A lot of Pennsylvania contractors run into the same problem at the worst possible time. The crew is lined up, the materials are ordered, and the job is finally big enough to move the business forward. Then the general contractor or property manager asks for proof of workers comp before anyone steps on site.

That request stops the job cold if the business owner has been relying on day labor, family help, or subcontractors paid on a 1099. For a small plumbing outfit, that can happen the moment a commercial fit-out or municipal repair contract lands on the desk. Until then, workers comp can feel like paperwork. Once a contract requires it, it becomes the difference between getting on the schedule and getting replaced.

Pennsylvania contractors usually don't need another generic insurance article. They need a field guide that deals with the choices they make every week. Who counts as an employee. How payroll should be classified. What to do when a sub sends an old certificate. Whether SWIF is the right move for a new or higher-risk operation. That's where workers compensation insurance in PA becomes a practical business issue, not just a legal one.

Table of Contents

- The Moment Every PA Contractor Faces

- Why Pennsylvania Requires Workers Comp Insurance

- When You Must Get Coverage in Pennsylvania

- How Your Workers Comp Premium Is Calculated

- Shopping for Coverage From Private Carriers to SWIF

- Managing Claims Audits and Subcontractor Compliance

- Take Control of Your Workers Comp Program

The Moment Every PA Contractor Faces

A plumbing contractor in Pennsylvania can run for years on small residential jobs with a loose staffing model. One week it's a cousin helping on a water heater replacement. The next week it's a “sub” handling rough-in work on a bathroom remodel. Cash flow stays manageable, and nobody asks many questions.

Then a larger commercial job comes in. The contract package asks for a certificate of insurance showing active workers comp. The owner calls the office manager, checks the existing policies, and realizes there isn't one.

That's the moment workers compensation insurance in PA stops being theoretical.

The problem usually isn't bad intent. It's growth. A contractor starts with owner-only work, adds a helper for busy weeks, and leans on 1099 labor because it feels flexible. Then a school project, retail fit-out, or tenant improvement job demands documentation before badges are issued or materials are delivered. The same contractor who could handle the work operationally can't clear the insurance requirement.

Bigger jobs often expose insurance gaps that small jobs let slide.

For a trade business, workers comp isn't just there to satisfy the state. It also acts as a gatekeeper for contracts, vendor approval, and jobsite access. A general contractor doesn't want to sort out injury responsibility after a loss. They want proof up front.

Contractors who are still sorting out the rest of their insurance stack can get a broader view from this guide to contractor insurance requirements. Workers comp is one part of that picture, but it's often the part that blocks the job first.

A roofer using two regular helpers has one set of issues. An electrician mixing W-2 techs with 1099 installers has another. The common thread is simple. If the business is growing, workers comp usually becomes unavoidable before the owner expects it.

