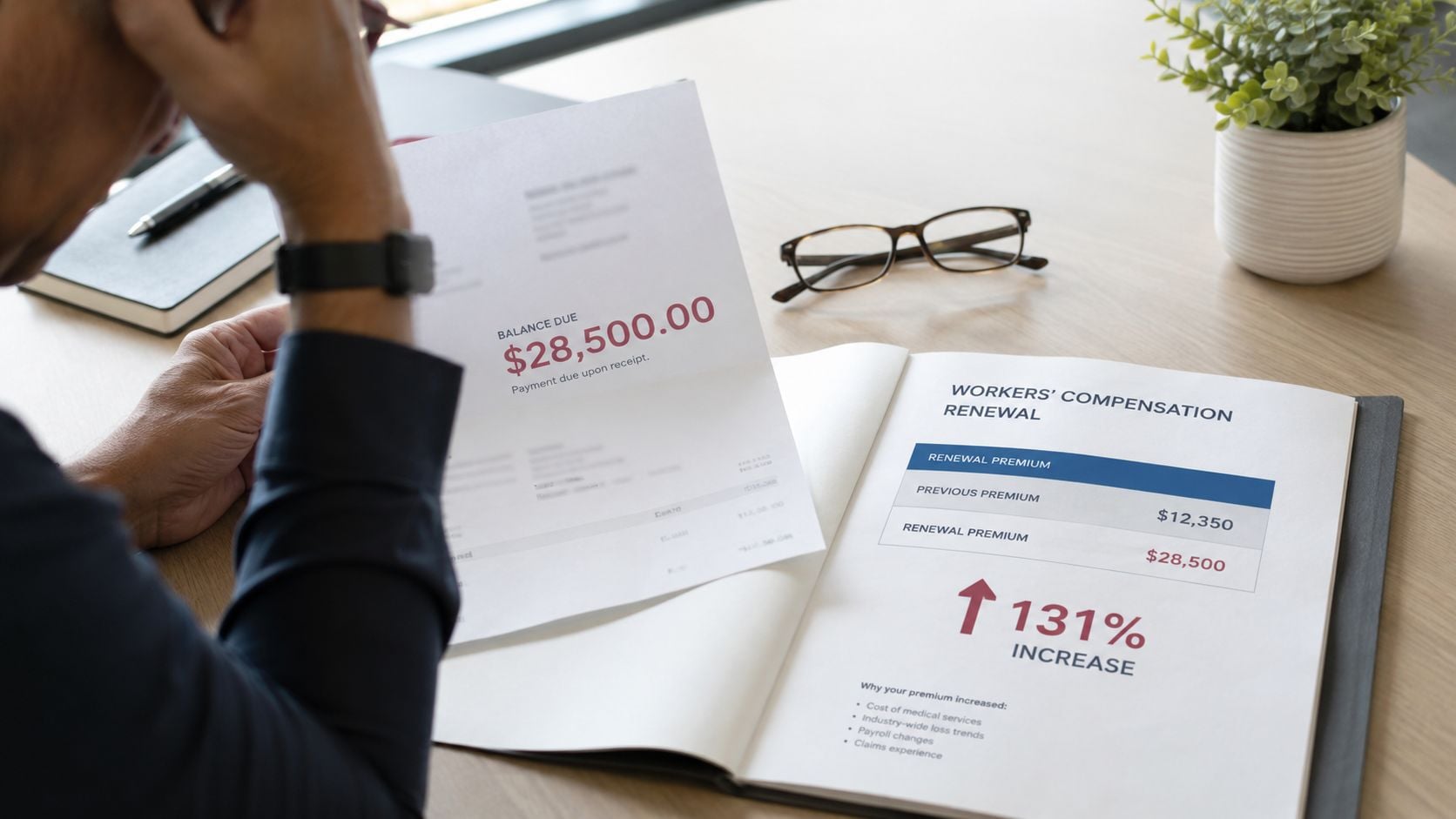

The renewal lands in the inbox on a Thursday afternoon. Payroll looks steady, claims haven't been dramatic, and the expectation is a routine signature. Then the premium is higher than expected, or worse, the audit letter says more premium is due because field payroll was assigned to the wrong class.

