A Texas contractor lands a promising commercial job, reviews the contract packet, and hits the same wall that stops a lot of good operators. The scope looks fine. The schedule is workable. Then the insurance requirements show up, and suddenly the issue isn't construction. It's whether the business can even qualify to start.

That happens every day in Texas. A residential remodeler moves into light commercial work. A Dallas plumbing contractor wants to bid a tenant finish project. An Austin electrician takes a shot at municipal work and finds out a basic policy isn't enough. The job isn't lost because of craftsmanship. It's lost because the coverage doesn't match the contract.

Texas gives contractors a false sense of simplicity. State law doesn't mandate every policy for every contractor, but owners, general contractors, property managers, lenders, and municipalities still set hard insurance requirements. That gap between legal minimums and contract reality is where expensive mistakes happen. Most problems don't start with a total lack of insurance. They start with a policy that looks fine until a bid gets rejected, a COI request can't be met, or a subcontractor injury gets pushed uphill to the general contractor.

Table of Contents

- Why Your Texas Contractor Insurance Matters More Than Ever

- The Four Essential Coverages for Every Texas Contractor

- Advanced Protection to Win Bigger Bids

- How Your Trade and Operations Drive Insurance Premiums

- Navigating Contracts COIs and Additional Insureds

- A Practical Plan to Get the Right Coverage

- Frequently Asked Questions About Texas Contractor Insurance

Why Your Texas Contractor Insurance Matters More Than Ever

A Dallas general contractor can run residential projects for years with a basic setup, then lose a commercial opportunity in one email. The owner asks for a Certificate of Insurance, the contract requires specific liability limits, and the agent on file can't meet the requirement quickly or cleanly. The contractor isn't unqualified to build the project. The paperwork says otherwise.

In Texas, that's common because state law and market requirements aren't the same thing. Texas doesn't require general contractor insurance by state law for all contractors, but the commercial market treats it as standard practice. Most commercial clients want a COI before they sign, and typical general liability requirements are $1 million per occurrence and $2 million aggregate, as outlined in this Texas contractor insurance requirement guide.

A contractor who wants to move past small residential jobs has to understand that difference early. The policy isn't just there to satisfy a lender or check a box. It determines whether the business can bid, sign, mobilize, and stay on a job when something goes wrong.

The real issue isn't the state minimum

Texas is more flexible than many states. That sounds good until a contractor realizes the actual gatekeepers are private contracts and public bid specs.

- Commercial owners set the bar: They often won't sign without proof of active coverage.

- General contractors flow requirements downhill: Subs usually have to match project standards to get onsite.

- Municipal contracts are stricter: The issue isn't just having liability insurance. The issue is having the right form, limits, and endorsements.

For a contractor trying to grow, the better question isn't "What does Texas legally require?" It's "What will this client require before work starts?" That is why many firms review their broader Texas commercial insurance options before they chase larger jobs.

Practical rule: The job often goes to the contractor who can deliver compliant insurance paperwork without delays.

A Houston HVAC contractor is a good example. On a small residential replacement job, insurance may never come up beyond general peace of mind. On a retail buildout, the landlord, tenant, and GC may all want documentation before the first unit is set. The contractor who understands that shift gets access to more work. The one who relies on a generic small business policy often finds out too late that the coverage was built for the wrong kind of project.

