A plumbing contractor opens a renewal packet, sees the workers comp number jump, and assumes the carrier pulled it out of thin air. The crew size looks about the same. The jobs look about the same. Yet the premium changed, and nobody on the insurance side explained why in jobsite language.

That frustration is common because workers compensation insurance premiums aren't intuitive. They're tied to payroll, job duties, claims history, state rules, and post-policy audits. A contractor can do the same headcount with a different payroll mix, a different class code setup, or one bad loss year, and the cost can move in a way that feels disconnected from day-to-day operations.

Contractors don't need a generic insurance lecture. They need to know why a roofing foreman costs more to insure than an office admin, why overtime records matter at audit, and why a third-party accident can still affect future premium. That's where the bottom line is made or broken.

Table of Contents

- Why Your Workers Comp Premium Is Not a Random Number

- The Basic Formula Behind Every Workers Comp Premium

- What Are Class Codes and Why Do They Matter So Much

- Your Experience Mod Is Your Company's Safety Scorecard

- Beyond the Formula Audits State Rules and Claims Impact

- Practical Tactics to Lower Your Workers Comp Premiums

- How an Advisor Helps You Get the Right Program Not Just a Policy

Why Your Workers Comp Premium Is Not a Random Number

It is Friday afternoon. A drywall contractor is closing out payroll, one crew is starting a school remodel on Monday, and the renewal quote hits the inbox. The premium is up, even though the owner feels like the business is running about the same.

That reaction is common, but the premium is not arbitrary. Workers compensation pricing follows exposure tied to the work your crews perform, how payroll is distributed, and how prior losses affect the account. For contractors, that can change faster than expected. A company may still look like the same business from the outside while the risk inside the policy has shifted from light service work to heavier installation, more ladder time, more driving, or more subcontractor coordination.

For smaller firms, this catches owners off guard because workers comp does not behave like a fixed monthly utility bill. It behaves more like a job cost that rises or falls with labor, trade mix, and claim activity. Contractors looking for a broader primer on coverage can start with this guide to workers comp for small business, but the pricing side gets more specific once crews are on active jobsites.

A plumbing contractor is a good example. Service techs running small residential calls do not create the same premium pressure as install crews handling water heaters, underground work, tenant improvements, or multi-story commercial jobs. Add an apprentice-heavy crew, more overtime, or a shift into larger remodels, and the premium can move even if revenue only changed modestly.

One job change can matter.

Here are the issues that usually move the number for contractors at renewal:

- Payroll movement: More field payroll increases the exposure base. A busy year often brings a higher premium before anyone looks at profit.

- Type of work performed: Framing, roofing, excavation, interior finish, and service work do not rate the same. The details of the job matter.

- Crew mix: Apprentices, helpers, working foremen, and office staff may be treated differently depending on duties and state rules.

- Loss activity: A single claim can affect cost well beyond the medical bill or lost time paid on that file.

- Jobsite conditions and contract structure: Work around other trades, owner-controlled sites, borrowed employees, and subcontractor issues can all affect how a carrier views the account.

One point many generic guides miss is that contractors do not operate in a vacuum. If your electrician gets hurt after another trade leaves debris in a corridor, that may turn into a third-party liability issue for someone else, but your workers comp claim can still hit your loss history first. From the owner's seat, that distinction matters because the claim can still influence future pricing even when another party shares fault.

State rules add another layer. A contractor with the same payroll and the same claim history can see different results across state lines because classification rules, rating bureaus, exemptions, and audit treatment are not uniform.

Treat the premium like a controllable operating expense. When you know which field decisions raise cost, you can fix the drivers before renewal instead of arguing with a number after it arrives.

The Basic Formula Behind Every Workers Comp Premium

The math involved is simpler than most contractors expect. Workers' compensation premium is mechanically driven by the class code rate × experience modification factor × payroll/100, and carriers often audit payroll 30–60 days after policy expiration according to ADP's explanation of how workers comp is calculated.

