A small electrical firm can easily land at over $5,000 per year once core policies are combined, and one national 2026 benchmark put a small electrical contractor package at $2,279 per year or $190 per month across five common coverage types. That's the starting line, not the finish line, because the actual electrical contractor insurance cost changes fast when a business adds employees, vehicles, tools, tougher jobsite exposures, or contract-required limits.

A familiar problem shows up when an electrician wins a chance to bid a solid commercial job, then reads the insurance requirements and realizes the low-cost policy bought online won't get past the certificate review. The general contractor wants higher liability limits, additional insured status, completed operations protection, and maybe umbrella coverage. Suddenly, insurance stops looking like a line-item expense and starts looking like a gatekeeper for revenue.

For an electrical contractor, that's the key issue. The question isn't just “What does insurance cost?” The better question is “What does the right insurance stack cost if the business wants to stay compliant, protect payroll, and keep bidding better work?”

Table of Contents

- What Is the Real Cost of Insuring Your Electrical Business

- Breaking Down the 4 Key Policies for Electricians

- How Crew Size and State Affect Your Insurance Costs

- Hidden Cost Drivers Beyond Payroll and Policy Type

- 5 Actionable Ways to Reduce Your Insurance Premiums

- Your Next Steps for an Accurate Insurance Quote

What Is the Real Cost of Insuring Your Electrical Business

A contractor lands a small commercial tenant build-out, sees an ad for low-cost electrician insurance, buys a basic policy, and figures the box is checked. Then the certificate request comes in. The property manager wants higher liability limits, the GC wants additional insured status and waiver of subrogation, and the van on the job is not even on the policy. That is how a cheap premium turns into an expensive mistake.

The cost to insure an electrical business is built in layers. The first number you see is rarely the number you need to operate, satisfy contract requirements, and keep work moving. A functioning electrical business usually needs coverage that follows the company on the road, on the jobsite, and after the work is done.

Cheap insurance and usable insurance are not the same product.

A bare-bones policy may be enough to print a certificate. It may do nothing for a commercial bid package, a landlord requirement, a helper who gets hurt, or a service van involved in a claim. Contractors who want a clearer picture of what owners, GCs, and licensing bodies often ask for should review these electrical contractor insurance requirements.

The practical question is not, “What is the lowest premium?” It is, “What coverage stack does this shop need to keep working without contract problems or uninsured losses?” For many electricians, that stack starts with liability and then adds workers' compensation, commercial auto, and tools or equipment coverage. Some jobs also push the need for higher limits, special endorsements, or excess liability.

That gap catches small shops all the time. A solo service electrician may only be thinking about price. Then a larger customer asks for proof of coverage that matches the contract, and the policy that looked cheap no longer works. The business either upgrades mid-job, pays more because the change is rushed, or loses the work.

Insurance belongs in the same operating-expense conversation as fuel, payroll taxes, and materials tracking. It is one of the costs that are essential for business survival and growth, especially when one claim or one rejected certificate can disrupt cash flow.

Here is the rule I give electrical contractors. If the policy cannot satisfy a GC, property manager, landlord, lender, or permit requirement, it is not the low-cost option. It is the option that risks delay, back charges, or a lost contract.

Benchmarks still help. They set a starting budget. They just do not tell you what your shop will pay, because underwriters price the work being done, the vehicles on the road, the payroll on the books, the loss history, and the kinds of jobs you take.

A company wiring custom homes is priced differently from a crew working in occupied offices, retail suites, or light industrial space. Add apprentices, more vans, higher payroll, more expensive tools, or stricter contract requirements, and the annual insurance cost climbs one layer at a time. That is how electrical contractor insurance cost shows up in the field.

