A lot of contractors hit the same wall at the same time. The company has grown past small service work, maybe added crews, maybe started chasing school, municipal, utility, or larger commercial jobs, and then the bid package says one phrase that changes the whole conversation: bonding required.

That line usually triggers two immediate questions. First, what kind of bond is this. Second, how much risk is the company really taking on by submitting it. Those are fair questions, because bid bond vs performance bond is not a paperwork distinction. It affects whether a contractor can bid, whether the owner will take that bid seriously, and what happens if the job goes sideways after award.

For an electrical contractor, this often shows up when moving from private tenant build-outs into public renovations, school upgrades, or larger infrastructure-related work. The estimator can price the feeders, switchgear, lighting controls, trenching, and labor. The owner, however, wants another answer before opening the bid. Can this contractor commit to the number, sign the contract, and finish the work if awarded?

Table of Contents

- The Moment a Bid Package Demands a Bond

- What Is a Bid Bond The Gatekeeper to Your Bid

- What Is a Performance Bond The Guarantee for Your Work

- A Side-by-Side Comparison for Contractors

- The Bond Claim Process What Happens When Things Go Wrong

- Beyond the Basics Contract Rules and Variations

- How to Get Bonded and Win More Work

The Moment a Bid Package Demands a Bond

A growing electrical contractor might be bidding a school renovation with panel replacements, emergency lighting, fire alarm updates, and phasing around occupied classrooms. The takeoff is done. Suppliers have quoted major gear. Labor has been sharpened. Then the front-end documents require a bid bond with the proposal and a performance bond after award.

At that point, the job stops being only about price.

The owner is now screening for two different risks. One risk exists before award. Will the low bidder stand behind the number, sign the contract, and provide the required follow-on bonds? The other risk exists after award. Will the selected contractor complete the work under the contract requirements?

Those are different problems, which is why they use different bonds.

A bid bond is the pre-award tool. It tells the owner that the bidder is serious and that a surety is willing to back that commitment at the bid stage. A performance bond is the post-award tool. It backs the contractor's obligation to finish the work according to the contract after the job has been awarded.

Practical rule: If the bid bond gets a contractor into the room, the performance bond is what keeps the contractor in the game after award.

Contractors often make one of two mistakes here. Some treat bonding like a clerical item and request it at the last minute. Others assume that if they can price the job, they can automatically bond the job. Neither assumption holds up on larger work.

The better move is to treat bonding like part of bid strategy. Before submitting on larger public or institutional work, contractors should already know their likely bonding capacity, what financials the surety will want, and whether the contract language creates unusual exposure. A practical starting point is understanding how to get bonded and insured for contractor jobs, because bonding and insurance usually move together once the work gets bigger and the paperwork gets tighter.

What Is a Bid Bond The Gatekeeper to Your Bid

A bid bond protects the project owner during the bidding stage. It does not promise that the job will be completed. It promises something narrower and very important. If the contractor is awarded the work, that contractor will sign the contract and furnish the required next bond package.

What the owner is really asking

Most owners use the bid bond as a seriousness filter. They don't want to spend time sorting bids from companies that may withdraw, discover they can't secure the follow-on bond, or decide the number was too aggressive after the fact.

Federal procurement rules make that timing point clear. The Federal Acquisition Regulation guidance on bid guarantees and related bond requirements states that a contracting officer generally may not require a bid guarantee unless a performance bond or a performance-and-payment bond is also required. That's why the bid bond should be viewed as a pre-award screening tool. The key question isn't just which bond is which. It's what obligation is being secured, and when the surety's exposure begins.

For trade contractors, this also changes estimating discipline. If a company is bidding work that requires a bond, the estimate has to be complete enough to live with. That includes supplier commitments, lead-time assumptions, scope exclusions, and manpower planning. Tools that tighten scope and pricing early can help reduce preventable bid mistakes. For contractors working on mechanical or multi-trade estimating workflows, Exayard HVAC estimating software is one example of the kind of system contractors use to standardize takeoffs and proposal logic before bonded bids go out.

Electrical trade example

Take an electrical contractor bidding a school generator and distribution upgrade. The contractor prices demolition, temporary power coordination, new conductors, gear setting, testing, and closeout. The district wants confidence that if this contractor is low, the company won't come back a week later and say the generator lead time was missed, the switchboard quote expired, or the job is no longer workable.

That is where the bid bond earns its keep.

