A lot of contractors hit the same moment. A good job lands in front of them, the scope looks solid, the client looks real, and then the insurance requirements page shows up. It's packed with terms that sound familiar but don't line up with how the work happens on site. General liability. Additional insured. Waiver of subrogation. Completed operations. Auto limits. Umbrella. Maybe a bond.

That page isn't paperwork for paperwork's sake. It's a stress test for the business.

The contractors who treat insurance like a system usually move through that process faster. They qualify for better work, protect the company when something goes sideways, and avoid the ugly surprises that show up after a claim, an audit, or a subcontractor mistake. Contractors who buy the cheapest policy and assume it covers “the usual stuff” often find the holes at the worst possible time.

A solid starting point is understanding what insurance contractors need for real-world jobs. From there, the decision gets more practical. Which policy handles damage to the customer's property? Which one responds when an employee gets hurt? Which one protects the truck, the trailer, the tools, the completed work, and the risks coming from subcontractors?

Table of Contents

- What General Contractor Insurance Really Means for Your Business

- The Foundation Your General Liability Insurance Policy

- Protecting Your Crew Workers Compensation and Commercial Auto

- Beyond the Basics Umbrella Bonds and Inland Marine

- Solving the Subcontractor Puzzle COIs and Risk Transfer

- What Drives Your Insurance Premiums and How to Control Them

- Get the Right Coverage Built for Your Contracting Business

What General Contractor Insurance Really Means for Your Business

General contractor insurance isn't one policy. It's the protection around the business itself. It keeps one accident, one fire, one injury, one bad subcontractor hire, or one vehicle claim from turning into a company-killing event.

For a small residential remodeler, that might mean keeping a customer's property damage claim from reaching personal assets. For a growing commercial GC, it might mean meeting bid requirements that make larger projects possible. Either way, insurance changes from a grudging expense to a tool that lets the business keep operating after a problem.

A contractor bidding a tenant improvement job sees that shift fast. The owner wants a certificate of insurance, specific liability limits, completed operations coverage, and proof the right entities can be added to the policy. Without that setup, the contractor may not even get through prequalification. With it, the contractor looks organized, insurable, and ready to perform.

Contractors don't buy insurance just to satisfy a contract. They buy it so one claim doesn't undo years of work.

The key is to stop looking at each policy by itself. General liability protects against outside claims. Workers compensation protects the crew. Commercial auto protects road exposure. Umbrella raises the ceiling. Inland marine protects movable equipment. Bonds help qualify for work. Subcontractor risk transfer keeps someone else's problem from landing on the GC's desk.

That system matters whether the company runs one pickup and a trailer or several crews across multiple sites. The details change by trade, but the pressure points stay the same. Someone can get hurt. Something can get damaged. A truck can crash. Tools can disappear. A sub can hand over a bad certificate and leave the GC holding the bag.

The Foundation Your General Liability Insurance Policy

A lot of claims hit a GC from the outside, not from payroll. General liability is the policy built for that lane.

Say a finish carpenter leaves a stair tread unprotected during a remodel and the homeowner slips. Or a laborer backing material through a hallway gouges finished drywall and trim in an occupied office. Those are the kinds of third-party bodily injury and property damage claims that usually start under GL.

What GL does on a job site

On a real project, GL handles claims brought by customers, visitors, owners, tenants, and other third parties who say your work or operations caused harm. It usually comes down to three buckets:

- Property damage: You or a trade damages the client's building, finished work, or nearby property during the job.

- Bodily injury: A non-employee gets hurt because of site conditions, falling debris, tools, materials, or active operations.

- Personal and advertising injury: Less common for contractors, but still part of the policy form.

The practical value is bigger than the policy definition. GL is often the policy that gets you through prequalification, satisfies lease and contract requirements, and gives the carrier a place to start defending a claim before it turns into a cash-flow problem. Contractors reviewing limits, forms, and common coverage parts can get a better baseline from this guide to general liability insurance for contractors.