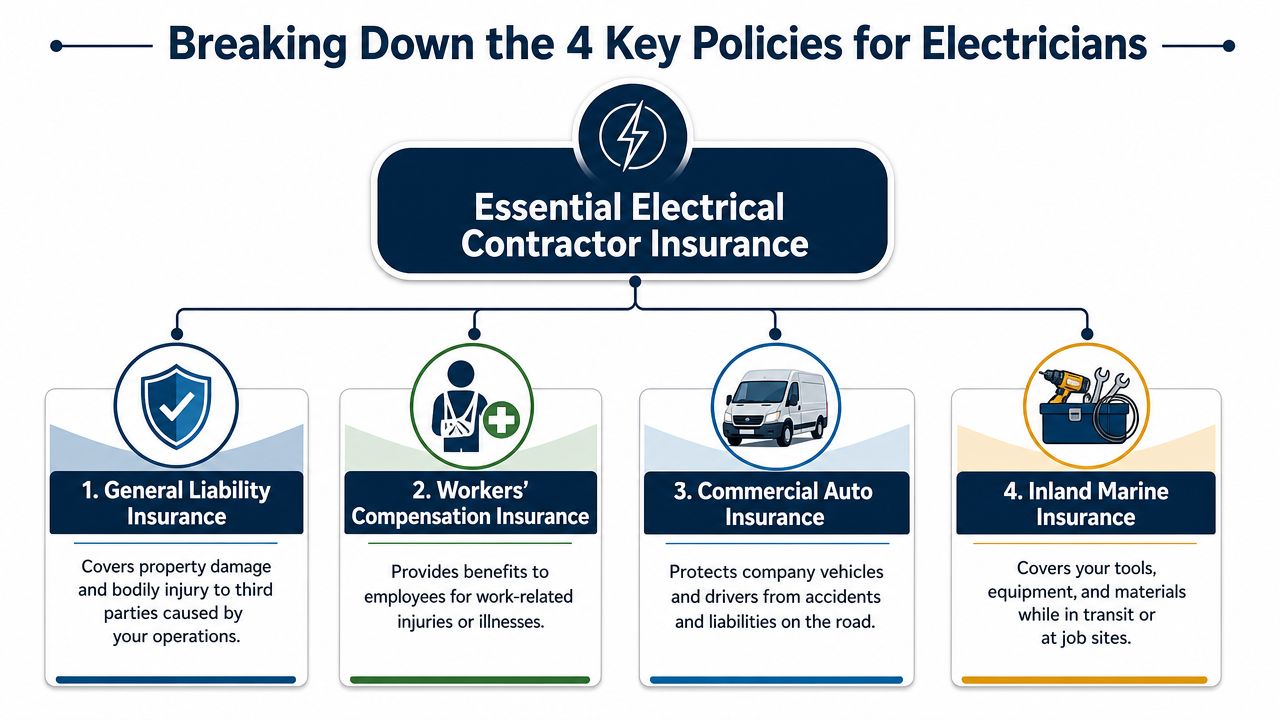

Breaking Down the 4 Key Policies for Electricians

The core package makes more sense when each policy is tied to an actual loss scenario instead of insurance jargon.

General liability

General liability protects the business when its work causes damage to someone else's property or causes bodily injury to a third party.

For an electrical contractor, the classic example is completed work. A crew finishes a panel change and branch circuit work in a mixed-use building. Weeks later, a fault tied to the work causes damage after the crew has left. That's the kind of claim contractors expect general liability to respond to, subject to policy terms and endorsements. This is also where coverage limits matter, especially on commercial work. Contractors comparing options often need a plain-English breakdown of general liability coverage limits before signing a policy.

Workers' compensation

Workers' compensation covers employee injuries tied to the job.

The electrician version of this isn't theoretical. An apprentice is helping terminate conductors in a live panel, takes a shock, falls, and needs medical treatment plus time away from work. That claim doesn't belong on general liability. It belongs on workers' compensation.

This policy is often one of the biggest cost drivers because electrical work combines injury severity with payroll. The more field labor on the books, the more this line usually matters.

Commercial auto

Commercial auto protects company vehicles and the liability that comes with putting them on the road for business.

A common claim looks simple at first. A service van heading to a remodel job rear-ends another vehicle at a stoplight. The tools in the back shift, materials are delayed, the other driver is injured, and now the business has an auto claim tied directly to operations.

For electricians, personal auto policies often don't match the way vehicles are used. Lettered vans, stocked racks, employees driving, and regular jobsite travel change the exposure.

A van isn't just transportation for an electrical contractor. It's rolling inventory, rolling tools, and often the first thing a claimant's attorney notices after a road accident.

Inland marine for tools and materials

Many contractors still call this tools and equipment coverage, and that's usually how they think about it.

The field example is familiar. A crew leaves conduit benders, testers, cordless tools, and spools of wire locked in a van or staged on a temporary site. Theft hits overnight. The truck policy may deal with the vehicle itself, but the tools and materials are a separate issue. That's where inland marine coverage comes in.

