A small painting contractor lands a commercial office repaint. The crew has handled houses, small tenant improvements, and punch work for years. Then the property manager asks for a certificate showing workers comp before anyone can start.

That's the moment a lot of trade owners hit the same wall. They've been paying helpers or “subs” on 1099s, assuming that kept them outside the workers comp system. Then a larger client, a general contractor, or a state audit forces a harder question: who counts as an employee, and what happens if someone gets hurt before the paperwork catches up?

For small contractors, workers comp isn't just a legal box to check. It's often the difference between staying stuck on small cash jobs and qualifying for larger, steadier work. It also protects the business from the kind of injury cost that can wreck a small crew's budget. The National Safety Council reported that the average cost of all workers' compensation claims for accidents in 2021–2022 was $44,179, and motor-vehicle crashes averaged $90,914 per claim on the same basis, according to the National Safety Council workers' compensation cost data.

A contractor trying to grow needs to think about workers comp the same way they think about licensing, payroll, and contracts. It's part of becoming bid-ready. It's also part of meeting common general contractor insurance requirements before a project owner ever hands over the job.

Table of Contents

- Introduction

- What Workers Comp Covers on a Real Jobsite

- State Rules and the Subcontractor Trap

- Decoding How Your Workers Comp Premium Is Priced

- The Biggest Cost Drivers You Actually Control

- Shopping for the Right Policy Not Just the Cheapest

- Actionable Ways to Lower Your Workers Comp Premiums

- Protecting Your Crew and Your Business

Introduction

A small contractor usually doesn't start by worrying about workers comp. The early focus is simple: get the truck running, keep the jobs booked, and find reliable help. For a while, that can make workers comp feel like something only larger companies deal with.

Then the business changes. A painting contractor wins a better commercial job. A framing crew adds a part-time helper. A plumber uses borrowed labor for a remodel that runs long. Suddenly, the old assumption that “everyone's a subcontractor” stops working.

That shift matters more than many owners realize. The National Academy of Social Insurance estimated that 850,427 jobs were excluded from mandatory workers' compensation coverage in 2020 because of small-firm exemptions, according to the NASI workers' compensation report using 2020 data. The same source notes that small businesses, defined for that research as fewer than 50 employees, tend to have higher rates of injuries and illness than larger firms and often have fewer resources for formal safety and health programs.

For trade contractors, that's the issue. Small crews face live jobsite risk, payroll changes, and shifting labor arrangements, but they usually have less room for error when a claim happens. That's why workers comp for small business matters so much in construction and service trades. It isn't paperwork. It's a financial backstop and a gatekeeper for better work.

The contractor who understands workers comp early usually has an easier time growing than the one who waits until a claim, an audit, or a contract requirement forces the issue.