The formula in plain English

Think of the premium like a job estimate with three main inputs.

| Part | What it means | Why it matters |

|---|---|---|

| Payroll divided by 100 | The carrier standardizes payroll into units of $100 | More payroll means a larger premium base |

| Class code rate | The rate tied to the type of work being done | Higher-risk work usually carries a higher rate |

| Experience modification factor | A multiplier based on loss experience | Better results can lower cost, poorer results can raise it |

That formula creates the starting point. After that, state rules, schedule credits or debits, minimum premiums, and audit adjustments can still affect the final amount. But the bones of the calculation stay the same.

A contractor example

Take an electrical contractor. The business has field electricians, maybe an estimator, maybe one office employee, and payroll that changes depending on backlog. The field payroll gets assigned to the electrical class code, while clerical payroll should be separated if the operation and records support it.

If the owner lumps everyone together, the office payroll may get dragged into the field rate. If payroll estimates come in low at the start of the policy and the company has a strong year, the audit can produce an extra bill later. If payroll was overestimated, the audit can move in the other direction.

That's why a workers comp program for small businesses needs to be built around real payroll and real job duties, not a rough guess made during a rushed application.

Contractors usually don't get in trouble on the formula itself. They get in trouble on the inputs.

What doesn't work

Two habits create avoidable premium problems:

- Using annual payroll guesses with no backup: That almost guarantees a surprise at audit if the year changes.

- Treating every employee as interchangeable: A shop runner, estimator, and journeyman electrician don't create the same exposure.

A clean application with segmented payroll by role gives the carrier a much better picture. That's the first step toward getting workers compensation insurance premiums under control.

