A lot of contractors hit the same wall at the same moment. The jobs finally get bigger, the bid invites start looking better, and then the specs say bonding is required. That's when a solid operator realizes growth isn't just about crew size, equipment, or estimating accuracy. It's also about whether a surety will stand behind the business.

For a contractor moving from smaller private work into public projects, school jobs, municipal work, or larger negotiated commercial contracts, bonding becomes a gatekeeper. It affects whether the bid is even responsive, whether the license stays active in some states, and whether owners believe the company can carry a more demanding job from award to closeout.

Table of Contents

- Why Bonding Is the Key to Bigger Contracts

- The Main Types of Contractor Bonds Explained

- When Are You Required to Be Bonded

- What Surety Underwriters Look For

- The Cost of Bonds Premiums and Collateral

- How to Get Bonded A Step-by-Step Process

- Your Contractor Bonding Compliance Checklist

Why Bonding Is the Key to Bigger Contracts

A surety bond is a three-party guarantee. The contractor is the principal. The project owner or licensing authority is the obligee. The surety backs the guarantee. That structure matters because a bond isn't insurance for the contractor. It's a promise to the customer, public entity, or regulator that the contractor will meet the obligation tied to that bond.

That's why bonding changes the conversation when a contractor starts chasing larger work. A bond tells the owner that someone has reviewed the contractor's financial strength, operating history, and ability to carry the job. It's one of the reasons bonded contractors often get a different level of consideration than contractors who can only say they're interested.

For a sitework contractor trying to move from small private pads into town utility work, the issue usually isn't field capability. The issue is access. If the bid package requires bonding and the contractor doesn't have it lined up, the estimating effort is dead on arrival.

Practical rule: Treat bonding like prequalification, not paperwork. If the company waits until bid day to think about it, the process usually gets harder, slower, and more expensive.

A lot of contractors also confuse bonds with general liability or workers compensation. They're not interchangeable. Liability insurance responds to covered claims. A surety bond backs a defined obligation and expects the contractor to honor that obligation. That distinction changes how sureties look at the business and why the underwriting process feels closer to a credit review than a standard insurance purchase.

Contractors who want a clearer overview of how these guarantees fit into a construction business can review surety bonds for general contractors. The main point is simple. Bonding is often the key that enables bigger contracts, larger owners, and more serious project opportunities.

The Main Types of Contractor Bonds Explained

Contractor bonding requirements make more sense when each bond is tied to the stage of work where it matters. The bond type changes with the risk the owner or regulator is trying to control.

Surety bond coverage options for contractors are easier to sort out when they're grouped by function, not by jargon.

How the bond stack works on a real job

Take an electrical contractor bidding on a public school addition. Before award, the owner may require a bid bond. That bond supports the bid itself. It tells the owner the contractor is serious and won't walk away if selected under the bid terms.

After award, the conversation changes. According to this construction bond guide, construction bonding is typically structured by risk function: bid bonds screen pre-award capacity, performance bonds transfer completion risk after award, and payment bonds protect subs and suppliers from nonpayment. The same guide explains that a performance bond guarantees the contractor will perform according to the contract and that the surety is responsible for arranging completion if the contractor defaults.

For that school project, the electrical contractor may also need a payment bond. If the contractor uses supply houses, low-voltage subs, or specialty installers, the payment bond helps protect those parties from nonpayment under the bonded contract.

Then there's the separate issue of licensing. A license bond doesn't attach to one specific school job. It's usually tied to legal operation in the state or local jurisdiction. That's the bond many contractors already carry before they ever pursue bonded public work.

A license bond and a project bond are not the same thing. One helps keep the business compliant. The other helps make the contract award possible.

Contractor bond types at a glance

| Bond Type | What It Guarantees | When It's Used | Trade Example |

|---|---|---|---|

| License and permit bond | Compliance with licensing rules or local regulations | Before operating, renewing a license, or pulling permits where required | A plumbing contractor maintains the bond required to keep the business legally licensed |

| Bid bond | The contractor will honor the bid and enter the contract if awarded | At bid submission | An electrical contractor submits a bid bond with a school project proposal |

| Performance bond | The contractor will complete the work according to contract terms | After award and before work begins, when required | A concrete contractor furnishes a performance bond on a municipal slab and foundation package |

| Payment bond | Subcontractors and suppliers on the project will be paid as required | Commonly paired with the performance bond after award | A general contractor on a bonded public job protects drywall, framing, and material suppliers from nonpayment |

The easiest way to think about these bonds is by the question each one answers:

- Can this contractor be trusted to stand behind the bid? That's the bid bond.