Why Pennsylvania Requires Workers Comp Insurance

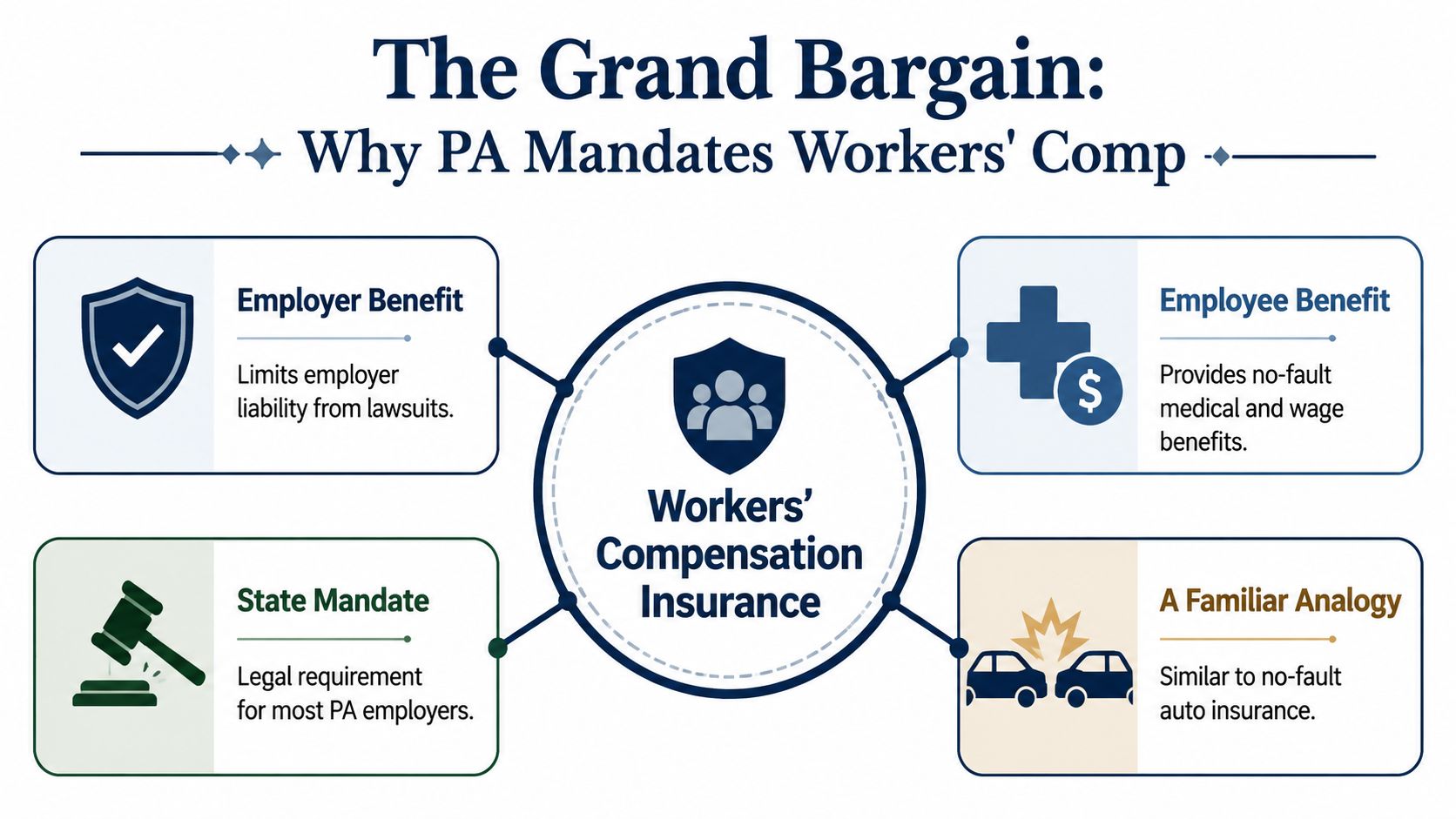

Pennsylvania didn't create workers comp as an optional benefit. It built it into how employers and employees handle workplace injuries. The Pennsylvania Workers' Compensation Act was enacted in 1915, and the state still requires most employers with one or more employees to carry coverage. Employers can buy that coverage through a licensed insurance carrier or through the State Workers' Insurance Fund, as described by Pennsylvania workers comp rules summarized here.

The two way shield on a jobsite

The simplest way to explain workers comp is that it works like a two-way shield.

If a roofer's employee falls off a ladder, workers comp is designed to provide medical care and wage benefits without turning fault into the first fight. On the employer side, the system helps limit direct injury-related lawsuits that could otherwise threaten the business itself. That's why contractors will often hear the term exclusive remedy. In plain language, it means the workers comp system is generally the main path for handling covered employee injury claims.

A lot of contractors understand liability insurance better because they see certificates for it all the time. Workers comp is different. It responds to injury claims involving employees, while a separate policy handles many third-party injury allegations. That distinction matters when reviewing employers liability insurance as part of the overall protection plan.

Practical rule: If your crew uses ladders, saws, trenchers, service vans, or roofs, workers comp isn't abstract. It's built for the exact injuries that can shut down a trade business fast.

Why this matters to growing contractors

The law matters most when a contractor starts hiring. A solo owner doing all field work alone may view insurance differently from a masonry company adding laborers for a foundation project. The moment payroll enters the picture, employment rules get tighter. Business owners trying to stay current on hiring duties, notices, and classification issues often benefit from understanding employment regulations alongside their insurance decisions.

For contractors, the key point is this. Pennsylvania requires workers comp because jobsites create injury risk, and the state wants a defined system in place before that injury happens. That protects the worker, and it also gives the employer a structured process instead of a financial free-for-all after an accident.

When You Must Get Coverage in Pennsylvania

Most contractors ask the question too late. They don't ask when they hire the first helper. They ask when a customer requests a certificate or when payroll is already moving.

