A general contractor signs a familiar framing crew, gets them started, and keeps the job moving. By midweek, one of the crew members falls and gets hurt. The next question isn't about schedule. It's about whose workers comp policy is going to respond, whether anyone had valid coverage, and whether that injury is about to land on the general contractor's desk.

That's why workers comp for subcontractors isn't a paperwork issue. It's a job cost issue, an audit issue, and in some cases a survival issue for the company that hired the sub. A signed subcontract, a 1099, or a verbal assurance that “they've got their own insurance” won't fix the problem after an injury.

For busy contractors, the question is simple. If a subcontractor gets hurt, or one of their workers gets hurt, does that risk stay with them, or does it roll uphill and hit the hiring contractor's policy, premiums, and profit?

Table of Contents

- The Million-Dollar Question on Your Jobsite

- Who Is Actually Responsible for an Injured Sub

- Is Your Subcontractor a True Business or a Disguised Employee

- How State Laws Change Your Workers Comp Obligations

- Mastering the Paper Trail COIs and Contracts

- How Uninsured Subs Secretly Inflate Your Premiums

- Stop Guessing and Start Controlling Your Risk

The Million-Dollar Question on Your Jobsite

A lot of subcontractor problems start with a crew that's already trusted. The framing contractor has worked with the GC before. They show up on time, move fast, and don't create drama. Nobody wants to slow down a good job over insurance paperwork when trusses are arriving and inspections are coming.

Then someone gets hurt.

On a residential build, that might be a framer falling from a second-floor deck edge. On a commercial tenant buildout, it could be an electrician taking a bad ladder fall while pulling branch circuits. The injury happens in seconds, but the fallout can drag on through claims handling, premium audits, and legal fights over who was responsible for that worker.

A subcontractor that looks independent on paper can still become the hiring contractor's problem if the actual jobsite relationship says otherwise.

That's the part many successful contractors learn the hard way. Workers comp for subcontractors isn't just about whether the sub checked a box on a bid package. It's about whether the sub had valid coverage, whether the worker was really an independent contractor, and whether state law treats the hiring contractor as the backup payer when things go wrong.

A drywall example makes the point. A GC hires a small drywall crew for a fast apartment turnover. The crew leader says he's self-employed and bills on a 1099. He uses laborers he brought in himself. If one of those laborers gets injured and the drywall crew doesn't carry proper coverage, the GC may discover that the insurance exposure never left the project. It sat there, hidden, until the loss happened.

The expensive question on every jobsite is the same. If this injury claim doesn't stay with the subcontractor, what does it do to the contractor who hired them?

