A lot of contractors land in the same spot. A bid is due, margins are tight, payroll is small, and the workers comp line item looks like the easiest place to save money. A residential painter with one helper, a small HVAC outfit with two owners, or a flooring installer using subs may look at an exemption form and think the answer is simple.

It usually isn't. Workers comp exemptions can be legal in some situations, but legal and safe aren't the same thing. One fall from a ladder, one hand injury on a saw, or one disputed subcontractor relationship can turn a short-term savings decision into a business-threatening problem.

That risk sits inside a system with real scale. In 2015, workers' compensation benefit payments totaled $61.9 billion nationally, with medical benefits accounting for $31.1 billion and wage loss compensation for $30.7 billion, averaging $0.86 per $100 of covered wages across all industries, according to the Social Security Administration workers compensation statistical supplement. That's the backdrop for every exemption decision a contractor makes.

Table of Contents

- The Exemption Gamble Many Contractors Consider

- What a Workers Comp Exemption Really Means

- Who Can Be Exempt Common Categories for Contractors

- Why State Rules Change Everything for Your Trade

- The High Cost of Getting Exemptions Wrong

- Smarter Choices Than Skipping Coverage

The Exemption Gamble Many Contractors Consider

A small trade business usually doesn't start by trying to break rules. It starts by trying to win work.

A residential painter gets asked to bid a repaint on a multi-unit building. Material prices are already up, labor is hard to line up, and the general contractor wants a sharp number. The painter looks at payroll, sees only a few people touching the job, and starts asking the same question many owners ask. Can the business skip workers comp and claim an exemption?

That question sounds administrative. It isn't. It's a risk calculation tied to who's on the job, how they're classified, what state law says, and what happens if somebody gets hurt before the final coat dries.

Why the savings can look tempting

For a contractor staring at thin margins, exemptions can feel like a competitive move. If a business owner, spouse, or family member works in the company, the owner may assume those people don't need to be on a policy. If labor comes through subcontractors, the owner may assume the exposure sits with them.

Sometimes those assumptions line up with state law. Sometimes they don't. And sometimes they work right up until an injury forces a state agency, auditor, or carrier to take a closer look.

Practical rule: If the only reason an exemption looks attractive is price, the contractor probably hasn't priced the real risk yet.

A painter on a two-story exterior job doesn't care what the payroll spreadsheet said that morning. If a fall happens, bills start immediately. Lost time starts immediately. Questions about who employed whom start immediately too.

Contractors need the full risk picture

The better question isn't just whether an exemption is available. It's whether the business can survive the consequences if the exemption fails, gets challenged, or leaves an owner personally exposed.

That's why workers comp decisions should sit next to the rest of the contractor's insurance planning, not off to the side as a cheap fix. A contractor reviewing what insurance contractors need should treat workers comp as part of the job-cost and compliance conversation, especially when crews, subs, and project requirements are changing from one job to the next.

What a Workers Comp Exemption Really Means

A workers comp exemption is often misunderstood because the paperwork looks simple. The decision behind it is not.

At the practical level, an exemption usually means a qualifying owner or officer formally chooses to operate outside the state workers compensation system for that person's own injury protection. In most states, corporate officers, sole proprietors, and LLC members can elect to be exempt if they own a specified percentage of the business, typically 10% or more, and file a formal Notice of Election to Be Exempt. If exempt, they forfeit all statutory benefits, including medical bill coverage and lost wage replacement, as outlined in this workers comp exemption overview.

It is an election, not a loophole

That trade-off is what many contractors miss. An exemption isn't free protection. It's a formal choice to give up protection.

A simple way to think about it is this. The contractor saves the premium tied to that person, but accepts that if the exempt person gets hurt on the job, there may be no workers comp benefits available for that injury. No automatic medical payment under the workers comp system. No wage replacement under that system either.

For contractors managing crews, payroll, and overtime rules, that distinction also gets mixed up with wage-and-hour classifications. Those are different issues. A useful primer on exempt vs nonexempt employees helps clarify that labor-law status and workers comp exemption status are not the same thing.

Going exempt can be lawful and still be a bad risk decision.

The HVAC owner example

Take a small HVAC company with one owner actively working in the field. The owner climbs attics, sets condensers, and handles service calls personally. The company elects an owner exemption to keep costs down.

Then the owner falls from a ladder during a rooftop access step on a replacement job. The business still has contracts to perform, payroll to meet, and customers waiting. But now the person who sells the work and performs the work is hurt, and the exemption means that person may have given up workers comp medical and wage-loss benefits.