Why the stack matters

Each policy handles a different slice of the risk:

- General liability deals with third-party injury and property damage.

- Workers' compensation deals with employee injury.

- Commercial auto deals with road exposure.

- Inland marine deals with mobile tools, equipment, and job materials.

Miss one layer, and the business can end up standing in the gap.

How Crew Size and State Affect Your Insurance Costs

Electrical contractor insurance cost moves in two directions at the same time. One is geographic. The other is operational.

A national 2026 analysis found a 191% spread between states, with a small electrical contractor package ranging from $230 per month in West Virginia to $671 per month in California, according to this state-by-state electrical contractor pricing analysis. The same analysis found that workers' compensation averaged $274 per month per employee, which is why adding field payroll can change the premium quickly.

Why geography changes the price

Two electrical contractors can run similar operations and still get very different pricing because state conditions change the baseline.

That includes how claims are handled, how labor risk is priced, local litigation conditions, and vehicle exposure. A contractor in a lower-cost market may think a quote looks high until a comparison is made with a higher-cost state. Geography alone can shift the budget before a single endorsement gets added.

A practical example helps. A two-person shop doing service work out of one van in a lower-cost state may still carry a manageable package. That same operating setup in a higher-cost state can come back noticeably more expensive before any umbrella or project-specific requirement is added.

A simple budgeting table

The table below uses verified monthly averages where available and applies the national workers' compensation per-employee benchmark to show how crew growth affects the total. It's a budgeting illustration, not a quote.

| Crew Size | General Liability (GL) | Workers' Compensation (WC) | Commercial Auto (1 Vehicle) | Inland Marine (Tools) | Estimated Total Monthly Premium |

|---|---|---|---|---|---|

| Solo operator | $57 | $0 | $140 | $41 | $238 |

| Two-person crew | $57 | $548 | $140 | $41 | $786 |

| Five-person crew | $57 | $1,370 | $140 | $41 | $1,608 |

The table shows why contractors need to budget insurance as a growth cost, not a static overhead item. Once payroll increases, workers' compensation often becomes the line that moves the fastest. Businesses that are hiring or adding apprentices should understand how workers comp for small business changes as payroll and headcount increase.

If a contractor adds three field employees and keeps budgeting insurance like a solo shop, the renewal usually becomes a surprise.

State and crew size don't explain every premium difference, but they explain a lot. They also explain why two contractors doing “electrical work” can have very different insurance costs.

