For contractors, bonded usually means the business or worker has qualified for a surety bond, which is a three-party financial guarantee that protects the client or project owner if contract obligations aren't met. On many public construction jobs, that requirement isn't optional, because under the Miller Act (1935) federal contractors generally must furnish performance and payment bonds on many public projects.

That's why the phrase licensed, insured, and bonded matters so much on a bid request. A plumbing contractor can have strong field crews, current licenses, and solid general liability coverage, then still get stopped cold because the owner wants proof of bonding before award. An electrical subcontractor can be fully capable of doing the work, but if the surety won't support the job, the bid may go nowhere.

For busy contractors, the fundamental question behind what does bonded mean for a job isn't academic. It's practical. Does this requirement affect bid eligibility, licensing, customer trust, crew access, or cash flow? In construction and trade work, the answer is often yes.

Table of Contents

- What Being Bonded Really Means on a Bid Request

- Bonded vs Insured A Critical Difference for Contractors

- The Main Types of Bonds Your Business Might Need

- Why Project Owners and Regulators Require Bonds

- How to Get Bonded The Underwriting Process

- Common Bonding Misunderstandings and Sample Language

- Secure Your Next Big Job with the Right Protection

What Being Bonded Really Means on a Bid Request

A general contractor opens a bid package for a municipal restroom remodel. The scope fits the company well. The crew can handle the schedule. The insurance is current. Then the requirement appears in one line: licensed, insured, and bonded.

That's the point where many contractors mix up bonded with a basic trust check. In trade work, that's usually the wrong read. For a contractor, bonded often means the business must qualify for a surety obligation tied to the job, the license, or both. Official surety guidance describes a surety bond as a three-party guarantee involving the principal, obligee, and surety, and notes that it's commonly required for licensing or contract performance, not just background-check approval, as explained in this surety bond overview for contractors.

For a roofer, this can show up when a public owner wants bid security before opening bids. For a plumber, it may come up at the licensing stage in one jurisdiction and then again when bidding a school project. For a GC, it often becomes the dividing line between small private jobs and larger contract opportunities.

What the bid language is really saying

When an owner asks whether a contractor is bonded, the owner usually wants to know whether the contractor can back promises with a financial guarantee. That's different from saying the contractor merely looks trustworthy.

A practical way to read it:

- If the language appears in a bid package, it usually affects whether the contractor can move forward at all.

- If it appears in licensing paperwork, it may be a compliance issue before work can start.

- If it appears in a customer contract, it often serves as risk control for completion, payment, or both.

Contractors don't lose bonded work only because they lack technical skill. They often lose it because they treated bonding like paperwork instead of qualification.

Contractors working toward larger projects often need to think about bondability early, especially in trades that move into public or institutional work. A roofing contractor preparing for that jump can see how trade-specific bonding expectations play out in this guide to surety bonds for roofing contractors.