For contractors with lean operations, that can be harder on the business than the premium ever was. One owner injury can stop production and cash flow at the same time.

A small contractor looking at workers comp for small business should weigh the exemption question against continuity, not just monthly cost. If the owner's labor is essential to finishing jobs, an exemption may create a hole bigger than it appears on paper.

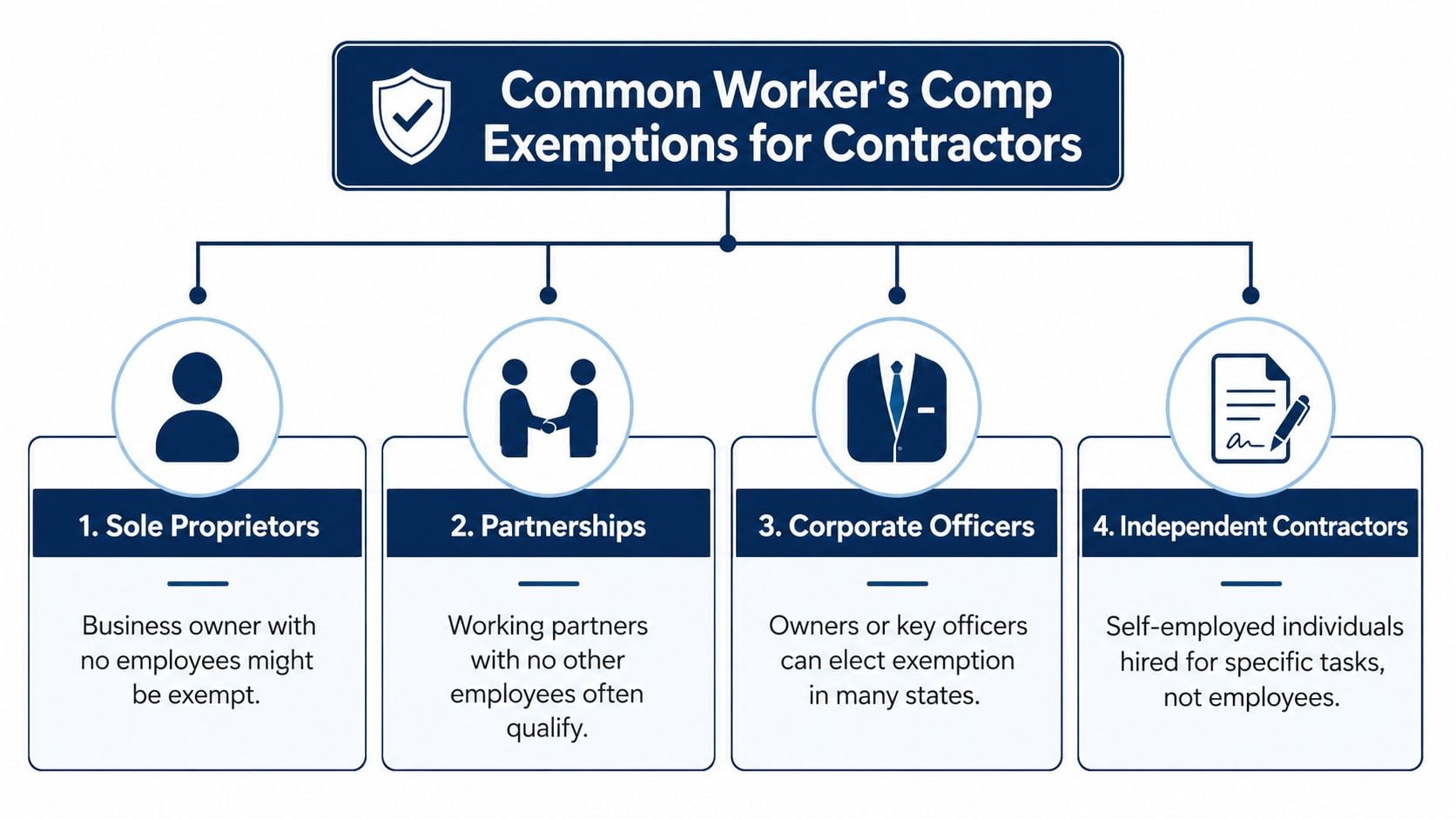

Who Can Be Exempt Common Categories for Contractors

Exemption rules vary by state, but contractors tend to run into the same categories over and over. The details matter because a label that sounds right on a job site can fail under scrutiny.