Pennsylvania treats workers comp as a broad employer obligation. The law requires most employers with employees to carry coverage, including part-time and seasonal staff, and only narrow exemptions apply, according to Pennsylvania employer requirements outlined here.

The trigger is usually simpler than contractors expect

For a landscaping contractor, the trigger may be one summer worker. For an HVAC shop, it may be the first office employee answering phones and scheduling service calls. For a painter, it may be the part-time helper who tapes, moves ladders, and finishes with cleanup.

What trips people up is the assumption that “part-time” means “doesn't count.” In Pennsylvania, that assumption can create a compliance problem fast.

A lot of owners also assume family help falls outside the rule. That's another common mistake. If a spouse helps in the office, a son assists on installs, or a sibling drives materials to jobs, the business needs to analyze whether that person triggers the requirement instead of assuming the relationship changes the answer.

Common contractor situations that create problems

These are the scenarios that most often cause trouble:

- The paid helper: A small electrical contractor pays someone for rough-in assistance on busy weeks. The owner treats it as temporary labor. Pennsylvania may still treat that arrangement as one that requires coverage.

- The family member in the business: A flooring company brings in a relative to schedule jobs and collect deposits. The work feels informal, but the insurance obligation may not be.

- The seasonal crew member: A landscaping business hires spring and summer labor. Seasonal status doesn't automatically remove the requirement.

- The “independent” installer: A remodeling company uses the same finish carpenter repeatedly, gives direction on start times, and folds that person into the project schedule. That setup often deserves a hard look before calling the worker a true subcontractor.

A contractor sorting through these edge cases may also want a broader small-business view of workers comp coverage obligations, especially when the business is moving from owner-only work to a mixed staff model.

If a worker is part of how the business gets jobs done, the owner shouldn't assume labels like part-time, seasonal, or family-based remove the workers comp issue.

The safest approach is to review each worker by role, payment method, and job function before the project starts. That's especially important in trades where staffing changes week to week. A mason may be solo on one job and use two laborers on the next. The coverage obligation follows the workforce, not the owner's intentions.

