problem can travel uphill. This is one of the biggest mistakes in contractor insurance administration because it often starts with convenience. The sub is available, the schedule is tight, and no one verifies coverage carefully enough.

Penalties and enforcement

Every state enforces compliance in its own way. The exact penalties vary, but the practical outcomes are familiar: project disruption, contract issues, claim disputes, and direct financial exposure after an injury.

The expensive mistake usually isn't buying the policy. It's learning too late that the business needed a different setup than the one it had.

For contractors, these five pillars work best as a standing checklist:

- Threshold check: How many workers trigger coverage where the job is located?

- Classification check: Who counts as an employee under that state's rules?

- Ownership check: Are officers or owners included, excluded, or elective?

- Subcontractor check: Does every sub have active workers comp when required?

- Jurisdiction check: Does the state where the work happens impose separate obligations?

Quick Reference Table Workers Comp Requirements by State

The table below works best as a starting screen, not as the final answer. Contractors should use it to spot obvious issues fast, then confirm the details that matter most to the job at hand: employee count, ownership treatment, subcontractor use, and where work is physically being performed.

Because state rules can turn on details like entity type, place of hire, or whether the work starts immediately, this quick-reference format is most useful for pre-bid review. A Pennsylvania contractor comparing nearby expansion opportunities can also use this alongside a practical overview of Pennsylvania workers compensation insurance when evaluating local obligations.

State-by-State Workers' Compensation Thresholds & Rules for 2026

| State | Employee Threshold | Officer/Owner Exemption Rules | Subcontractor/1099 Guidance | Link to State Board |

|---|---|---|---|---|

| Alabama | Coverage required at five or more employees | Confirm by entity type and state rule | Don't rely on 1099 status alone. Verify independent subcontractor coverage | Official state workers comp authority |

| New Jersey | Near-universal for nearly all employers | Corporations have no minimum payroll or single-officer exemption. Partnerships and LLCs cover employees while excluding partners or LLC members from the count | Out-of-state employers may also trigger obligations if contract or work connects to New Jersey | Official New Jersey workers comp resources |

| New York | Virtually all employers require coverage | Confirm officer treatment and elective options by entity structure | Subcontractor review should include active workers comp proof | Official New York workers comp board |

| Pennsylvania | Confirm based on state rule and business facts | Confirm owner treatment and election rules | Coverage begins on the first day on the job for covered workforces, which matters for short hires and traveling crews | Official Pennsylvania workers comp authority |

| Wisconsin | Coverage required at three or more employees | Corporate officers generally count toward thresholds. Sole proprietors, LLC members, and partners generally do not | Verify subcontractor status carefully before work starts | Official Wisconsin workers comp agency |

| Texas | Not covered by a state workers comp system for most employers | Confirm voluntary arrangements and contract requirements carefully | Project owners and upstream contractors may still impose proof requirements | Official Texas workers comp resources |

| South Dakota | Not covered by a state workers comp system for most employers | Confirm business-specific obligations and contract requirements | Contract risk still makes proof of coverage an important issue | Official South Dakota workers comp resources |

| Wyoming | Coverage required for workers in extra-hazardous occupations | Confirm whether the trade falls within required classes | Do not assume home-state treatment applies | Official Wyoming workers comp resources |

When Coverage Kicks In Employee Thresholds

The employee threshold question looks simple until a contractor starts counting real people instead of boxes on an org chart. That's where mistakes happen. A business may think it has two employees because only two people are full-time field staff, while the state may look at the office coordinator, part-time estimator, and seasonal laborer too.

The broad starting point is this: workers' compensation is mandatory in all but three states: Texas, South Dakota, and Wyoming. The National Academy of Social Insurance explains that Texas and South Dakota do not cover employers through a state workers' comp system, while Wyoming requires coverage only for workers in “extra-hazardous” occupations in its system, as described in the NASI workers compensation report. For most contractors operating in more than one state, that makes workers comp close to a universal compliance issue.