That surprise usually traces back to a small number on the policy. A workers comp class code looks harmless on paper, but it drives how the carrier prices the risk attached to the work being done. For a growing contractor, that number can change when the crew changes, when a new service line gets added, or when uninsured subcontractor labor gets pulled into the audit.

A roofing company that starts offering siding, an electrician that adds light concrete cutting, or a plumbing contractor that uses mixed in-house labor and subcontracted help can all outgrow the code setup that worked last year. That's where premium shocks start. The code issue isn't abstract. It hits cash flow, bid pricing, and profit.

Table of Contents

- Why Your Workers Comp Codes Matter More Than You Think

- Decoding the Numbers What Are Workers Comp Codes

- How Your Class Code Determines Your Premium

- A Field Guide to Common Construction Class Codes

- The High Cost of Misclassification Audits and Penalties

- Your Action Plan for Correct Workers Comp Codes

Why Your Workers Comp Codes Matter More Than You Think

A contractor can run clean jobs, keep the crew busy, and still get blindsided by workers comp cost. The problem often starts when the policy no longer matches the business that exists today. Last year's code setup may have fit a two-crew operation. It won't necessarily fit a company that's now doing service work, installs, and punch-list labor under one roof.

A common example is a small trade business that starts with one governing code, then grows fast. The owner hires a dedicated office person, adds a working foreman who still spends time on-site, and starts using labor subs during busy months. If payroll isn't separated properly and the policy isn't updated, the audit can treat a lot of that labor as higher-risk payroll.

That changes the bill after the work is already done.

Small code errors turn into large premium problems

Workers comp codes aren't just labels. They determine how payroll is rated. If a field crew is sitting in a lower-cost classification, the carrier will usually correct it at audit and collect the difference. If lower-risk staff are lumped into the governing field code, the business may overpay month after month without noticing.

A contractor should think of workers comp codes the same way they think about material takeoffs. If the inputs are wrong, the price is wrong.

Practical rule: If the business has added a service, changed crew structure, or started using more subcontractors since the last renewal, the class codes should be reviewed before the audit does it first.

The frustrating part is that most owners don't see the issue until money is already owed. The declarations page may list the code, but it doesn't explain what changed operationally to make that code incomplete or inaccurate.

The bottom-line impact shows up before a claim ever happens

Class code mistakes affect more than compliance. They affect bidding. A contractor who underestimates workers comp cost may submit jobs at margins that don't hold up after audit. A contractor who overstates field exposure may price work too high and lose jobs that should have been profitable.

For smaller firms trying to get a handle on payroll-rated coverage, a plain-English overview of workers comp for small business helps clarify why this line item behaves differently from many other insurance costs.

One code can change whether payroll is priced like office work or steep-slope field work. That isn't back-office trivia. It's a direct lever on profitability.