Who Is Actually Responsible for an Injured Sub

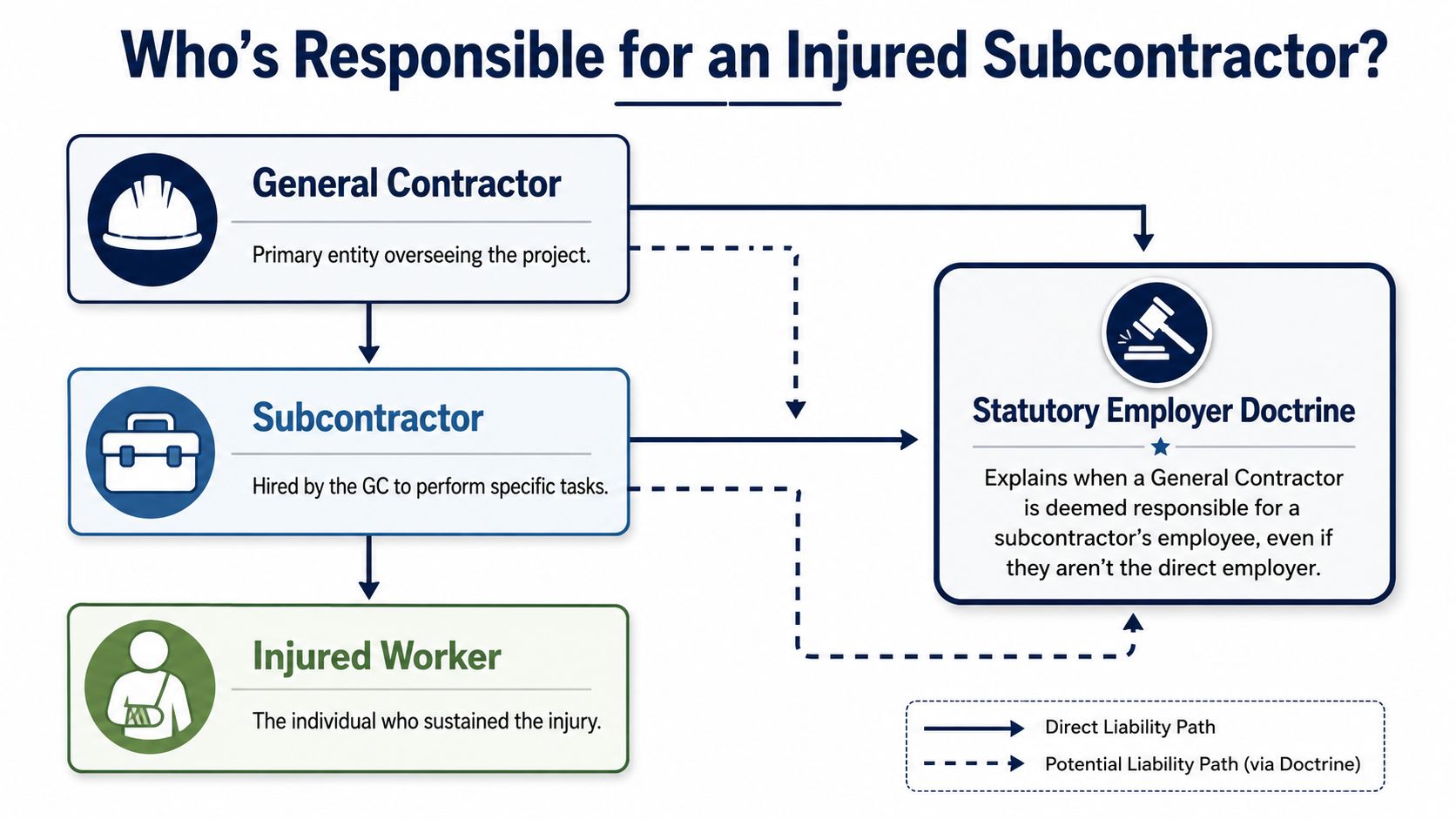

A general contractor often acts as the project's insurance safety net, whether that was the intent or not. If a subcontractor has employees and fails to carry workers comp when required, state law can push responsibility uphill to the contractor above them. That's why this issue matters even when the GC never hired the injured person directly.

A visual helps clarify how that liability can travel through a project:

Why risk often flows uphill

In plain language, a statutory employer rule means the law may treat the hiring contractor as responsible even when the injured worker technically belongs to someone else. Contractors see this most often in construction because so much of the work is performed through layers of subs.

A large homebuilder provides a good example. The builder hires an “independent” electrician for rough-in work on several homes. The electrician gets hurt on site. If the electrician doesn't have proper workers comp, or if the relationship doesn't meet the legal standard for true independence, the builder may still end up exposed.

That's one reason contractor insurance requirements need to be handled before a job starts, not after an injury. A written vetting process, clear subcontract terms, and project-specific documentation do more to protect the GC than a handshake ever will. This becomes even clearer when reviewing general contractor insurance requirements as part of job setup.

For injured workers trying to understand rights when an “independent contractor” relationship is disputed, practical legal guidance like independent contractor work injury help can also be useful. The reason that matters to a GC is simple. Those same disputes often become the path by which liability gets redirected back up the chain.

The one-person subcontractor problem

The trickiest file is often the one-person subcontractor with no employees. Many contractors assume that if there's only one person and no crew, there's no workers comp issue. That assumption can be costly.

According to Insureon's discussion of subcontractor workers comp exposure, a key issue is who pays when a one-person subcontractor is uninsured. They can often opt out of buying workers comp, but an injury on the jobsite can still expose them to major personal medical costs and may still create liability for the hiring contractor if the worker is later treated as misclassified or if state law wasn't followed closely.

A tile subcontractor is a good example. If that tile setter works only for one GC, uses materials and equipment controlled by that GC, follows the GC's daily direction, and gets paid in a way that looks more like wages than a business invoice, the file can stop looking like “independent subcontractor” and start looking like “disguised employee.”

Practical rule: If the subcontractor's coverage status is unclear, the GC should assume the risk hasn't been transferred yet.

That's the operating mindset that keeps claims from turning into uninsured losses.