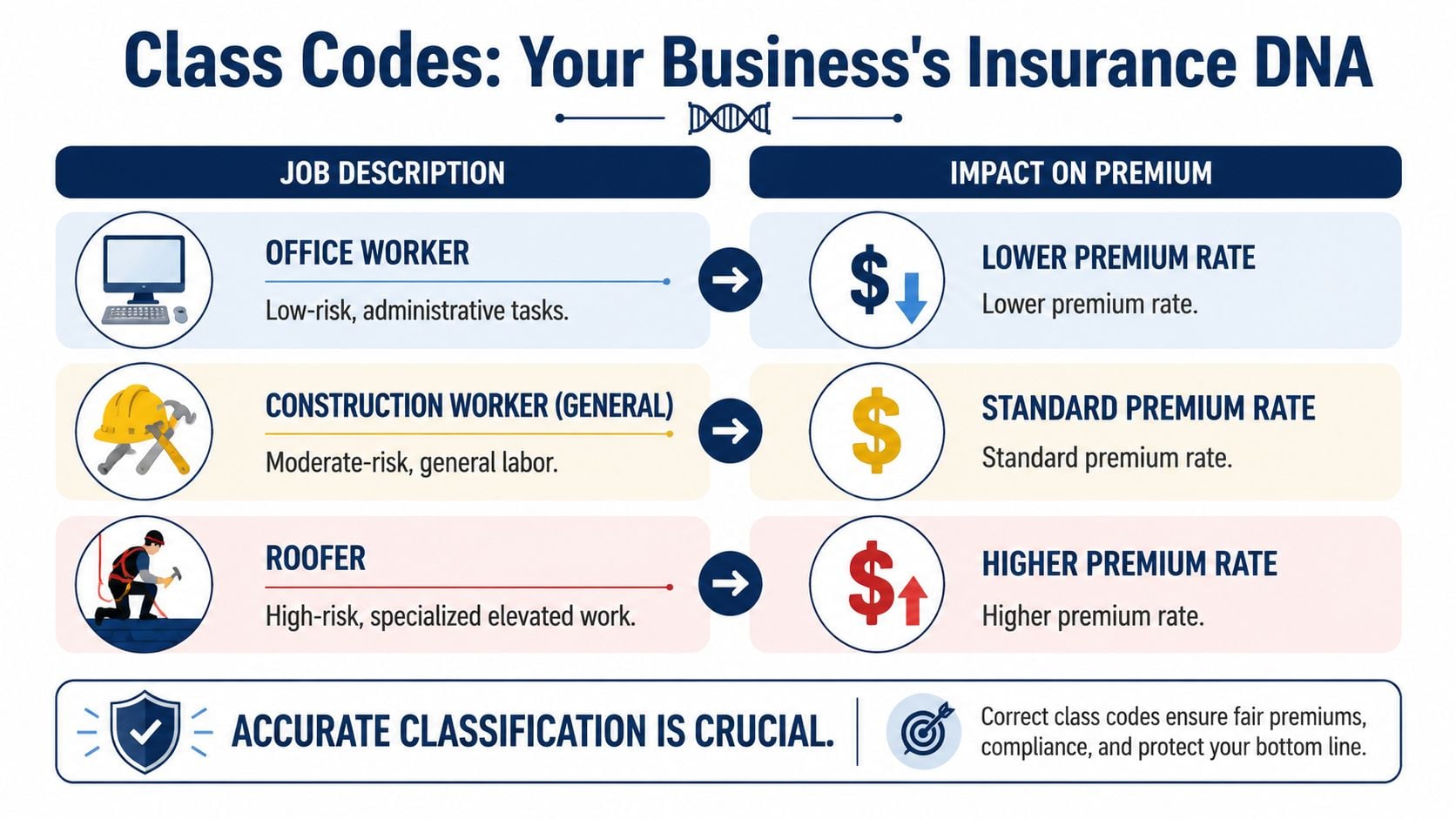

What Are Class Codes and Why Do They Matter So Much

Class codes are the language carriers use to sort job duties by risk. For contractors, they often matter more than any other line on the application because they determine which rate applies to each slice of payroll.

A roofing company is the easiest example. The field crew working on pitched roofs presents one level of hazard. The office admin answering phones and handling invoices presents another. If both groups have payroll but only one high-risk class code gets used, the premium can be distorted fast.

Benchmark cost data shows how sharply workers comp pricing changes by industry. The overall small-business average is about $54 per month, while construction averages $179 per month. Landscaping averages $150 per month, businesses with one employee average $38 per month, and firms with more than ten employees average $160 per month, based on TechInsurance workers comp cost benchmarks. The takeaway for contractors isn't that there's one cheap market. It's that risk category changes the price dramatically.

Why roofing payroll needs to be separated correctly

A roofing company might have four buckets of labor:

- Roof installers: High-hazard field work with fall exposure.

- Yard or warehouse staff: Material handling and loading exposure.

- Sales staff: Site visits, measurements, customer meetings.

- Clerical staff: Office-only duties.

If payroll records don't separate those roles clearly, the carrier or auditor may place more wages into the higher-rated classification. That doesn't happen because the carrier is being difficult. It happens because the records didn't support a lower-rated allocation.

Common classification mistakes

Contractors usually run into trouble in the same places:

- Blended roles: An employee who spends part of the week in the office and part in the field can't be treated like pure clerical staff if the recordkeeping doesn't prove distinct duties.

- Owner assumptions: Calling someone a “manager” doesn't make them low-risk if they still climb ladders, inspect active sites, or help crews.

- Bad payroll segregation: If there's no clean split between service work, installation, excavation, or shop time, the auditor may default to the broader, riskier class.

A title on a business card doesn't control workers comp. The actual work does.

What accurate class coding looks like

A contractor doesn't need perfect paperwork. But the business does need records that make sense.

| Situation | Likely outcome |

|---|---|

| Separate payroll by duty and keep job descriptions current | Better chance of accurate premium treatment |

| Lump all labor into one broad category | Higher chance of overclassification |

| Change operations mid-year and don't tell the agent or carrier | More audit friction and possible premium correction |

For trade businesses, class codes are where discipline pays off. A roofer will never price like an office firm, but that doesn't mean the business should overpay because the payroll story was sloppy.

Your Experience Mod Is Your Company's Safety Scorecard

A drywall contractor finishes a year with solid revenue, then gets hit with a renewal that costs more than expected. Payroll did not spike. Class codes did not change. The problem sits in the loss history. Two strain claims, one ladder fall, and a delayed report that turned a manageable medical claim into a more expensive file can all push the experience mod in the wrong direction.

The experience modification rate, usually called the experience mod or EMR, adjusts premium based on your company's claims experience compared with other employers in the same trade. For contractors, it works like a financial record of how jobsite losses are trending, not a general statement about whether the company cares about safety.

How contractors should read the mod

A mod below 1.00 generally helps premium. A mod above 1.00 usually pushes cost up. The part many owners miss is timing. The mod often reflects prior policy periods, so the foreman who lets ladder rules slide this quarter may be affecting insurance cost well after the job closes.