It serves three practical functions:

- It tells the owner the bid is credible. A surety has looked at the contractor closely enough to support the bid submission.

- It commits the bidder to the next step. If awarded, the contractor is expected to execute the contract and move into final bonding.

- It weeds out weak submissions. Contractors who can't support the number operationally or financially are less likely to survive this gate.

A bid bond is often written at about 10% of the bid amount in North American construction, and if the winning bidder refuses to execute the contract, the owner's recovery is typically capped at the bond penalty or the spread to the next compliant bid, whichever is lower, as explained in this surety overview of bid and performance bonds.

What Is a Performance Bond The Guarantee for Your Work

A performance bond starts mattering after the contractor wins the job. This bond protects the owner against failure to complete the work according to the contract.

That difference sounds simple, but it changes everything. The bid bond concerns commitment to the bid. The performance bond concerns execution of the actual job.

What changes after award

Once the owner issues notice of award, the contractor isn't just a bidder anymore. The company is now responsible for mobilizing, buying out material, staffing the work, sequencing trades, handling submittals, and performing according to plans, specs, and schedule.

For an electrical contractor on the same school project, the risk shifts from "Will they sign?" to "Can they finish?" If the contractor falls into default midstream, the owner may be dealing with half-installed raceway, gear that hasn't been energized, inspection delays, and a building that can't open on schedule.

That is why performance bonds are much broader in practical effect than bid bonds. They exist to protect the owner's completion risk. Contractors who want a plain-English explanation of that post-award expectation can review what bonded means on a construction job, because the bond obligation follows the contract, not just the proposal.

The performance bond is where the owner transfers the biggest practical fear on a construction project: paying one contractor and still needing another one to finish.

Why underwriting gets more serious

Performance bond underwriting is usually stricter because the surety's exposure is much larger. The contractor has to show more than the ability to submit a believable estimate. The surety wants evidence that the company can manage the project and absorb the stress if margins tighten, labor gets thin, or a supplier issue hits the schedule.

That file often includes items like:

- Financial strength to support payroll, materials, and working capital through the life of the project

- Work-in-progress visibility so the surety can see backlog, profit fade, and whether the company is stretched

- Relevant experience on jobs with similar size, complexity, contract terms, and phasing requirements

In practice, some otherwise successful trade contractors often get stuck. They can perform the work technically, but the company records, statements, backlog reporting, or internal controls haven't caught up to the size of jobs being pursued. A performance bond exposes that gap quickly.

Unlike a bid bond, the performance bond isn't just a ticket into the procurement process. It is the owner's protection if the awarded contractor cannot deliver what the contract requires.

