For a small contractor, a standard $1 million per occurrence / $2 million aggregate general liability policy often lands around $750 to $2,500 per year. That number can swing fast, though, because the same coverage form can price very differently depending on trade, payroll, location, subcontractor use, and how the policy gets reconciled after audit.

That's the part many contractors miss. The quote that looks cheap in January can turn into a very different number after the policy term if revenue grew, payroll changed, or more subcontractors were used than originally estimated.

A common version of this problem looks like this: a contractor wins a few extra jobs midyear, hires help, leans on subs to keep deadlines, and assumes the original GL premium still tells the whole story. Then the audit lands. Suddenly the final cost of coverage isn't the down payment or monthly installment. It's the final billed premium after the carrier compares the estimate against what occurred in the business.

For contractors trying to budget tightly, that distinction matters as much as the quote itself. General liability insurance cost for contractors isn't just about shopping for the lowest number. It's about understanding what drives the price, what changes it during the year, and how to avoid getting surprised when the books are reconciled.

Table of Contents

- Why Contractor GL Insurance Costs Are So Variable

- The 7 Key Factors That Drive Your GL Premium

- Cost Scenarios What Contractors Like You Actually Pay

- How to Estimate Your Own General Liability Cost

- Smart Strategies to Lower Your Contractor Insurance Costs

- Beyond the Price How to Compare Quotes and Policies

- Get the Right Coverage at a Fair Price

Why Contractor GL Insurance Costs Are So Variable

A contractor gets a renewal and sees a number that feels off. Another contractor in the same town says his policy costs less. A project owner requires a certificate by Friday, and the new quote comes back higher than expected. On the surface, it can look arbitrary.

It usually isn't.

A standard contractor GL policy with $1M / $2M limits commonly falls around $750 to $2,500 annually, but the market spread can run from $25 per month to over $26,000 per month depending on the risk profile, according to contractor general liability cost data. That gap looks wild until the actual exposures are on the table.

A solo residential painter and a roofing company with multiple crews may both ask for “general liability,” but they're not bringing the same risk to the carrier. One has lighter third-party property damage exposure and less severe bodily injury potential. The other has ladder work, height exposure, more people on sites, more vehicle movement between jobs, and a bigger chance that completed work turns into a costly claim later.

Practical rule: If two contractors have very different day-to-day operations, they shouldn't expect similar GL pricing just because the limit is the same.

A plumbing contractor is a good example. A shop doing small residential service calls has one kind of exposure. A plumbing contractor doing tenant improvements in occupied commercial buildings has another. A burst line in a finished office suite is a different property damage problem than replacing a fixture in a vacant home under renovation.

That's why “fair” cost isn't one fixed number. It's a risk price.

Contractors who want the full picture should also look beyond the GL policy itself and understand what insurance contractors typically need across the whole operation, because GL pricing often makes more sense when it's viewed alongside payroll, autos, subcontractors, and project type.