What Workers Comp Covers on a Real Jobsite

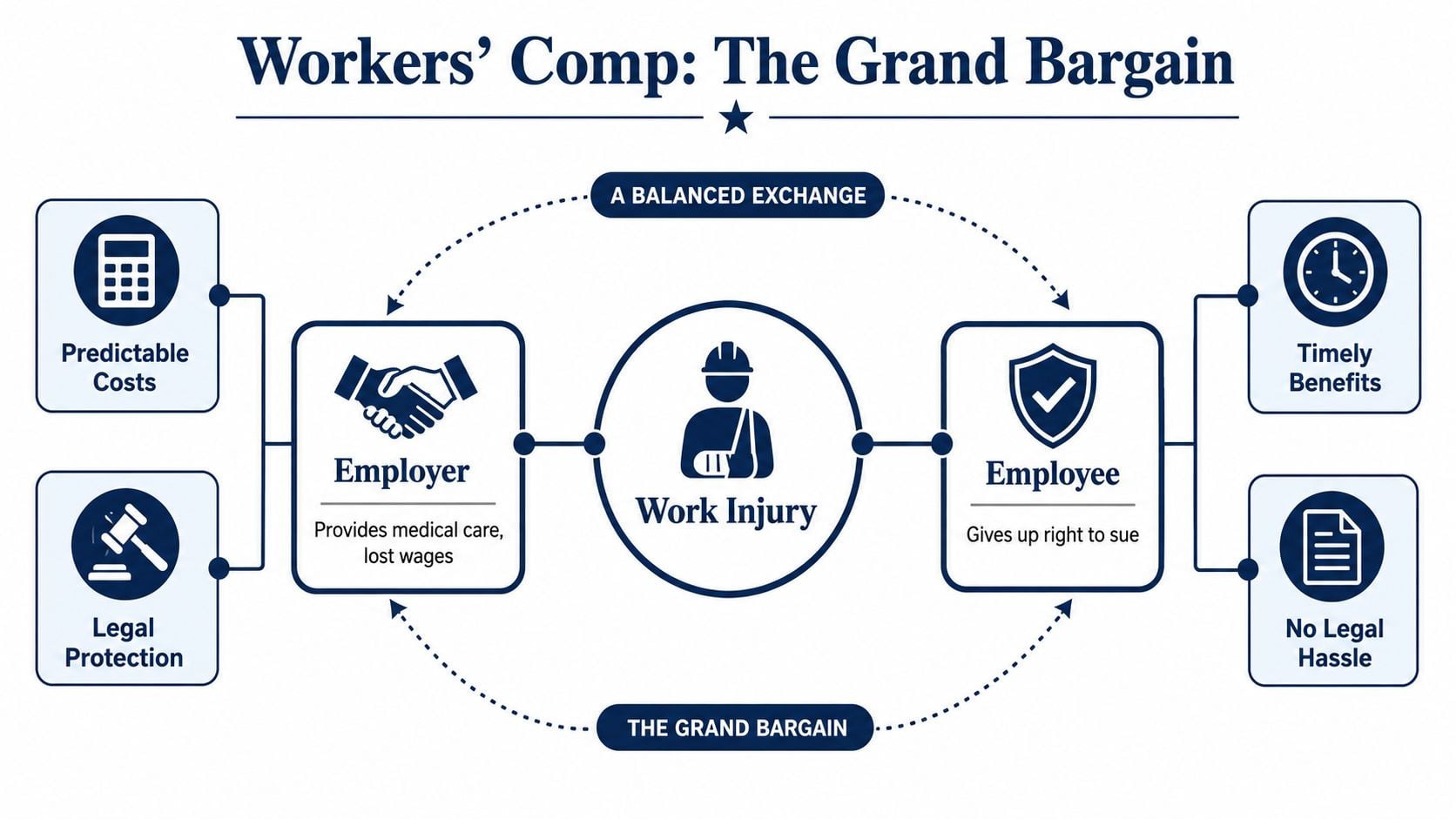

Workers comp is built around a practical exchange. If someone gets hurt doing the job, the policy responds without turning every injury into a fault fight between employer and worker.

How the no-fault tradeoff works

The CDC explains that workers' comp is a no-fault system that pays medical expenses, rehabilitation, and partial wage replacement while limiting most employee lawsuits against the employer, as outlined by CDC NIOSH on how workers' compensation works.

For a contractor, that tradeoff is a big deal. A business owner doesn't have to fund every covered medical bill out of pocket or defend most injury lawsuits the old-fashioned way. The employee gets a defined path to treatment and partial wage replacement while recovering.

An electrician on a residential remodel is a good example. A helper opens a panel, gets shocked by faulty wiring, and ends up in the emergency room. Workers comp can step in for the emergency visit, follow-up care, rehabilitation if needed, and part of the worker's lost wages while that person can't return to normal duties.

What coverage looks like after an injury

On an actual job, the value shows up in very ordinary places:

- Medical treatment gets started fast. Emergency care, specialist visits, and rehab aren't left to the worker and owner to argue over in the parking lot.

- Lost time doesn't turn into a total income gap. The system is designed to provide partial wage replacement while the employee is out.

- The claim has a process. That matters when the crew is small and one injury can throw off the schedule, payroll, and customer commitments.

Practical rule: If an owner can picture exactly how an injury would be handled on a Tuesday afternoon jobsite, that owner is already ahead of most small businesses.

Claims handling still matters. Delays, poor communication, and bad documentation can drag out recovery and payroll disruption. Contractors trying to understand the human side of the process can review this guide on speeding up workers' comp recovery and payments, which helps explain why treatment coordination and return-to-work planning matter after the first report is filed.

The mistake is treating workers comp like a paper requirement only. On a real jobsite, it's part medical response plan, part wage protection, and part lawsuit shield.