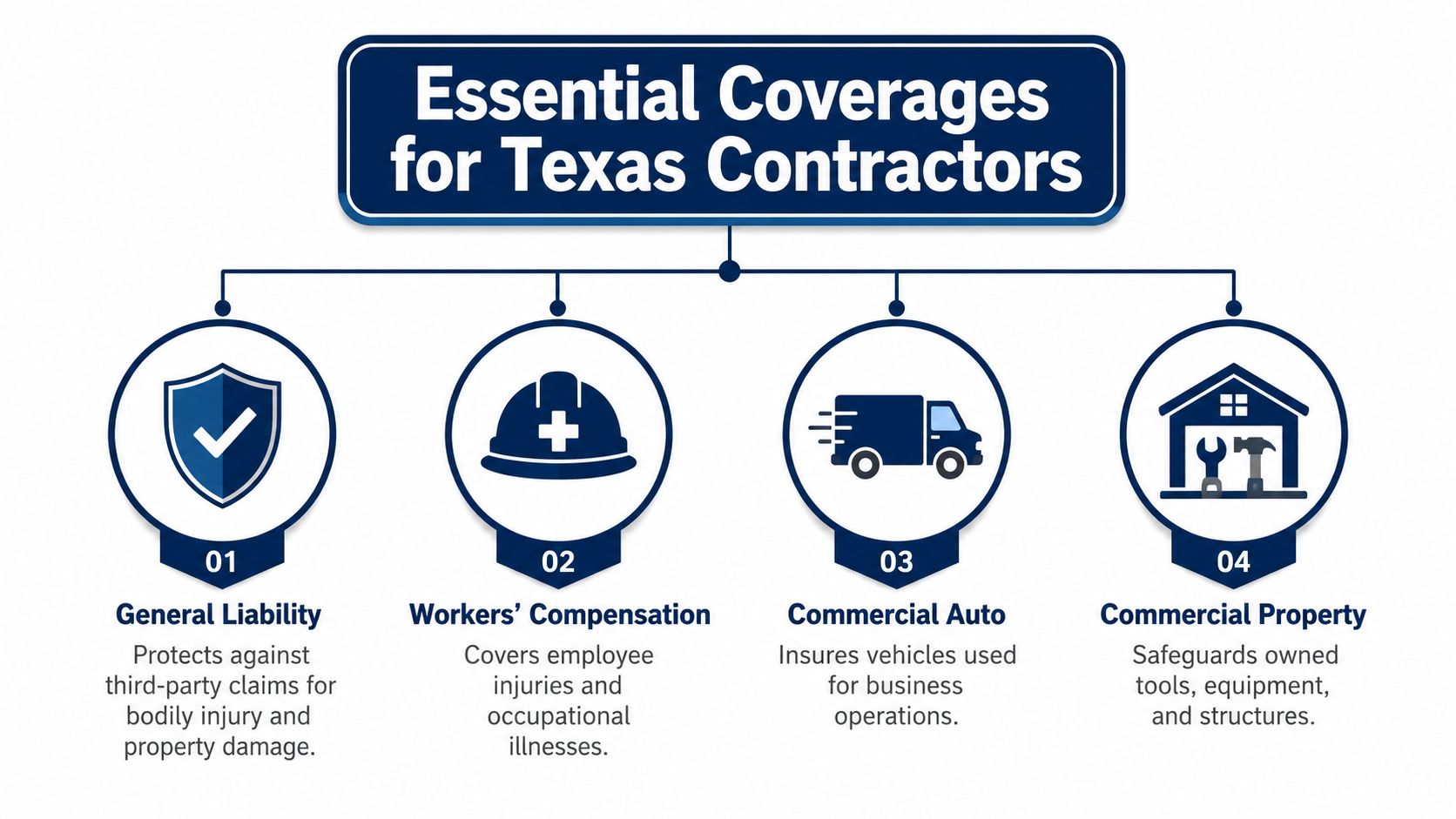

The Four Essential Coverages for Every Texas Contractor

Most Texas contractors don't need every policy on day one. They do need the right foundation. For most trade businesses, that means four core coverages that handle the claims most likely to interrupt cash flow, stall a project, or put personal and business assets at risk.

General liability is the entry ticket

General liability is the shield for third-party bodily injury and property damage claims. If a plumbing contractor cuts into a line and water damages finished space below, this is the policy that usually responds. If a roofer drops material and damages a customer's vehicle, a general liability claim is initiated.

Texas commercial contracts often push contractors toward a standard $1,000,000 per occurrence and $2,000,000 aggregate CGL structure, and many require ISO Form GL 00 01 on an occurrence form, as noted in this Texas commercial contractor insurance requirements reference. Occurrence form matters because it ties coverage to when the incident happened, not when the claim was reported.