That delay matters in construction because losses are rarely random. A roofing company with one unusual claim is different from a roofing company that keeps producing similar fall, strain, or vehicle losses. Rating bureaus and carriers look for frequency and severity patterns inside the trade, then price accordingly.

For a closer explanation of how the factor is calculated, see this guide to workers comp experience modification.

What actually improves your score

Posters in the break room do not improve a mod. Field habits do.

- Fast reporting from the site: Same-day reporting gives the adjuster a cleaner file and usually helps control claim cost.

- Return-to-work options: Light duty for an injured tech, driver, or shop hand can keep a claim from getting more expensive than it needs to be.

- Supervisor discipline: If the written policy says tie-off is required, the superintendent has to enforce it on the roof, not just during orientation.

- Job-specific loss control: Fleet review for service contractors, lift plans for mechanical crews, and material-handling rules for framing teams reduce the types of claims that repeat.

A good mod usually comes from boring consistency. Crews know the rule. Supervisors enforce it. Injuries get reported fast. Modified duty exists before the claim happens.

The trade-off contractors deal with

Lowering the mod is not only about preventing injuries. It is also about managing claim cost without creating friction with the crew. Some owners wait too long to report because they do not want a small injury on the record. That decision often backfires. Small claims can become larger claims when treatment, documentation, and return-to-work planning all start late.

There is an administrative side too. Contractors with tight books and clean job costing usually spot claim trends earlier because payroll, project activity, and incident records line up. That is one reason firms that already value disciplined reporting, including those focused on accounting for London contractors, tend to handle premium questions with fewer surprises.

A jobsite example

Take an HVAC contractor with technicians driving between calls, hauling equipment, climbing attic ladders, and setting condensers. One isolated shoulder strain may have limited effect. A run of similar lifting claims tells a different story. Add a vehicle accident or two, and the mod can move enough to affect bidding costs on future work.

That is why experienced contractors treat the mod as an operating metric. It tracks whether field decisions, reporting habits, and return-to-work planning are protecting margin or pushing next year's premium higher.

Beyond the Formula Audits State Rules and Claims Impact

The formula gets most of the attention, but contractors usually get surprised somewhere else. The three biggest blind spots are premium audits, state-by-state legal rules, and claims that affect premium even when someone else caused the accident.

A general contractor sees this often. The firm starts the policy with an estimated payroll, adds a laborer crew for a fast-moving project, uses more subcontracted help than expected, and changes project mix during the year. The policy still looks fine on paper until the audit lands.

The audit is where estimates meet records

Workers comp starts with estimated payroll. It ends with actual payroll. If the estimate came in low, the carrier can bill additional premium after the year closes. If it came in high, the policyholder may receive money back.

That's why the bookkeeping side matters almost as much as the safety side. Clean payroll summaries, overtime records, class-code segregation, and certificates for subcontractors should be organized before the auditor asks. Contractors that already rely on disciplined project financials or outside support for accounting for London contractors understand the larger point. Insurance audit disputes often begin as recordkeeping problems, not coverage problems.

Third-party accidents can still affect future premium

This is one of the least explained parts of workers comp pricing. A worker can get injured because of a negligent driver, another subcontractor, a property owner condition, or a defective product. The contractor may still have a workers comp claim on its record, and that can influence future premium through experience-based pricing.

Whether the employer can recover those increased premium costs from the responsible third party depends heavily on state law. A legal review of this issue notes that some states may allow recovery, while many reject it as too indirect or speculative. Texas is specifically cited as barring recovery on that theory in the state-law discussion of recovering increased workers comp premiums.

A third party can cause the injury, and the employer can still feel the premium consequences.

That matters for contractors because jobsite liability is often shared. A masonry subcontractor may do everything right and still have an employee injured by another trade's equipment movement. The workers comp claim still exists. The premium impact question is separate from fault.

State rules change the practical answer

A contractor working across state lines can't assume one rule applies everywhere. Classification treatment, rating details, assigned risk issues, legal recovery theories, and filing requirements vary by jurisdiction. That's one reason contractors operating in Pennsylvania often review Pennsylvania workers compensation requirements before expanding payroll there.