Owners working alone

A solo plumber working alone is often the cleanest example. If there are no employees and no laborers brought in for jobs, state rules may allow that owner to go without a workers comp policy or elect out if the business form requires it.

Many contractors often get comfortable too early. A solo setup stays simple only while it remains solo. The moment that plumber hires a helper for rough-in work, uses a laborer for demolition, or brings in someone for repeat trenching work, the analysis changes.

A lot of “one-man shop” businesses stop being one-man shops long before the paperwork catches up.

Officers and LLC members

A small roofing company with two owners organized as a corporation or LLC often falls into the officer exemption conversation. In many states, owners or officers can elect exemption if they meet the ownership and filing requirements.

That sounds straightforward. But the filing step matters, and the state-specific rules matter more. Some officers assume ownership alone is enough. It usually isn't. The election has to be properly made under the applicable state process.

For subcontracting trades, this issue often comes up when a general contractor asks for proof of workers comp. An owner saying, “I'm exempt,” may be accurate for that person, but it doesn't answer whether everyone else touching the work is covered. That's one reason contractors should understand how workers comp for subcontractors fits into bid review and subcontractor onboarding.

Family help and casual labor traps

Outdoor maintenance contractors, remodelers, and painters often rely on family members or short-term labor during busy periods. That's where contractors get burned by informal assumptions.

A contractor may call someone “just helping out for a few days,” but state law may not treat that person as exempt. The same problem shows up with casual labor. For construction trades, work is only considered casual employment and thus exempt from workers' compensation if it lasts no more than 20 days and the total labor cost is under $500 for the entire job, as explained in this state-by-state workers comp exemptions guide.

That threshold is tighter than many contractors expect.

| Situation | Common job site assumption | Practical risk |

|---|---|---|

| Owner's son helping on summer landscaping jobs | “He's family, so he doesn't count” | Family status alone may not solve coverage issues |

| Day labor on a small remodel | “It's casual work” | The job can exceed the casual labor threshold fast |

| Retired neighbor helping with cleanup | “He's not really an employee” | Injury can trigger a classification dispute |

Independent contractors

This is the category that causes the most damage. A tile installer, drywall finisher, or electrician may be paid on a 1099 basis and still not be treated as an independent contractor when an injury claim appears.

The contractor's day-to-day control matters. So does who sets schedule, supplies tools, directs methods, and controls the job relationship. Contractors working in Wisconsin can see how nuanced that analysis gets in this discussion of independent contractor workers' compensation Wisconsin.

The practical takeaway is simple. Calling someone an independent contractor doesn't settle the issue. The facts of the working relationship do.