A simple way to think about it:

| Coverage | What it protects | Trade example |

|---|---|---|

| General Liability | Other people's property and injury claims | An HVAC installer's condensate drain issue causes water damage after startup |

That baseline matters even more when a contractor starts reviewing what insurance contractors need for different project types, because the right policy form is often just as important as the limit.

The other three policies that keep work moving

Workers' compensation protects the crew when jobsite injuries happen. A concrete laborer can overheat on a summer pour. An electrician can strain a shoulder pulling wire. A carpenter can fall from a short ladder and still miss weeks of work. Workers' comp is about medical care, wage replacement, and keeping one employee injury from turning into a business-threatening event.

Commercial auto covers vehicles used in the business. Personal auto policies are built for personal use, not loaded work vans, trailer pulls, or crews moving between jobs. A service electrician rear-ends another vehicle on the way to a call. A landscaping truck backs into a gate at a commercial property. Those aren't rare claims. They're routine contractor exposures.

Inland marine, often called tools and equipment coverage in contractor conversations, protects mobile property. That includes items that move between the shop, the truck, and the jobsite. A Houston HVAC crew leaves copper coils and diagnostic equipment in a van overnight, and the truck gets hit. A tile contractor's saws disappear from a trailer. A painter's sprayer is stolen from a locked site container. General liability doesn't handle those losses.

A contractor can survive one broken tool. A contractor struggles when a theft or vehicle claim shuts down a crew for a week.

A practical breakdown looks like this:

- Workers' comp: Best for employee injuries from heat, lifting, falls, cuts, and repetitive strain.

- Commercial auto: Best for owned work trucks, vans, and liability from road accidents during business use.

- Inland marine or tools coverage: Best for portable equipment, materials in transit, and jobsite theft exposures.

A San Antonio roofer gives a clean example of why all four matter. General liability handles third-party damage. Workers' comp responds if a crew member gets hurt. Commercial auto covers the dump trailer setup on the road. Inland marine helps replace nail guns, compressors, and other mobile equipment after theft. Miss one layer, and the business has a gap where real claims tend to hit.

Advanced Protection to Win Bigger Bids

The jump from small private jobs to larger commercial or public work usually exposes gaps that basic policies don't address. That's where many Texas contractors get frustrated. They have insurance. They still can't satisfy the contract.

Why bigger jobs expose hidden gaps

Take an Austin electrical contractor bidding municipal work. The firm may already carry general liability and auto. Then the bid package asks for umbrella coverage, a bond, additional insured wording, and endorsements tied to underground work. Without those items, the bid can die before pricing is even considered.

One of the most misunderstood gaps in Texas involves uninsured subcontractors. Texas doesn't universally require workers' comp for private employers, but failing to carry it, or failing to make sure subs carry it, can leave an employer exposed to direct lawsuits because of Action Over issues tied to uninsured sub losses, as discussed in this Texas contractors liability analysis.

That catches general contractors off guard. They assume the sub is responsible for the sub's own crew. On paper that sounds logical. In a lawsuit, it often gets much messier.

If a subcontractor's employee gets hurt and the subcontractor has weak coverage or no coverage, the claim pressure often moves uphill.

Another advanced issue is XCU coverage, which refers to explosion, collapse, and underground exposures. This matters for utility work, trenching, boring, demolition-adjacent operations, and municipal projects where underground damage is a real concern. A contractor can hold a general liability policy and still have a serious problem if the required endorsement isn't there.

What advanced protection actually does

A stronger insurance program for bigger bids often includes more than one moving part:

- Umbrella liability: Adds extra liability capacity above underlying policies. A contractor looking into commercial umbrella insurance usually does so because base limits don't satisfy the contract or don't feel sufficient for larger jobs.

- Surety bonds: These don't work like insurance for the contractor's own claim. They support bid qualification and project obligations, especially on commercial and public work.

- Professional liability: Important when the contractor takes on design-build responsibility, consulting functions, calculations, or advice that goes beyond installation.

- Project-specific endorsements: These can include XCU, broad form contractual liability, completed operations language, and other wording that owners or municipalities require.