- Can this contractor finish what was promised? That's the performance bond.

- Will the downstream trades and suppliers get paid? That's the payment bond.

- Is this contractor legally compliant to operate? That's the license bond.

What doesn't work is assuming one bond solves every requirement. Contractors lose time when they think the bond already on file with a licensing board will satisfy a public owner's bid specification. It usually won't.

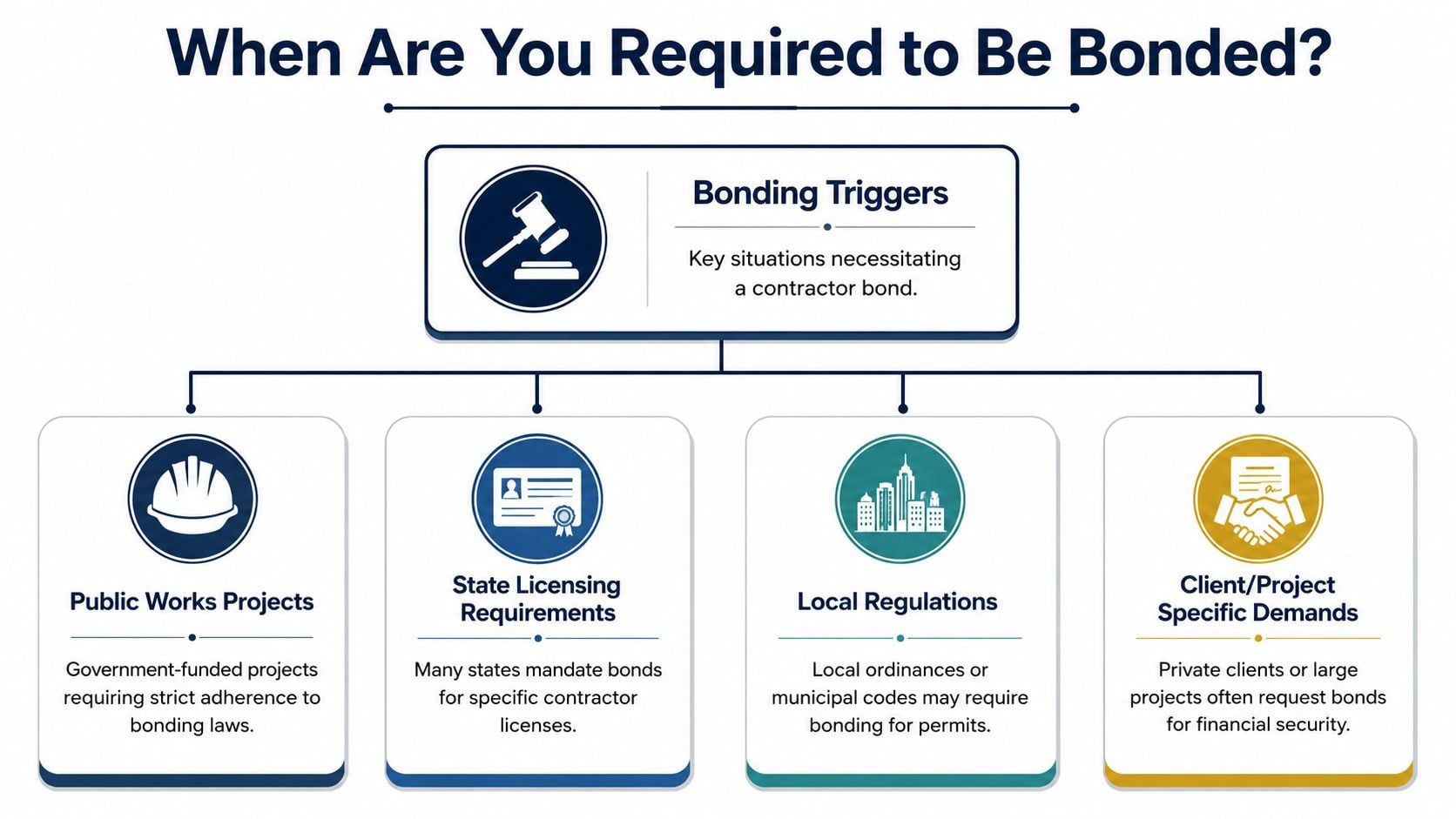

When Are You Required to Be Bonded

Contractor bonding requirements usually come from more than one place at the same time. A contractor may need a bond because a law requires it, because a license board requires it, because a city requires it for permits, or because the customer wrote it into the contract.