Why the headcount gets misread

Contractors often count only the people swinging hammers or turning wrenches. States may not limit the analysis that way. A part-time dispatcher, a spouse doing payroll, or a temporary laborer used during the busy season may matter depending on the jurisdiction and business structure.

A landscaping contractor is a good example. During winter, the payroll might be lean. In spring, the business brings on mowing crews, irrigation helpers, and office support. If the owner only thinks in terms of permanent year-round staff, the company may miss the point where coverage is required.

Common counting mistakes

The following issues come up repeatedly in contractor reviews:

- Part-time staff: A worker doesn't need a full-time schedule to become relevant under state rules.

- Seasonal hires: Busy-season labor can change the compliance picture quickly.

- Admin personnel: Office employees still count in many states even if they never visit a site.

- Family on payroll: Family relationship alone doesn't settle whether someone is counted.

- Mixed roles: A shop worker who also performs field tasks can complicate both counting and classification.

A contractor should count people the way the state counts them, not the way the payroll app labels them.

A better audit method

For practical field use, contractors should audit the workforce by relationship to the business, not by tax form alone. Start with everyone who receives wages or regular compensation tied to the operation. Then separate owners, officers, members, part-time staff, temporary hires, and subcontractors. After that, apply the state's rules to each category.

A small electrical contractor can do this with a basic worksheet:

- List every working person tied to the business.

- Mark each one by role. Office, field, owner, officer, family member, helper, seasonal, subcontractor.

- Mark where the work is performed. Home state only, multiple states, temporary out-of-state jobs.

- Confirm state treatment before a bid goes out.

The trade-off contractors face

Some owners hesitate because they don't want to add cost before they think they have to. That instinct is understandable, especially in low-margin trades. But the downside of waiting is bigger than the premium issue. A contractor may lose a project, fail a vendor setup, or face an uninsured injury problem that costs far more than carrying the right policy from the start.

For a drywall company adding a third installer, the question isn't just “Are there enough employees yet?” The better question is whether the business is already operating in a way that a state, a GC, or a claims adjuster would treat as subject to workers comp requirements.

Owner Exemptions and Officer Rules

Owner exemptions create more confusion than almost any other workers comp topic in contracting. Many owners assume the answer is tied to common sense. If they own the company, they think they can exclude themselves. Sometimes they can. Sometimes they can't. Sometimes the answer changes based on whether the business is a corporation, partnership, LLC, or sole proprietorship.

The problem gets more serious when the owner still works in the field. A master plumber who owns the company but spends most days on ladders, in crawl spaces, and around active jobsite hazards is taking on a very different risk than a passive owner who only handles contracts and banking.

State treatment can differ sharply

Ownership rules aren't standardized. In New Jersey, corporations have no minimum payroll or single-officer exemption, and partnerships and LLCs must cover employees while excluding partners or LLC members from the count. In Wisconsin, corporate officers generally count toward employee thresholds, while sole proprietors, LLC members, and partners generally do not, according to the New Jersey guidance on counting ownership roles and employer obligations.

That difference matters in practice. Two contractors with similar payroll and similar revenue can end up with different workers comp obligations based on where they work and how the business is organized.

A side-by-side trade example

Consider two business owners doing hands-on trade work:

| Business setup | Field reality | Compliance question |

|---|---|---|

| S-corp electrician | Owner still installs panels and troubleshoots service calls | Can the officer be excluded, and is that wise if the owner is exposed to live-work hazards? |

| LLC plumber | Owner performs service calls and supervises helpers | Does the state count the member toward the threshold, and will employees still need mandatory coverage? |

The legal answer depends on the state. The risk answer is more practical. If the owner's labor is essential to the company and the owner gets hurt, excluding that person may reduce premium but increase financial fragility.

What works and what backfires

A careful owner exemption decision usually considers both compliance and business continuity.