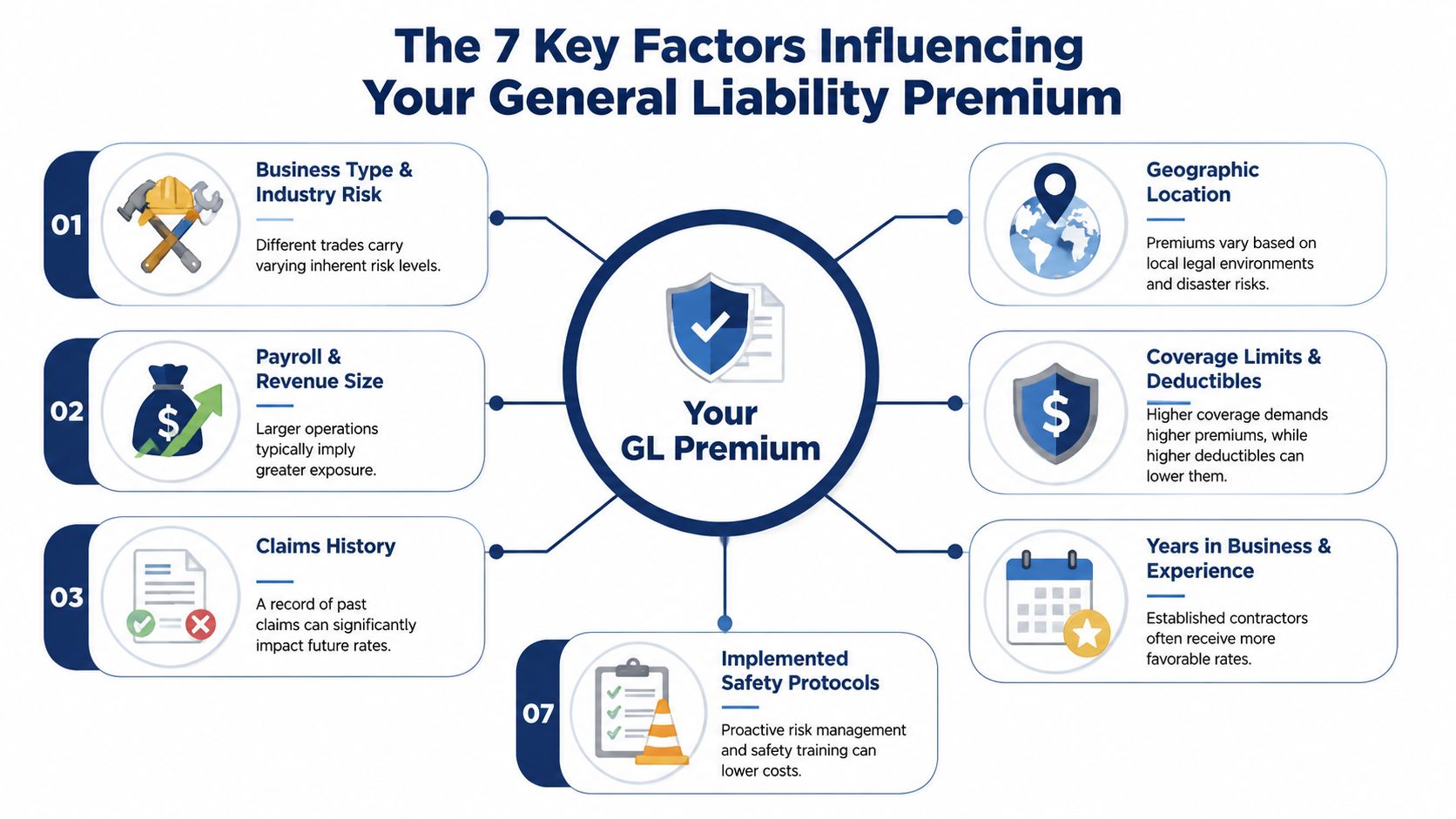

The 7 Key Factors That Drive Your GL Premium

To easily understand general liability insurance cost for contractors, envision it as seven pricing dials. Carriers turn each dial based on what the business does, then the premium lands where those combined exposures point it.

Trade classification sets the starting point

1. Trade classification

This is the big one. Carriers care what kind of work gets performed, not just what the business card says. An electrician, framer, roofer, HVAC installer, and plumber all create different claim patterns.

For an electrical contractor, residential service work usually presents a different profile than industrial installation or work tied to larger build-outs. The more severe the likely third-party injury or property damage claim, the more pressure there is on the rate.

2. Annual revenue

Revenue acts like a rough measure of how much work passes through the business. More jobs usually mean more customer contact, more site visits, and more chances for something to go wrong.

A one-truck electrician doing service upgrades has a different premium picture than an electrical contractor billing across many active projects. Even if both want the same limits, the volume of operations matters.

3. Total payroll

Payroll tells the carrier how much labor is moving through the operation. More employees usually means more time on jobsites, more tools in motion, and more opportunities for accidental damage to someone else's property.