The four places bonding requirements usually come from

The biggest trigger is public work. As summarized in the ABC Carolinas overview of construction surety bond thresholds, the federal Miller Act requires performance and payment bonds for federal construction projects over $150,000 in 2026. That same summary notes that North Carolina requires similar bonds on state and municipal work exceeding $50,000, while South Carolina's threshold is $100,000. It also states that California requires a $25,000 contractor license bond on file with CSLB for all work.

That single set of examples shows why there's no one-size-fits-all answer. A contractor can cross from one state into another and face a different threshold, a different license rule, or both. A civil contractor working in North Carolina may need to think first about public project thresholds. A remodeling contractor in California may need to think first about keeping the license bond current.

Local rules add another layer. Some counties and municipalities require their own financial responsibility or permit-related bonding. For contractors expanding into new territories, that local layer can be the one that causes delays because the state bond on file doesn't automatically satisfy a city requirement.

What trips contractors up

The most common mistake is assuming the question is only about project size. It isn't. The primary variables are project type, location, license status, and contract language.

A mechanical contractor may be fully capable of handling a private industrial retrofit and still run into a bond requirement because the owner's contract department wants stronger financial backstops. Private owners don't always require bonds, but some do, especially on work where schedule pressure, subcontractor exposure, and completion risk matter.

Contractors sorting through jurisdiction-specific requirements often benefit from practical state examples such as Liberty Insurance Associates surety bonds, which show how bond obligations can shift by license class and local rules. Trade-specific contractors can also review plumber surety bond requirements when the question is tied to a licensed specialty trade rather than a general contracting operation.

Bid specs decide some bond requirements. State law decides others. Good contractors verify both before they price the work.

What Surety Underwriters Look For

Getting bonded feels different from buying standard insurance because the surety is trying to answer one core question. Can this contractor take the obligation, finish the work, and survive the financial stress that comes with construction?

Character capacity and capital in plain English

Underwriters often think in terms of character, capacity, and capital.

Character is the track record. Does the contractor have a pattern of finishing jobs, handling disputes professionally, and keeping obligations current? A framing contractor with organized records, a steady project history, and a reputation for paying suppliers on time usually presents better than a contractor with constant ownership changes, missing paperwork, and unresolved issues.

Capacity is operational ability. Can the business perform the job being requested? Crew depth matters. Supervision matters. Equipment access matters. So does project history. If an HVAC contractor has spent years on tenant build-outs and now wants to bond a far larger public mechanical package, the surety will want to know how that jump will be managed.

Capital is financial strength. Cash flow, liquidity, debt load, and overall balance sheet quality all matter because construction problems usually become financial problems before they become legal ones.

Strong field performance helps. Strong financial reporting makes that performance usable to a surety.

A contractor dealing with complicated claims history or prior disputes should also understand how bond obligations can interact with allegations of default or nonperformance. This overview of surety bonds and contractor litigation exposure is useful when that issue is part of the risk picture.

Documents that usually matter most

Sureties don't just want reassurance. They want documents. The most important items usually include:

- Business financial statements that are current and readable

- Personal financial information when the ownership structure requires it

- Work-in-progress schedules showing active jobs, backlog, and where the strain points are

- Resumes of key people who run the work

- Bank references that help show financial relationships and discipline

- Project history that matches the type of bond being requested

What works is consistency. Clean books, current job schedules, and accurate applications make underwriters more comfortable. What doesn't work is handing over stale financials, vague job descriptions, and numbers that don't match across documents.

The Cost of Bonds Premiums and Collateral

This is usually the first question from a contractor, and the honest answer is that bond cost depends on the contractor, the job, and the type of bond. There isn't one universal rate card that fits every trade and every project.