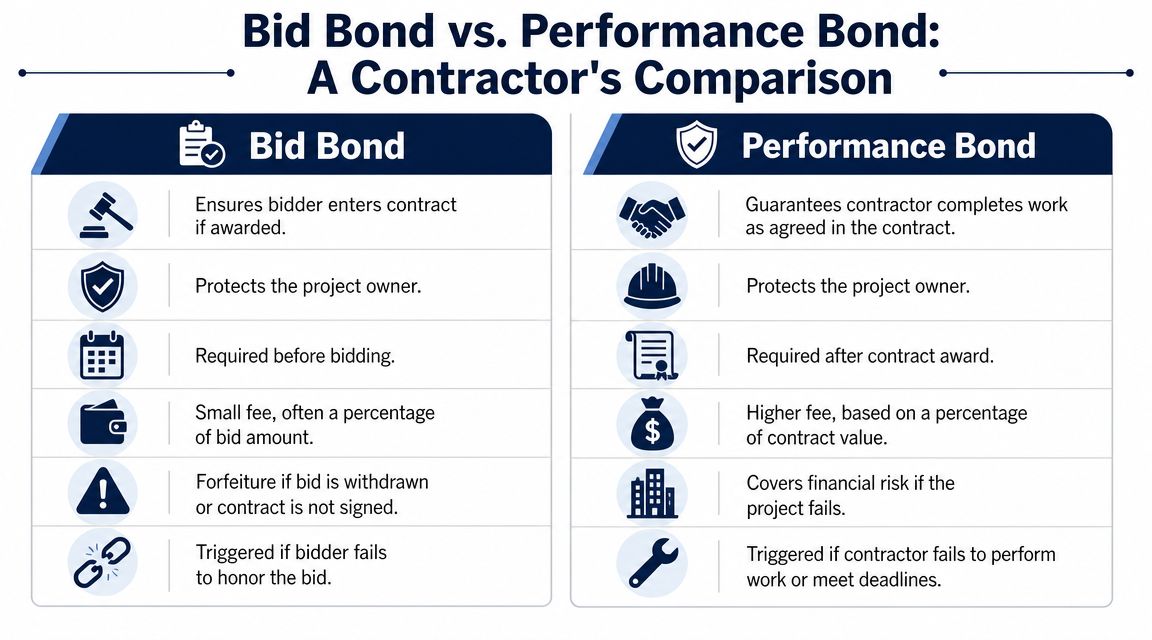

A Side-by-Side Comparison for Contractors

Contractors often treat these two bonds as part of the same paperwork stack. In practice, they solve two different problems and create two different risks for your company. One protects the owner from a bad bid commitment. The other protects the owner from a failed job.

That distinction matters because the consequences hit at different points in the project.

Quick comparison table

| Issue | Bid bond | Performance bond |

|---|---|---|

| Primary purpose | Secures the bidder's commitment to sign the contract and provide required follow-on bonds | Secures completion of the work according to the contract |

| When it applies | Before award, during bidding | After award, during performance |

| Typical amount | Usually a modest percentage of the bid, based on the solicitation requirements | Often tied to the full contract amount on bonded work |

| Typical pricing | Often nominal once a contractor has an established surety program | Priced based on the contract size, risk, and contractor profile |

| What triggers a claim | The contractor withdraws, refuses to sign, or cannot provide required post-award bonds | The contractor fails to complete the contract according to its terms |

| Who it protects | The project owner | The project owner |

What the differences mean in the field

A bid bond puts your estimate under a microscope. It tells the owner your number is real, your company intends to honor it, and your surety is willing to stand behind that commitment for the bidding stage. If your team misses scope, carries bad supplier pricing, or bids work your company cannot staff, the problem shows up fast after award.

A performance bond tests something different. It is less about whether you can price the job and more about whether you can deliver it under contract pressure. Cash flow, manpower planning, project management, change order discipline, and subcontractor control all matter once the work starts.

For electrical contractors stepping into larger public or negotiated work, that is usually the dividing line. Bid bond risk lives in preconstruction. Performance bond risk lives in operations.

The insurance and bond package is often reviewed together. Contractors pursuing larger work should line up bonding with their broader general contractor insurance requirements because owners and upstream contractors usually check the full compliance file, not one item at a time.

Here is the practical trade-off:

- Bid bond stage: You need a clean estimate, committed pricing, and confidence that you can execute the award if you win.

- Performance bond stage: You need the balance sheet, reporting, field supervision, and vendor support to finish the work without the job getting away from you.

- Financial exposure: A bid bond problem usually creates a defined dollar dispute tied to the bid spread. A performance bond problem can pull in delay, completion cost, replacement contractor expense, and heavy scrutiny from the surety.

- Relationship risk: A failed bid obligation can hurt your standing with an owner. A performance problem can hurt your standing with the owner, the surety, and your future bond capacity.

Contractors who understand that difference bid more selectively. They stop asking only, "Can we win this job?" and start asking, "Can we bond it, staff it, finance it, and finish it without putting the rest of the company at risk?"