The fine print matters. Construction-focused GL should address issues like completed operations, contractual liability tied to your written agreements, and exclusions that can gut coverage for the kind of work you perform. Public owners and commercial clients often spell out those requirements in their insurance exhibits, as outlined in the Austin construction insurance requirements document.

What GL does not pay for

Here, contractors encounter significant problems.

GL does not replace workers compensation. If your own employee gets hurt hauling pipe, falling off staging, or cutting blocking, that claim belongs in the workers compensation bucket. GL also does not work like a warranty for your workmanship. If your crew installs something wrong, the cost to tear out and replace your faulty work is often your problem, while resulting damage to other property may be handled differently depending on the facts and the policy language.

That difference is not academic. It is one of the gaps that can hit a contractor from two directions at once. A bad install can trigger a customer claim under GL, while the same event injures one of your workers and sends a separate loss into workers compensation. If a subcontractor caused the problem and did not carry the right coverage or contract terms, the GC can end up defending a claim that should have been pushed downstream.

Practical rule: If the claim comes from the public, the owner, or another outside party, start with GL. If it involves your employee's injury, start with workers compensation.

Completed operations deserves a hard look too. Liability does not stop when the truck pulls away. A shower pan leak, failed flashing detail, or wiring issue can surface months later, after turnover, when the owner expects you to make it right and their carrier starts asking questions.

That is why GL has to fit the whole operation, not just the certificate you hand over at bid time. A policy with the wrong exclusions, weak completed operations protection, or no attention to how your subs perform can leave expensive holes right in the middle of the system.

Protecting Your Crew Workers Compensation and Commercial Auto

General liability protects the business from outside claims. Workers compensation and commercial auto protect the parts of the operation that contractors put in motion every day. The people and the vehicles.

A roofing contractor can do everything right on a bid and still have a crew member fall from a ladder. An electrical contractor can run clean jobs and still have a van rear-ended on the way to a service call. Those losses don't belong in the same bucket, and trying to stretch one policy to cover another is where a lot of damage gets done.

Workers compensation handles your people

Workers compensation covers employee job injuries. That sounds obvious, but the practical point is bigger than compliance. It creates a defined path for medical care and wage-related benefits after an injury and helps keep that loss from becoming an open-ended liability fight.

For a framing crew, this matters fast. One slip on wet decking, one saw injury, one back strain from material handling, and the business has a serious exposure. Without workers compensation set up correctly, the contractor can face direct financial pressure at the same moment labor is already disrupted.

A lot of contractors also get themselves into trouble by treating everyone as a subcontractor on paper when the work relationship looks like an employee arrangement in the field. Misclassification can create ugly problems at audit time and after claims. If a person works under the contractor's direction, uses the contractor's schedule, and functions like part of the crew, the insurance setup needs to match reality.

Commercial auto handles your road risk

Personal auto insurance and work vehicles don't mix well. If a truck, van, or pickup is being used for business, carries materials, hauls equipment, or sends employees from site to site, the contractor needs commercial auto built for that exposure.

An electrician's van is a good example. It isn't just transportation. It's mobile inventory, rolling signage, and a liability exposure every time it pulls into traffic. If that van causes a major accident, the claim can exceed bare minimum limits quickly. Many states set low minimums, but contractors often choose $1 million in commercial auto liability to match the GL structure, as explained in this breakdown of contractor auto requirements. Contractors sorting through that decision can compare coverage details through commercial auto liability insurance options.

A few practical differences matter:

| Coverage need | Why it matters to a contractor |

|---|---|

| Liability | Pays when the business vehicle causes injury or property damage to others |

| Physical damage | Repairs or replaces the insured vehicle after covered damage |

| Hired and non-owned auto | Helps when employees use rented or personal vehicles for business tasks |

The same source notes that adding another $1 million through an umbrella policy is often the most cost-effective way to increase liability protection, commonly around $300 to $500 annually in many contractor situations. That matters for fleet-heavy trades, but it also matters for one-truck operations that can't survive a severe road claim.

