A contractor finds a solid project, lines up pricing, checks the scope, and then hits the line that changes everything: must be bonded and insured. That's usually where the confusion starts. Insurance is familiar. Bonding feels like paperwork, underwriting, and one more hurdle standing between the business and a good contract.

For small contractors, that hurdle often decides who gets to bid, who gets approved, and who gets paid without delays. A bond can be the difference between staying on small private jobs and stepping into municipal work, larger commercial contracts, and clients who won't release a notice to proceed until every compliance item is in place. Bond insurance for small business matters because it isn't just about checking a box. It affects access to work.

The part many owners miss is this: insurance and surety bonds don't do the same job. Insurance is built to protect the business from covered losses. A surety bond is built to protect the customer, project owner, or government entity that requires it. That distinction drives almost every problem contractors run into later, especially when a claim, a payment dispute, or a contract default lands on the desk.

Table of Contents

- Why Being Bonded Unlocks Better Contracting Jobs

- What a Surety Bond Is and What It Is Not

- The Main Types of Bonds Your Business Might Need

- How Underwriters Assess Your Bonding Capacity

- Understanding the Costs of Bond Insurance

- Your Step-by-Step Process to Get Bonded

- Common Pitfalls and Your Next Steps

Why Being Bonded Unlocks Better Contracting Jobs

You line up a solid bid. The numbers work, the crew is available, and the job fits your experience. Then the bid package says the contractor must be bonded and insured. If the bond is missing, the owner may reject the bid before anyone even looks at your schedule or price.

That is why being bonded gives a small contractor access to better work. Public jobs, larger private projects, and contracts with strict lender oversight often treat bonding as a screening tool. Owners use it to narrow the field to firms that have already passed a financial and operational review by a surety.

For small businesses, that matters more than many contractors realize. The SBA's Surety Bond Guarantee Program applies to contracts up to stated size limits for eligible small businesses, as outlined in the agency's Surety Bond Guarantee Program details. The practical takeaway is simple. Bonding is not reserved for large regional firms with deep balance sheets. Smaller contractors can qualify too, and getting that approval can put you in the running for jobs that would otherwise be off limits.

Why owners ask for both

Owners ask for insurance and bonds because they solve different problems, and mixing them up causes expensive mistakes.

- Insurance protects your business: It can respond to covered accidents, injuries, vehicle losses, and property damage.

- A bond protects the owner or obligee: It guarantees that you will meet the contract terms or other legal obligations.

- You still carry the financial risk on the bond: If the surety pays a valid claim, it usually has the right to seek repayment from you under the indemnity agreement.

That last point is the one contractors miss.

A bond can help you qualify for the job, but it does not shift your performance risk the way general liability or workers' comp shifts certain covered losses. If you default, abandon the project, or fail to pay certain subs or suppliers when the bond covers that obligation, the surety may step in for the owner first and then come back to you for reimbursement. From the contractor's side, that means bonding helps you get the contract, but it does not erase the cost of poor job execution.

A plumbing contractor bidding a municipal restroom upgrade sees this in real life. The city may require general liability, workers' compensation, commercial auto, and a contract bond. Miss the insurance documents and you have a compliance problem. Miss the bond and you may lose the award entirely. Contractors reviewing broader general contractor insurance requirements by project type usually find both items sitting on the same pre-award checklist, even though they serve different purposes.

The contract language matters here too. Scope, payment terms, delay clauses, and default provisions can all affect whether a bond requirement becomes a real payment problem later, which is why it helps to review practical contract breakdowns like SheetMergy insights on contracts before signing.

Practical rule: If a project says bonded and insured, treat that as two separate approvals with two separate consequences if you get them wrong.