- What works: Reviewing the rule by entity type before payroll is reported, matching officer treatment to state law, and deciding whether exclusion makes operational sense.

- What backfires: Assuming an accountant's tax treatment answers the insurance question, or excluding a working owner just to cut premium without considering injury exposure.

- What deserves extra review: Single-officer corporations, husband-and-wife operations, and family-run trades where everyone does a little of everything.

A legal exemption and a smart risk decision aren't always the same thing.

For a small HVAC company, excluding the owner may look attractive on paper. But if that owner is the one climbing attic ladders, brazing line sets, and handling emergency service calls, the company is betting that the one person it can least afford to lose won't get injured.

That's why owner treatment should never be handled as a box-checking exercise. For contractors, it's a coverage design decision tied directly to how the company runs.

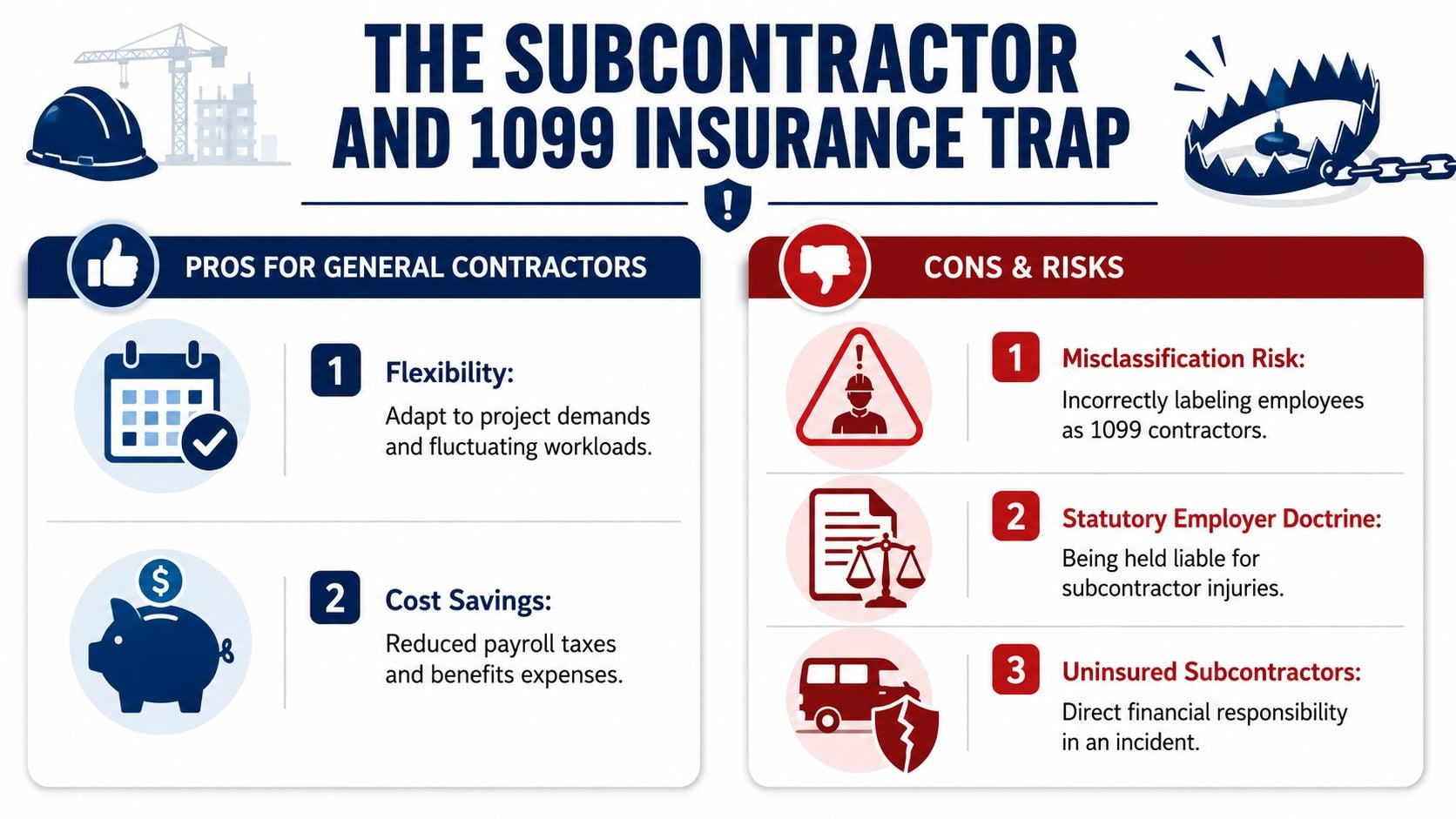

The Subcontractor and 1099 Insurance Trap

A general contractor hires a drywall crew for a fast commercial build-out. The crew arrives with tools, starts hanging board, and sends invoices as an independent subcontractor. Everything feels clean because the GC isn't treating them as payroll employees. Then one worker falls and gets badly hurt. The GC asks for the subcontractor's workers comp certificate and learns there isn't one.

That's the trap. The 1099 label can make a labor arrangement look simpler than it is. But workers comp exposure doesn't disappear because payment is structured as subcontract labor instead of payroll wages.

Why this problem hits general contractors hard

In construction, liability often moves uphill. If the subcontractor isn't properly insured, the hiring contractor may be pulled into the problem through contract obligations, site control, or state treatment of uninsured labor relationships. Even before a formal legal analysis starts, the project owner, upstream GC, or carrier is going to ask the same question: who should have made sure this crew was covered?

That's why a subcontractor file needs more than a signed W-9 and a handshake.

What a contractor should collect before work starts

A practical subcontractor screening process should include:

- Current workers comp proof: Ask for a valid certificate that shows active workers comp coverage where required.

- Entity review: Confirm whether the sub is operating as a sole proprietor, corporation, partnership, or LLC.