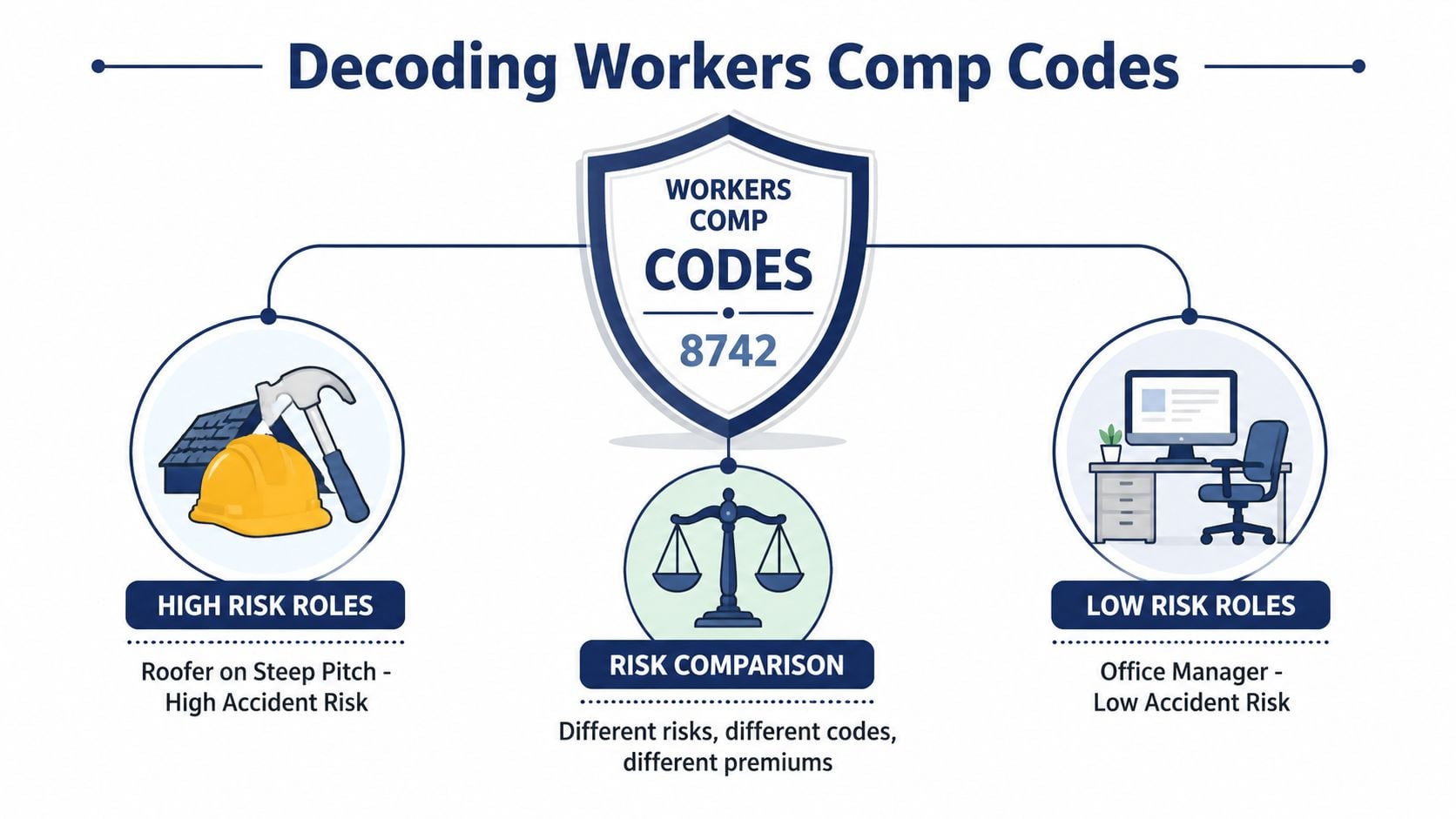

Decoding the Numbers What Are Workers Comp Codes

Workers comp codes are the rating labels attached to the actual work your people perform. They are usually 3- or 4-digit classification codes, and they tell the carrier whether payroll belongs with clerical work, plumbing, roofing, framing, or another type of exposure. If your company has grown since the last renewal, those codes may need to change too.

That matters most when a contractor expands operations faster than the policy setup keeps up. A painting company adds light carpentry. An electrical contractor starts trenching and site utility work. A GC that used to subcontract everything begins self-performing framing with its own crew. Those are the kinds of operational changes that can trigger a different classification approach at renewal or, worse, at audit.

The classification system used in many states is built around standardized class descriptions published by NCCI, which maintains hundreds of workers compensation class codes and the governing rules behind them, as described on the NCCI class codes and statistical codes resource page. Contractors do not need to memorize the full code set. They do need to know that code selection is rule-based, and small changes in operations can move payroll into a different bucket.