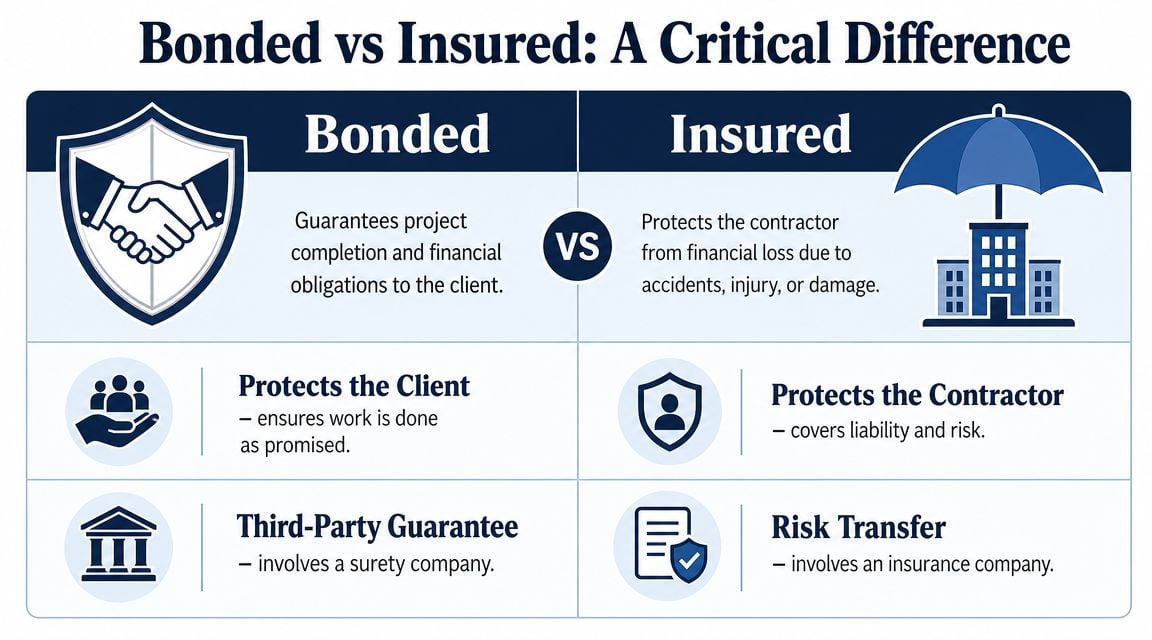

Bonded vs Insured A Critical Difference for Contractors

The easiest way to separate these terms is this: insurance protects the contractor's business from covered losses, while a bond protects the client or project owner if the contractor doesn't meet a stated obligation.

That difference gets blurred every day in job conversations. A contractor says the company is “bonded and insured,” but the owner may care about two completely different risks. One is accidental damage, injuries, or liability. The other is failure to perform, failure to pay, or dishonest conduct in a covered situation.

Who each one protects

In a job context, being bonded can mean an employer has a fidelity or surety bond that transfers part of the financial risk from employee dishonesty to an insurer. It isn't the same as being insured for accidents. It's a third-party guarantee that can reimburse the employer for losses caused by theft, embezzlement, forgery, or other dishonest acts by covered workers, especially in businesses where employees handle keys, cash, valuables, or sensitive access, as outlined in this explanation of bonded versus insured in business settings.

For contractors, that distinction matters on real jobs:

| Situation | Insurance response | Bond response |

|---|---|---|

| A plumber's tech cracks a finished tile floor while replacing a valve | General liability may respond if the loss is covered | A surety bond usually isn't the first tool here |

| A GC fails to complete the work according to contract obligations | Insurance typically isn't designed to guarantee contract completion | A surety bond may protect the owner |

| A service employee with building access steals from a client | Certain employee dishonesty bond structures may apply | General liability usually isn't built for that risk |

The three parties in a surety bond

Contractors hear terms like principal, obligee, and surety, and many tune out. On a job site, the translation is simple:

- Principal means the contractor or business that must perform.

- Obligee means the party requiring the bond, often the project owner, municipality, or licensing authority.

- Surety means the company backing the guarantee.

For an electrical contractor on a tenant improvement project, the electrical firm is the principal. The property owner or public entity is the obligee. The surety stands behind the bond if the bonded obligation isn't met.

Why owners ask for both

Clients want both because the risks are different. Insurance handles covered accidents and liability exposures. Bonds address trust and performance obligations that insurance doesn't replace.

A contractor who wants stronger overall risk planning should think beyond the bond itself and tighten the rest of the insurance program too. This practical look at business liability protection strategies is useful context, especially for firms that assume a bond can substitute for liability coverage. For the insurance side of that equation, contractors should also understand how general liability coverage fits into day-to-day field risk.

Practical rule: If a contract says “insured,” send proof of insurance. If it says “bonded,” be ready to show actual bond capacity or a bond form tied to the job. One doesn't replace the other.

The Main Types of Bonds Your Business Might Need

The phrase what does bonded mean for a job changes depending on the work. A GC bidding a public addition doesn't face the same bond issue as a locksmith with access to occupied buildings or an electrician renewing a local license.

The fastest way to sort it out is to divide bonds into two buckets. One bucket supports construction contracts. The other supports licensing, compliance, or employee dishonesty protection.