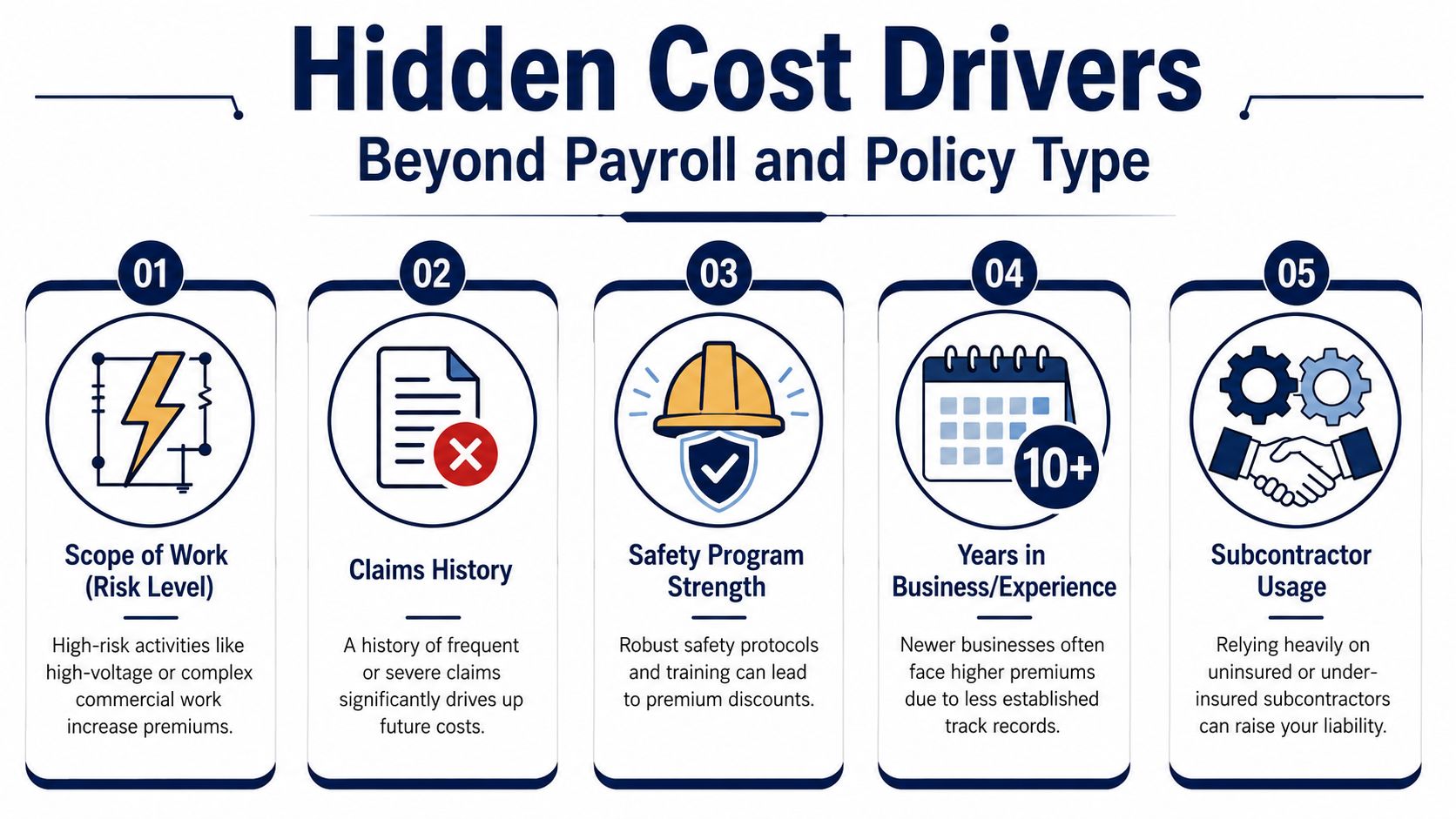

Hidden Cost Drivers Beyond Payroll and Policy Type

Payroll and policy count are only the visible part of the bill. Underwriters usually go deeper.

What underwriters look at after the basics

Two electrical contractors can have similar headcount and still price very differently because the work itself isn't the same.

A company focused on low-voltage residential service calls usually presents a different exposure than a contractor doing energized commercial service, high-elevation lighting installations, or work in occupied medical or industrial spaces. The farther the operation moves from routine service and toward higher-hazard work, the more attention it usually gets from underwriting.

Claims history also matters. Frequent losses, even smaller ones, can tell an insurer that field controls are weak, drivers aren't being managed well, or tool theft is recurring because storage practices are loose.

A documented safety culture can help. So can accurate payroll reporting, clean vehicle schedules, and clear job descriptions. Contractors that keep better records usually have better conversations with underwriters. Shops that struggle with documentation often struggle with pricing too. That's one reason many firms lean on organized financial support, including outside bookkeepers, to keep payroll, job costing, and insurance records consistent.

Subcontractors and paperwork that actually matter

Subcontractor management is one of the most overlooked premium drivers in the trades.

If an electrical contractor hires subs and doesn't collect current certificates of insurance, signed agreements, and proof of proper coverage, the risk can roll uphill. That can affect liability exposure and how the insurer views the account at renewal. Paperwork isn't glamorous, but it changes how much risk the insured business is really carrying.

A practical field example is common. A contractor subs out a portion of finish work on a retail project. The sub damages finished property or causes an injury; the sub's coverage is then missing, expired, or inadequate. The hiring contractor is now pulled into the mess.

Good subcontractor paperwork won't make a bad risk good, but bad subcontractor paperwork can make a decent risk look worse than it is.

Another hidden driver is the workers' compensation experience picture over time. A contractor's loss record affects how future workers' compensation pricing is viewed, which is why businesses should understand the basics of workers comp experience modification and how claim frequency can follow them.

Other factors that often move the premium

- Years in business: Newer firms usually face more scrutiny because they haven't built a long operating record.

- Vehicle use patterns: Long daily routes, multiple drivers, and poor motor vehicle records tend to increase concern.

- Equipment handling: Loose storage, overnight vehicle parking habits, and inconsistent tool inventories can affect tools coverage.

- Project mix: Work in schools, hospitals, multi-tenant buildings, or industrial sites may bring tighter insurance requirements and tougher underwriting questions.