The code follows the work, not the title

Classification problems usually start with internal labels that sound clean on a payroll report but do not match field reality.

A "project manager" who spends four days a week on active sites, climbs ladders, checks installs, and directs crews is not viewed the same way as an office employee who handles schedules and submittals from a desk. A helper and a lead installer often stay in the same field code if they are exposed to the same job conditions. The carrier and auditor look at duties, jobsite presence, and the governing operation.

Growing contractors often find themselves surprised. Owners often keep the original code setup from years earlier, even after the business adds new services or mixes office, shop, and field staff differently. If payroll is still assigned the old way, the audit can reclassify it after the policy period ends and bill the difference.

Expansion, mixed crews, and subs complicate coding

Real jobs rarely fit neat org charts. One crew may handle service calls in the morning and installation work in the afternoon. A remodeling contractor may use employees for demo and carpentry while hiring uninsured subcontractors for drywall or flooring. If records are weak, auditors often default payroll into the governing class with the higher exposure.

That is expensive.

Contractors should also separate workers comp coding from claim categories. The policy code determines how payroll is rated. A claim is later sorted by injury type and legal issues. For readers who want that claims-side context, this overview of 5 workers' comp classifications is a useful companion reference.

A good operating habit is to review class codes any time the business adds a trade, changes who self-performs work, opens a shop, or increases subcontractor use. That review should happen before renewal and before the auditor asks questions. Contractors who want a clearer view of how classification feeds into cost can also review this guide to workers compensation insurance premiums.

