A contractor opens a bid package for a solid commercial job. The scope fits the crew, the schedule is workable, and the revenue would move the business up a tier. Then one line stops everything: must be bonded.

That moment is common for electricians, plumbers, roofers, and general contractors trying to win better work. The phrase sounds simple, but for many owners it raises immediate questions about cost, paperwork, and risk. Beyond these, it raises a practical question. What does bonded mean for a business when real jobs, real cash flow, and real client expectations are on the line?

For contractors, bonding isn't just legal language. It's often the difference between staying in the small-job lane and qualifying for larger, more professional work.

Table of Contents

- What Being Bonded Means on a Bid Sheet

- Surety Bonds vs Insurance A Clear Comparison

- The Four Main Bonds Every Contractor Should Know

- Why Clients and States Require You to Be Bonded

- How Much Contractor Bonds Cost and What Affects Your Rate

- How to Get Bonded A Step-by-Step Guide for Contractors

- What Happens If There Is a Claim

What Being Bonded Means on a Bid Sheet

A bid sheet doesn't care whether a contractor is confused by insurance language. It merely states the requirement and moves on. For a growing trade business, that line usually means the client, project owner, or public entity wants financial backing behind the contractor's promise to perform.

Being bonded means a business has secured a surety bond, creating a legally binding three-party agreement between the Principal (the business), the Obligee (the client or government entity), and the Surety (the bonding company) that guarantees the Principal will fulfill contractual obligations; if the Principal fails, the Surety compensates the Obligee but legally obligates the Principal to reimburse the full claim amount, as explained in this legal definition of being bonded.

For contractors, that's the plain-English version. A bond tells the client, “This company isn't just making promises. A surety has reviewed the business and is willing to stand behind that promise.”

A commercial electrician sees this often on tenant improvement work. The job may require a bond before the owner will even treat the bid as responsive. Without it, the contractor might have the right labor capacity, pricing, and schedule, but still lose before the bid is really considered.

Practical rule: On larger jobs, “bonded” isn't a decoration on the company profile. It's part of the qualification package.

That matters because bonding changes how a contractor is perceived. It signals structure, financial discipline, and readiness for more demanding contracts. It also opens up job opportunities that aren't available to firms operating only with a license and a basic insurance package.

For owners who want a deeper explanation of the bond categories they may run into, this guide to business insurance bonds gives helpful background. Contractors sorting out project-specific requirements can also compare bid bond vs performance bond so they don't assume every bond does the same job.

Why it feels like a milestone

A plumbing contractor taking on small residential service calls may not think about bonding much. Then a school renovation, municipal utility job, or larger private build lands on the radar. The business is now playing in a different arena, and the paperwork reflects it.

That doesn't make bonding a burden by itself. In practice, it often marks the point where a contractor starts operating like a larger, more professional business.

Surety Bonds vs Insurance A Clear Comparison

Contractors mix these up all the time, and the confusion causes bad decisions. A business owner may think being bonded means the same thing as being insured. It doesn't.

The cleanest way to separate them is this. Insurance protects the contractor. A surety bond protects the client or project owner.

The easiest way to think about it

Insurance works like a shield. If a plumbing crew accidentally floods a mechanical room during a repipe, the contractor's liability policy is designed to respond to covered property damage.

A surety bond works more like a co-signed obligation. If that same plumbing contractor signs a contract and then walks off the job or fails to meet the required standard, the bond can protect the client from that failure. But the contractor remains financially responsible to the surety if the surety pays.

Unlike insurance, which protects the business itself from unforeseen events like accidents or property damage, a surety bond specifically protects the third-party client from financial loss due to non-compliance, misconduct, or employee theft. If a surety bond company pays a claim on behalf of the principal, the business is legally required to reimburse the surety company for that payment, according to Investopedia's explanation of what bonded means.

A bond isn't there to absorb a contractor's loss the way insurance does. It's there to guarantee the contractor's obligation to someone else.

That distinction matters on real jobs. If an HVAC installer damages a finished floor while moving equipment, that's an insurance issue. If the contractor fails to complete the installation under the signed contract, that moves into bond territory if the project requires one.

For owners trying to sort through the overlap in terminology, this outside resource on how to get surety bond insurance can help frame the conversation, and this overview of bond insurance for small business is useful when a contractor is still deciding what needs a bond and what needs a policy.