- Scope match: Make sure the trade shown on the insurance documents matches the work being performed.

- Expiration check: A certificate that lapses mid-project creates a live problem, not just a paperwork problem.

- Crew review: Confirm whether the sub uses employees or further lower-tier subs.

Contractors dealing with owner-only operations in Florida often run into exemption questions, so a focused resource on workers' comp exemption for Florida owners can help clarify why exemption paperwork still doesn't excuse poor subcontractor vetting by the hiring contractor. For broader risk control on hired trades, a practical review of workers comp for subcontractors helps frame what should be collected before a crew is allowed on site.

The myth that creates the loss

The myth is simple: if the subcontractor gets paid on a 1099, then the hiring contractor is safe.

That approach fails in several ways. First, tax treatment and workers comp treatment aren't the same question. Second, a certificate request made after an injury is already too late. Third, project owners and upstream contractors often care less about labels than about whether there was valid coverage in force when the injury occurred.

If a subcontractor can't produce solid workers comp documentation before mobilizing, the hiring contractor should treat that as a risk decision, not an admin delay.

A painting contractor hiring an overflow crew for a school project may feel pressure to keep the schedule moving. The better move is to slow down long enough to verify the paperwork. Delays can be managed. Uninsured injury disputes usually get more expensive and more disruptive the longer they sit.

Working Across State Lines A Contractor's Dilemma

The hardest workers comp problems usually start when a contractor thinks in home-state terms and the job happens somewhere else. A storm-repair roofer may be insured in one state, chase hail work into another, and assume the existing policy setup will carry the company through the project. Sometimes it won't. The state where the work is performed may have its own rules about when coverage applies, when local obligations begin, and whether the out-of-state employer needs a different arrangement.

The question contractors should ask

The useful question isn't just whether the home state requires workers comp. It's whether the state tied to the worker, jobsite, hiring arrangement, or project contract imposes its own requirement.

That's especially important for mobile trades:

- Roofers: Crews move quickly after storms and may cross state lines on short notice.