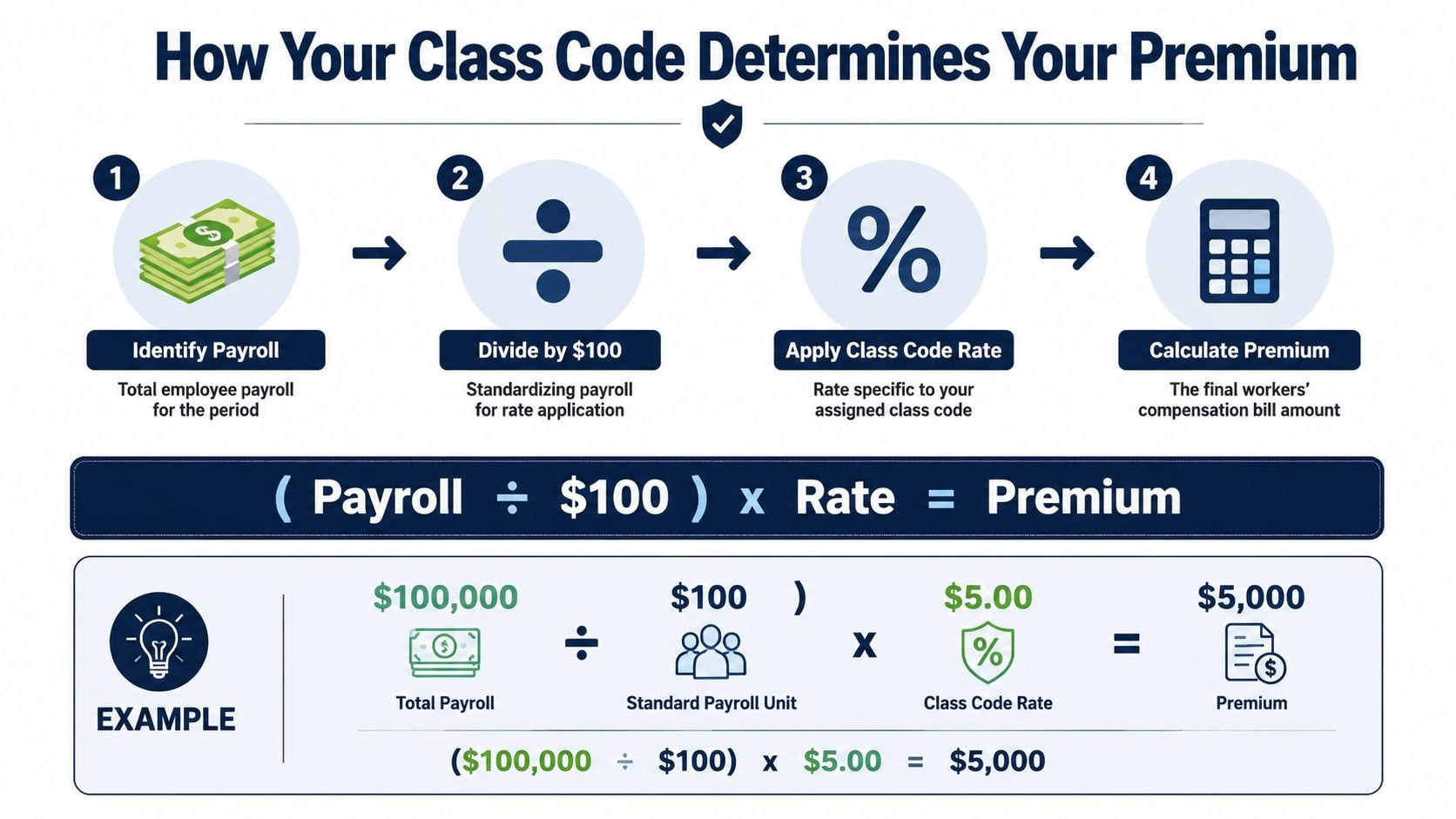

How Your Class Code Determines Your Premium

A contractor can run payroll all year, pay the deposit, and still get hit with a large audit bill because the work changed faster than the policy did. That usually starts with class code drift. The company began the year doing one type of work, then added service work, took on a higher-risk trade, expanded crews, or used more subcontractors. The premium followed the old code until the audit caught up.

Workers comp pricing starts with a simple formula. (Payroll ÷ $100) x Rate = Premium. The part that swings the cost is the rate, and the rate follows the class code attached to that payroll.

Two contractors can have the same payroll and pay very different premiums because the work is different. Structural steel, roofing, and concrete are priced higher than clerical or outside sales for an obvious reason. Falls, tools, heavy material handling, and active job sites produce a very different injury profile.

That difference gets expensive fast.

Same payroll, different code, different bill

Take a growing mechanical contractor with a crew that used to do light plumbing service and now also installs equipment on larger commercial jobs. If payroll stays under the old code all year, the policy can look underpriced from the carrier's side. At audit, the higher-rated operation may be pulled into the right class and the contractor gets billed for the difference after the money is already spent.

That is why class code review should happen when operations change, not just at renewal.

The same problem shows up with mixed crews. An electrical company may have office staff, estimators, warehouse help, and field electricians on the same payroll system. Field electricians are rated for field exposure. Clerical employees can often be reported separately if they meet the rule requirements. If the records are sloppy, payroll usually does not get the benefit of those distinctions.

Growth changes the premium math

Class codes are not static for a contractor that is growing.

A plumbing shop that adds excavation, a remodeler that starts self-performing framing, or a GC that brings more labor in-house can all trigger a different pricing outcome. The premium changes because the exposure changed. Carriers and auditors care about what employees did during the policy period, not what the business was doing two years ago.

Subcontractors add another layer. If uninsured subs are used, their labor can be picked up in the audit and charged under the class code that fits the work performed. If that work is higher hazard, the added premium can be significant. I see this catch contractors by surprise when they assume subcontracted work is automatically off their books.

Three operating rules help keep the premium tied to reality:

- The main field operation usually drives the governing class. The code should reflect the work that defines the business, not the lowest-risk task on payroll.