Surety Bond vs Liability Insurance at a Glance

| Feature | Surety Bond | Liability Insurance |

|---|---|---|

| Who is protected | The obligee or client | The business named on the policy |

| Purpose | Guarantees contract performance or compliance | Covers covered losses such as property damage or bodily injury |

| Parties involved | Principal, obligee, surety | Insurer and insured |

| If a claim is paid | The contractor typically must reimburse the surety | The business doesn't repay the insurer for a covered claim |

| Typical jobsite example | Contractor fails to complete agreed work | Crew accidentally causes damage during operations |

Where contractors get burned

Problems usually start when a contractor thinks one product replaces the other. It doesn't. A bond won't handle accidental jobsite damage, and liability insurance won't guarantee contract completion.

That gap shows up fast on larger jobs. The contractor who understands both products tends to bid cleaner, negotiate better, and avoid ugly surprises after signing.

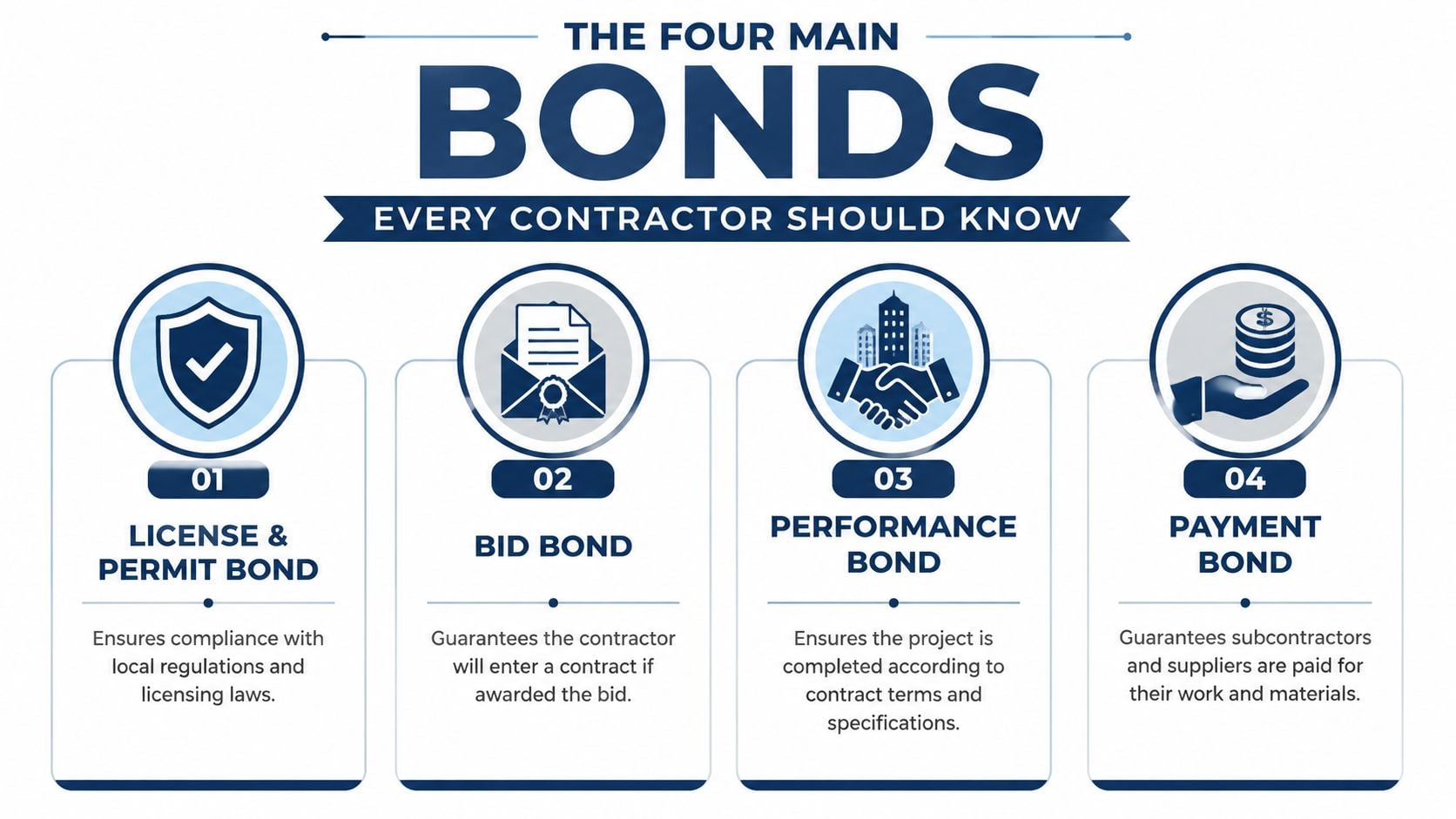

The Four Main Bonds Every Contractor Should Know

Most trade business owners don't need a long list of bond terminology. They need to know which bond applies to which situation and why the requirement shows up.