A two-person electrical shop wiring panel replacements has less exposure than a larger crew running multiple sites at once. More hands can increase production, but they also widen the path for claims.

Payroll, revenue, and subcontractors change the exposure

4. Subcontractor costs

Subcontracting changes GL exposure in a way many owners underestimate. If a general contractor hires uninsured or poorly documented subs, the carrier may look at those payments as part of the insured's exposure base, especially at audit.

That matters a lot for remodelers and general contractors who sub out drywall, electrical, plumbing, or finish work. The certificate file has to be tight, or the “cheap” quote can get expensive later.

5. Coverage limits and deductibles

The policy structure still matters. Market data cited by contractor GL pricing benchmarks shows 89% of independent contractors choose a $1M / $2M limit structure, which makes that a useful baseline when comparing quotes. The same source also notes a median monthly premium of $55 and an average of $79 for new customers, while emphasizing that underwriting tier heavily affects where a contractor's premium is determined.

That's why a roofer and a handyman can both buy $1M / $2M limits and still see very different prices.

Limits, claims, and geography finish the pricing picture

6. Claims history

A contractor with prior liability losses gives the underwriter a reason to expect future trouble. Even one preventable claim can change how the account gets viewed.

For example, an electrician with prior property damage from panel work may still get coverage, but pricing and carrier options may tighten. Carriers don't just insure the trade. They insure the pattern of how that business has performed.

7. Geographic location

State and legal environment matter more than many contractors expect. Construction liability pricing guidance notes that carriers commonly base advance premium on estimated gross receipts and payroll, then adjust at year-end, and it also shows how sharply location can affect cost. The same type of GL policy in New York might cost $3,500 to $6,500+, while a similar policy in Ohio could run $700 to $1,800.

A contractor doesn't control the state's legal climate, but that legal climate still shows up in the premium.

A flooring contractor in a lower-cost state may be frustrated hearing what another business pays elsewhere, but state pricing isn't interchangeable. The project environment, litigation climate, and local rating conditions all play a role.

Cost Scenarios What Contractors Like You Actually Pay

Abstract ranges are useful, but they don't help much when a contractor is trying to place his own business on the map. Side-by-side examples make the pricing logic easier to see.

Three contractor profiles side by side

| Contractor Profile | State | Annual Revenue | Key Risk Factors | Estimated Annual Premium |

|---|---|---|---|---|

| Solo residential electrician doing service calls and panel swaps | Texas | Lower revenue profile relative to multi-crew firms | Moderate trade exposure, customer homes, light crew size, limited subcontractor use | Likely toward the lower end of the common $750 to $2,500 annual range for a standard $1M / $2M policy |

| Three-person roofing crew focused on residential installs | Florida | Higher activity than a solo operator | Height exposure, completed operations concerns, larger crew, more severe bodily injury and property damage potential | Likely above lower-risk trades, potentially outside the lower end of the common range depending on underwriting |

| General contractor using subcontractors for remodel and light commercial work | California | Higher operational volume than a solo trade contractor | Heavy subcontractor management, broader jobsite exposure, more moving parts, higher chance of audit adjustment | Often priced higher than small single-trade contractors, especially if subcontractor documentation is weak |

These aren't quoted prices. They're practical reference points built from the market ranges discussed earlier.

The important takeaway is that the same $1M / $2M policy limit doesn't create the same premium across trades. A roofer can't price coverage by asking what a painter pays. A general contractor that subs out most of the work can't assume a solo electrician's number applies either. The operation drives the price.

A useful comparison point for trade-specific planning is this guide to electrical contractor insurance cost, because electrical contractors often sit in the middle ground where the work isn't priced like the lowest-risk trades, but it also isn't automatically treated like the highest-hazard classes.

The real question isn't “What does a contractor pay?” It's “What does a contractor with this trade, this payroll, this subcontracting model, and this state usually pay?”