- Separate classifications only work when records support them. Clerical, outside sales, and some distinct operations need clean payroll separation and job descriptions.

- New services should trigger a code review right away. Waiting until the year-end audit usually means finding out about the change as a bill, not as a planning decision.

Contractors who want a clearer breakdown of the pricing mechanics can review this guide to workers compensation insurance premiums.

The practical takeaway is simple. Your premium is not based on payroll alone. It is based on payroll matched to the right work, and growing contractors are the ones most likely to see that match change mid-policy.

A Field Guide to Common Construction Class Codes

Most contractors don't need the entire classification manual. They need a practical way to sanity-check the codes tied to their crews. The table below covers common construction and trade examples that frequently show up on policies.

The code always has to match the actual operation. A company can have one governing code and additional classifications for qualifying support staff or separate operations. But the description matters as much as the number.

Common workers comp codes contractors should recognize

The NCCI classification structure includes nearly 800 unique four-digit class codes, and construction trades like roofing and concrete often sit in distinctly higher-cost categories because the work itself carries higher injury exposure, according to this overview of common workers comp class codes.

| Trade | Common code | Typical work covered | Relative cost level |

|---|---|---|---|

| Roofing | 5403 | On-site roofing operations, material handling, installation | High |

| Concrete work | 5170 | Pouring, finishing, rebar-related concrete operations | High |

| Electrical | 5190 | Wiring, panel work, troubleshooting, on-site electrical labor | Medium to high |

| Plumbing | 5180 | Pipefitting, fixture installs, drain-related plumbing service | Medium to high |

| Structural steel | 5000 | Steel erection and related structural field work | High |

| Clerical office | 8810 | Pure office duties with no field exposure | Low |

That table isn't a substitute for underwriting review, but it's a strong first filter. If a roofing company's declarations page doesn't look like a roofing operation, that's a signal to stop and review the file.

Trade example for a concrete contractor

Take a concrete contractor with a small office team and a field crew that pours, finishes, and ties rebar. The field labor generally belongs under the concrete code, while a true office employee may qualify separately if the duties are strictly clerical.

The expensive mistake is blending everyone into one bucket without support. The other expensive mistake is trying to force field labor into a cheaper office code because one employee also handles scheduling or purchasing part of the day. Carriers and auditors focus on the governing operation and actual exposure.

For contractors in that trade, it's worth comparing the policy setup against common issues in concrete contractor insurance, especially when the business includes pumping, forming, hauling, or multiple crews with different scopes.

What doesn't work

A few habits repeatedly create problems:

- Using generic descriptions: "Construction" is too broad to support accurate classification.

- Relying on job titles: Titles don't override actual duties.

- Ignoring service creep: A company that starts with one trade often expands before the policy catches up.

A field guide only helps if it's used before renewal and before audit. Once the labor is booked and the records are muddy, the contractor loses their advantage.

The High Cost of Misclassification Audits and Penalties

Misclassification cuts in both directions. Understating exposure can lead to a surprise balance due at audit. Overstating exposure can mean paying too much all year long. Neither outcome helps a contractor who is trying to protect margin.

The more dynamic the business becomes, the easier it is for the policy to fall behind reality. A plumbing contractor adds a new service line. A roofing business starts offering siding. A general trades firm leans harder on subcontracted labor during peak season. If those changes don't show up clearly in payroll and insurance records, the audit usually becomes the moment of truth.

Subcontractor labor is where many audits go sideways

Subcontractor handling is one of the most misunderstood parts of workers comp. If a subcontractor doesn't carry compliant coverage, or if the paperwork is incomplete, the hiring contractor may see that labor pulled into its own audit exposure depending on the state rules and the facts of the relationship.

Recent Ohio Bureau of Workers' Compensation data from 2025 shows that 34% of mid-sized contractor audits involve misclassified subcontractor labor, leading to an average 22% premium adjustment, as summarized by Coverage Axis on contractor audit issues.