Is Your Subcontractor a True Business or a Disguised Employee

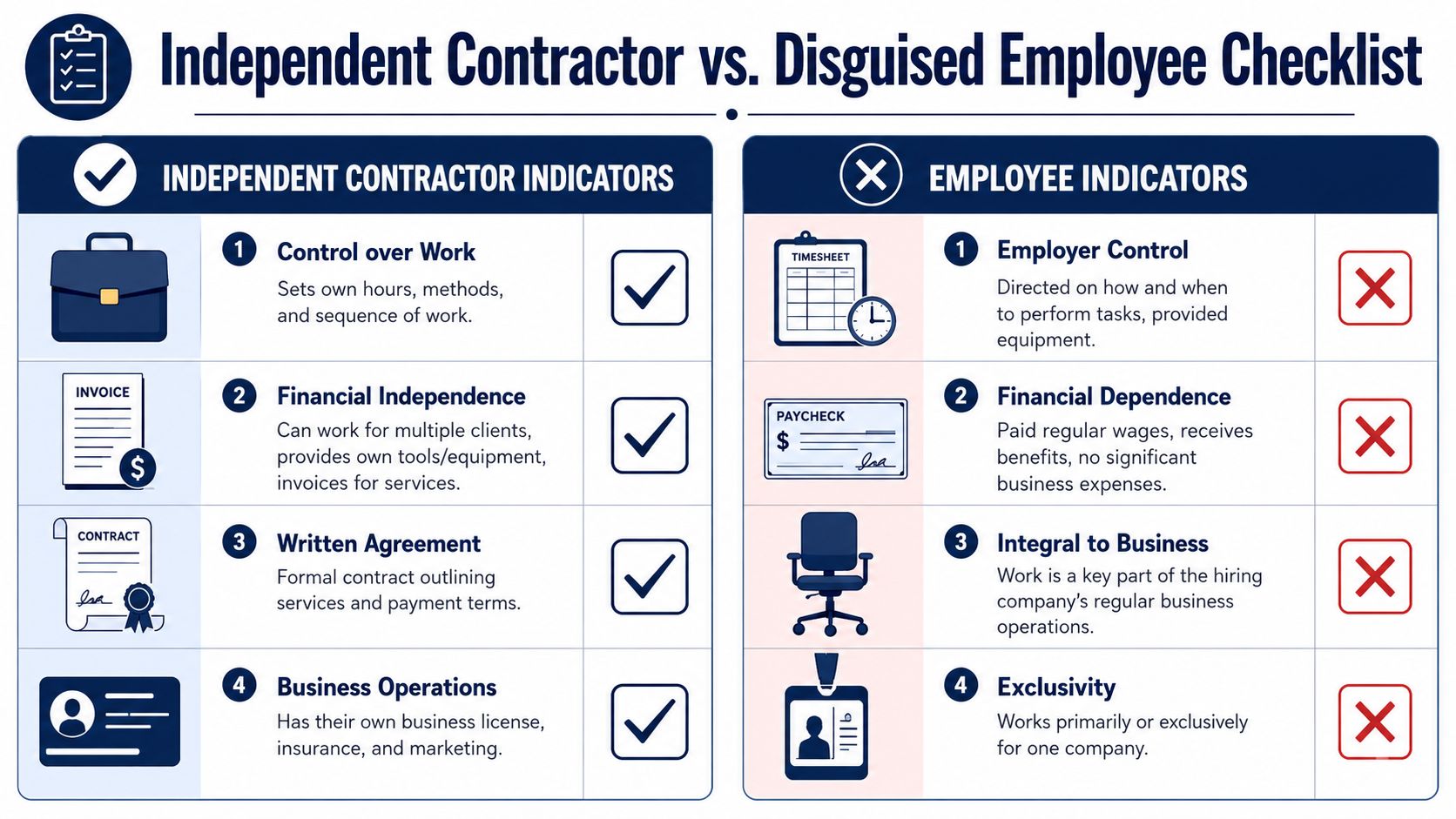

Most disputes over workers comp for subcontractors don't start with the injury itself. They start with the relationship that existed before the injury. If the subcontractor isn't running a real business, regulators, insurers, and auditors may look past the paperwork and treat the worker as an employee.

That problem is widespread in construction. The Economic Policy Institute states that 12.4% to 20.5% of U.S. construction workers are misclassified as independent contractors or work off the books, and it also notes that Wisconsin uses a nine-part statutory test to evaluate status in this area through factors such as control and investment in the work (Economic Policy Institute on independent contractor status).

The classification checklist below captures the practical divide contractors should be watching for on every job:

What regulators look at

A real subcontractor usually looks like a separate business. They bid jobs, invoice for completed work, bring their own tools, carry their own insurance, and can work for other clients. They have some control over how the work gets done, even if the GC controls the schedule and final product.