That's why broad averages only go so far. A contractor gets a better budget number by matching his own operation to a realistic peer profile than by chasing a single market average.

How to Estimate Your Own General Liability Cost

A contractor doesn't need a rating manual to get a useful ballpark. The better approach is to estimate the way an underwriter looks at the account, then place the business on the low, middle, or high side of the likely range.

Start with trade and project type

Start with the work itself.

Classification risk and project exposure are the biggest cost drivers, according to market benchmarks for contractor GL pricing. The same source notes that 89% of independent contractors choose a $1M / $2M limit structure, which makes that a sensible baseline when comparing one quote to another.

A drywall contractor doing interior remodel work has a different profile than a roofer handling tear-offs. An electrician doing residential service work is different from an electrical contractor doing commercial tenant improvements. The first estimate should answer one question: is this operation generally lower hazard, middle hazard, or higher hazard compared with other trades?

Use a simple mental screen:

- Lower-hazard end: Trades with less severe third-party injury potential and less catastrophic property damage potential.

- Middle range: Trades with regular site work, customer property exposure, and meaningful completed operations concerns.

- Higher-hazard end: Trades with height, heat, structural, or larger-loss exposure.

Build the estimate the way an underwriter does

Once trade is clear, the next step is operational scale.

- Payroll: More labor usually means more exposure.

- Gross receipts: More work volume usually means more opportunities for claims.

- Subcontracted cost: More subs can change the rating picture and the audit outcome.

- Claims history: Prior losses can move the account into a tougher underwriting tier.

- State: Local legal climate can push pricing up or down.

The same benchmark source notes a median monthly GL premium of $55, but that figure is heavily affected by underwriting tier. That's the key. Median numbers are only useful if the contractor understands whether his own business belongs in a favorable tier or a tougher one.

A small plumbing contractor can walk through this quickly. If the company works in a lower-cost state, has no recent claims, uses little or no subcontracting, and does straightforward residential service work, the premium will often track closer to the lower side of the normal contractor range. If that same company adds crews, starts doing larger occupied commercial projects, and uses more subs, the estimate should move upward even before a formal quote arrives.

Field check: If payroll, receipts, or subcontractor use are likely to change during the year, the starting quote should be treated as a deposit, not the final number.

That mindset helps with budgeting. It also keeps contractors from comparing policies based only on the first invoice.

Smart Strategies to Lower Your Contractor Insurance Costs

Contractors usually have more control over premium than they think. Not total control, because nobody can change the trade class or the state overnight. But enough control to keep costs from drifting upward for preventable reasons.

Control the parts of the premium you can actually influence

The most overlooked cost issue is audit reconciliation. Contractor audit guidance notes that final GL premiums are often adjusted after year-end audits based on actual gross receipts, payroll, and subcontracted costs. If the business underestimates activity during quoting, the carrier can bill a back-charge later.

That changes how smart contractors manage the policy year.

- Give realistic estimates up front: A low estimate may make the initial quote look better, but it doesn't reduce the true exposure if the business is growing.

- Track subcontractor paperwork carefully: Missing certificates can create trouble when the carrier reviews who worked on jobs.

- Update the broker or carrier when operations change: A contractor that adds crews, expands territory, or changes project type shouldn't wait until audit to explain it.

- Separate insured subs from uninsured subs in the records: Clean documentation makes audit disputes easier to resolve.

A masonry contractor is a good example. If the business starts the year expecting small residential work but picks up larger commercial projects and hires more subcontracted labor to keep pace, the audit likely won't care what the January estimate was supposed to be. It will care what really happened.

Treat the audit like a job cost review

The contractors who handle audits well tend to treat them like bookkeeping, not like a surprise inspection.

A simple administrative routine helps:

- Review payroll monthly so labor changes don't pile up unnoticed.

- Match subcontractor invoices to certificates before payment files get buried.

- Check revenue trends quarterly if the schedule is filling faster than expected.