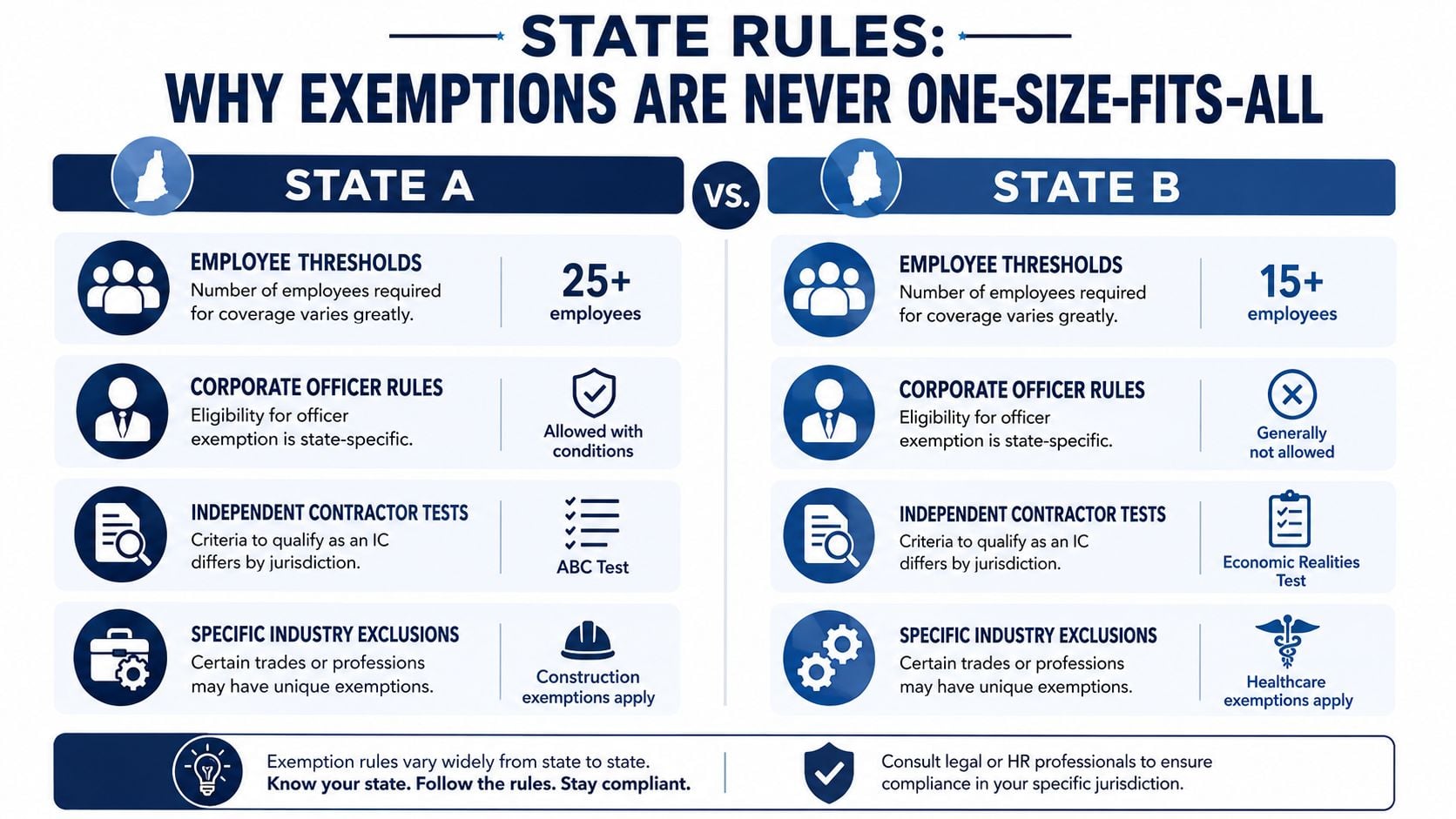

Why State Rules Change Everything for Your Trade

Contractors often ask for a national answer to workers comp exemptions. There isn't one.

State law drives who must carry coverage, who can elect out, which industries get special treatment, and how narrowly exemptions are interpreted. For construction businesses, those differences can be dramatic enough to change hiring decisions, subcontractor requirements, and even whether a job can be staffed the way the owner planned.

Construction rules can change at the state line

Florida is a good example of how strict construction rules can be. In Florida, construction businesses need workers' comp with one or more employees, including owners and partners treated as employees, while non-construction businesses need coverage only once they reach four or more employees. In Pennsylvania, exemption is only possible if all workers fall into specific exempt categories, and in Wisconsin, a closely held corporation with no more than two officers and no other employees can be exempt if both officers elect out, as summarized in this state comparison on workers comp exemption rules.

A framing contractor working in one state may be used to a narrow owner-only operation and assume the same setup works elsewhere. Cross into a stricter jurisdiction, and the contractor may suddenly need coverage for a crew structure that seemed acceptable at home.

That's why contractors bidding in multiple states should check workers comp requirements by state before they hire, not after a certificate request or injury report lands on the desk.

Narrow exemptions create false confidence

Pennsylvania shows how dangerous partial understanding can be. A contractor may hear that certain workers can be excluded and assume that means the business can avoid coverage. But if even one worker falls outside the exempt categories, the result can be very different from what the owner expected.

A mason contractor with one exempt officer and one nonexempt laborer doesn't have the same compliance position as a business where every worker fits a valid exempt category. That distinction matters because many exemption conversations happen casually at bid time, without anybody testing each worker against the actual state rule.

The mistake isn't usually bad intent. It's treating a state-specific rule like a general industry shortcut.

Different trades also get different scrutiny. Construction remains one of the least forgiving spaces for casual assumptions because work is physical, injury exposure is obvious, and subcontracting relationships are common. A paper exemption that looks fine in the office can collapse quickly when a site injury pulls in a state agency, a carrier, or a project owner.

The High Cost of Getting Exemptions Wrong

The biggest danger in workers comp exemptions isn't the form itself. It's the gap between what the contractor thinks the form solved and what happens after someone gets hurt.