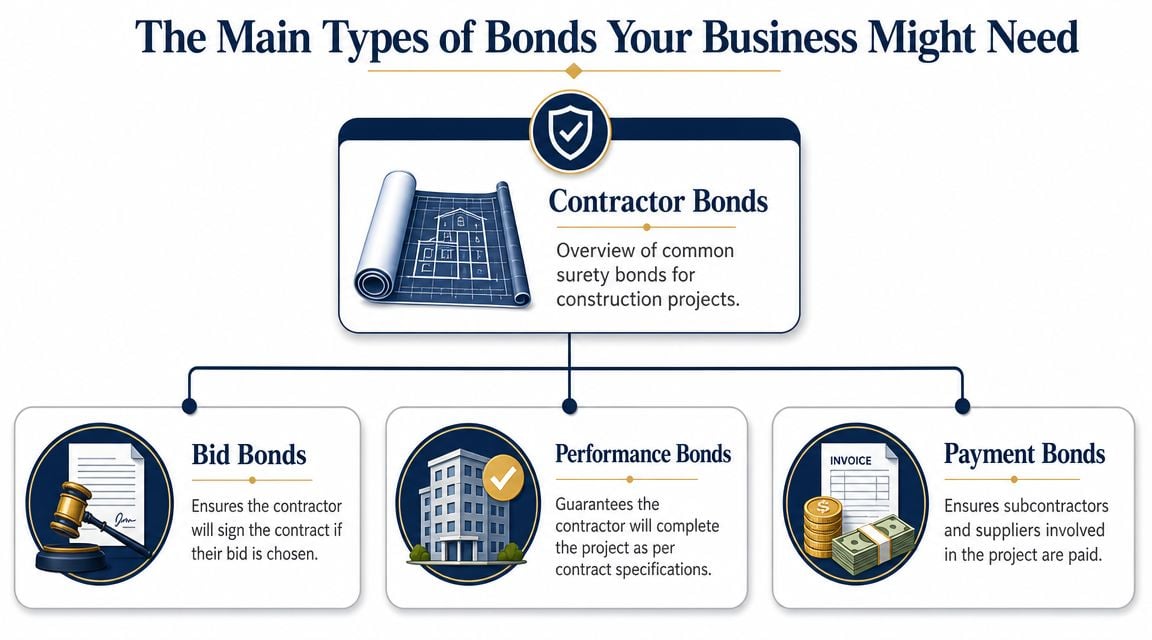

Contract bonds on construction jobs

These are the bonds contractors most often run into when trying to win bigger work.

Bid bond

A bid bond usually supports the contractor's promise that, if selected, the contractor will enter the contract and provide any required follow-up bonds. On a county reroof project, a roofing contractor may submit a bid bond with the proposal so the owner knows the bidder won't disappear after award.

Performance bond

A performance bond is tied to finishing the work according to contract terms. A GC building out medical office space may need a performance bond so the owner has a financial backstop if the contractor defaults or fails to perform as required.

Payment bond

A payment bond helps protect against nonpayment to subs and suppliers. If a drywall supplier or electrical subcontractor isn't paid on a bonded job, the payment bond can become part of the remedy path. Owners care about this because unpaid parties can create project disruption and legal headaches.

On public and larger private work, bid, performance, and payment bonds usually travel together as part of the owner's risk control system, not as isolated paperwork.

License, permit, and fidelity bonds

Outside project-specific contract bonds, contractors may need other bond types to stay eligible to operate.

- License and permit bonds support compliance with licensing rules. A plumber may need one to keep a local or state license active before even touching a permit-driven job.

- Fidelity bonds focus on employee dishonesty risk. These matter more in service businesses where crews enter occupied homes, hold keys, handle money, or access valuables.

- Business service or access-related bonds may come up when customer trust is part of the sale, especially in trades that work inside finished spaces.

A useful reminder is that bond amounts and requirements aren't symbolic. In one federal labor setting, covered organizations must bond anyone who handles union funds, with coverage set at at least 10% of the funds handled in the prior fiscal year, up to a $500,000 cap, showing that bond requirements can be directly tied to financial exposure, as noted in this discussion of bonding requirements tied to handled funds.

For contractors, the same logic applies in the field. A city may want a license bond because poor work affects the public. A developer may require a performance bond because an unfinished shell space costs real money. A property manager may ask whether service techs are bonded because those workers enter occupied units.

Contractors sorting through which category applies to their trade can get a better framework by reviewing these surety bond basics for contractors.

Why Project Owners and Regulators Require Bonds

Owners and regulators ask for bonds because they don't want to absorb a contractor's failure alone. Their concern isn't whether the contractor sounds confident in the pre-bid meeting. Their concern is whether there's a financial mechanism in place if the job goes sideways.

A city awarding a public electrical upgrade has different pressures than a homeowner hiring a small repair crew. Public agencies answer to procurement rules, budgets, and public accountability. Private developers answer to lenders, lease deadlines, and project schedules. Both want a contractor that can perform, pay downstream parties, and stay compliant.