How Your Workers Comp Premium Is Calculated

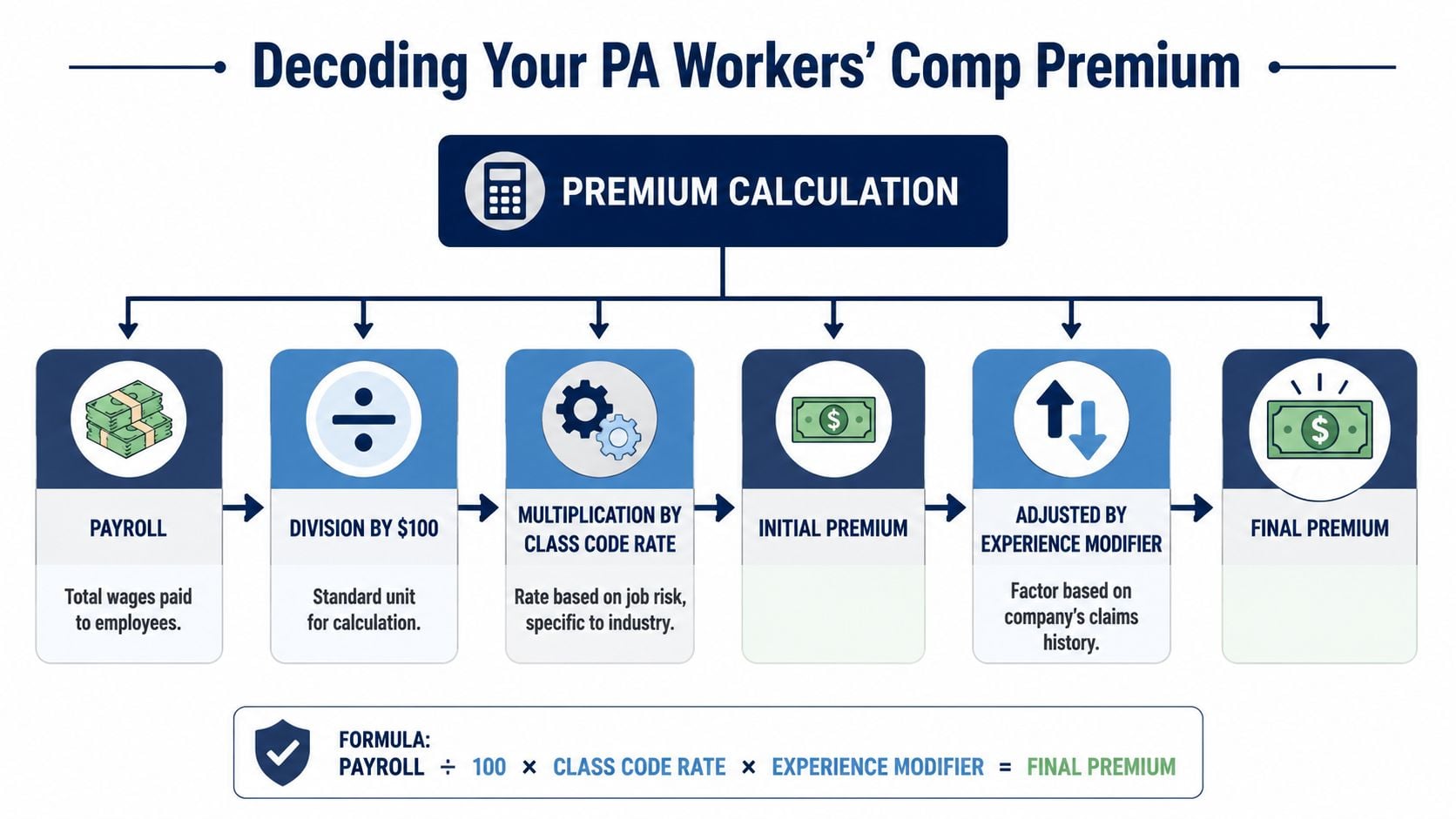

The premium usually starts with a simple concept even if the final number gets more technical. Payroll drives the exposure. Job duties shape the rate. Claims history can change the result.

For contractors, that means workers compensation insurance in PA is tied directly to how the business staffs jobs and records wages. A landscaping company with office staff, foremen, and mowing crews shouldn't expect one flat treatment across every role.

What actually drives the premium

At the working level, contractors should think in this sequence:

- Payroll is the starting point. The insurer looks at wages paid to employees.

- Class codes matter. A field installer and an office administrator don't present the same injury exposure.

- The rate follows the work. Higher-risk operations generally carry higher rates than clerical roles.

- Claims history can affect the final result. A business with a tougher loss record may not pay the same as a similar contractor with cleaner experience.

An HVAC company is a good example. Service techs climbing ladders, handling tools, and working in mechanical spaces present one exposure. The dispatcher in the office presents another. If payroll isn't separated correctly, the contractor can end up paying too much for low-risk wages or create problems at audit if the records don't support the classifications used.

Pennsylvania's injury data explain why insurers pay so much attention to trade risk. In 2023, the state reported 162,194 workplace injury and illness cases, and about $2.9 billion in wage and medical benefits were distributed statewide to injured employees, according to Pennsylvania workers compensation statistics. In a state with that level of claims activity, insurers price trade work carefully.

Where contractors lose control of cost

Most premium problems come from operations, not from the policy form itself.

- Mixed payroll without separation: A contractor pays one employee partly for shop work and partly for field work but keeps poor records.

- Wrong class code assumptions: The owner tells the insurer everyone is clerical except for one crew lead, even though multiple workers perform hands-on trade labor.

- Untracked labor changes: The business starts the year with repair work only and ends the year taking on new installation projects without updating the carrier.

- Claims management drift: Small injuries don't get documented early, and later they become harder to manage cleanly.

A company's experience modification factor can also affect premium. Contractors who want to understand how that piece works can review this plain-English guide to workers comp experience modification.

Clean payroll records do more than satisfy an auditor. They give the contractor a fairer premium basis.

A paving contractor can't control every claim. That contractor can control recordkeeping, role definitions, and whether each worker is assigned to the right classification. That's where premium management starts.