A flooring contractor is a common example. The business wins residential and light commercial jobs, uses three installers treated as independent contractors, and pays each by the job. Everyone signs an agreement. Everyone invoices the company. On the surface, it feels clean.

Then one installer tears up a knee carrying material into a second-floor unit. That's when the true test starts.

The flooring crew scenario

If the injured worker says he was effectively part of the contractor's crew, a state board or agency may look past the label and inspect the facts. Who controlled the schedule? Who assigned the work? Who required attendance? Who supplied material? Who decided how the work had to be performed?

That's where many exemption-based labor setups fail. The burden of proof for independent contractor status rests entirely on the employer. With a sharp rise in state-level enforcement, including laws like California's AB5, independent contractors are frequently reclassified as employees after an injury, leaving the hiring contractor with no insurance to cover medical bills and lost wages, according to the Indiana Compensation Rating Bureau discussion of excluded workers.

For the flooring contractor, that means the “subcontractor model” may not protect the business at all if the facts point toward an employment relationship.

Why paperwork alone does not protect the contractor

Many contractors rely on three weak forms of comfort.

- A 1099 form: Tax treatment does not automatically settle workers comp status.

- A signed independent contractor agreement: Helpful, but only if the actual working relationship matches the document.

- Verbal understanding on the job site: This carries almost no weight when a claim is being examined.

A reclassification dispute can hit the contractor from several directions at once. First comes the injury itself. Then the question of unpaid premium exposure. Then the possibility of penalties, project fallout, and direct out-of-pocket responsibility where the contractor thought insurance would respond.

An exemption that works only until someone gets hurt was never much of an exemption.

The damage isn't limited to one claim. A general contractor may stop using that sub. A project owner may ask harder questions about compliance. Payroll records, contracts, and certificates may all get reviewed more closely. The issue starts with one knee injury or one fall. It rarely ends there.

That's why premium shopping and workers compensation insurance premiums should be viewed in context. The premium is a known cost. Misclassification exposure is an unknown cost with much worse timing. Contractors usually feel it when cash flow is already under pressure and jobs still need to be completed.

Smarter Choices Than Skipping Coverage

Contractors don't need a lecture. They need a workable plan that protects bids, keeps projects moving, and reduces the chance that one injury will blow up the business.

The smart move is usually not “find a way around workers comp.” It's “build a labor and insurance setup that can survive scrutiny.”

A better subcontractor control process

A remodeling contractor using specialty subs should have a repeatable vetting process before anyone starts work.

- Collect certificates early: Require a current certificate of insurance before the sub steps onto the project.

- Verify the policy matches the work: A certificate is only useful if the named business and coverage line fit the trade being performed.

- Use written agreements: Independent contractor agreements should describe scope, payment terms, and the independent nature of the relationship in plain language.

- Check for consistency: If the contract says the sub controls the work, the job site should reflect that reality.

- Review changes during growth: A sub who worked independently last year may function more like an employee now.

A concrete contractor, for example, might use an owner-operator for hauling one month and then begin directing that same person daily, setting hours, assigning routes, and supplying equipment access. The paperwork may stay the same while the risk changes completely.

When buying coverage is the cheaper decision

Some contractors spend too much effort trying to preserve an exemption that no longer fits the business they've built. Once the company has regular field labor, recurring subcontractor use, or owner dependence on personal field work, a right-sized policy is often the cleaner answer.

That doesn't always mean buying more insurance than needed. It means structuring coverage around actual payroll, actual job type, and actual crew makeup. For many trade businesses, that's easier to budget than the uncertainty created by borderline classifications and inconsistent subcontractor documentation.

A practical checklist for contractors looks like this:

- Map every person touching the job. Include owners, family helpers, laborers, and subs.

- Test each relationship accurately. Don't rely on what the crew calls someone.

- Match the labor model to state rules. Especially for construction.

- Require documentation before work starts. Not after an incident.

- Price insurance into the bid. Risk transfer belongs in the job cost.

Smart contractors transfer risk before the claim arrives.

The strongest trade businesses usually aren't the ones that avoid every premium. They're the ones that know where a legal exemption still creates a practical exposure, and they fix that gap before a worker gets carried off a site.

Contractors who aren't sure whether their current setup is compliant, affordable, or exposing the business to avoidable risk can get a free quote or coverage review from Coverage Axis. A licensed advisor can review crew structure, subcontractor use, trade class, and state requirements, then help build a workers comp program that fits the work.