- HVAC installers: Multi-week commercial installs often happen outside the company's home state.

- Restoration firms: Emergency response work can start fast, before the insurance review catches up.

- Specialty subcontractors: A small crew may follow a GC into a jurisdiction the company hasn't worked in before.

Why short-duration work can still trigger obligations

New Jersey explicitly says that out-of-state employers may need coverage if a contract of employment is entered into in New Jersey or if work is performed there, and Pennsylvania says coverage begins on the first day on the job, according to the New Jersey employer requirements guidance. For contractors, that shifts the conversation from “Where is the company based?” to “Which state's rules attach to this actual work?”

That's where certificates often fail. A COI may be accurate as far as it goes, but it may not satisfy a project requirement if the policy hasn't been structured for the state where the crew is headed.

A workable pre-bid process

Before taking an out-of-state project, contractors should run a short insurance check tied to the job itself.

- Confirm where the work will physically occur.

- Confirm where the worker was hired and where the employment relationship connects.

- Ask whether the policy addresses that state exposure clearly enough for certificate review.

- Review subcontractor paperwork separately if local subs will be used.

- Check contract transfer language, including whether upstream parties want added protection such as an additional insured endorsement.

Multi-state compliance fails most often when a contractor treats insurance as a home-office issue instead of a jobsite issue.

An Indiana HVAC firm sending technicians into Illinois, or a New Jersey electrical contractor sending a crew into Pennsylvania, needs more than a generic assumption that “the policy covers us everywhere.” The right answer depends on the state rules attached to the work, the people doing it, and the contract that put them there.

Penalties and Your Next Steps to Full Compliance

Non-compliance usually doesn't stay theoretical for long. It shows up when a project owner rejects a certificate, when an upstream contractor asks for proof that isn't there, or when a worker gets hurt and the company learns the policy setup didn't match the exposure. For contractors, the immediate cost is often lost time. After that comes claim friction, contract trouble, and direct financial pressure.

That's why this issue shouldn't be handled like a paperwork cleanup project. It belongs in estimating, hiring, subcontractor onboarding, and pre-mobilization review.

Where contractors slip

The most common failures are operational, not intentional:

- Home-state assumptions: The business assumes local rules follow the crew into other states.

- Loose worker counting: Part-time, seasonal, and mixed-role workers are ignored.

- Bad subcontractor files: A GC collects incomplete certificates or never checks expiration dates.

- Owner confusion: Officers or members are handled based on guesswork instead of state treatment.

- Late review: Insurance gets checked after the contract is signed instead of before the bid goes out.

A simple compliance action plan

A contractor doesn't need a legal memo to start tightening this up. A practical review usually starts with three steps:

- Check the state issue first. Use the quick-reference section to identify where threshold, ownership, or cross-state questions are likely to exist.

- Audit the full workforce. Review W-2 staff, part-time help, seasonal labor, owners, officers, and subcontractors using state definitions rather than internal labels.

- Review premium and structure before growth. If payroll, crew mix, or state footprint is changing, review how the policy is built and how cost drivers work, including workers compensation insurance premiums.

One practical option is Coverage Axis, an independent commercial insurance advisory that helps contractors shop multiple carriers and match workers comp structure to trade, crew size, and project type. The value in that kind of review is simple: it can identify whether the policy fits the work being done, not just whether a policy exists.

Contractors that treat workers comp as part of job planning usually have fewer surprises when certificates, payroll audits, and claims hit the desk.

Workers comp carries significant implications because it sits at the intersection of compliance and survival. A contractor can recover from a tough audit. Recovering from a bad injury with the wrong setup is much harder.

If the business is adding employees, using more subcontractors, or taking work across state lines, this is the right time to request a free quote or coverage review from Coverage Axis. A licensed advisor can review the crew structure, project footprint, and current policy setup, then help close workers comp gaps before they turn into claim or contract problems.