Shopping for Coverage From Private Carriers to SWIF

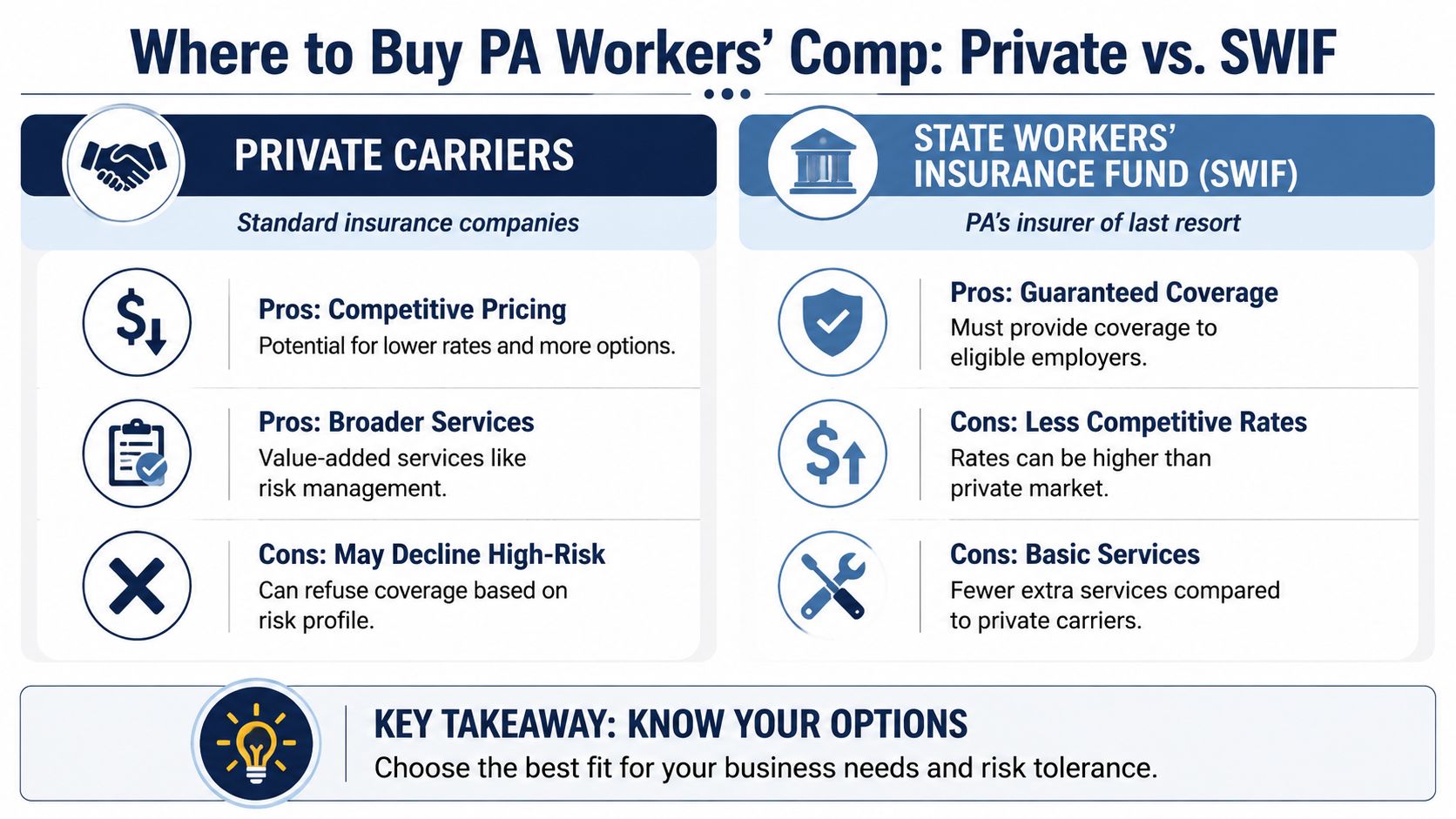

Pennsylvania contractors usually have two practical paths. They can buy a policy through a private carrier in the regular market, or they can look to SWIF, the State Workers' Insurance Fund.

That choice matters because not every contractor is viewed the same way. A long-established electrical company with stable payroll and clean records may have one set of options. A new roofing or demolition operation may have another.

Private market versus SWIF

A simple side-by-side view helps.

| Option | Best fit | Trade-offs |

|---|---|---|

| Private carriers | Contractors with a marketable risk profile, organized records, and operations that fit standard underwriting appetite | More choice and flexibility, but some contractors may be declined |

| SWIF | New businesses, harder-to-place trades, or contractors who can't secure standard market terms | A statutory path to coverage, but often with fewer options and less flexibility |

Private carriers can be a strong fit when the contractor has clear payroll reporting, a defined safety process, and stable operations. That often describes established plumbers, electricians, HVAC contractors, and similar trade firms with documented procedures.

