A contractor opens a bid package, flips to the insurance requirements, and sees a line that says $1,000,000 employers liability. The crew is already lined up. The pricing is tight but workable. The confusion starts when that requirement sits next to workers compensation, because many contractors assume workers comp already handles any employee injury.

That assumption causes trouble.

For a plumbing contractor, electrician, roofer, or concrete crew, workers comp is only part of the answer. It pays statutory benefits after a work injury. It doesn't always protect the business when that same injury turns into a lawsuit, a third-party claim, or a contract dispute over who should pay. That gap is where employers liability insurance matters, and it matters most when a job goes bad in a way that spreads blame across multiple parties.

Table of Contents

- That Line Item Your Workers Comp Policy Might Not Cover

- What Employers Liability Insurance Actually Protects

- Workers Comp vs Employers Liability A Side-by-Side Look

- Real Lawsuits Where This Coverage Saves a Business

- State Rules and Contract Requirements You Must Know

- Your Checklist for Buying the Right EL Coverage

- Get Covered Before the Next Lawsuit Hits

That Line Item Your Workers Comp Policy Might Not Cover

An electrical contractor bidding a school retrofit often sees the same pattern. The project spec asks for general liability, auto, umbrella, workers comp, and then a separate employers liability requirement. The owner reads it twice and thinks the same thing many trade businesses think. Isn't that already inside the workers comp policy?

Sometimes yes. Sometimes not in the way the contract expects.

A standard workers comp placement often includes employers liability as part of the package. But the practical problem isn't just whether it exists. The problem is whether the limit is high enough, whether the state setup allows it, and whether the certificate matches what the general contractor's risk team wants to see. A plumbing contractor can have a valid workers comp policy and still fail a contract review because the employers liability piece is missing, too low, or structured wrong for the states where the crew is working.

For contractors trying to find workers' compensation coverage, it's worth looking beyond payroll and class codes and asking how the liability piece is attached. That question gets missed all the time when the focus stays only on getting a certificate out fast.

Why the confusion shows up on jobsites

Workers comp feels complete because it handles the first wave of a loss. An employee gets hurt carrying cast iron, falls off staging, or suffers a hand injury using a power threader. Medical treatment starts. Wage benefits may start. The claim moves.

Then the second wave hits if someone alleges negligence, defective maintenance, improper training, or another legal theory outside the basic benefit system. That is where the owner's attention shifts from the injury itself to legal exposure.

Practical rule: Workers comp pays the injured employee's statutory benefits. Employers liability insurance steps in when the injury starts producing lawsuits around the claim.

Contracts can also pull this issue into the open. A prime contract may require a certain employers liability limit because the upstream party knows employee injury claims don't always stay inside workers comp. If contractual risk transfer is part of the job, it helps to understand related obligations like contractual liability language in construction agreements, because insurance and contract wording often collide after a serious incident.