An excavation contractor provides the clearest example. If the crew damages an underground line, a generic reading of "we have GL" won't solve the problem if underground work was restricted or the contract required broader wording than the policy covered. The same goes for a design-build HVAC contractor who provides energy calculations and layout recommendations. A property damage claim may point in one direction, while an alleged design error points in another.

This is what separates basic insurability from bid-ready insurability. The contractor who understands that difference can pursue larger work with fewer surprises.

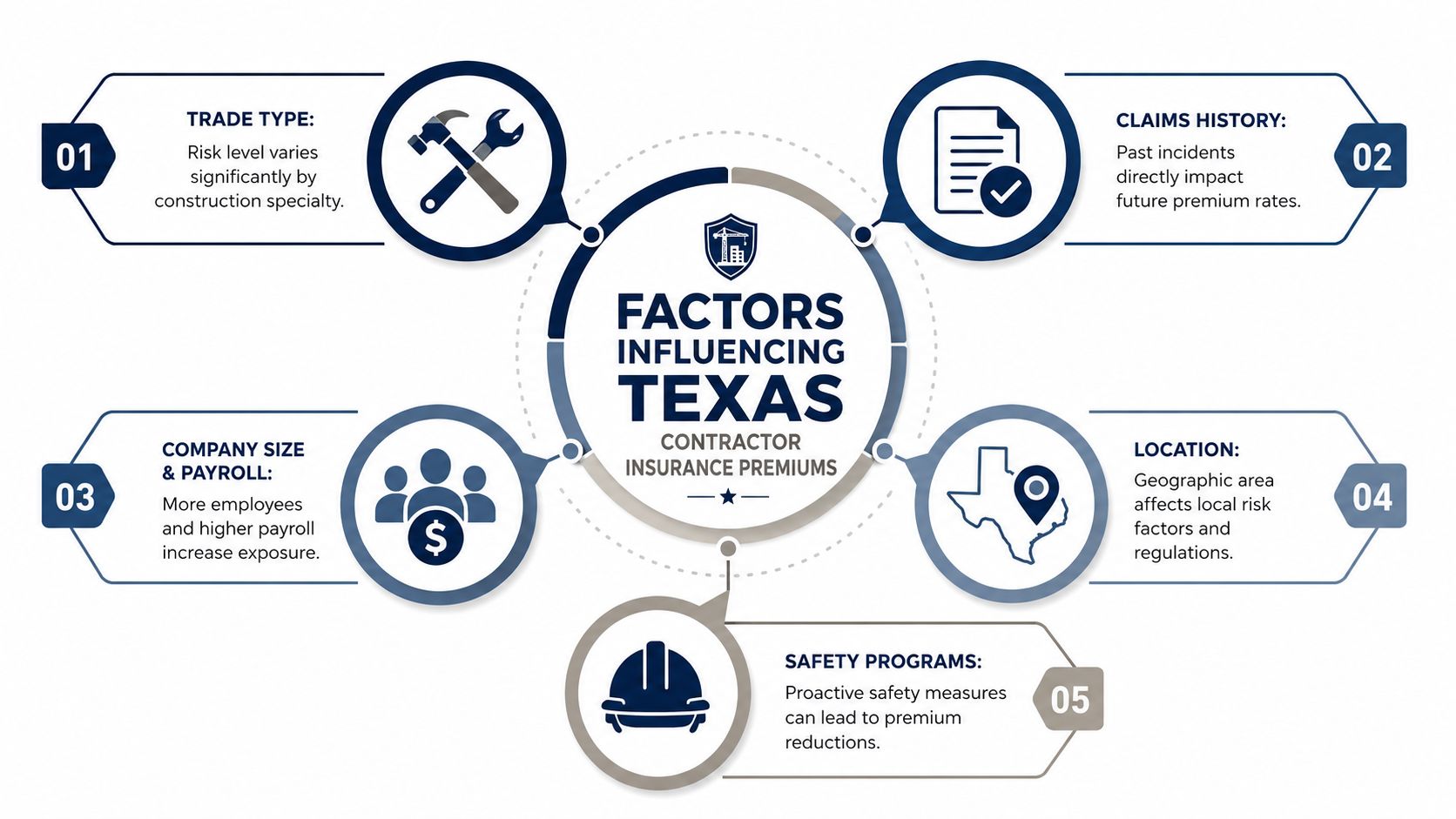

How Your Trade and Operations Drive Insurance Premiums

Insurance pricing in Texas isn't random. Underwriters look at the kind of work being done, who is doing it, where it happens, how many vehicles are on the road, and whether the business has shown good control over losses. Two contractors with the same revenue can pay very different premiums if one installs flooring and the other does roofing or excavation.