State Rules and the Subcontractor Trap

Most contractors don't get in trouble because they meant to ignore the rules. They get in trouble because they relied on a shortcut. The biggest shortcut in this area is assuming a 1099 settles the question.

Why a 1099 doesn't settle the issue

For construction, landscaping, and repair businesses, the better question is who controls the work. New York's Workers' Compensation Board says employees can include day laborers, leased staff, volunteers, part-time workers, family members, and “most subcontractors.” It also warns that workers under direct control may be treated as employees even if they receive 1099s, as stated in the New York Workers' Compensation Board guide for business owners.

That's why workers comp for small business gets messy fast in the trades. A contractor may think the crew is made up of independent subs, but the state may see employees if the business sets the hours, directs the sequence of work, provides the tools, or folds those workers into daily operations.

Contractors operating in more than one state need to stop guessing. A practical starting point is Benely's state workers' comp guide, then compare that with trade-specific advice on workers comp for subcontractors before hiring for the next project.

A landscaping example that goes sideways fast

A landscaping company lands a large spring cleanup contract. The owner brings in three “1099 subs” for two weeks. The company truck picks them up in the morning. The owner supplies the mowers, trimmers, and blowers. The crew follows the company foreman's route and works the same schedule each day.

On paper, that may look like subcontracting. In practice, it often looks a lot more like employment.

If one of those workers gets injured, the problem usually shows up all at once:

| Jobsite fact | Why it matters |

|---|---|

| The business sets hours | Direct control suggests employee status |

| The business provides tools and equipment | Independent businesses usually bring their own |

| The worker performs the core trade work | That's harder to separate from regular payroll labor |

| The owner supervises the daily tasks | Control is one of the first things regulators review |

A worker's tax form and a worker's legal status are not always the same thing.

That's the subcontractor trap. The business saves money in the short term, then faces a much bigger problem after an injury or audit. For contractors, the safer move is to review labor setup before the project starts, not after someone falls, gets cut, or crashes a truck.

Decoding How Your Workers Comp Premium Is Priced

A lot of owners treat workers comp pricing like a mystery. It isn't. The formula is straightforward, even if the moving parts can get expensive.