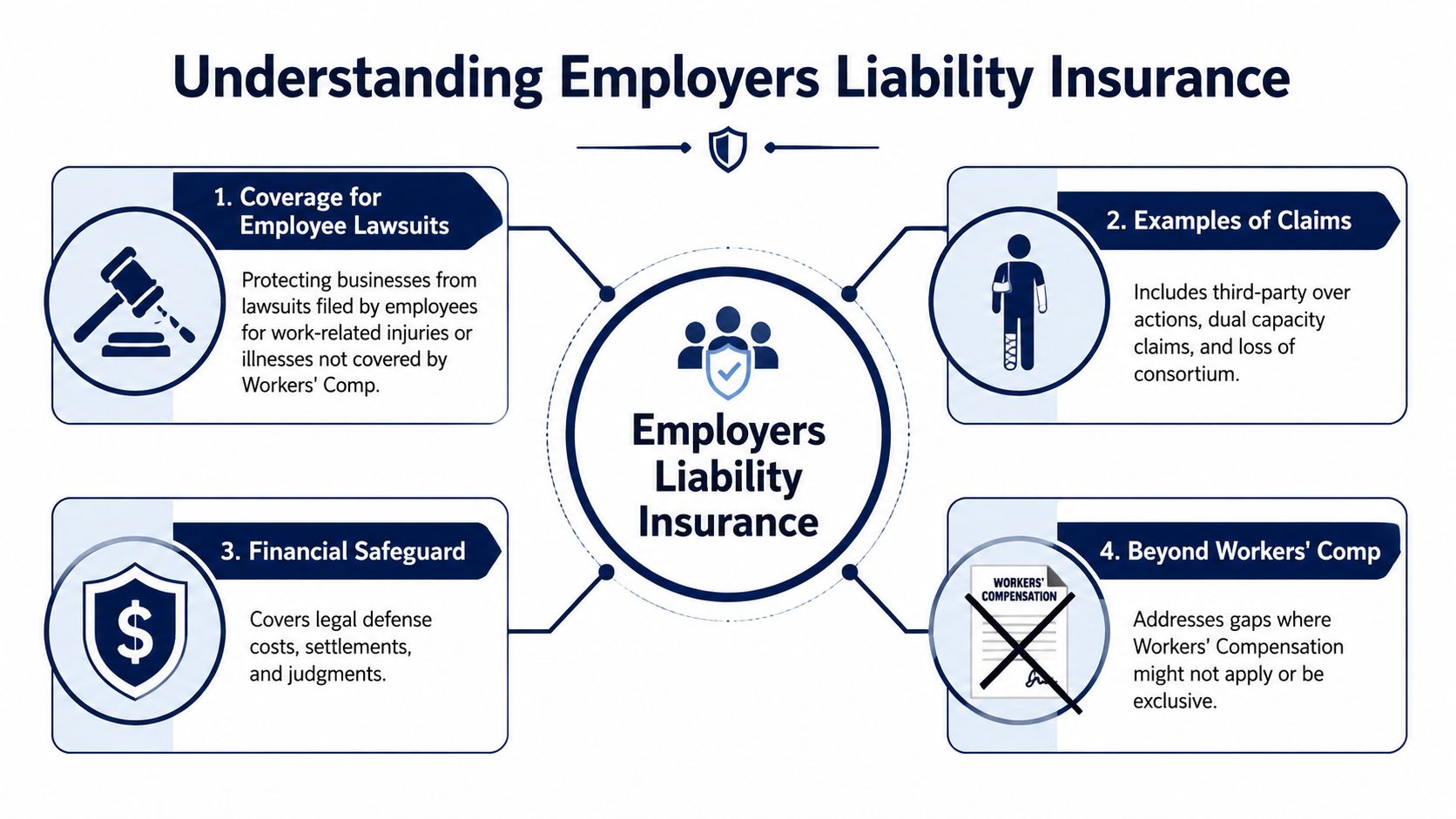

What Employers Liability Insurance Actually Protects

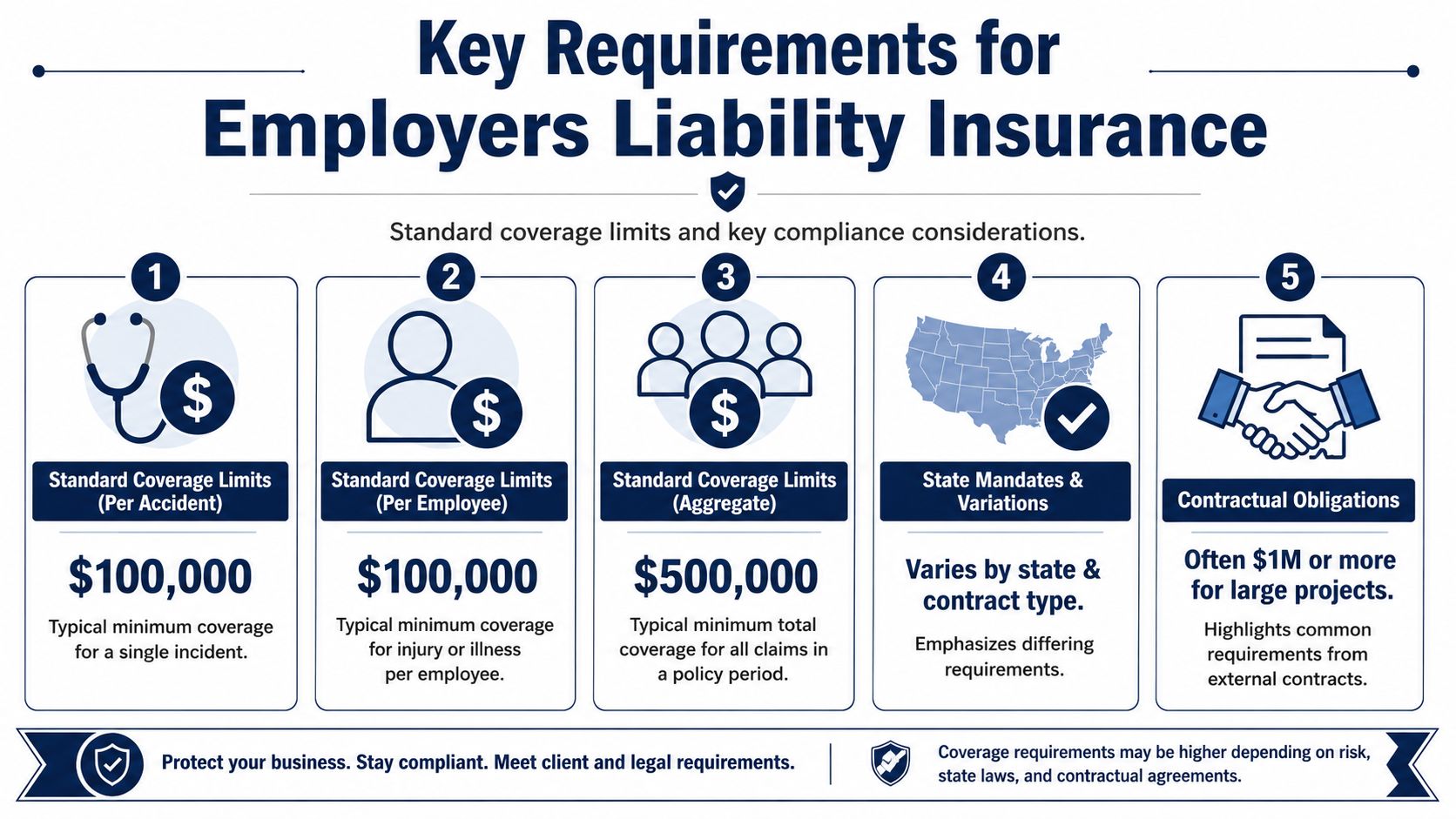

Employers liability insurance protects the business when an employee's work-related injury or illness leads to a lawsuit outside the workers compensation system. Historically, employers liability became Part Two of the workers comp policy to fill the gap between statutory benefits and civil liability exposure, and the standard structure commonly carries $500,000 per accident, $500,000 per disease, and a $1,000,000 lifetime maximum for disease claims according to the workers compensation and employers liability coverage outline.

That structure matters because those limits set the ceiling for defense costs, settlements, and judgments when an employee sues outside the no-fault system.

Where the lawsuit risk starts

Workers comp is built on an exclusive remedy idea. In plain language, the employee usually gets defined benefits without having to prove the employer was at fault, and in return the employer is generally shielded from direct injury lawsuits.

But construction losses don't always stay that clean.

A welder can get burned using equipment the employer allegedly failed to maintain. A sheet metal worker can get injured at a site controlled by another party, which leads that party to bring the employer back into the case. A spouse can file a related claim after a catastrophic injury changes the household.

Those aren't wage replacement issues. Those are liability issues.

What the policy is built to pay

Think of it this way. Workers comp pays the hospital and statutory benefits. Employers liability insurance pays the legal bill when someone says the employer's actions helped cause the injury and the dispute leaves the workers comp lane.

That usually means the policy is there for things like:

- Defense costs: Hiring counsel, responding to the lawsuit, and managing litigation.

- Settlements: Resolving covered claims before trial if that makes financial sense.

- Judgments: Paying covered court-awarded amounts up to the policy limit.

A plumbing example makes this easier to see. A service plumber sends a technician into a commercial mechanical room. The technician is injured while using a company-supplied piece of equipment that had a known maintenance problem. Workers comp may address the injury benefits. If the facts lead to allegations that the employer's negligence contributed to the injury in a way that supports a lawsuit, employers liability insurance is the backstop.

When a work injury turns into a blame case, the cost driver often shifts from treatment to legal defense.

This also helps separate employers liability from other legal risks. A bodily injury lawsuit tied to a workplace injury isn't the same thing as wage and hour exposure, officer exposure, or labor code issues. Business owners dealing with management-side exposure sometimes also review how personal liability for labor law infractions can arise, but that is a different category of claim and not a substitute for employers liability insurance.