What contractors are really paying for

A bond premium isn't the same as an insurance premium in the way most contractors think about insurance. With a bond, the surety is charging for its guarantee and for the underwriting behind that guarantee. The contractor is still expected to fulfill the obligation and, if necessary, reimburse the surety under the bond agreement.

For a roofer moving into larger negotiated work, the premium question usually comes right after contract award. The practical answer is that stronger contractors with cleaner financials and more relevant project history usually get more favorable terms than newer firms, distressed firms, or firms stretching into unfamiliar work.

The bond amount itself also shouldn't be confused with the premium. A state may require a certain bond amount for licensing, but that doesn't tell a contractor exactly what the cost to obtain that bond will be. The underwriting result drives the offer.

When collateral enters the conversation

Collateral is where the conversation gets serious. It isn't required on every account, but sureties may ask for it when the file shows weakness, inexperience, unusual risk, or financial strain.

Florida is a useful example of how financial strength can affect bonding obligations. The state's official licensing FAQs state that applicants may need a bond or letter of credit if they have a 660 FICO-derived score or lower, and the amount can depend on license class, with examples of $20,000 for Division I contractors and $10,000 for Division II contractors in the FAQ guidance on construction licensing from Florida's official licensing resource.

That doesn't mean every contractor with a tough credit profile is shut out. It does mean the surety and the licensing authority may ask for more support. For a roofing contractor, that may mean more financial documentation, tighter terms, or additional security before a bond is issued. Contractors in that trade can compare the issues that commonly affect roofing contractor surety bonds.

What works is preparing for the credit and financial discussion early. What doesn't work is treating collateral like an insult. From the surety's side, it's a risk control tool.

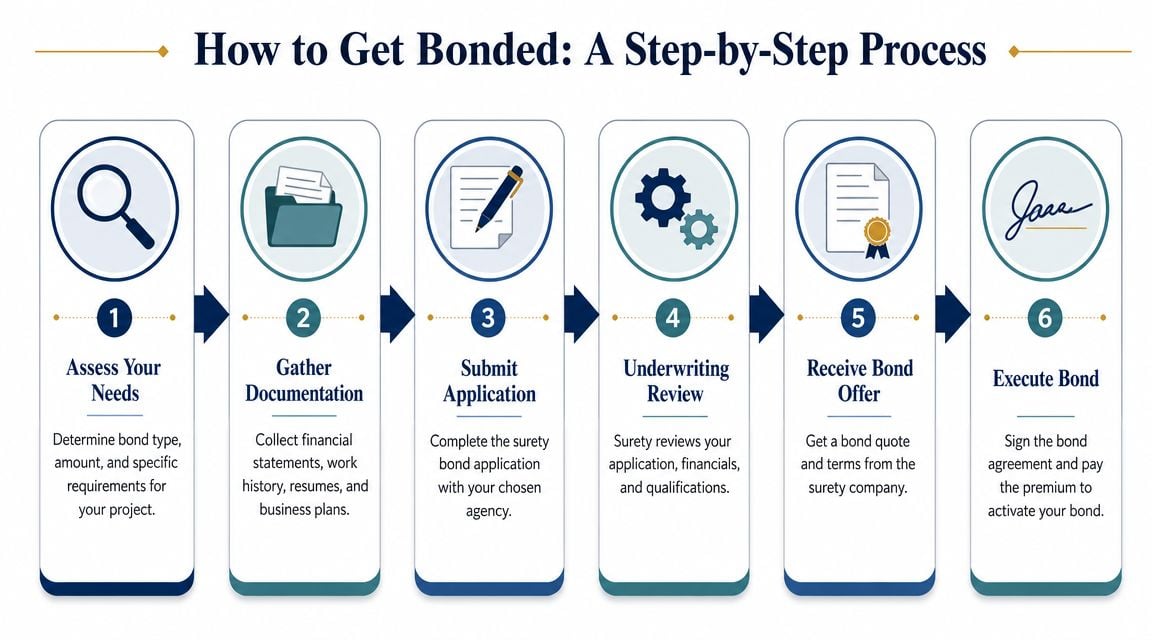

How to Get Bonded A Step-by-Step Process

A contractor usually finds out how prepared they are for bonded work when a better job lands on the table. The estimate is solid, the crew can handle it, and then the bid package asks for a bond the company has never had to produce before. At that point, speed matters, but preparation matters more.