A state filing can move the pricing environment too. Public rate news cited in industry glossary material shows that Wisconsin announced an 8.4% workers' compensation rate decrease for businesses effective Oct. 1, 2023 in the workers comp premium glossary discussing rating structures. The lesson isn't just that rates can go down. It's that workers compensation insurance premiums are shaped by regulation and market conditions as well as payroll math.

A short contractor checklist before renewal

- Review payroll by trade activity: Don't wait for the audit to discover that installation, service, and shop labor were mixed together.

- Track subcontractor documents: Missing certificates can create expensive audit disagreements.

- Document accident facts early: If a third party may be responsible, that information needs to be preserved from the start.

- Check state-specific assumptions: Multi-state contractors get in trouble when they assume one state's approach applies everywhere.

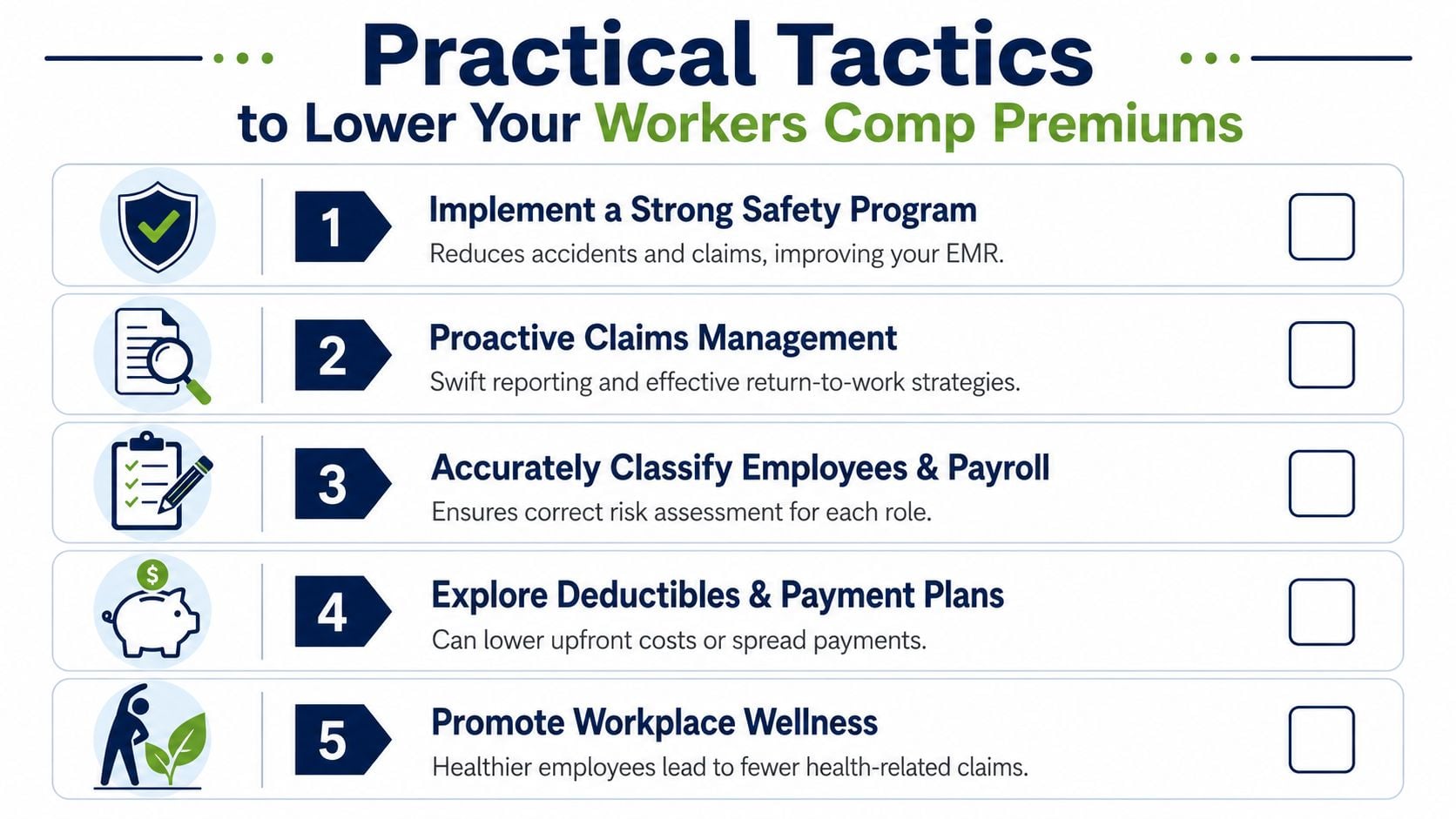

Practical Tactics to Lower Your Workers Comp Premiums

The best premium reduction strategy usually isn't “shop harder.” It's “operate cleaner.” Workers comp has long been structured as a percentage of payroll rather than a flat charge per employee, according to the Bureau of Labor Statistics analysis of employer workers comp costs. For contractors, that means cost control comes from managing labor-related variables, not just trimming headcount.

A landscaping company is a good example because the exposures vary. One employee may mow flat residential lawns. Another may trim trees. Another may install hardscape. Another may drive a truck and trailer all day. If the business treats that operation like one undifferentiated labor bucket, it gives away control.

What actually helps

- Build a written safety routine: Not a binder that sits in the truck. A real process with training, site-specific hazard checks, and foreman accountability.

- Use modified duty when possible: A return-to-work plan can help contain claim costs instead of letting small injuries become long absences.

- Separate payroll accurately: Tree work, irrigation, mowing, and hardscape don't always belong in one bucket. Good records support accurate rating.

- Prepare for the audit all year: Waiting until the auditor emails is too late.

- Consider program structure as the company grows: Larger contractors may need to evaluate whether standard guaranteed-cost pricing still fits.

Tactics that fail in the real world

Some cost-saving ideas sound good but backfire fast.

| Tactic | Why it usually fails |

|---|---|

| Underreport payroll | The audit can correct it later and create a retroactive bill |

| Put field employees in clerical codes | Job duties and records usually expose the mismatch |

| Chase the lowest quote only | Misclassification and bad structure often surface after binding |

| Ignore small claims | Repeated smaller losses can still damage the loss picture over time |