The three parts of the formula

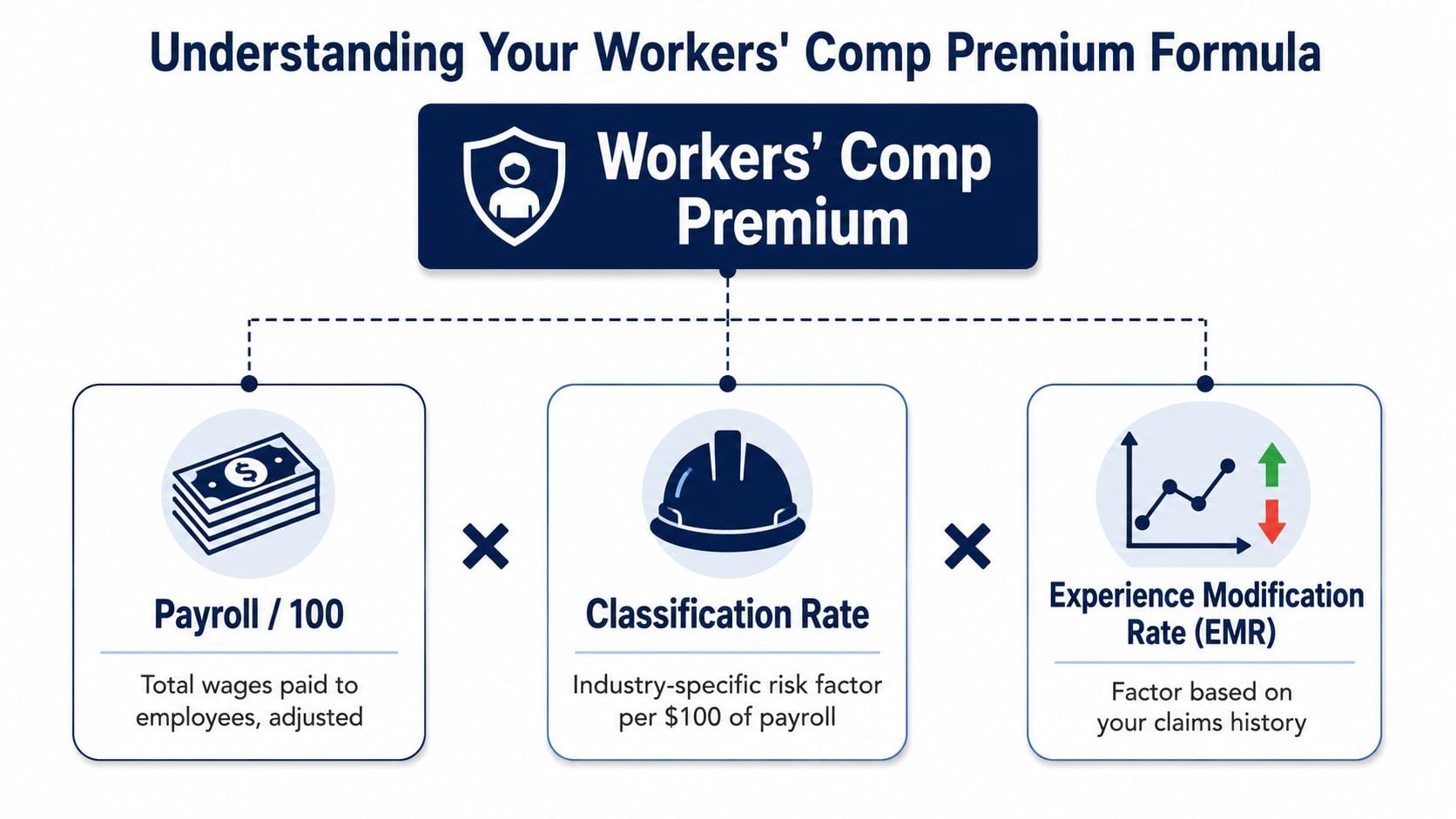

State guidance and industry summaries commonly use this formula for workers comp premium: classification rate × experience modification factor × payroll / 100, as explained in Georgia workers' compensation pricing guidance summarized by Insureon.

That formula is the backbone. A contractor doesn't need to memorize every rating manual, but the business owner does need to know what each part means.

Payroll

Workers comp is payroll-driven. As the crew grows, premium usually grows with it. That's one reason small contractors feel workers comp cost changes quickly when they move from solo operator to hired labor.

Classification rate

This is the risk price attached to the kind of work being done. Roofing, framing, electrical field work, and office admin don't belong in the same bucket. Higher-risk work carries a higher classification rate.