Workers Comp vs Employers Liability A Side-by-Side Look

The fastest way to clear up confusion is to put both coverages next to each other. They travel together on many policies, but they do different jobs.

A small HVAC contractor adding new installers should understand both before signing a subcontract or handing over a certificate. For businesses still sorting out the basics, this guide to workers comp for small business helps frame where Part One ends and the liability side begins.

| Coverage Aspect | Workers' Compensation (Part One) | Employers' Liability (Part Two) |

|---|---|---|

| Primary purpose | Pays statutory benefits for a work injury or occupational illness | Protects the employer when a covered lawsuit arises from that injury or illness |

| How a claim starts | Employee suffers a job-related injury or illness | A lawsuit or legal allegation is made outside the basic workers comp remedy |

| Fault standard | No-fault system in most situations | Liability allegations usually involve negligence or another theory against the employer |

| What it usually pays | Medical care, wage-related benefits, and other statutory benefits | Defense costs, settlements, and judgments for covered suits |

| Who is being helped first | The injured employee | The employer facing legal exposure |

| Where contractors get tripped up | Assuming this solves every employee injury issue | Assuming this is optional because the injury was already reported to workers comp |

| Trade example | An electrician strains a back lifting conduit and receives benefits | The same injury later leads to allegations about unsafe lifting practices or faulty supervision |

Bottom line: These aren't duplicate coverages. One addresses employee benefits. The other addresses employer liability.

Real Lawsuits Where This Coverage Saves a Business

The danger becomes real when the injury doesn't stay between the employee and the workers comp carrier. On a jobsite, one accident can pull in the owner, the GC, the subcontractor, the equipment supplier, and the employer.

That chain reaction is why employers liability insurance matters to trade businesses with crews in the field.

A roofer gets pulled back into the claim

A roofing employee falls on a commercial reroof project and gets workers comp benefits. The employee then sues the general contractor, alleging unsafe site conditions. The GC responds by filing a third-party action against the roofing company, arguing the roofer's employer failed to train, supervise, or protect the worker properly.

Now the roofing contractor is back in the fight.

This is the kind of claim owners don't expect when they say, "The worker already got comp." Yes, the worker did. But the lawsuit moved sideways through another party and came back at the employer through a different door. That is a classic situation where employers liability coverage can be the difference between having a defense and funding one out of company cash.

Contractors also run into this problem when upstream parties ask for broad risk transfer. That is why endorsements and contract review matter alongside issues like additional insured status in construction agreements.

An excavation contractor faces a dual role allegation

An excavation company modifies a trench-support component in-house for a field fix. An employee is later injured while using that setup. The employee's claim doesn't stay limited to the employment relationship. The legal theory becomes, in effect, "You weren't only the employer. You also supplied or altered the thing that caused the harm."

That is the practical meaning of a dual-capacity style allegation.

For excavation, concrete, and utility contractors, this risk appears whenever the business repairs, adapts, fabricates, or repurposes equipment and tools for field use. The operation may think it's solving a jobsite problem fast. Later, plaintiff counsel may describe the same facts as a second role that carries separate liability.

A plumbing accident reaches the family

A plumbing contractor sends a foreman and helper into a renovation with active overhead work and tight access. A severe incident occurs. The injured employee's spouse later brings a related claim tied to the fallout from the injury itself.

That kind of case surprises owners because the person suing isn't the employee. But serious accidents often affect more than the worker. The legal exposure can spread to the household and widen the financial stakes.

A catastrophic claim rarely stays neat. Once multiple people and multiple legal theories enter the file, defense costs start climbing long before anyone talks settlement.

The financial side shouldn't be underestimated. Loss data from Ireland's National Claims Information Database showed that in the first half of 2023, the total cost of settled employers' liability and public liability claims was 21% higher than in the second half of 2022, which is one reason liability severity remains a serious concern for employers with jobsite exposure, according to the mid-year 2023 claims database report.

For contractors, the lesson is simple. Frequency isn't the only problem. A single severe claim can become expensive because of who gets pulled into it and how long the legal fight lasts.

State Rules and Contract Requirements You Must Know

A certificate of insurance can look fine at a glance and still hide a problem. That happens when the employers liability line shows a limit, but the policy setup doesn't match the states where the crew is working or the contract terms attached to the project.