License and permit bonds

This is often the first bond a contractor encounters. A license and permit bond is usually tied to legal operation in a state, city, or local jurisdiction.

An electrician is a simple example. The business may need this bond before it can hold or renew a contractor license. The bond supports compliance with licensing rules and local regulations. It doesn't protect the electrician's tools, vans, or crew. It supports the public or regulating authority.

What works:

- Checking local rules early: Some contractors wait until license renewal week and then scramble.

- Treating it like part of startup cost: For newer contractors, this belongs in the licensing checklist, not the emergency list.

What doesn't:

- Assuming one bond covers every city: Requirements can vary by jurisdiction.

- Confusing it with general liability: They solve different problems.

Bid bonds

A bid bond shows the project owner that the contractor is bidding in good faith. It tells the owner the bidder is prepared to enter the contract if awarded the job under the stated terms.

A commercial landscaping company bidding on a city park project may need one before the municipality will accept the proposal. Without the bond, the number on the page may never matter.

Owners use bid bonds to weed out contractors who price aggressively but aren't prepared to sign and perform.

A bid bond is less about construction quality at that stage and more about seriousness, credibility, and follow-through.

Performance bonds

A performance bond is tied to finishing the job according to the contract. This is the bond many contractors think of first because it sits closest to the day-to-day risk of default.

Take a general contractor building a commercial addition. The owner wants assurance that the project will be completed as agreed if the contractor can't finish. That's where the performance bond comes into play.

This isn't just abstract legal language. If a contractor overextends, loses labor, mismanages cash, or otherwise can't deliver, the owner wants a financial backstop in place.

Payment bonds

Payment bonds protect subcontractors and suppliers by guaranteeing they get paid under the project terms.

A large roofing contractor is a good example. If that roofer takes on a substantial commercial project, the owner may want assurance that material suppliers and lower-tier trades won't go unpaid and create downstream problems.

That matters because unpaid subs and suppliers can disrupt jobs fast. Material holds, collection pressure, and reputation damage can spread well beyond one project.

A quick way to match bond to job

- License and permit bond: Needed to operate legally in certain jurisdictions

- Bid bond: Needed to submit a qualified bid on some projects

- Performance bond: Needed to guarantee completion of the contracted work

- Payment bond: Needed to assure subs and suppliers are paid

A contractor doesn't need all four on every project. But once the business starts crossing into public work, larger private contracts, or stricter licensing environments, these bonds stop being theory and become operating requirements.

Why Clients and States Require You to Be Bonded

Bond requirements make more sense when viewed from the other side of the table. The owner, municipality, school district, or general contractor isn't asking for a bond to create paperwork. They're trying to control risk before a problem starts.

Public work and licensing rules

In many cases, the requirement is built into law or licensing rules. Surety bonds are often a mandatory precondition for obtaining a contractor's license in most states and many local governments, and they are frequently required before a contractor can bid on public or private construction projects, making bonding not just a trust signal but a legal and operational necessity, as outlined by Surety Bonds Direct on licensed, bonded, and insured contractors.

A school district hiring for a new building or major renovation is a good example. The district has to protect public money, project deadlines, and the practical reality that the building needs to open on schedule. If the contractor fails, the district needs recourse.

A state licensing board sees it differently but reaches the same answer. It wants contractors operating under its rules to meet minimum financial accountability standards. That's one reason many licensing frameworks tie bond requirements directly to legal operation.

For contractors reviewing broader insurance obligations on larger projects, this summary of general contractor insurance requirements helps put bonds in the larger compliance picture.

Private clients want proof of reliability

Private owners and upstream contractors often use bonding as a screening tool. They want evidence that the subcontractor or prime contractor has enough financial stability and operating discipline to handle the job.

A commercial developer doesn't want to discover halfway through the build that the framing contractor underbid the project, can't fund payroll, and is already behind with suppliers. Requiring a bond helps filter out some of that risk before the contract is signed.