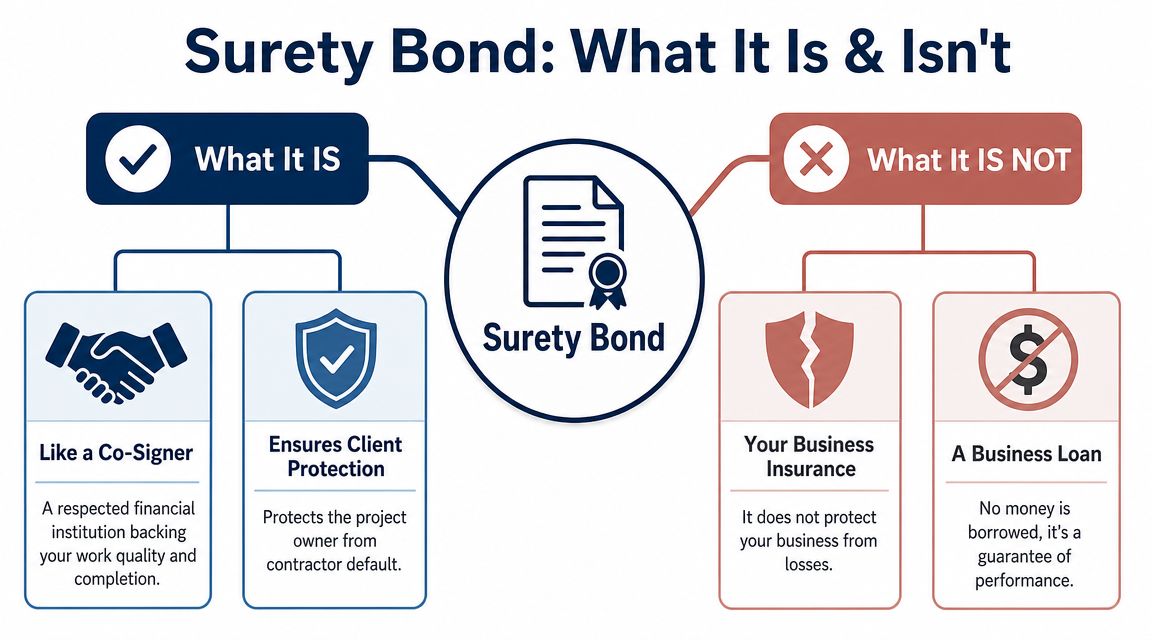

What a Surety Bond Is and What It Is Not

A surety bond isn't business insurance dressed up with a different name. It's closer to a financial guarantee. A useful way to explain it to a contractor is this: the surety is acting like a co-signer for the contractor's obligation. The owner or obligee gets comfort that if the contractor doesn't meet the terms, the surety stands behind that promise.

The central misunderstanding is what happens after a claim. A small-business surety bond is a three-party credit instrument, not traditional insurance. The surety guarantees the obligee that the principal will perform, and if the surety pays a claim, the principal must reimburse the surety under an indemnity agreement, as explained in The Hartford's overview of small business bond insurance. That's why weak credit, poor financial statements, or thin business capacity can stop a bond approval even when the contractor can still buy standard insurance.

The three parties on every bond

Every surety bond involves three players:

- Principal: The contractor or business that must meet the obligation.

- Obligee: The customer, government entity, or project owner requiring the bond.

- Surety: The company issuing the guarantee.

That structure changes how a contractor should think about risk. With general liability insurance, the policy is there to protect the insured business from covered claims. With a bond, the contractor is still on the hook if the surety has to step in.

Good contract reading matters here. Scope, deadlines, retainage terms, change-order language, and default triggers can all affect bond exposure. Contractors that want a plain-language refresher on contract fundamentals can review SheetMergy insights on contracts, especially when they're signing owner-drafted forms that shift more risk downstream.

Roofing example that makes the difference clear

Take a roofing contractor on a commercial reroof.

If a crew accidentally damages the building façade while loading tear-off debris, general liability may respond if the claim fits the policy. That's an insurance problem. If the contractor abandons the project, misses the completion obligation, or can't finish according to the signed contract, a performance bond addresses the owner's concern. That's a surety problem.

A bond doesn't replace GL, workers' comp, or auto coverage. It also doesn't erase the contractor's financial responsibility if the surety pays.

That's where many owners get surprised. They think being bonded means the loss has been transferred away from the business. It hasn't. Contractors sorting through that distinction can see how owners and hiring parties often use the term in what bonded means for a job, but the short version is simple: insurance protects the business, while the bond protects the party requiring the bond.

The Main Types of Bonds Your Business Might Need

Contractors usually don't need “a bond” in the abstract. They need the right bond for the right reason. That's where confusion starts, especially when an owner, city, or project manual just says bonding is required without spelling out what kind. A plain-language breakdown matters because many public and private contracts require surety bonds, and guidance is often weak on whether the contractor needs a license and permit bond, bid bond, performance bond, or payment bond. That same need for clarity shows up in surety bond guidance for small businesses.