- Keep safety routines documented because disciplined operations often support a cleaner loss history over time.

For shops that already run regular fleet and equipment checks, a good preventive maintenance checklist can also reinforce the kind of operational discipline that reduces avoidable incidents. Better records and fewer preventable mishaps won't rewrite the trade class, but they can support a better overall insurance profile.

Good insurance costs usually start with good records. Sloppy paperwork is expensive on the back end.

Workers' comp performance also affects the broader insurance picture for many contractors. For firms trying to tighten overall insurance costs, understanding workers comp experience modification helps connect safety, claims, and long-term premium control across the business.

When a contractor needs market access help, one factual option is Coverage Axis, which works as an independent commercial insurance advisory for contractors and places accounts with multiple A-rated carriers. That kind of setup can help when the goal is comparing structure, not just chasing the smallest invoice.

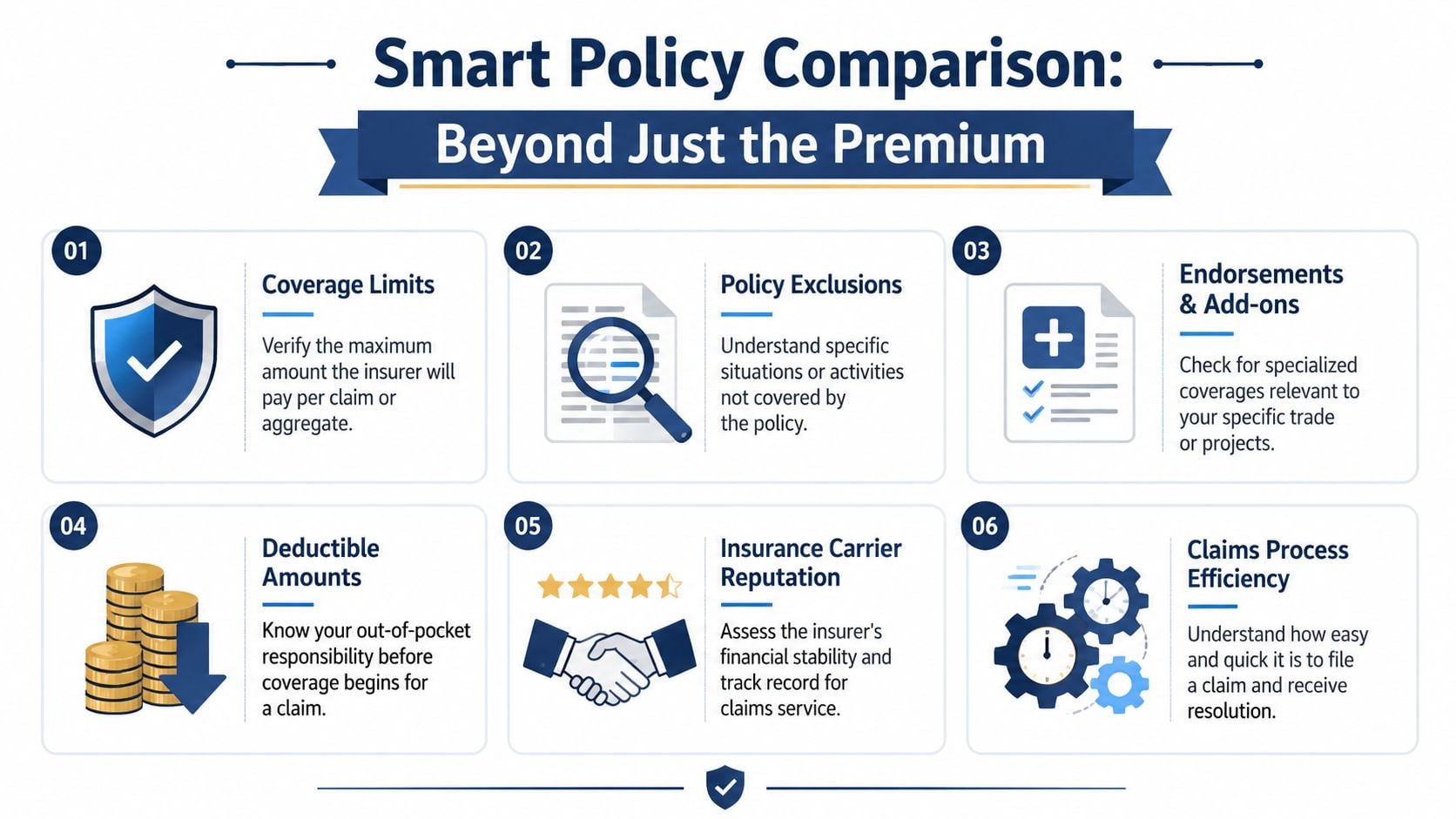

Beyond the Price How to Compare Quotes and Policies

A cheap GL quote can become an expensive mistake if it cuts out the work the contractor performs. Premium matters, but policy language decides whether the claim gets paid.

Read the coverage, not just the premium

A contractor should start by confirming the quote matches their actual operation.

For example, a roofing contractor needs to know whether the policy has exclusions tied to certain roofing methods or operations. An electrician needs to know whether the form is limited to residential work if the company also touches commercial jobs. A remodeler should check whether subcontracted work is treated the way the business model requires.

The financial strength of the carrier matters too. Contractors often hear “A-rated carrier” and move on, but the practical reason is simple. A policy only helps if the insurer can respond when a claim hits.

A lower premium doesn't help if the exclusion removes the exact work that creates the exposure.

Another point that gets missed is form type. Contractors should confirm whether the GL policy is written on an occurrence basis and understand how completed operations is treated, because that can matter long after the crew leaves the site.

Use an apples-to-apples checklist

When comparing proposals, this checklist keeps the review grounded:

- Match the limits: Don't compare one quote at $1M / $2M against another built on a different structure.