SWIF matters when the voluntary market gets tight. Pennsylvania allows employers to obtain coverage through SWIF, which gives contractors and other employers a statutory path to comply with the state mandate, as noted earlier in the discussion of the state's framework.

Which path fits which contractor

A new excavation contractor may need SWIF first because the business has limited operating history and a risk profile that private underwriting may treat cautiously. An established drywall contractor with better documentation and a cleaner submission may have more room to shop.

One practical route is to work through an independent advisory that can shop multiple markets and identify whether the business fits the private market or needs assigned-risk style placement. Coverage Axis does that for contractor accounts, including workers comp placement based on trade, crew structure, and project type.

Some contractors don't need a cheaper policy first. They need an available policy first, then a cleaner path to better options later.

For a concrete contractor, the wrong move is waiting until the contract deadline to find out which market will even write the risk. The better move is deciding early whether the business is likely to fit standard underwriting or whether SWIF is the more realistic starting point.

Managing Claims Audits and Subcontractor Compliance

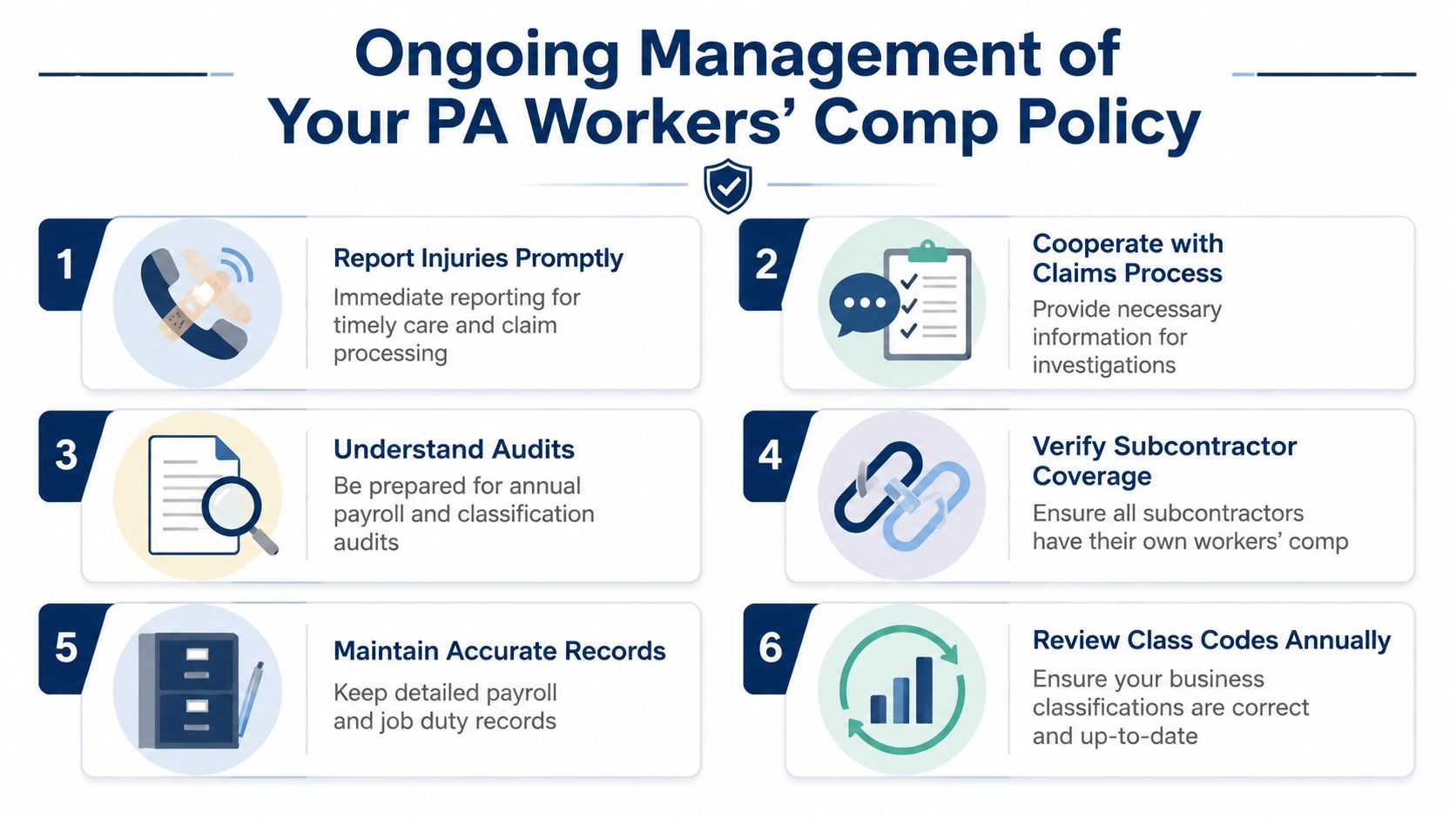

Workers comp isn't a buy-it-and-forget-it policy. It has to be managed in real time. The contractor has to respond when someone gets hurt, maintain records during the policy period, and prepare for the annual audit after the policy expires.

That matters most in construction because claim handling, payroll accuracy, and subcontractor paperwork all connect. A mistake in one area usually shows up somewhere else later.

Claims handling starts before the injury happens

Pennsylvania benefits generally involve wage-loss payments that typically pay about two-thirds of the injured worker's average weekly wage, subject to statutory maximums, while also covering medical care and other benefits. Claims generally must be filed within three years, employers must receive notice within 120 days, and approved-provider rules can apply in the early treatment period, as summarized in this overview of Pennsylvania workers comp benefit rules.

For a contractor, those rules create a straightforward responsibility chain:

- Report injuries fast: If a carpenter strains a back lifting material, don't wait to see if it “works itself out.”

- Direct the employee appropriately: Follow the policy and applicable provider rules for treatment.

- Document what happened: Write down task, location, witnesses, and tool or equipment involved.

- Stay involved: Respond to adjuster questions and provide payroll or job-duty details when requested.

A framing contractor who reports an injury late creates friction immediately. Medical treatment may still happen, but late reporting can complicate compensability, return-to-work planning, and claim documentation.