The Bond Claim Process What Happens When Things Go Wrong

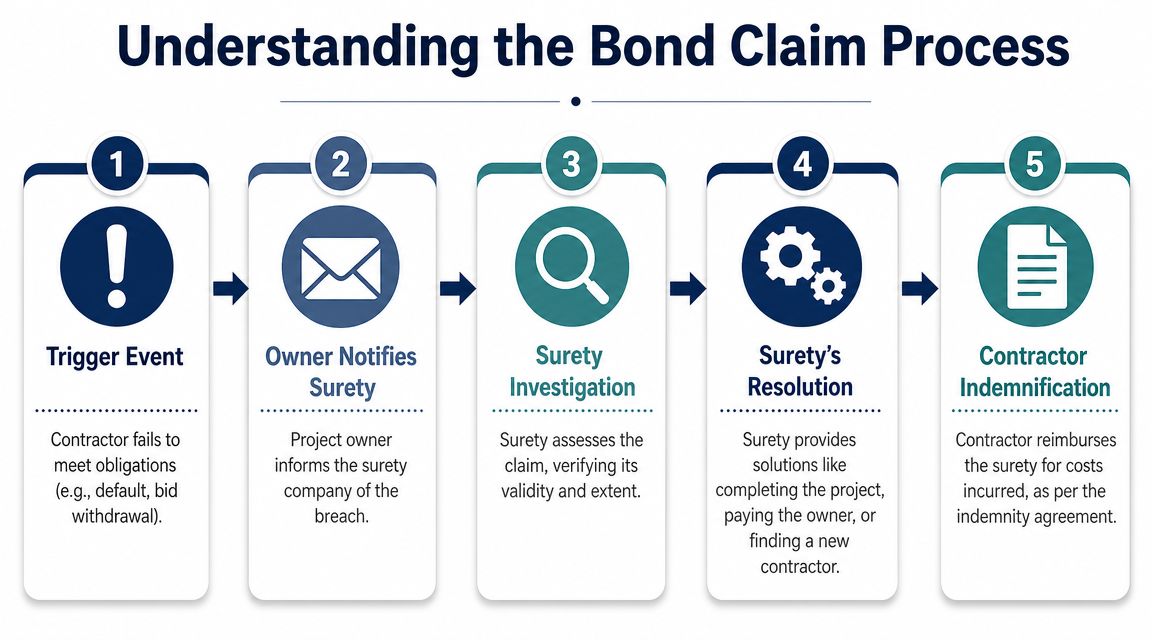

This is the part many contractors never get a straight answer on. Owners, estimators, and project managers often use the phrase "call the bond" as if the surety merely writes a check and moves on. That isn't how most bond claims work.

A surety investigates. It looks at the contract, the bond form, the notice requirements, and what happened. Then it decides what obligation has been triggered and what response the bond requires.

When a bid bond gets called

A bid bond claim usually starts when the low bidder won't honor the bid after award. That might happen because the contractor found a scope error, lost a key supplier quote, realized labor was undercounted, or couldn't obtain the required post-award bond package.

The owner then notifies the surety and supports the claim with the award decision and the contractor's failure to follow through. At that point, the issue is not project completion. The issue is the financial gap caused by the failed bid commitment.

For the contractor, the consequences can include:

- Immediate reputational damage with that owner or public entity

- Strain with the surety because the contractor failed at the very first bonded promise

- Potential reimbursement obligation to the surety under the indemnity agreement

A bid bond claim is usually narrower than a performance claim, but it still tells the surety something serious. The contractor either didn't understand the bid, didn't control the number, or couldn't support the award obligations.

When a performance bond claim starts

A performance bond claim is heavier. It usually begins only after the contractor is declared in default under the contract and the owner has followed the bond's notice process. The surety then investigates whether the default is valid and what remedy the bond allows.

This is why performance bonds should never be thought of as simple cash instruments. The Clark Wilson construction bonding guide notes that upon default, the surety may be obliged to remedy the default, complete the contract, or solicit completion bids. That makes the bond a controlled completion mechanism, not just a payout.

For an electrical contractor, a performance bond claim might grow out of repeated schedule failures, abandonment, insolvency, or inability to complete critical systems. If the contractor leaves a school project with unfinished switchgear startup, incomplete branch circuits, and failed inspections, the owner still needs the building energized and accepted. The surety's role is to respond within the bond terms so the project can move toward completion.

A simplified claim path often looks like this:

- A trigger event occurs. The contractor fails to perform contractual obligations.

- The owner gives notice. The surety receives formal claim information.

- The surety investigates. Contract status, default procedure, and damages are reviewed.

- A remedy is selected. The surety may support completion, arrange completion, or respond financially within the bond structure.

- The contractor remains on the hook. Most surety arrangements include indemnity, so the contractor may have to reimburse the surety.

Calling a bond doesn't erase the contractor's problem. It usually creates a bigger one, because the surety expects to be repaid under the indemnity agreement.

Beyond the Basics Contract Rules and Variations

A lot of bond trouble starts before performance does. It starts in the bid package, in the supplementary conditions, or in the bond form attached at the back of the contract.

For contractors stepping into larger public or negotiated private work, the rule changes matter because they affect more than paperwork. They affect whether your bid is responsive, how a default must be declared, how fast a surety has to react, and how much room you have to cure a problem before the owner pushes the claim forward.

Federal work has tighter rules and less margin for admin mistakes

Federal jobs usually leave less room for informal fixes. Bond requirements, forms, and submission timing are handled with strict compliance standards, and a mistake that looks minor in a private bid can get a federal bid rejected.