A disguised employee usually looks different:

- Control sits with the hiring contractor: The GC tells the worker when to show up, how to do the work, and who supervises each task.

- Tools and equipment come from the hiring contractor: The more the worker relies on the contractor's ladders, lifts, tools, and materials, the weaker the independent business argument gets.

- Payment resembles payroll: Hourly pay, regular draws, and no meaningful job-based invoicing raise questions.

- The worker is economically tied to one company: If the same crew works only for one roofer or one remodeler, year-round, that relationship won't look very independent.

For contractors that want a non-legal plain-English reference on this issue, proper worker classification for SMBs is a useful overview. It doesn't replace state-specific advice, but it helps owners spot relationships that need a harder look.

A roofing example that raises red flags

A roofing contractor says every installer is a subcontractor. On paper, each crew leader signs an agreement. In practice, the company sets the work hours, assigns each house, supplies dumpsters and materials, requires branded shirts, pays by the hour, and uses the same crews on nearly every project.

That arrangement creates obvious classification risk.

The issue isn't whether the contractor intended to do anything wrong. The issue is whether the facts support an independent business relationship. If they don't, the “subcontractor” label won't hold up well in a claim or audit.

A contractor trying to clean this up should look beyond insurance certificates. The better starting point is the full package: licensing, contract language, business entity documents, invoices, tax treatment, and how the relationship works in the field. For companies tightening their compliance process, it often makes sense to review both classification and bonding requirements together, especially when preparing for larger jobs that require a more formal risk file, such as those discussed in how to get bonded and insured.

If the crew looks, acts, and gets managed like employees, a certificate alone won't fix the classification problem.

How State Laws Change Your Workers Comp Obligations

A contractor can run the same trade, use the same subcontract structure, and still face very different workers comp obligations depending on the state. That's where many expanding businesses get into trouble. They build one internal rule and assume it travels cleanly across state lines.

It doesn't.

A commercial painting contractor with crews in both New York and Virginia is a good example. In one state, the fight may center on whether a construction worker can be treated as an independent contractor at all. In another, the issue may be whether subcontractor headcount pulls the contractor into a workers comp requirement even when those subs already carry their own policies.

New York and Virginia are not playing by the same rules

New York is strict. The Workers' Compensation Board says that a person working for an employer in the construction industry is only an independent contractor if they meet a two-part test, and the state's Construction Industry Fair Play Act says workers are presumed to be employees unless they satisfy all three statutory requirements. The state's guidance also expressly says the law covers employees, contractors, and subcontractors, which is why relying only on a subcontract or 1099 is risky in New York construction (New York Workers' Compensation Board guidance on identifying an independent contractor).

Virginia comes at the problem differently. There, a contractor can be pulled into a coverage requirement based on a statutory employee count. Virginia explains that if a contractor has one direct employee and hires two subcontractors who each have one employee, that creates three statutory employees and triggers the need for coverage. The state also says subcontractor employees performing the same trade or helping fulfill the contract are counted, and the contractor should collect proof of coverage so premium isn't charged for covered subcontractors (Virginia contractor information on workers comp).

A contractor working in multiple states can't use one blanket assumption about subcontractors and stay protected.

Florida adds another variation. In Florida construction, each subcontractor is responsible for workers comp for its own workers, but the primary contractor is still responsible for verifying that coverage exists. If the subcontractor is uninsured, the contractor can become responsible for benefits. Florida's guidance recommends obtaining either a proof-of-coverage database printout or a certificate of liability insurance plus carrier or producer confirmation before work starts (Florida workers compensation employer FAQ).

Subcontractor WC responsibility state law snapshot

| State | General Contractor's Responsibility | Key Compliance Action |

|---|---|---|

| New York | Construction workers are presumed to be employees unless strict tests are met | Review the actual working relationship, not just the contract or tax form |

| Virginia | Subcontractor workers can count toward statutory employee totals that trigger coverage | Count everyone tied to the trade or contract and collect proof of coverage |

| Florida | Primary contractor must verify subcontractor coverage and may be liable if the sub is uninsured | Confirm coverage before work starts through a proof-of-coverage check or verified COI |

A painting contractor working in Buffalo and Richmond can't hand the same onboarding packet to both crews and assume that's enough. In New York, the core concern may be whether the worker can lawfully be treated as independent. In Virginia, the business has to track who counts toward the statutory employee threshold and keep proof that covered subcontractors already carry their own policies.