Bondability often says as much about a contractor's financial housekeeping as it does about the project itself.

That's why bonding matters beyond compliance. It becomes part of how serious clients judge whether a contractor is ready for bigger work.

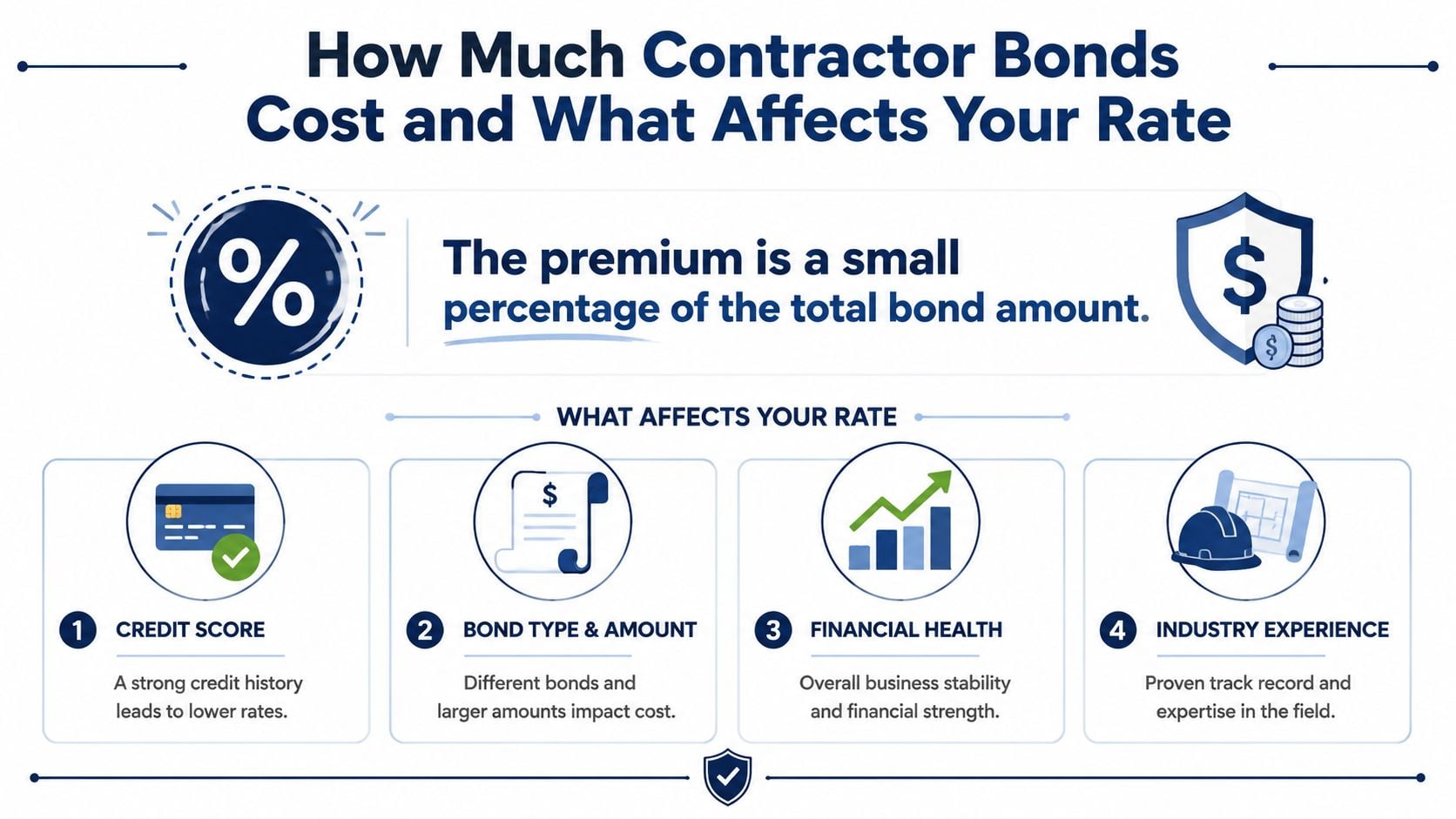

How Much Contractor Bonds Cost and What Affects Your Rate

This is the question contractors ask right after they learn they need a bond. The answer starts with one point. The premium is usually a percentage of the total bond amount, not the full amount itself.