That matters in real terms. If the wrong surety seal is used, the bond amount does not match the solicitation requirement, or the signature package is incomplete, the owner may never get to your price or qualifications. The bid is out.

Private and local public work can be more varied. Some owners use standard industry bond forms. Others revise them heavily, especially around default notice, termination rights, and the surety's options after a claim. That is where experienced contractors slow down and read the actual form instead of assuming every performance bond works the same way.

The paperwork stack grows fast on bonded jobs. Keeping bond forms, endorsements, and insurance documents organized with a certificate of insurance template for construction compliance tracking helps prevent the kind of admin miss that turns a good bid into a nonresponsive one.

The bond form can change the claim outcome

This is the part many articles skip. Two performance bonds can carry the same penal sum and still behave differently once a project goes sideways.

One form may require the owner to declare default formally, terminate the contractor, and give the surety a chance to choose a remedy before completion costs start stacking up. Another may be written more tightly for the owner and give the contractor less room to cure. Some forms tie the bond response closely to the contract's default language. If that contract language is broad, the claim risk is broader too.

For an electrical contractor, those differences have practical consequences:

- A stricter notice clause can buy time to correct manpower, procurement, or schedule problems before a claim hardens.

- A broad default definition can turn repeated missed milestones into a bond issue sooner than expected.

- A modified obligee form can reduce the surety's flexibility and increase pressure on the contractor once a dispute starts.

- Paired performance and payment obligations can widen the financial mess if subcontractors or suppliers are already unpaid.

Contractors who win larger work usually review these points before they submit a number, not after award. Good estimating discipline still matters, and so does proposal strategy. TruTec's guide to winning bids is useful on the front end, but once bonding enters the picture, contract review has to sit right beside pricing.

Read the front-end documents. Confirm which bond form is required. Check the default language. Verify the notice steps. Those details decide what happens if the job gets into trouble, and they often decide it long before anyone says the word claim.

How to Get Bonded and Win More Work

You win a larger school job, then the bond request lands on your desk with a short turnaround and a long list of underwriting questions. At that point, the issue is not whether the estimate was sharp. The issue is whether the surety believes your company can carry the job, absorb problems, and finish without creating a claim.

That decision affects how much work you can chase next year.

Sureties underwrite the business behind the bid. They look at whether management has handled similar contract size, whether financials show enough working capital, and whether backlog is controlled instead of stacked too high. They also pay close attention to job cost reporting, change order discipline, billing practices, and the quality of your internal controls. A contractor can be profitable and still make an underwriter nervous if project information comes in late or margins move around without a clear explanation.

For a practical overview of what underwriters usually request, this construction bond requirements guide for contractors gives a solid baseline.

What gets a file approved faster

The contractors who expand their bond program usually make underwriting easy to follow. They submit current financial statements, clean work in progress schedules, an accurate backlog report, and bid information that shows the scope was reviewed instead of rushed. If there was a bad job in the past, they explain what happened and what changed. That helps more than trying to hide it.

Sureties also look for evidence that the company can manage growth. For an electrical contractor, that often means field supervision depth, supplier relationships, labor availability, and a clear plan for projects that involve long-lead gear or tight phasing. Those issues turn into bond problems when they are ignored early.

What actually helps you win more work

Bonding capacity is a sales tool, but only if it is credible. Owners and general contractors read the bond requirement as a screen for stability. If your surety support is thin, you may have to pass on jobs you could build profitably. If your program is set up well, you can bid larger public work, negotiate from a stronger position, and respond faster when a good opportunity opens up.

Preparation also matters after award. Once a performance bond is on the job, weak project controls carry more risk because a dispute can pull in the owner, the surety, and your bank at the same time. That is why getting bonded is not just about checking a compliance box. It is about building a company that can take on larger contracts without putting the balance sheet in a bind.

Strong proposal discipline still helps on the front end. TruTec's guide to winning bids is useful for tightening scope presentation, assumptions, and pricing before submission.

Coverage Axis works with contractors that need bonding and insurance lined up at the same time. That coordination matters on larger jobs, where bond forms, liability coverage, workers compensation, auto, and owner requirements all have to match the contract package.

The firms that win more bonded work usually do the same few things well. They keep financials current, know their backlog, bid the work they can staff, and treat underwriting as part of business planning rather than a last-minute paperwork drill.

Contractors moving into larger bonded work can request a free quote or coverage review from Coverage Axis. A licensed advisor can review current insurance, bond needs, and project requirements in plain English so the business can bid with fewer compliance surprises.