A landscaping company sees this system clearly. The crew can be fully covered for injuries through workers compensation and still have a major gap if the dump truck is insured incorrectly. Protection works only when the pieces line up.

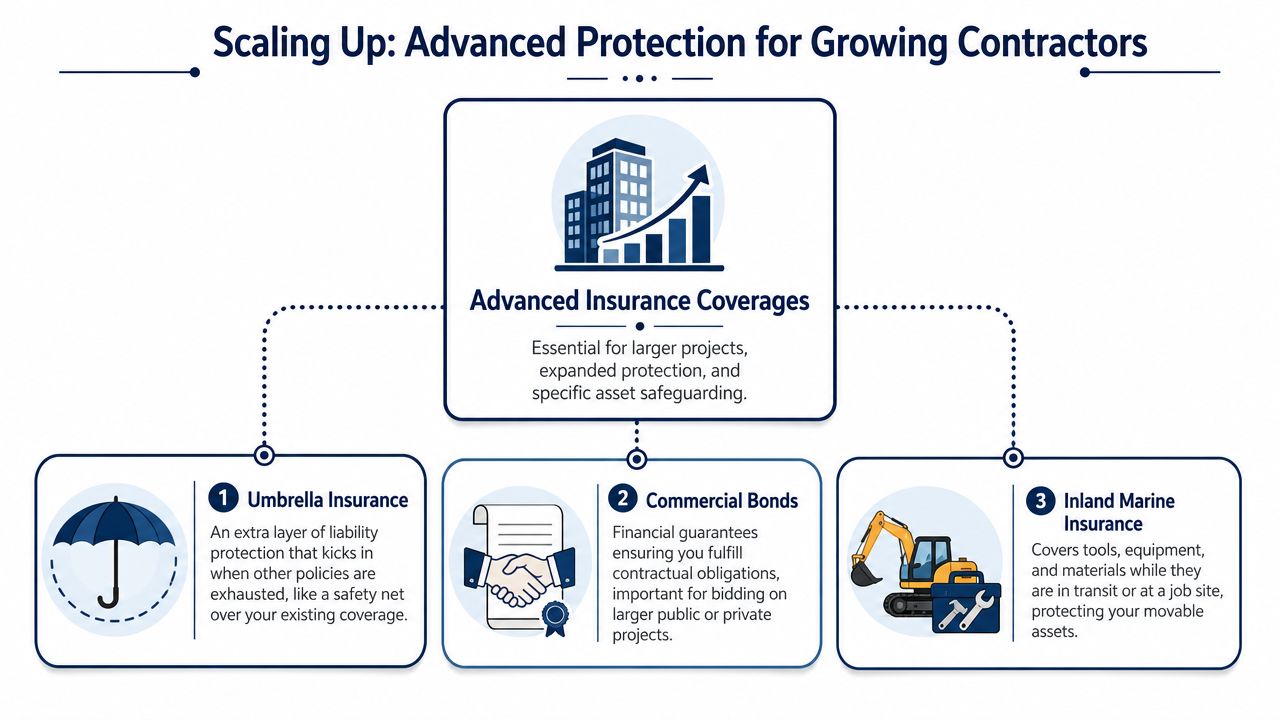

Beyond the Basics Umbrella Bonds and Inland Marine

A crew finishes for the day, then serious trouble starts. A passerby is badly hurt near the site, the owner says your work delayed the opening, and two saws disappear off the trailer overnight. One policy does not solve that pileup. This part of the insurance system exists to catch the losses that fall between basic liability, property, and contract requirements.

Umbrella adds height to the system

Umbrella insurance increases the liability limits sitting above the policies underneath it, usually general liability, commercial auto, and sometimes employers liability. The key point is how the pieces connect. If the underlying policy does not apply, umbrella may not step in either. Contractors get burned when they buy extra limits but leave a hole in the policy below.