That's why workers comp for subcontractors is a state-law issue first and an administrative issue second.

Mastering the Paper Trail COIs and Contracts

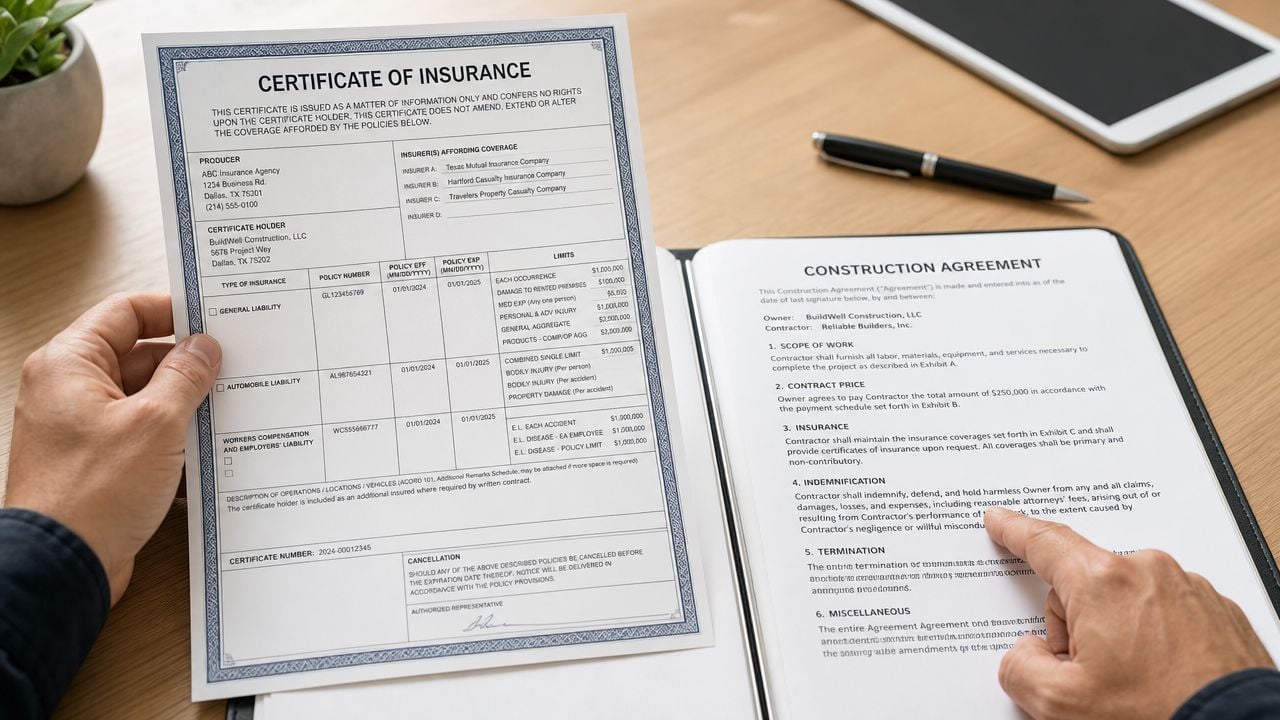

A lot of contractors think collecting a COI means the file is done. It isn't. A certificate of insurance is useful, but it's only one piece of the protection package. If the certificate is outdated, incomplete, or inconsistent with the subcontract, it may create false confidence instead of real protection.

An HVAC contractor bringing a plumbing sub onto a commercial project should treat the paperwork review like pre-task planning. The goal is to verify that the risk was transferred the way everyone thinks it was, before the first worker unloads tools.

What to verify before work starts

Florida's approach is a good model for discipline even outside Florida. As noted earlier, the state says the primary contractor is responsible for verifying a subcontractor's coverage and can be responsible for benefits if the sub is uninsured. Its guidance recommends a proof-of-coverage printout or a COI plus confirmation with the carrier or producer before work begins. That makes certificate tracking a control point, not a clerical task.

A contractor should check at least these items:

- Named insured accuracy: The business name on the certificate should match the subcontractor entity signing the contract.

- Policy dates: Coverage has to be active for the period the sub will be on the job.

- Workers comp listed: If workers comp is required for that subcontractor under the law or contract, it should appear clearly.

- General liability shown separately: A sub can have GL and still lack workers comp. One doesn't prove the other.

- Confirmation process: If anything looks off, verify it before work starts, not after a loss.

For contractors building a standard document package, a working reference like this certificate of insurance template can help teams understand what fields should be reviewed every time.