That matters well beyond Ohio because the operational mistake is common everywhere. The contractor assumes the sub is independent. The auditor asks for certificates, payroll support, and work descriptions. The file is incomplete. Premium goes up.

For businesses that also place labor or operate in hybrid labor models, operational systems matter. Resources on staffing agency solutions can help owners think through worker tracking and assignment visibility, which is often where classification issues begin.

Overpaying is quieter, but still expensive

Not every mistake results in a big audit invoice. Some businesses sit in the wrong high-cost code for months because nobody revisits the classifications after the company changes.

A simple example is a contractor that separates part of the operation into lower-hazard support roles but never reports that split cleanly. The business keeps paying field rates on payroll that may have qualified differently. That doesn't create a dramatic audit letter. It just drains cash.

Keep certificates, subcontract agreements, payroll records, and job descriptions organized before the auditor asks. If those records are missing, the carrier usually interprets the exposure in the least favorable way for the contractor.

State rules also matter. A contractor working in multiple jurisdictions should review workers comp requirements by state before assuming one coding or subcontractor rule applies everywhere.

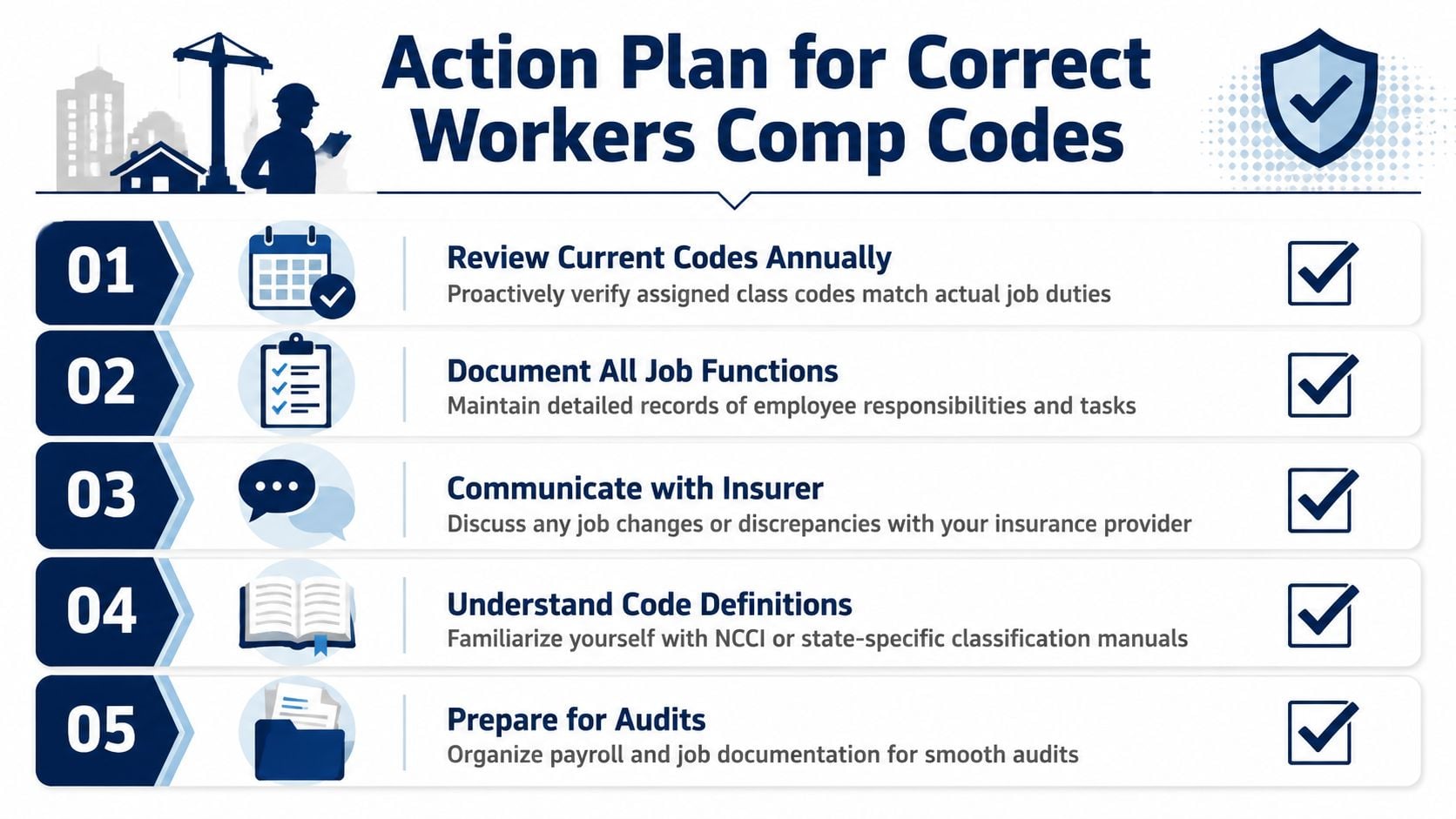

Your Action Plan for Correct Workers Comp Codes

A contractor doesn't need to memorize every code in the manual. The practical goal is to keep payroll, job duties, and subcontractor records clean enough that the policy mirrors the actual business. That matters most when the company is growing.

One recurring blind spot is business evolution. A roofing contractor that adds siding may trigger a shift from 5403 to 5405, and that change can involve a 12-18% premium variance, as noted in Coverage Axis guidance on contractor code changes. That's why code review can't be a one-time setup task.

Review operations before renewal, not after audit

Start with the business as it exists today.

- List each revenue-producing service: Roofing, siding, electrical, concrete repair, service calls, shop fabrication, and delivery should be identified separately if they exist.

- Match payroll to actual duties: If an employee splits time, the records should show when and where that labor occurred.

- Flag anything new: A recently added trade or specialty service is often where the class code setup falls behind.