Why public owners insist on bonds

Federal public construction helped cement bonding as a standard part of contractor qualification. The Treasury Department has long recognized the need for surety protection on federal construction and public works, and under the Miller Act (1935) federal contractors generally must furnish performance and payment bonds on many public construction jobs, which helped normalize bonding as a qualification standard in construction and related trades, as summarized in this overview of bondable requirements in hiring and construction.

That history still shapes the market today. If a contractor wants to work on public projects, being bondable often isn't a nice extra. It's a gate.

Why private owners use the same logic

Private owners may not always be required by statute to demand bonds, but many use the same risk logic. A developer hiring a GC for a retail build-out doesn't want a half-finished project, unpaid suppliers, or a contractor that runs out of capacity midstream.

From the owner's side, a bond does several things at once:

- Screens contractors early by forcing outside underwriting review

- Strengthens the contract because the obligation is backed by a surety

- Helps protect project continuity if performance problems develop

- Reduces payment-chain risk when payment bonds are required

For subcontractors, this matters too. A subcontractor can be fully competent and still get boxed out if the upstream contract requires bond support the firm hasn't prepared for. That's one reason many growing trade contractors spend time tightening contracts, risk transfer, and subcontractor liability planning before they chase larger work.

Owners don't require bonds because they expect failure on every job. They require bonds because one serious failure can wreck a project budget and schedule.

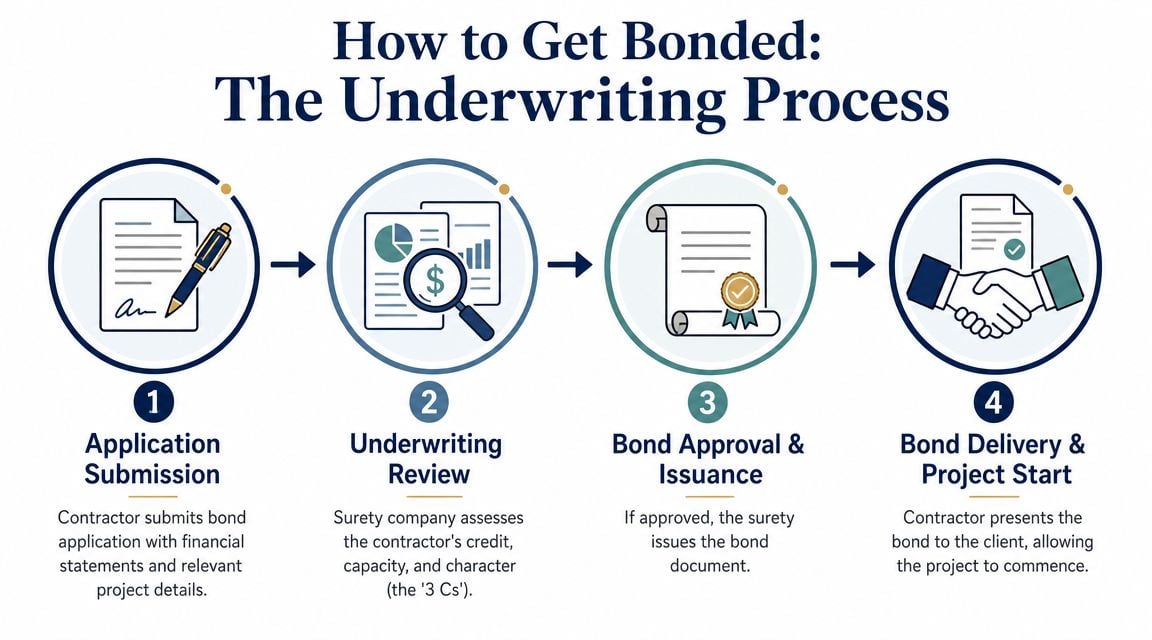

How to Get Bonded The Underwriting Process

Getting bonded feels less like buying a routine policy and more like applying for financial backing. The surety wants to know whether the contractor can finish the work, manage the money, and stay reliable under pressure.

For a general contractor moving from small tenant improvements into public work, this is often the first surprise. Strong field execution matters, but the underwriting file matters too. A surety wants evidence, not just confidence.

What underwriters actually review

A practical framework is character, capacity, and capital.