Audits and subcontractors are tied together

The annual audit is where many contractors get blindsided. The insurer compares estimated payroll to actual exposure. If books are messy, workers are misclassified, or uninsured subcontractor labor shows up in the records, the premium can increase.

Pennsylvania specifically notes that coverage is mandatory if all workers do not fit an exemption, and it explicitly states that part-time workers and family members still trigger the requirement. For contractors, that means misclassifying a subcontractor can lead to surprise premium charges during an audit, according to Pennsylvania employer guidance on worker status and exemptions.

That's why subcontractor compliance should be handled like a repeatable process, not a last-minute file chase.

- Collect certificates before work starts: Don't let the sub mobilize first and send documents later.

- Check that the policy is active: Expired certificates create avoidable audit trouble.

- Match the named insured to who is being paid: If the invoice name doesn't match the certificate, ask why.

- Keep records together: Store certificates with contracts, payment records, and scope details.

- Review subs each year: A subcontractor who had coverage last year may not have it now.

Contractors that rely heavily on independent crews can dig deeper into workers comp for subcontractors when building a certificate and audit process.

The audit surprise usually didn't start at audit time. It started the day the contractor hired a sub without checking coverage.

A masonry contractor using labor-only subs on short projects faces this risk constantly. If the paperwork is weak, the policy will eventually reflect that weakness.

Take Control of Your Workers Comp Program

For Pennsylvania contractors, workers comp is part compliance tool, part financial control system, and part ticket to better work. It affects whether the business can bid, whether payroll is priced correctly, and whether a subcontractor relationship creates a hidden cost later.

Three habits matter most.

First, treat coverage as necessary the moment the workforce expands beyond a true owner-only setup. Second, keep payroll and job duties clean enough that classifications can be defended. Third, demand current proof of coverage from every subcontractor before any work begins.

A contractor who does those three things usually makes better insurance decisions across the board. A contractor who ignores them often finds out there's a problem when a claim happens, a certificate is requested, or the audit bill arrives.

Workers compensation insurance in PA doesn't have to be mysterious. It does have to be managed.

If your business is hiring, bidding larger jobs, or relying on subcontractors, Coverage Axis can help with a free quote and workers comp coverage review built around your trade, crew setup, and project mix.