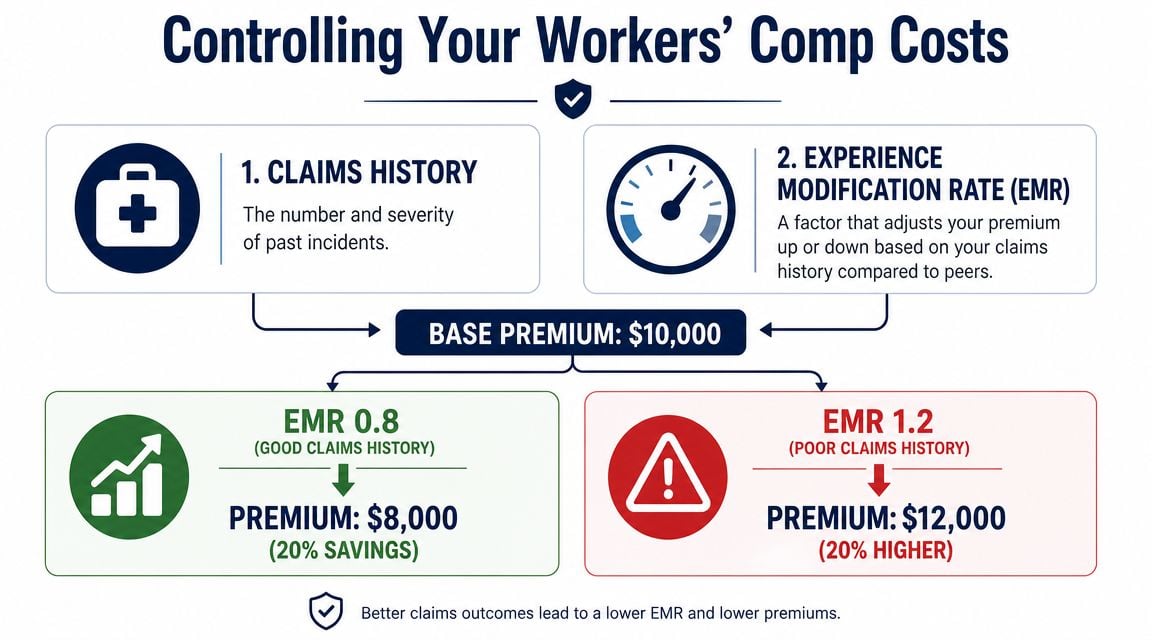

Experience modification factor

This is the factor tied to the business's claims history relative to the applicable rating system. If losses run poorly, the factor can make the same payroll cost more. If losses improve, the factor can help.

Where contractors overpay

The most common overpayment problem is bad payroll separation. A general contractor might have two field carpenters and one office manager. If all wages get dumped into a higher-risk field code, the business may pay more than it should.

Misclassification can also create trouble in the other direction. If field labor gets placed into a lower-risk code, the business may look cheaper at first, then get hit at audit with back premium.

A clean setup usually includes:

- Separate payroll records by role. Office staff, estimators, and field workers shouldn't be blended if the classifications differ.

- Clear job descriptions. Underwriters and auditors need to see who does what.

- Consistent time tracking. If a worker splits time between office and field duties, records have to support that split.

- Review before renewal. Don't wait for the audit surprise at the end of the policy term.

Contractors often focus on rate first. Classification accuracy usually matters just as much.

A contractor that wants to understand how claims history connects to that final multiplier can review this breakdown of workers comp experience modification. It helps connect premium math to day-to-day safety and claims decisions.

The Biggest Cost Drivers You Actually Control

A drywall contractor wins a school remodel, staffs up for the job, and then gets hit with a back strain claim halfway through the project. The medical piece is only part of the problem. The owner loses a productive installer, the foreman spends time on incident paperwork, and the claim follows the account into the next renewal. On a small crew, one injury can change insurance costs fast enough to show up in bid pricing.

Small contractors usually have more control over workers comp cost than they think. The biggest levers are claim frequency, claim handling, payroll discipline, and subcontractor paperwork. Owners often focus on rate because it is easy to compare. The expensive mistakes usually happen in the field and in the audit file.

What one claim does to a small construction business

A serious claim hits a five-person crew differently than it hits a company with three hundred employees. The loss can raise the experience mod, put pressure on cash flow, and make future jobs harder to price. If you bid public work or larger private jobs, that higher mod can also hurt your position with general contractors and project owners who review insurance numbers before award.

The operational drag is just as real.

An injured employee may need light duty, transportation to appointments, or a replacement worker who does not know your systems yet. The owner or office manager ends up handling adjuster calls, wage records, and return-to-work coordination while trying to keep jobs on schedule.

The cost drivers owners can actually fix

Some factors are set by state rules and class codes. Others come down to day-to-day management.

- Late reporting. A claim reported days late usually gets more expensive and harder to control.

- No modified duty plan. If an employee stays home longer than necessary because there is no restricted work available, indemnity costs tend to climb.

- Poor driver screening and vehicle rules. For plumbers, electricians, HVAC techs, and service contractors, fleet losses can become a repeating problem.

- Weak housekeeping and material handling practices. Slip, trip, strain, and lifting claims are common on smaller jobs where supervision gets stretched thin.

- 1099 subcontractor mistakes. If a sub has no valid workers comp coverage and someone gets hurt, the cost can come back to the hiring contractor.

- Messy payroll records. Bad time tracking creates audit disputes and makes it harder to defend how labor should be allocated.

One pattern shows up all the time in construction. The owner treats workers comp as something to shop once a year, but pricing gets set all year long by hiring decisions, training, supervision, and documentation.

A better approach is to run loss control the same way you run production. Set clear fleet rules. Investigate near misses. Get injury reports in the same day. Offer modified duty that is real and documented. Keep certificates and subcontract agreements organized before a job starts, not after a claim. Contractors that want a practical framework can review this loss control guidance for construction businesses.