A practical workflow for first-time bonded work

Take an HVAC contractor stepping up from smaller private jobs to a larger commercial project. The bond request is really a test of whether the business is operating at the next level already, on paper as well as in the field.

Start with the business file, not the bond form.

Gather current financial statements, ownership information, work history, active job schedules, bank details, and resumes for key people. Underwriters are trying to confirm that the company can finish the work it is asking to bond. If those records are incomplete or inconsistent, the file slows down fast.Work with an advisor who understands construction surety.

A general insurance conversation is not enough here. The right advisor can review the bid specs, flag indemnity requirements, spot missing documents, and present the account to sureties that write contractors in that size and trade.Complete the application carefully and match every document.

Small errors create avoidable delays. The legal business name has to match the license, contract, and bond form. Ownership percentages, entity type, and project history also need to line up across the file.Submit early enough for real underwriting.

A simple license bond may move quickly. A first bid bond tied to a larger contract often triggers questions about backlog, job size, cash position, and who is supervising the work. Waiting until the night before bid day limits options.

The fastest bond approvals usually come from contractors who prepare before they need the bond.

What happens after you apply

Once the submission is in, expect follow-up questions. That is standard underwriting, especially when a contractor is moving into a larger project size or a new type of bonded obligation.

The surety may ask for:

- Current financial statements

- A work-in-progress schedule

- Banking information

- Evidence of prior similar jobs

- Personal financial information from owners

- A copy of the contract or bid package

For a growing contractor, those requests are not paperwork for paperwork's sake. They are how the surety measures whether the company has enough working capital, project controls, and management depth for the obligation in front of it.

What helps the process move faster

A few habits make a real difference:

- Bring the exact bond requirement. Bid instructions, obligee forms, and license notices should be part of the first conversation.

- Describe the project clearly. “Commercial HVAC” is vague. “Tenant improvement with rooftop units, controls, test and balance, and startup” gives the underwriter something useful.

- Address weak spots directly. Credit issues, rapid growth, thin liquidity, or a jump in backlog are easier to handle when explained early.

- Keep financial reporting current. Sureties can work with imperfect numbers. They cannot work with stale numbers and guesses.

The long-term goal is not just getting one bond approved. It is building a bonding program that grows with the business. A contractor that starts with license compliance, then develops capacity for bid and performance bonds, is in a much better position when public work, larger private contracts, or multi-job backlogs become part of the plan.

Your Contractor Bonding Compliance Checklist

Bonding works best when it's treated as an ongoing part of operations, not a last-minute document chase. Requirements change by jurisdiction, project type, and license status, and stale assumptions create expensive delays.

A quick compliance checklist helps:

- Confirm the bond type. Make sure the requirement is for a license bond, bid bond, performance bond, payment bond, or a local financial responsibility obligation.

- Verify the bond amount and form. The right bond on the wrong form can still cause rejection.

- Check renewal dates. A lapsed bond can interrupt licensing or contract compliance.

- Keep financials current. Sureties need usable numbers, not rough estimates from memory.

- Review bid specs before estimating time gets wasted. If bonding is mandatory, that affects the go or no-go decision early.

- Track local rules when expanding territory. State compliance doesn't always satisfy county or city requirements.

- Maintain a working relationship with a bond specialist before the urgent bid arrives.

Washington offers a good reminder that bond rules don't stand still. In a Washington legislative report on contractor bonding requirements, the state reported in 2021 that general contractors were required to maintain a surety bond of $12,000, while specialty contractors held $6,000. The report used those figures to illustrate a broader policy issue: regulators keep reassessing whether statutory bond amounts still match current risk. For contractors, the practical takeaway is simple. Always verify the current requirement before assuming last year's rule still applies.

Bond compliance isn't a one-time task. It's part of staying license-ready, bid-ready, and growth-ready.

If a contractor is getting ready to bid larger work, expand into a new state, or clean up an existing bond program, Coverage Axis can provide a free quote or bonding review. A licensed advisor can help review current requirements, identify gaps in license or project bonding, and map out what the business needs before the next opportunity lands.