The main point is simple. Electrical contractor insurance cost isn't just built from payroll and policy type. It's also built from how the business operates when nobody is looking.

5 Actionable Ways to Reduce Your Insurance Premiums

A cheap quote can fall apart the moment a GC asks for higher limits, waiver language, or extra insured status. Then the contractor buys the missing pieces under deadline, pays more than planned, and still risks losing the job if the paperwork is late. Premium control starts with building the right coverage stack the first time.

The goal is simple. Lower avoidable cost without weakening the insurance program you need to bid, get approved, and keep working.

Cut waste without cutting usable coverage

Bundle policies if the operation is small enough for it to make sense

For a smaller electrical shop with an office, basic tools, and limited property exposure, packaging general liability and business property can reduce overlap and simplify renewals. It also cuts down on gaps that show up when one carrier writes liability and another writes property. Bundling is less useful once the operation grows, adds multiple vehicles, takes on larger commercial jobs, or needs separate layers to meet contract requirements.Put the safety program on paper and keep records

A carrier can only price what it can verify. Written toolbox talks, driver rules, ladder procedures, lockout and tagout practices, and incident reporting logs give underwriters something concrete to review. That matters most on workers' compensation and auto, where a pattern of preventable claims can push costs up for years.Clean up subcontractor controls before a claim exposes the weakness

If subs are used for trenching, low-voltage work, or overflow labor, collect certificates before work starts and track expiration dates. Match the sub's coverage to the work being hired out. If a contract calls for status for the upstream party, know how an additional insured endorsement applies before agreeing to it in the bid or subcontract.Review insurance against current operations 60 to 90 days before renewal

Proactive review allows contractors to save money and avoid being caught off guard later. New vans, added journeymen, a shift from residential service to tenant improvement, or entry into public work can change the account enough to affect both pricing and eligibility. Early review gives time to fix classifications, remove old equipment, update driver lists, and address contract requirements before a certificate gets rejected.Raise deductibles only to a level the business can absorb in cash

Higher deductibles can reduce premium, but they shift claim cost back onto the contractor. That trade-off works for firms with steady cash reserves and a clean loss history. It is a bad fit for shops that would struggle to fund repairs, replace stolen tools, or cover a liability claim deductible while payroll and suppliers still need to be paid.

Insurance savings should come from cleaner operations, better documentation, and fewer surprises in underwriting. That same operating discipline shows up in broader financial planning too, which is why these business-focused strategies for cost reduction are worth reviewing.

Saving a few hundred dollars on premium means little if the policy cannot satisfy contract terms or support a commercial bid.

The best result is not the smallest number on the quote. It is the lowest sustainable total cost for coverage the business can put to work.

Your Next Steps for an Accurate Insurance Quote

Most bad quotes start with bad inputs. If the business description is vague, payroll is incomplete, or vehicle use isn't explained clearly, the pricing usually comes back rough and the coverage gaps show up later.

What to gather before asking for pricing

An electrical contractor will usually get a better result by preparing five basics up front:

- Payroll details: Separate office staff from field labor and be clear about who performs electrical work.

- Vehicle information: List each vehicle, who drives it, and how it's used.

- Job description: Explain whether the work is residential service, tenant improvement, new commercial build-out, industrial, low-voltage, or a mix.

- Claims history: Be upfront about past losses. Surprises found later don't help pricing.

- Tools and equipment information: Identify mobile tools, testing equipment, and materials that travel to sites.

A specific trade example shows why this matters. If a contractor says the company does “electrical work,” that leaves too much open. If the submission says the business handles service calls, panel upgrades, tenant build-outs, and one company van, the insurer can price that operation more accurately.

The same goes for contract requirements. If the business is bidding commercial jobs, the quote request should include any insurance specifications early. Waiting until after binding to ask for endorsements, higher limits, or extra layers is one of the fastest ways to find out the original policy wasn't built for the work.

A solid quote process should feel more like a pre-job checklist than a paperwork maze. Clean information leads to cleaner options, fewer surprises, and better odds that the insurance program will hold up when a client asks for a certificate on short notice.

Electrical contractors that want a faster way to compare real options can get a free quote or coverage review from Coverage Axis. A licensed advisor can review payroll, vehicles, project types, and contract requirements, then shop the market and help build a policy stack that fits the work instead of just chasing the lowest upfront premium.