Contractors that keep claims predictable and records clean usually have more room to compete on bids than contractors who only chase a lower quote at renewal.

Shopping for the Right Policy Not Just the Cheapest

A workers comp quote can look acceptable until the first contract review or claim. That's where the cheapest option often falls apart.

What to compare besides price

As a business grows from owner-only work to a mixed workforce, workers comp needs get more specific. Market-facing guidance summarized by Super Lawyers on what small business owners should know about workers' compensation notes that insurers now offer more flexible features such as waivers of subrogation and varied employer liability limits.

That matters in construction because general contractors, property managers, and project owners often care about paperwork details, not just whether a policy exists.

A solid quote review should include:

- Employer's liability limits. This helps with certain injury-related legal exposures that sit outside the core statutory benefit structure.

- Waiver of subrogation availability. Some contracts require it before work starts.

- Multi-state fit. A contractor working across state lines can't assume a basic setup covers every hiring and reporting issue.

- Claims handling reputation. Slow claims service creates friction with injured workers and with return-to-work plans.

- Certificate turnaround. If jobs depend on proof of insurance, delays can cost start dates.

An HVAC bidding example

An HVAC contractor adds two installers and starts bidding new construction work. Two quotes come in. One is cheaper, but it doesn't line up well with the contract package. The other costs more, but it fits the project's insurance requirements and is easier to use in the field.

That difference can decide whether the contractor gets on site without delays.

A fast review of bid paperwork should include the certificate request itself. This certificate of insurance template helps owners compare what the contract asks for against what the policy provides.

For contractors who want outside help reviewing options, Coverage Axis is one available option for workers compensation placements and coverage review for trade businesses. The useful part isn't brand name. It's having someone check whether the quote matches the crew size, state exposure, and contract terms instead of only chasing the lowest premium.