What underwriters look at first

Trade type usually hits first. A painter, tile installer, or low-height interior finish contractor often presents a different profile than a roofer, demolition contractor, or utility contractor. The higher the fall exposure, vehicle exposure, underground exposure, or third-party damage potential, the more pressure there is on pricing.

Company size and crew count come next. According to this Texas contractor insurance cost breakdown, a solo operator pays $430 to $780 annually for general liability, while a small contractor with 2 to 5 employees pays $780 to $1,900. That same source notes that commercial auto typically runs $1,500 to $3,000 per vehicle, and performance bonds are priced at 1% to 3% of contract value.

Payroll matters too, especially on workers' comp. The actual class codes assigned to the work can change pricing significantly, which is why contractors often need a clean review of workers' comp codes for their trade operations before they assume a quote is correct.

A quick cost snapshot

Here is a practical view of how pricing tends to move:

| Factor | Why it changes premium | Example |

|---|---|---|

| Trade | Riskier operations cost more to insure | A roofer usually prices differently than a painter |

| Crew size | More workers mean more injury exposure | A three-person framing crew isn't rated like a solo handyman |

| Vehicles | Every work truck adds road exposure | A fleet plumber pays differently than a one-van operator |

| Project type | Commercial and public jobs often raise requirements | Tenant improvement work can require broader insurance than residential repair |

| Loss history | Prior claims affect future pricing and appetite | Frequent auto losses can push rates up or narrow options |

Regional differences also matter. A contractor working in dense metro areas may see different pricing pressure than one in a smaller county. Dallas is a good example. A plumbing contractor working Dallas commercial service routes, tight parking areas, and larger contract requirements doesn't present the same exposure profile as a rural plumber doing mostly small residential calls.

Another source focused on contractor liability pricing notes that most small Texas contractors pay between $1,000 and $5,000 annually for general liability, higher-risk trades can exceed that, and Dallas-area contractors often pay about 10% to 15% more than the statewide average due to urban density, litigation pressure, and larger contract demands in that market, as described in this Texas contractor liability cost overview.

Underwriting view: Insurers don't just price the trade. They price the way that trade actually operates.

That distinction matters. An electrician doing mostly occupied commercial remodels with multiple vans and after-hours service calls can price differently than an electrician doing lighter residential work, even under the same license classification.

Navigating Contracts COIs and Additional Insureds

A lot of insurance problems show up in paperwork before they ever show up in a claim. That's why contractors need to understand certificates, endorsements, and contract wording well enough to catch issues before mobilization.

What a COI does and does not do

A Certificate of Insurance, or COI, is proof that coverage exists on the date the certificate is issued. It is not the policy itself. It works a lot like an insurance ID card for a business. A commercial property manager hiring a landscaping contractor may ask for a COI before gate access is approved or before the first maintenance visit is scheduled.

That document matters because it shows key facts quickly:

- Named insured: Confirms the legal business name on the policy

- Coverage types: Shows whether GL, auto, workers' comp, and other lines are active

- Policy dates: Helps the hiring party confirm coverage is current

- Limits shown: Gives the client a quick view of whether the contract standard appears to be met

A COI should never be treated as the full answer. If the contract requires endorsements, waiver wording, or completed operations language, the certificate alone doesn't guarantee those details are in place.

Why additional insured status and completed operations matter

Texas general contractors routinely require subcontractors to carry general liability and name the GC as an additional insured. Many contracts also require completed operations coverage for at least two years after project completion, according to this contractor insurance guideline resource.