Contractor bond types at a glance

| Bond Type | What It Guarantees | Typical Scenario |

|---|---|---|

| License and Permit Bond | The contractor will follow licensing rules or permit requirements | An HVAC contractor registering in a new city before pulling permits |

| Bid Bond | The bidder will accept the contract and provide required follow-up bonds if awarded the job | A general contractor submitting a bid on a public school project |

| Performance Bond | The contractor will complete the work according to the contract | A concrete contractor hired to build foundations on a commercial site |

| Payment Bond | The contractor will pay subs, suppliers, and certain labor costs as required | A general contractor using multiple subcontractors and material vendors on a bonded job |

How each bond shows up on real jobs

License and permit bonds usually come first for small trade businesses. An electrician entering a new municipality may be fully competent, fully insured, and still unable to pull permits until the local authority receives the required bond. This bond doesn't protect the electrician's business. It protects the city or public body expecting compliance with code and licensing rules.

Bid bonds matter at the estimating stage. A paving contractor can spend days building a sharp proposal, only to find the owner wants a bid bond included with the bid package. The point isn't project completion yet. The point is proving the contractor is serious and financially able to move forward if awarded the work.

Performance bonds show up after award and before work starts. A drywall contractor on a large tenant improvement might hear the owner say, “No notice to proceed until the performance bond is approved.” That owner wants assurance that if the contractor defaults, there's a mechanism behind the obligation.

Payment bonds protect the upstream party from lien and nonpayment problems. A general contractor managing electrical, plumbing, framing, and finish trades may need a payment bond to show the owner that subs and suppliers won't be left unpaid if the job gets messy.

A lot of contractors ask which matters more, bid or performance. The answer is usually “both, at different points.” Bid bonds get the contractor through the front gate. Performance and payment bonds matter after award. Contractors trying to sort out those stages usually benefit from a practical comparison of bid bond versus performance bond in construction.

The wrong bond can be as useless as no bond at all. Contractors need to match the bond to the job trigger, not just buy whatever sounds familiar.

There's one more category worth mentioning even when it isn't the core issue on a construction project: fidelity or service bonds. Those come up more often when employees enter client property and the customer wants protection tied to dishonesty risk rather than contract completion. For a janitorial company, restoration firm, or service contractor working inside occupied spaces, that distinction matters.