That matters on larger jobs, occupied buildings, and any project where one bad incident can pull in multiple injured parties, attorneys, and a demanding owner. Contract requirements often push umbrella limits higher as project size and public exposure increase. Contractors sorting out those higher-limit requirements can review commercial umbrella insurance coverage for contractors.

Here is the trade-off. Umbrella is often one of the cheaper ways to buy more liability limit, but it is not a fix for poor underlying coverage. If your auto policy is missing hired and non-owned auto, or your GL excludes a class of work you are performing, more umbrella limit does not clean that up.

Bigger limits help only when the base policy is built correctly.

Bonds and inland marine solve different gaps

Surety bonds handle a contract promise. Inland marine handles movable property. They belong in the same conversation because contractors often confuse both with insurance for their own balance sheet.

A bond protects the project owner or other obligee if the contractor fails to meet the job terms. Bid bonds help you get in the door. Performance and payment bonds help you keep the job and satisfy the contract after award. If the surety pays, it can seek reimbursement from the contractor. That is a very different deal from an insurance carrier paying a covered claim for accidental loss.

Inland marine covers tools, equipment, and materials that move from yard to truck to trailer to jobsite. That is the property most likely to disappear, get damaged in transit, or sit exposed where a standard property policy may not respond the way a contractor expects. I have seen plenty of contractors find out too late that a theft from a temporary site or a loss while equipment was being hauled was never set up properly under their property coverage.

This is where the system view matters. General liability handles damage you cause to others. Bonds satisfy project obligations. Inland marine protects the gear that keeps revenue moving. Leave one out, and the claim may land in the gap instead of on a policy.

For a concrete contractor, that could mean a required performance bond for the public job, umbrella to satisfy the owner's higher liability limits, and inland marine for lasers, saws, compactors, and forms moving from site to site all week. Different policies. Different triggers. One business protection system.