- Read exclusions carefully: Trade-specific exclusions can gut the value of a lower premium.

- Check endorsements required by contracts: Additional insured language often matters as much as the base policy.

- Confirm who counts as insured: Owners, entities, and named insured details should line up with contracts and licenses.

- Review deductibles and reporting obligations: A lower premium paired with terms the contractor can't realistically manage may not be a good deal.

Contractors that regularly issue certificates should also understand how general liability coverage limits affect project requirements, because a quote that looks fine on price can still fail a contract review if the structure doesn't match what the owner is asking for.

The goal isn't to buy the cheapest GL policy. It's to buy the cheapest policy that still does the job when the claim or contract arrives.

Get the Right Coverage at a Fair Price

General liability insurance cost for contractors is never just one number. The upfront premium depends on trade, payroll, project type, claims history, subcontracting, and state. The final cost can shift again if the year-end audit shows the business was larger or busier than originally estimated.

That's why contractors get into trouble when they shop by invoice alone. A quote has to be measured against the actual operation, specific contract requirements, and the likelihood of audit changes later. A low starting premium can still be the wrong choice if the classification is wrong, the exclusions are too tight, or the estimate was unrealistic from day one.

A framing contractor, electrician, plumber, or general contractor doesn't need the same policy just because all of them need GL. Each operation has its own exposure pattern, and the pricing follows that pattern.

Project owners also care about policy structure, not just whether a certificate exists. That's one reason many contractors should review contract requirements around items like additional insured endorsement language before binding coverage.

The best move is simple. Get quotes built on accurate numbers, compare the forms carefully, and budget for the policy as a living cost that can change if the business changes.

Coverage Axis offers free, no-obligation contractor insurance quotes and coverage reviews. A licensed advisor can help compare policy terms, check whether estimated payroll and receipts are realistic for audit purposes, and shop the market for a better fit based on trade, crew size, and project type. Contractors who want a cleaner number before renewal or a second look at their current policy can start with Coverage Axis.