How Underwriters Assess Your Bonding Capacity

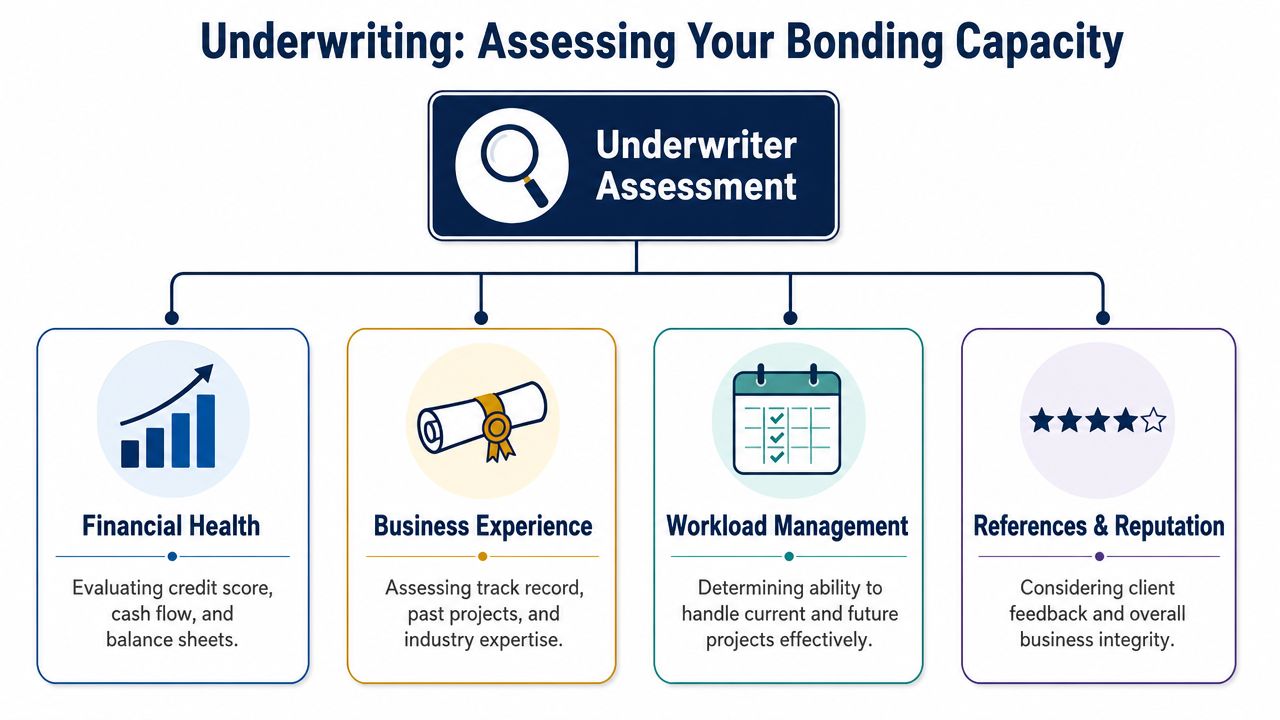

Bonding approvals rarely come down to one document or one score. Underwriters are trying to answer a practical question: can this contractor take this job, manage it, and finish it without creating a claim? They review the business the way an owner would if real money were on the line, because it is.

A helpful way to think about it is character, capacity, and capital. Those labels sound formal, but on a jobsite they translate into plain business habits. Does the owner pay bills on time. Has the company completed similar work before. Are the financials current enough to show whether the business can handle payroll, materials, and schedule pressure?

What underwriters want to see

Underwriters usually focus on a few practical areas:

- Financial strength: Clean financial statements, manageable debt, and enough liquidity to carry work in progress.

- Relevant experience: Jobs of similar size, scope, and complexity.

- Operational control: A stable crew, dependable subcontractors, and realistic scheduling.

- Reputation and references: Signs that the contractor finishes work and handles disputes without chaos.

Cash flow gets special attention because project stress usually shows up there first. A contractor can be profitable on paper and still struggle if receivables lag and payroll hits every week. Owners trying to tighten that side of the business can review practical guidance that helps unlock cash flow with Jumpstart Partners, especially when growth is outrunning working capital.

Concrete contractor example

A growing concrete contractor is a classic example. The company has handled flatwork, small foundations, and a few site packages. Now it wants its first larger bonded job. The underwriter won't just ask whether the owner wants to grow. The underwriter will ask whether the company has the crew, equipment, supervision, and financial cushion to perform if weather shifts, change orders stack up, or a payment draw gets delayed.

That review often overlaps with broader risk habits. A company with weak payroll controls, frequent injury issues, or poor claims discipline can look less stable overall. Even though workers' compensation and surety are different products, a contractor's operating discipline still matters. That's part of why some owners also keep an eye on items like workers' comp experience modification and loss trends while preparing for larger projects.

Strong bonding capacity usually starts before the bond application. It starts with organized books, realistic job costing, and a history of finishing what the business takes on.