According to Embroker's explanation of licensed, bonded, and insured businesses, surety bonds function more like loans than insurance policies, with premiums primarily determined by the business's credit score and financial health; businesses with strong credit (typically FICO 700+) pay 1–5% of the bond amount, while those with poor credit (below 600) may face rates up to 20%.

What underwriters are looking at

In contractor terms, underwriters usually care about three practical issues:

- Capital: Can the business support the work financially?

- Character: Does the owner have a solid reputation, clean history, and responsible track record?

- Capacity: Can the crew, management team, and systems complete the job?

A restoration contractor bidding a $200,000 project sees this firsthand. The bond cost won't be based only on the project size. The surety will care about the firm's financial statements, credit profile, and whether the contractor has successfully handled similar work before.

What helps and what hurts

Strong submissions tend to include:

- Clean financial records: Current statements make underwriters more comfortable.

- Good personal and business credit: Better credit usually means better pricing.

- Relevant project history: A contractor stepping gradually into larger jobs looks more stable than one making a sudden leap.

Common problems include:

- Messy bookkeeping: If the numbers don't tell a clear story, the surety gets cautious.

- Thin working capital: A contractor may be skilled in the field but still look weak on paper.

- Taking too large a jump: A small plumbing company chasing a much larger municipal contract may get more pushback than expected.

Contractors preparing for first-time or larger bond submissions should review contractor bonding requirements before the bid deadline arrives. That avoids a common mistake. Waiting until the contract is ready to sign.