Actionable Ways to Lower Your Workers Comp Premiums

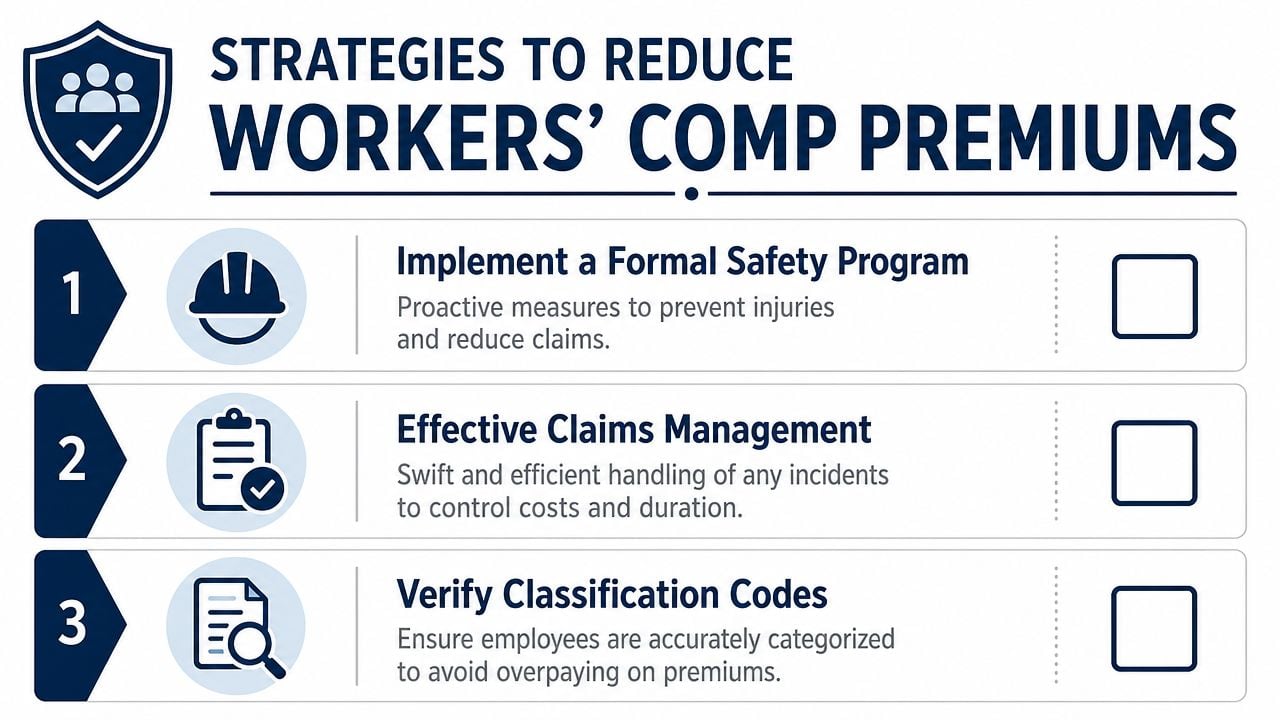

A small roofing crew can go a full year without a claim and still get hit with a higher audit bill because payroll was sloppy, certificates were missing, or a worker doing field labor got reported under the wrong class code. For trade contractors, premium control usually comes from fixing those preventable mistakes.

Build a safety routine that an underwriter can see

As noted earlier, smaller employers often do worse when safety lives only in the owner's head. On a jobsite, informal safety usually means rules change by foreman, new hires learn by watching others, and near misses never get documented. Carriers do not give much credit for that.

A better approach is simple and repeatable. A concrete or framing contractor does not need a thick binder that sits in the truck. The carrier wants to see habits that are used in the field and backed up by records.

- Weekly tailgate talks. Keep them tied to the work in front of the crew, such as trenching, ladders, saws, silica, lifting, or traffic flow.

- Consistent PPE enforcement. If one supervisor enforces eye protection and another ignores it, the rule does not hold.

- New-hire orientation. Short-term and seasonal workers are often involved in avoidable injuries because nobody slowed down to cover the basics.

- Immediate incident reporting. A cut hand or strained back can turn into a bigger claim when treatment gets delayed and facts get fuzzy.

Documentation matters.

Sign-in sheets, training notes, corrective actions, and photos of jobsite controls help during renewal conversations. They also help after a claim, when the carrier starts asking whether the business had any real safety process in place before the injury happened.

Tighten claims handling and audit prep

The next savings usually come from what happens after someone gets hurt. A light-duty plan can keep an employee working in some capacity, whether that means shop cleanup, tool tracking, material deliveries, permit runs, or warehouse support. For a small crew, that matters twice. It can reduce claim duration, and it keeps one injury from turning into a staffing problem on every active job.

Audit prep is less exciting, but it has a direct effect on premium. I have seen contractors pay more because the books could not clearly separate office payroll from field payroll, or because a “helper” spent half the year doing installation work that was never reflected in the records.

| Action | Why it lowers waste |

|---|---|

| Keep payroll records current | Reduces audit disputes and surprise premium charges |

| Separate office and field duties clearly | Helps prevent higher-rated field codes from being applied too broadly |

| Review subcontractor certificates before work starts | Cuts down on uninsured-sub exposure showing up at audit |

| Match job descriptions to actual tasks | Supports the class code the carrier is using |

Subcontractor paperwork deserves special attention. If a 1099 drywall crew shows up without valid workers comp coverage, the auditor may treat that labor as your exposure. That can raise premium fast, especially if the labor falls into a higher-rated trade code.

A contractor does not need a complicated safety manual first. The business needs a routine the crew follows and records that hold up during a claim review or payroll audit.

These steps will not change the base risk of roofing, concrete, framing, or electrical work. They do cut down on the avoidable problems that push premiums higher, especially for small contractors who cannot absorb a bad claim, a bad audit, and a weaker EMR in the same year.

Protecting Your Crew and Your Business

Workers comp is part of how a trade business becomes stable. It protects the crew after an injury, protects the owner from a much larger financial hit, and helps the company qualify for work that better clients won't award without proof of coverage.

The hard parts are usually the practical ones. Figuring out who counts as an employee. Keeping classifications clean. Managing audits. Preventing claims that can follow the business into future renewals and bids. Contractors who handle those issues early usually have more room to grow and fewer ugly surprises.

If a small crew is hiring, bidding larger work, using subcontractors, or unsure whether the current setup would hold up after an injury or audit, it's worth getting a fresh review. Coverage Axis offers free workers comp quotes and coverage reviews for contractors who need a policy structure that matches their trade, payroll, and job mix.