Understanding the Costs of Bond Insurance

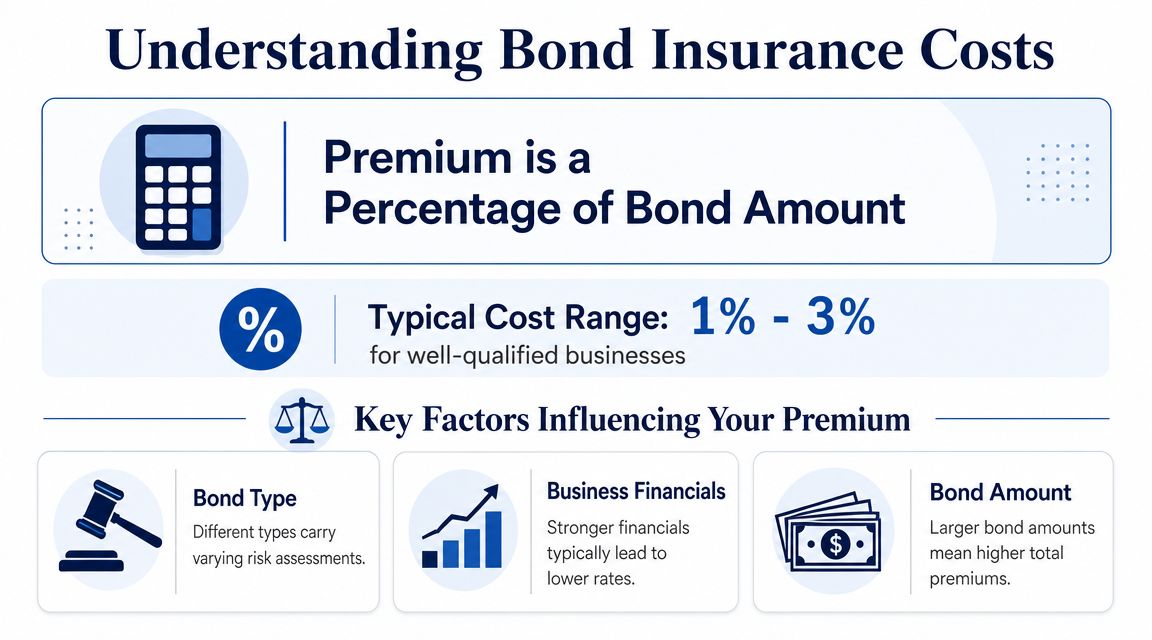

A contractor wins a school addition, signs the contract, and then hits the line that stops the job from starting: performance and payment bonds required before mobilization. At that point, the premium is only part of the decision. The bigger question is whether the job still makes sense after bond cost, indemnity exposure, and cash flow pressure are all on the table.

The first number owners ask about is the premium. Fair enough. Small license or permit bonds can be relatively inexpensive, while contract bonds usually price as a percentage of the job and rise or fall with the contractor's financial strength, experience, and the size of the obligation.

What the upfront cost can look like

A small electrical, plumbing, or license bond often feels manageable because the bond amount is modest and the business needs it to stay licensed, pull permits, or meet a local filing requirement.

Project bonds are a different budget item. On a public works bid or a larger private contract, the bond is tied directly to getting the award and getting paid. If the bid package requires a bond and the contractor cannot produce it on time, the job is gone. If the contract requires final bonds before notice to proceed, work can stall before the first invoice ever goes out.

Owners insist on bonds for the same reason lenders insist on collateral. They want a backstop if the contractor fails to perform or leaves subs and suppliers unpaid. Earlier in the article, I noted the SBA-backed analysis showing owner savings across bonded project portfolios. The practical takeaway is simple. Project owners do not view bond cost as wasted overhead. They view it as protection against delay, default, and payment disputes.

The cost that matters more than the premium

This is the part many small contractors miss. A surety bond does not protect the contractor the way a liability policy does. It protects the obligee, usually the owner, and in payment bond situations it also protects certain subs and suppliers.

If the surety pays a valid claim, the contractor usually owes that money back under the indemnity agreement. The premium buys the surety's guarantee to your client. It does not transfer the financial loss away from your company.

That distinction matters on real jobs. If a sitework contractor gets behind, the owner declares default, and the surety funds completion costs, the contractor can still be on the hook for reimbursement. If a drywall subcontractor is not paid and makes a valid payment bond claim, the surety may resolve it, then pursue recovery from the bonded principal. Insurance is built to absorb covered loss. Surety is built to guarantee your performance and then look to you for repayment if that guarantee is called.

How to evaluate the real cost of a bonded job

Premium is only one line item. The full cost also includes the personal indemnity you may sign, the working capital tied up by the project, the possibility of delayed draws, and the administrative burden of owner reporting, waivers, and closeout requirements.

That is why smart contractors price bonded work differently from unbonded work. They look at retainage, schedule risk, subcontractor reliability, and whether one dispute could trigger a claim problem that freezes progress payments. A practical review of contractor bonding requirements on real projects helps owners see that full picture before they commit to the job.

Your Step-by-Step Process to Get Bonded

A lot of bond problems start the same way. The contractor wins or chases a job, sees the bond requirement late, and then tries to force underwriting into a 24-hour window while the bid clock is running. That is how good jobs get missed, or get awarded with terms the contractor did not fully read.