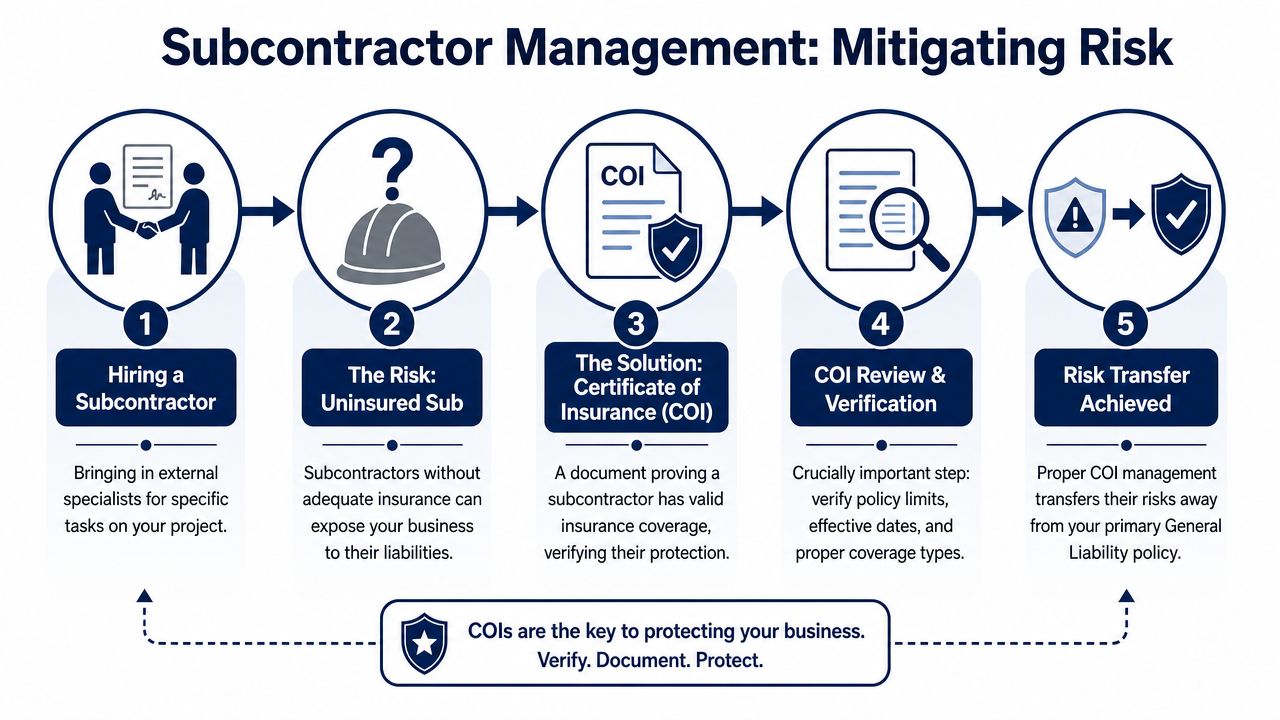

Solving the Subcontractor Puzzle COIs and Risk Transfer

Subcontractors create one of the biggest blind spots in general contractor insurance. Many GCs assume their own GL policy catches whatever goes wrong downstream. It doesn't.

If a subcontractor creates the problem and carries weak coverage, expired coverage, or no coverage at all, the GC can still get pulled into the claim, the cleanup, the legal fight, and the policy audit issues afterward. That's why collecting a certificate of insurance isn't clerical work. It's field-level risk control.

Why a subcontractor can become your problem

Take an HVAC contractor managing a job with a sheet metal sub. If that sub causes a fire during installation and doesn't carry proper coverage, the GC or prime contractor doesn't get to shrug and point at the purchase order. The claim still reaches upstream.

A key industry gap is the mistaken belief that GL covers all subcontractor exposure. It doesn't cover uninsured subcontractor negligence, and that mistake can lead to audit charges and direct claim exposure for the general contractor, as outlined in this discussion of uninsured subcontractor risks. The practical fix is stronger risk transfer through contract language and insurance status, not wishful thinking. Contractors building that process can tighten it through subcontractor insurance requirements and COI review practices.

What to check before the sub starts work

A COI matters, but only if someone reads it and matches it to the contract.

- Named insured: The legal entity on the certificate has to match the company doing the work.

- Effective dates: Coverage must be active for the time the subcontractor is on the project.

- Coverage types: The sub needs the policies the contract requires, not just any policy.

- Limits: The limits must line up with job requirements and the actual risk.

- Additional insured status: This is one of the main tools that pushes the sub's policy into the claim before yours.

- Indemnification language: The subcontract should back up the insurance transfer instead of contradicting it.

Field check: A certificate by itself is evidence, not the coverage grant. The endorsement and the contract language do the heavy lifting.

A masonry GC using independent crews sees this issue all the time. One uninsured labor-only sub can trigger premium disputes, payroll headaches, and uncovered claim questions that were avoidable before the first pallet was delivered. Good subcontractor management isn't busywork. It's part of the insurance system.

What Drives Your Insurance Premiums and How to Control Them

A contractor lands a bigger job, adds two trucks, hires a few more hands, and starts using labor a little differently than last year. Renewal shows up and the premium jumps. The carrier is not reacting to one thing. It is pricing the whole operation as a system. Payroll, vehicles, trade class, claims, subcontractor use, and where the work happens all stack on top of each other.

That is why premium control starts long before renewal. If the insurance file tells the wrong story, the price usually goes up, the audit gets ugly, or a claim exposes a gap nobody priced for.

What moves the price up or down

Trade class is one of the biggest pricing drivers because it affects how underwriters see injury risk, property damage risk, and claim severity. A roofer, a remodeler working in occupied homes, and an interior painter may all call themselves contractors, but they do not bring the same exposure to a policy.

The same goes for how the business is built. A GC with a small direct payroll and heavy subcontractor use gets reviewed differently than a self-performing contractor with a large field crew. One account may lean harder on risk transfer. The other puts more pressure on workers compensation, auto, and day-to-day safety controls.