For a framing contractor opening a branch in another state, generic advice no longer helps.

What the certificate is really showing

When a general contractor asks for employers liability on a certificate, the request usually isn't random. That line tells the upstream party that if an employee injury develops into employer liability litigation, there is a stated limit available for that part of the risk.

The number matters operationally because a legal department or contract administrator may reject the certificate if the employers liability limits don't match the subcontract. Owners often focus on general liability and umbrella because those are more familiar. Meanwhile, the employers liability line becomes the reason payroll can't start on site.

A similar compliance issue shows up in transportation-adjacent operations. Contractors with trucks, hauling activity, or regulated fleet work also have to line up insurance with operating requirements, which is why some review resources on active operating authority insurance when fleet obligations overlap with contracting operations.

Why monopolistic states change the buying decision

This is the nuance many generic explainers miss.

In North Dakota, Ohio, Washington, and Wyoming, employers must buy workers compensation from the state fund, and those state-run policies may not include employers liability protection. That can create a gap that requires separate stop-gap coverage, as outlined in IRMI's explanation of employers liability coverage in monopolistic states.

That matters most for contractors that:

- Travel crews across state lines: A drywall or mechanical contractor may be based in one state and pick up work in another without rethinking how the workers comp and employers liability structure changes.

- Use temporary project offices: A business can create state-specific exposure faster than the owner expects.

- Run mixed payroll in different jurisdictions: One policy assumption doesn't always travel cleanly.

Contractors shouldn't ask only, "Do we have employers liability?" They should ask, "Is our employers liability structure valid for every state where our people are working?"

A subcontractor bidding jobs in monopolistic states needs to verify whether the state fund arrangement leaves a hole and whether a stop-gap policy needs to sit beside it. That is especially important for trades that move fast between projects, such as electrical, plumbing, roofing, concrete, and restoration. For businesses hiring trade partners, this overview of workers comp for subcontractors is also useful when reviewing downstream compliance.

Your Checklist for Buying the Right EL Coverage

Buying employers liability insurance shouldn't be a box-checking exercise. For contractors, the right decision comes from matching the policy to the job mix, state footprint, and contract demands.

Use this checklist before renewal or before signing a new project.

Start with the state setup: Confirm whether the business operates only in standard workers comp states or also enters monopolistic states. If crews cross borders for jobs, that question needs a clear answer before work starts.

Read the contract insurance section carefully: Look for required employers liability limits, manuscript wording, and any project-specific insurance exhibits. A subcontract can create a problem even when the policy looked acceptable at the last renewal.

Map the actual injury path: Think through how an employee injury could widen into a lawsuit. A plumbing contractor working in occupied buildings has different exposure than a paving crew working in open roadway zones.

Review what drives premium and placement: Payroll, class codes, job duties, and claims history all affect pricing and carrier appetite. If the payroll estimate is wrong or the classifications are sloppy, the quote may look good and still be built on bad assumptions.

Check how certificates will be issued: If a GC needs proof fast, make sure the policy can be shown correctly on a certificate. Contractors that regularly issue project paperwork often keep a sample certificate of insurance template handy so they know what information owners and upstream parties will look for.

One strong habit helps more than most. Review employers liability insurance at the same time as workers comp, not after the contract gets kicked back.

Get Covered Before the Next Lawsuit Hits

A contractor can do a lot right and still get blindsided after a serious employee injury. The claim starts in workers comp. Then another party gets sued, a family member asserts a related claim, or a lawyer frames the employer's conduct as negligence outside the basic benefit system.

That is why employers liability insurance isn't optional window dressing for contractors. It's the legal backstop that helps the business survive the part of the loss workers comp doesn't solve.

For trade businesses, the practical takeaway is clear:

- Workers comp handles the statutory injury claim

- Employers liability insurance handles covered lawsuits tied to that injury

- State rules and contract wording can make the difference between real protection and a dangerous gap

A plumbing contractor adding vans and helpers, an electrician expanding into another state, or a roofer signing larger commercial jobs should review this coverage before the next bid, not after the next accident.

If a contractor wants a free, no-obligation review of workers comp and employers liability insurance, Coverage Axis can help evaluate the current setup, check for stop-gap issues, review contract requirements, and shop options that fit the trade, crew size, and states where the business operates.