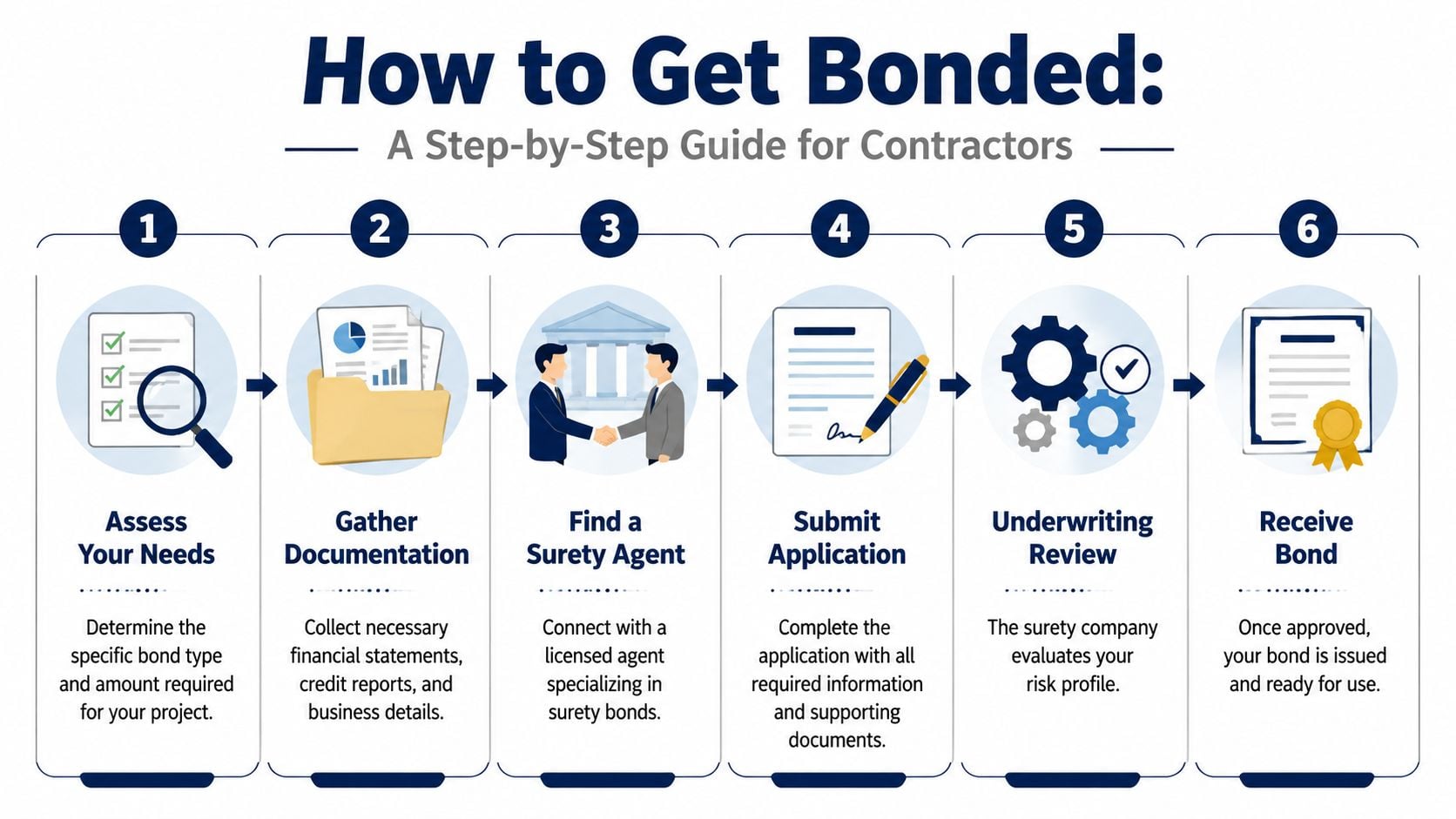

How to Get Bonded A Step-by-Step Guide for Contractors

For most contractors, getting bonded feels complicated only until the process is broken into pieces. In practice, it follows a fairly direct path.

Step 1 through Step 3

Assess the requirement

Start with the exact bond type and amount required. A bid bond requirement calls for a different response than a license bond or a performance bond.Gather documents

Contractors usually need business details, project information, and financial records. A larger bond request may also require more detailed financial support.Work with a surety-focused advisor

The process gets easier when someone can match the risk to the right surety market and explain what underwriters want to see. Contractors who need a broader overview can review how to get bonded and insured before starting the application process.

Step 4 through Step 6

Complete the application

Accuracy matters here. A rushed application with incomplete information slows everything down and can create underwriting questions that didn't need to exist.Go through underwriting review

The surety reviews the business, the owners, and sometimes the job itself. A plumbing contractor applying for a modest license bond may move through quickly. A general contractor pursuing a larger performance bond should expect closer review.Sign indemnity and pay the premium

This is the part many contractors don't fully appreciate the first time. The indemnity agreement matters because it confirms the contractor's repayment obligation if the surety pays a valid claim.

The smoothest bonding process usually starts before the bid date, not after the owner asks for documents at the last minute.

A few habits make the process cleaner:

- Keep financial statements current

- Know the exact obligee name and bond wording required

- Ask early if personal indemnity will be required

- Don't hide credit issues that underwriting will find anyway

A small HVAC business applying for a bond for the first time doesn't need perfect paperwork. It does need organized paperwork. That's usually the difference between a manageable process and a frustrating one.

What Happens If There Is a Claim

Bond claims are serious because they test both the contract and the contractor's financial responsibility. When an obligee believes the contractor failed to meet the bonded obligation, the obligee files a claim with the surety.

How a claim usually plays out

The surety investigates. If the claim doesn't fit the bond or the facts don't support it, the surety can deny it. If the claim is valid, the surety may pay the obligee up to the bond limit and then pursue reimbursement from the contractor under the indemnity agreement already signed.

That repayment piece is why contractors need to think of bonding as a financial obligation, not a safety net for their own business.

A concrete example helps. A subcontractor abandons a portion of the contracted work and leaves the project incomplete. That can fit the kind of performance failure a bond is designed to address.

What a bond does not cover

Contractors often confuse bonding with insurance. Existing content conflates bonds with insurance, but bonds only cover performance failure (e.g., unfinished work), not accidental damage or employee fraud unless a specific fidelity bond is purchased. Data confirms contractor general liability covers accidental ruptures (e.g., gas lines), but bonds cover abandonment or subpar standards, according to Next Insurance on understanding bonded and insured.

If a plumber's crew accidentally ruptures a line and damages property, that's a liability issue. If the plumber stops work and fails to fulfill the contract, that can become a bond issue.

Contractors that stay organized, document change orders, and manage subcontractors tightly are less likely to end up in a bond claim dispute.

The practical takeaway is simple. Bonding supports growth, but it also rewards discipline. The contractors who use it well usually price jobs carefully, watch cash flow, document their work, and avoid taking on projects their team can't carry.

Contractors who need help sorting out bond requirements, insurance gaps, or job-specific coverage can get a free quote or coverage review from Coverage Axis. The process is built for trade businesses that need plain-English guidance, fast answers, and coverage that fits the work.