A few other drivers matter just as much.

| Cost driver | What insurers look at | What contractors can do |

|---|---|---|

| Payroll | Exposure tied to labor, job duties, and workers compensation classes | Keep payroll records clean and split classes correctly |

| Revenue | Size of operations, contract value, and pace of growth | Describe project mix directly instead of relying on rough estimates |

| Claims history | Frequency, severity, and whether losses point to a pattern | Fix repeat problems and document what changed |

| Location | State rules, court climate, and jobsite conditions | Review forms and limits based on where the work is performed |

One mistake I see all the time is treating each policy like its price stands alone. It does not. A bad hiring loss can hit workers compensation. A truck claim pushes auto. A weak subcontractor setup can spill into GL. The account gets more expensive because the carrier sees poor control across the business, not just one bad line item.

A landscaping contractor shows how fast this changes. Start with mowing and maintenance, then add hardscape work, trailers, more drivers, and seasonal labor. The exposure has changed in three directions at once. If the insurance still reads like a small maintenance outfit, the contractor is set up for audit corrections, classification disputes, and hard renewal questions.

How contractors lower costs without gutting coverage

Premium control comes from running a tighter operation and making sure the insurance matches it.

- Build a safety process that leaves a paper trail: Toolbox talks, driver rules, equipment checks, and incident follow-up matter more when they are documented.

- Classify labor correctly from the start: Cleanup labor, carpentry, roofing, and clerical work should not all be dumped into one bucket.

- Keep subcontractor records tight: Missing certificates, bad entity names, and uninsured labor can turn into audit charges and claim fights.

- Report operational changes early: New vehicles, new states, new services, and larger jobs should be discussed before renewal, not after a loss.

- Check how one policy affects the others: A contractor using more employee labor may need to revisit workers compensation, auto, and umbrella together instead of shopping each line in isolation.

Higher deductibles can lower premium, but that only works if the business can absorb smaller losses without wrecking cash flow. Lower limits can reduce cost too, but that decision should line up with contract requirements, job size, and what a serious claim could do to retained earnings. Cheap coverage is easy to buy. Recovering from a claim with the wrong structure is expensive.

Expensive insurance usually points to an operational problem, a reporting problem, or both. Fixing the root issue protects the business better than cutting coverage to make the number look nicer.

Contractors have more control here than they think. Clean books, accurate classifications, fewer preventable losses, and a policy set that matches their actual operation usually lead to better pricing over time. The contractors who get burned are usually the ones whose insurance paperwork lags behind the way they work in the field.

Get the Right Coverage Built for Your Contracting Business

Good general contractor insurance isn't generic. It has to fit the trade, the crew structure, the job size, the vehicles, the equipment, and the contract requirements the business deals with.

A solo handyman doing light repair work doesn't need the same structure as a GC managing multiple subs on commercial renovations. An HVAC contractor with vans and field techs has a different pressure point than a concrete contractor with heavy movable equipment. A remodeler working in occupied homes has a different claim profile than a site contractor working on open ground. The policy set may include similar names, but actual protection depends on how those pieces work together.

That's why “good enough” insurance usually isn't good enough. The cheapest quote may leave out completed operations details, leave a vehicle gap, ignore inland marine, or do nothing meaningful for subcontractor risk transfer. On paper, it looks insured. In a claim, it may fall apart.

The better approach is to review coverage like a contractor reviews a set of plans. Check the assumptions. Look for missing pieces. Make sure the system works together before the job starts.

A coverage review has a strong return because it can protect both sides of the business at once. It helps avoid overpaying for the wrong structure, and it helps avoid underinsuring the exposures that can do real damage. That includes the jobs already on the books and the larger opportunities the business wants next.

Coverage review beats claim regret. Coverage Axis offers free quotes and no-obligation coverage reviews for contractors who want a right-sized insurance program built around their trade, crew size, vehicles, subcontractor setup, and project requirements. Licensed advisors shop multiple A-rated carrier options, explain the gaps in plain English, and help contractors put together coverage that works as a system, not a pile of disconnected policies.