Good workers comp management starts in payroll, shows up on the jobsite, and gets tested at audit.

A subcontractor-heavy example

A concrete contractor using multiple subs can lower friction by collecting certificates before work starts, keeping signed agreements current, and documenting who is an employee versus who is an independent subcontractor under the applicable rules. Contractors that rely on subs regularly should understand how a workers comp approach for subcontractors fits into the broader risk plan.

For bigger operations, alternative structures may deserve a look. Retrospective rating, large-deductible, and dividend plans can make sense in the right circumstances, but only when the contractor understands the loss-retention tradeoff and has the financial controls to manage it. For everyone else, the first savings usually come from classification discipline, claims handling, and cleaner records.

How an Advisor Helps You Get the Right Program Not Just a Policy

By the time a contractor has dealt with class codes, payroll segmentation, audits, state rules, and claim-driven pricing, one thing becomes clear. Workers compensation insurance premiums aren't just about buying a policy. They're about building a program that matches how the business operates.

That's where experienced advisory work matters. A good advisor reviews job duties, checks whether office and field payroll are being separated correctly, looks for audit trouble before renewal, and discusses whether the current pricing structure still fits the size and volatility of the operation. For larger contractors, alternative approaches such as retrospective rating, large-deductible, and dividend plans can be worth evaluating, as noted in the earlier discussion of premium structures.

One practical piece that often gets missed is how workers comp connects to the employer liability side of the policy. Contractors that haven't reviewed that exposure recently should understand how employers liability insurance fits alongside workers comp when employee injury allegations move beyond a standard statutory claim.

Coverage Axis is one option contractors use when they want an independent advisor to shop multiple carrier options and structure coverage around trade type, payroll mix, crew size, and project profile rather than forcing the business into a generic package.

The cheapest quote on day one often becomes the most expensive policy at audit or claim time. The right program is the one that classifies the operation correctly, anticipates how payroll will change, and gives the business a workable plan for controlling losses over time.

If a contractor wants a second look at workers compensation insurance premiums, Coverage Axis offers a free quote and coverage review built for trade businesses. A licensed advisor can review class codes, payroll setup, claims trends, and current policy structure to help make sure the program fits the work being done.