That requirement is practical, not bureaucratic. A roofing subcontractor can finish a job, leave the site, and still face a later claim tied to water intrusion or property damage that appears after the project is complete. If completed operations coverage isn't maintained long enough, the problem may hit after the contractor assumed the exposure had ended.

A subcontractor agreement should be reviewed with the same care as the policy. If a GC requires additional insured status, the subcontractor needs the correct endorsement support, not just a certificate note. Consequently, understanding additional insured endorsements becomes critical for both GCs and subs.

The safest paperwork habit is simple. Match the contract to the policy, then match the policy to the certificate.

A practical field example makes the point. A Dallas roofing subcontractor gets approved on a commercial project only after delivering a COI that reflects the required liability setup and shows the GC as additional insured. Without that step, the roofer may have the labor, crew, and equipment ready, but still can't step onto the site.

A Practical Plan to Get the Right Coverage

The most effective insurance buying process is simple, but it can't be rushed. Contractors who get better results usually do three things before they ask for quotes.

First, gather the operating details that affect underwriting. That includes payroll, estimated revenue, vehicle schedules, driver information, subcontractor use, project types, and the states or cities where work happens. A framing contractor that does new residential tracts presents a different profile than a remodeler doing occupied interior work. The quote only gets accurate when the operation is described accurately.

Second, work with an advisor who understands contractor risk. Generic small business placement often misses the details that matter most in construction. That includes classification, endorsements, subcontractor controls, and how contract requirements flow into policy structure. Cheap pricing can look attractive right up until a bid requirement, exclusion, or claims dispute exposes what was left out.

Third, compare quotes as insurance programs, not just price tags.

A strong review should include:

- Policy form and exclusions. Check whether the coverage fits the specific trade and project type.

- Endorsements required by contract. Confirm that additional insured wording, completed operations language, and any project-specific requirements are properly addressed.

- Carrier fit for construction claims. The issue isn't just premium. It's whether the carrier handles contractor losses well.

- Service speed. If the business needs COIs, revised certificates, or quick binding, slow service becomes a real operating problem.

The cheapest quote is often the most expensive one after a loss or a rejected contract packet. Texas contractor insurance works best when it is built around how the company bids, staffs, drives, and subcontracts. If the coverage doesn't match the operation, it won't perform when the pressure is on.

Frequently Asked Questions About Texas Contractor Insurance

Does a solo operator really need this coverage

Often, yes. A solo operator may have no employees and still need general liability, commercial auto, tools coverage, or a bond because the client or property manager requires it. Even when a contract doesn't force insurance, the business still carries liability for damage, injuries, and vehicle accidents tied to its work.

A solo tile installer is a good example. One cracked water line or one trip-and-fall claim at a customer's property can become a serious financial problem without the right coverage in place.

How fast can a contractor get a COI for a bid

Turnaround depends on whether the policy is already active and whether the request is simple or contract-specific. Straightforward certificates can often move quickly. Requests involving custom wording, additional insured language, or contract review usually take more coordination.

The important point is this. Contractors shouldn't wait until bid day to discover the policy can't support the request.

What happens if a subcontractor without insurance gets hurt

That can become very expensive for the hiring contractor, especially if the subcontractor's own coverage is missing or weak. The issue isn't just the injury itself. The issue is who gets pulled into the lawsuit and whether the upstream contractor has protected against that exposure contractually and through insurance.

A small GC hiring an uninsured drywall sub for a fast commercial finish-out might think the risk sits with the sub. It often doesn't stay there.

Is general liability enough for most contractors

Not if the business has vehicles, employees, mobile tools, or subcontracted labor. General liability is a core policy, but it doesn't replace workers' comp, commercial auto, inland marine, umbrella, or bond needs when those exposures exist.

What should a contractor review before signing a project contract

At minimum, the contractor should review required limits, additional insured language, completed operations requirements, auto and workers' comp expectations, and any special endorsements tied to the work. Underground work, design responsibility, public projects, and subcontracted labor all deserve extra attention.

Coverage Axis helps contractors build insurance programs that fit the work they perform. Whether the need is a free quote, a COI-ready policy setup, or a full coverage review for larger bids, Coverage Axis can help evaluate gaps, compare options, and put practical protection in place.