The cleaner approach is to treat bonding like job qualification. The surety is sizing up whether your company can finish the work, pay subs and suppliers, and carry the job if cash flow gets tight. The bond protects the owner or obligee. It does not protect your balance sheet. If a claim is paid, your company and any indemnitors may still have to reimburse the surety.

Five practical steps

Gather your business and job documents early

Start with current financial statements, ownership details, work-in-progress schedules, backlog, bank information, and the contract or bid package for the job you want bonded. If there are old disputes, tax issues, or slow-pay accounts, put them on the table early. Underwriters do not expect a perfect file. They do expect a file that makes sense.Confirm the exact bond requirement in the contract

Read the solicitation, subcontract, or award documents line by line. A contractor may need a bid bond to submit the price, then a performance bond and payment bond after award. A license bond will not satisfy a contract bond requirement, and the wrong bond can cost time you do not have near bid day.Submit the request through a qualified bond advisor or broker

Some contractors place bonds through an existing surety relationship. Others use an advisor who handles commercial insurance and surety together. Coverage Axis is an independent commercial insurance advisory for contractors that also handles surety bond needs as part of broader compliance planning, which matters when the bond request shows up with general liability, workers' comp, auto, and certificate requirements on the same job.Work through underwriting and answer questions fast

This is usually where the file either moves or stalls. The underwriter may ask about experience on similar job sizes, gross profit fade on recent work, open claims, or whether key subcontractors are already lined up. Quick, straight answers help. So does explaining the job the way a field-tested contractor would explain it, including schedule pressure, material lead times, and where the cash pinch could hit.Review the quote, indemnity, and bond form before you pay

Premium matters, but it is not the whole decision. Check who has to sign the indemnity, whether personal indemnity is required, what bond form the obligee demands, and how quickly the bond has to be issued after award. If the surety pays a claim, repayment responsibility can come back to you. That point needs to be clear before the first invoice goes out on the job.

A real-world example

Take a landscaping contractor bidding a city parks maintenance contract. The city may require a bid bond with the proposal, then performance and payment bonds once the contract is awarded. Before crews mobilize, the city may also want certificates for liability, auto, and workers' compensation, plus vendor paperwork and scheduled start dates.

If the owner waits until the day before bids are due, every missing document becomes a crisis. If financials are current and the bid package is reviewed early, the bond becomes part of the job setup instead of the reason the contractor loses the work.

That is the practical goal. Get the bond in place early enough to win the job, and understand clearly that the bond backs your promise to the client while the financial risk still stays tied to your company.

Common Pitfalls and Your Next Steps

Most bonding problems aren't caused by the bond itself. They start earlier, with bad timing, weak paperwork, or a false assumption about what the bond does. Contractors who understand the practical side usually avoid the expensive mistakes.

The first mistake is waiting too long. Bond requests sent in right before a bid deadline force everyone into a rush, and rushed files get declined, delayed, or priced poorly. The second mistake is disorganized financials. A contractor doesn't need perfect books to start the conversation, but the numbers need to be current, readable, and consistent with the project being pursued.

Mistakes that slow down approvals

- Late applications: Bonding is often tied to award timing, bid timing, and owner review. Last-minute requests create pressure the contractor can't control.

- Wrong bond assumption: A contractor may buy a license bond when the issue is really a contract bond requirement, or assume a bid bond covers later obligations.

- Ignoring indemnity: Owners sometimes focus on the premium and skip the part where they remain financially responsible if the surety pays.

Bonding works best for contractors who treat it like a qualification process, not a formality.

What to do before the next bid goes out

A contractor should check three things before chasing the next larger job.

First, confirm whether the contract requirement is about licensing, bid submission, project completion, payment protection, or a mix of those. Second, make sure the financial package is clean enough for underwriting. Third, line up the insurance side at the same time, because many owners review all compliance items together.

For trade businesses trying to grow, bond insurance for small business can be a practical tool, not just a contract headache. It opens doors, but it also creates real obligations. The contractor who understands that difference is in a better position to bid smarter, avoid payment delays, and keep stronger jobs moving.

If a bond requirement is holding up a bid, contract award, or licensing step, Coverage Axis can help review the requirement, assess current bonding capacity, and provide a free quote or coverage review for the insurance and bond pieces that need to work together.