What a contract should actually do

The subcontract should do more than say “subcontractor will maintain insurance.” It should assign responsibility clearly enough that operations staff, accounting, and project managers can all follow the same process.

A workable subcontract usually addresses:

- Insurance obligations: What policies the sub must carry and when proof is due.

- Endorsement requirements: Whether the GC must be added as an additional insured on GL and whether a waiver of subrogation is required where applicable.

- Indemnity language: Who takes responsibility when their work, workers, or operations create the loss.

- Stop-work authority: The GC should have the right to halt work if coverage lapses or documentation isn't provided.

A plumbing example shows why this matters. A plumbing subcontractor sends a COI showing general liability but no workers comp because the owner says there are “no employees.” On paper, that might be true. In the field, the owner shows up with two helpers every week. If the contract doesn't require updated proof and the GC doesn't reconcile the paperwork with reality, the file is already drifting toward a claim problem and an audit problem.

The safest document is the one that matches how the subcontractor actually operates on the jobsite.

For growing contractors, this is also one area where using a licensed advisor to standardize review can help. Coverage Axis, for example, handles contractor insurance placements and COI review as part of broader commercial insurance support, but the key point isn't the vendor. The key point is that someone needs to own the process with enough authority to stop noncompliant subs before they start work.

How Uninsured Subs Secretly Inflate Your Premiums

Most contractors understand that an uninsured subcontractor can cause a claim problem. Fewer connect that risk to what happens after the claim. That's where profit gets squeezed.

The first hit is obvious. If an injury claim lands on the hiring contractor's workers comp policy, the contractor may deal with claim activity that never should have touched its account in the first place. The second hit is slower and often more frustrating. The file can affect future pricing and underwriting, especially when loss history no longer reflects only the contractor's own direct workforce.

Claims are only part of the damage

A landscaping contractor that hires mowing crews as 1099 subs may believe those crews are outside its workers comp exposure. Then one uninsured crew member gets hurt trimming along a roadside. If the claim is pushed back toward the hiring contractor, the business may not just face the immediate disruption. It may also see the downstream effect on future insurance costs.

That's one reason many contractors watch their experience modification so closely. When claims hit the wrong policy, they don't stay in the past. They can follow the business into renewal discussions, bid competitiveness, and hiring decisions. Contractors trying to understand that relationship in plain terms can review how a workers comp experience modification affects long-term cost.

Audit surprises hit after the job is done

The other painful moment comes at audit.

If a contractor paid uninsured or poorly documented subcontractors during the policy period, the auditor may ask for proof that those subs carried their own workers comp. If the proof isn't there, the carrier may treat those payments as part of the contractor's exposure base. That can generate a large additional premium bill after the revenue from the job has already been spent.

A concrete example helps. A landscaping company uses several uninsured mowing crews over a season and keeps only invoices, not valid certificates or coverage proof. At audit, those payments are questioned. The owner thought the labor cost was closed months ago. Instead, it comes back as insurance cost.

Uninsured subcontractor exposure often shows up twice. Once in a claim file, and again in the audit.

That's why workers comp for subcontractors belongs in the estimating process, the onboarding process, and the accounting process. It isn't just a field issue and it isn't just an insurance issue. It's margin protection.

Stop Guessing and Start Controlling Your Risk

Contractors don't need more theory. They need a repeatable process that keeps uninsured subcontractor exposure from slipping into live jobs.

That process is straightforward when it's enforced:

- Use a written subcontract every time: Terms should match the actual working relationship.

- Collect and review coverage proof before mobilization: Don't treat certificates as a box-checking exercise.

- Check classification, not just insurance: A worker who looks like an employee can still create workers comp exposure even with a signed independent contractor agreement.

- Follow the state rule where the work happens: New York, Virginia, and Florida show how different the obligations can be.

- Require the right endorsements where appropriate: Protection often depends on more than the face of the COI.

When contractors tighten these controls, they reduce claim surprises, audit disputes, and preventable premium increases. They also put themselves in a stronger position when owners, upstream contractors, and lenders ask for cleaner risk management documentation. A practical part of that review is confirming when an additional insured endorsement belongs in the subcontractor package and when it doesn't solve the workers comp issue by itself.

Coverage Axis helps contractors review workers comp, subcontractor documentation, and overall insurance structure in plain English. If a company wants a free quote or a coverage review for its subcontractor insurance requirements, Coverage Axis can review the current program and flag gaps before they turn into claims or audit costs.