A useful companion for contractors tightening up their documentation is this estimate code compliance checklist. It helps translate job scope thinking into a more disciplined review process, especially when service offerings are expanding.

Build payroll records that can survive an audit

Messy payroll is where good intentions fall apart. If payroll can't be separated by operation, the auditor may classify it broadly.

Good records usually include:

- Job-cost detail: Labor tied to project type and work performed.

- Crew clarity: Which employees worked roofing, siding, electrical, or concrete tasks during the period.

- Separate clerical support: Office-only payroll tracked distinctly from field labor when the duties qualify.

A contractor adding new services should update payroll coding immediately. Waiting until year-end invites reconstruction from memory, and memory is weak evidence in an audit.

Tighten subcontractor paperwork

Subcontractor files should be current, complete, and easy to retrieve. That means certificates of insurance, effective dates, and written agreements that fit the labor arrangement. If the subcontractor's coverage lapses or the role looks more like leased labor than an independent trade contractor, the audit exposure can change quickly.

Jobsite advice: If a subcontractor's file can't be produced in a few minutes, the workers comp exposure probably isn't under control.

Challenge the code when the description is wrong

Contractors shouldn't assume the policy is correct just because it was issued. If the code description doesn't match the operation, gather support and raise the issue early. Useful documents include job descriptions, payroll breakout reports, contracts, invoices, website service descriptions, and project schedules showing the actual scope of work.

When payroll and classification are being reviewed, it's also smart to monitor the business's workers comp experience modification, because the interaction between losses, payroll, and classification can materially affect future pricing.

The contractors that control workers comp costs best usually do three things well. They review codes every renewal, document operational changes as they happen, and treat the audit like a financial event rather than an administrative nuisance.

If the current workers comp setup no longer matches the way the business operates, a second review can prevent expensive surprises. Coverage Axis provides free quotes and coverage reviews for contractors who need workers comp that fits their trade, payroll structure, crew mix, and subcontractor exposure.