Character covers how the business has conducted itself. Surety carriers can review broader financial and business signals such as credit history, tax history, payment delinquencies, and past business conduct, and bondability can be affected by issues such as payment delinquencies, criminal records, or poor credit or tax history, as discussed in this overview of bondability and financial background review.

Capacity is about whether the contractor can perform the work. A surety looks at job history, crew depth, project type, backlog, and whether the new job is a reasonable step up or a dangerous leap.

Capital comes down to financial strength. That usually means the contractor should expect requests for business financial statements, work-in-progress information, and details about liquidity and obligations.

A plumbing contractor pursuing larger municipal work should expect the surety to care about more than technical skill. Clean books, organized reporting, and a stable payment pattern often help the file move faster.

What helps and what slows approval

Some contractors make underwriting harder than it needs to be. They bid first, scramble later, and send incomplete financials when the bond is suddenly required.

What tends to help:

- Current financial records that clearly show how the business is performing

- Accurate job history with contract sizes similar to the work being pursued

- A clean tax and payment trail that doesn't raise avoidable questions

- Realistic growth steps instead of jumping too far beyond proven capacity

What commonly slows things down:

- Messy bookkeeping

- Late tax issues

- Unexplained credit problems

- Weak visibility into ongoing jobs and backlog

Contractors that need to tighten their financial presentation before approaching a surety can benefit from practical budgeting and reporting discipline. This overview of building a comprehensive financial plan is useful for firms that know the books need to look more lender-ready and surety-ready.

A contractor doesn't usually “talk” a surety into support. The file does the talking.

For firms preparing to grow into larger bonded work, it helps to review the expectations that commonly apply to general contractor surety bond programs. That's often where contractors spot the gaps between being good at the trade and being ready for bond-backed bidding.

Common Bonding Misunderstandings and Sample Language

Contractors lose time and jobs when they use the word bonded loosely. In trade work, sloppy language creates the wrong expectation with owners, brokers, and procurement teams.

Misunderstandings that cost contractors jobs

“Being bonded just means the crew passed a background check.”

Sometimes bondability does involve underwriting review, but that's not the whole story in contracting. On bid and license work, the issue is usually whether the business can qualify for the bond required by the owner or regulator.

“If the company is insured, that should be enough.”

It isn't. Insurance and bonds solve different problems. A COI doesn't satisfy a performance bond requirement.

“An LLC means a bond isn't necessary.”

Entity structure and bonding serve different purposes. Forming a company doesn't create the project guarantee an obligee may require.

“If one bond was approved once, the company is bonded for everything.”

Bondability can vary by project type, obligee, scope, and business condition. A contractor may qualify in one setting and hit resistance in another.

Owners notice the difference between a contractor who says “we carry insurance” and a contractor who clearly states what bond support is available.

Sample language for bids and proposals

A contractor doesn't need fancy wording. The language should be accurate and specific.

Use copy like this in a proposal when it's true:

- Bid-ready statement: “Our company is bondable and can provide required bid, performance, and payment bonds upon request.”

- License-focused statement: “Our company maintains the bonding required for applicable license and permit obligations.”

- Service-trade statement: “Our team is insured for field operations, and bonding support is available where contract or client requirements apply.”

- Subcontractor qualification statement: “Bond documentation can be furnished when required by the prime contract or project owner.”

For example, an HVAC contractor bidding on a school retrofit shouldn't just write “fully bonded” unless the company is prepared to deliver the bond forms required under that contract. Specific language is safer and more credible.

Secure Your Next Big Job with the Right Protection

For contractors, what does bonded mean for a job usually comes down to one business reality. It means access. Access to licenses, bid lists, public work, larger private jobs, and customers who want more than a handshake.

The companies that handle bonding well usually treat it as part of business readiness, not an afterthought. They keep financials clean, understand which bond type applies to which project, and avoid confusing bonds with insurance. That makes them easier to qualify, easier to trust, and easier to award.

A GC chasing larger tenant improvements, an electrician moving into public work, and a plumbing contractor seeking municipal jobs all face the same basic test. Can the business show that it's built to perform, not just built to bid?

Contractors who need help sorting out surety bonds, liability coverage, workers comp, commercial auto, and the rest of the insurance stack can get a free quote or coverage review from Coverage Axis. A licensed advisor can help review current requirements, spot gaps that may affect bondability, and build a program that fits the trade, crew, and project mix.