A lot of concrete contractors hit the same wall at the same point. The takeoff is done, the labor is figured, the material price is tight, and the job looks worth chasing. Then the bid package lands with insurance language that reads like a second contract. It asks for general liability, workers' comp, auto, maybe additional insured status, maybe a bond, maybe higher limits than the company carries now. The job can be buildable on paper and still be unwinnable if the insurance program isn't built for it.

That's why concrete contractor insurance isn't just overhead. It affects whether a crew can mobilize, whether equipment losses turn into cash flow problems, and whether a finished slab becomes a closed file or a lawsuit months or years later. Concrete work has a long memory. A crack, settlement complaint, or drainage issue often doesn't show up on punch day.

The smart move is to treat insurance the same way a contractor treats mix, subgrade, weather, and cure time. It has to fit the work. A residential flatwork crew doesn't need the same structure as a contractor pouring commercial foundations, and a policy that looks cheap at renewal can get expensive fast when a claim shows up after the project is already off the books.

Table of Contents

- Why Your Insurance Matters as Much as Your Mix Design

- The Four Foundational Policies for Concrete Contractors

- Protecting Your Equipment Onsite and In Transit

- How Jobsite Risks and Past Work Affect Your Premiums

- Winning Bigger Bids with COIs and Surety Bonds

- When to Add an Umbrella Policy for Ultimate Protection

- How to Get the Right Insurance Program for Your Business

Why Your Insurance Matters as Much as Your Mix Design

A common scenario goes like this. A concrete subcontractor prices a commercial slab job, lines up labor, confirms pump access, and gets ready to submit. Then the owner's contract requires limits, endorsements, and certificates the business has never had to produce on a smaller project. The estimate was right, but the insurance program was too small for the opportunity.

That happens more often than most contractors expect. Insurance controls who gets through procurement, who can satisfy a general contractor's paperwork, and who gets pushed aside before anyone compares field experience. The policy set behind the company can matter as much as the company's production ability.

A contractor that understands general contractor insurance requirements early usually makes better bid decisions. That contractor can look at the insurance section before spending hours on estimating and decide whether the job fits the current program, needs a policy change, or needs bonding lined up first.

Insurance changes what work a contractor can pursue

For a concrete company, insurance does three jobs at once:

- It protects the balance sheet: A vehicle accident, an injury claim, or a stolen machine can turn into a direct hit on cash if the wrong policy is in place.

- It protects scheduling: A carrier that can issue certificates and endorsements quickly helps keep mobilization from stalling.

- It protects reputation: Owners and general contractors want subs who can meet requirements without last-minute scrambling.

Practical rule: If a policy only gets reviewed at renewal, it's already behind the business.

A patio and driveway contractor may mostly need a clean, dependable setup that handles routine exposures well. A contractor doing walls, foundations, or public work needs something more deliberate. That business has more contract review, more equipment exposure, and more completed-work risk after the forms are stripped and the crew is gone.

Cheap insurance often costs more later

The wrong way to buy concrete contractor insurance is to focus only on the premium and ignore how the work behaves. Concrete claims aren't always immediate. Some losses are obvious on the day they happen. Others surface after weather, load, settlement, or owner use exposes a problem.

That's why the better question isn't “What's the cheapest policy?” It's “Will this program still protect the business when the claim shows up after closeout?” For concrete contractors, that question matters more than most basic insurance guides admit.

The Four Foundational Policies for Concrete Contractors

Most concrete businesses need four policies at the core of the program. Everything else usually builds on top of them. If one of these is missing or poorly structured, the company is operating with a hole in the floor.

General liability handles the mess that spreads beyond the pour

General liability is the policy contractors usually think about first, and for good reason. It's built for third-party bodily injury and property damage claims. In plain language, it responds when the company's operations allegedly hurt someone else or damage someone else's property.

A concrete example is simple. A crew washes out too close to finished landscaping, or slurry gets where it shouldn't, and the property owner wants the damage fixed. Another example is a pedestrian or site visitor tripping over materials, cords, or uneven access around the work area.

For contractors comparing options, it helps to understand how general liability insurance for contractors is supposed to fit active jobsites instead of treating it like a generic business policy.

Workers comp protects the crew doing heavy work

Concrete crews lift forms, handle wet material, work around moving equipment, and spend long days repeating hard physical motions. Workers' compensation exists for the claims that come from that environment. If an employee strains a back carrying forms, gets hurt around placement equipment, or is injured doing normal work duties, workers' comp is the first place the claim usually goes.

This policy is also part of staying compliant as an employer. If the business has payroll, the workers' comp structure has to match who is on the crew and what roles they perform.

The crew is the production engine. If an injury claim isn't handled cleanly, the damage goes beyond medical bills. It disrupts manpower, scheduling, and morale.

Commercial auto follows the trucks between jobs

Concrete businesses depend on pickups, flatbeds, service trucks, and sometimes heavier units to move people, tools, and material between shop and site. Personal auto coverage isn't built for that exposure. Commercial auto is.

A realistic claim scenario is a company truck rear-ending another vehicle while hauling tools to a morning pour. Another is a site run that turns into a liability issue because the vehicle is titled to the business and being used for business purposes.

Inland marine protects mobile gear

Concrete contractors don't make money with equipment sitting in one place. They move bull floats, forms, vibrators, saws, screeds, generators, and heavier machines from yard to trailer to jobsite and back again. That mobility creates a gap if the contractor assumes standard property insurance covers everything everywhere.

Inland marine, often called contractor's tools and equipment coverage, serves this purpose. It's designed for property that travels with the work.

Core Concrete Contractor Insurance Coverages

| Coverage | What It Protects | Trade-Specific Example |

|---|---|---|

| General Liability | Third-party injury and property damage claims | Wet concrete or runoff damages adjacent property |

| Workers' Compensation | Employee injury claims arising out of work | A finisher strains a back lifting forms |

| Commercial Auto | Business-owned vehicles used in operations | A company pickup causes an accident on the way to a pour |

| Inland Marine | Mobile tools and equipment away from the shop | A screed or skid-steer is damaged or stolen at a jobsite |

A contractor can add other policies later, but these four do the heavy lifting first. Without them, the company is exposed on the road, on the site, and after an ordinary workday turns into a claim.

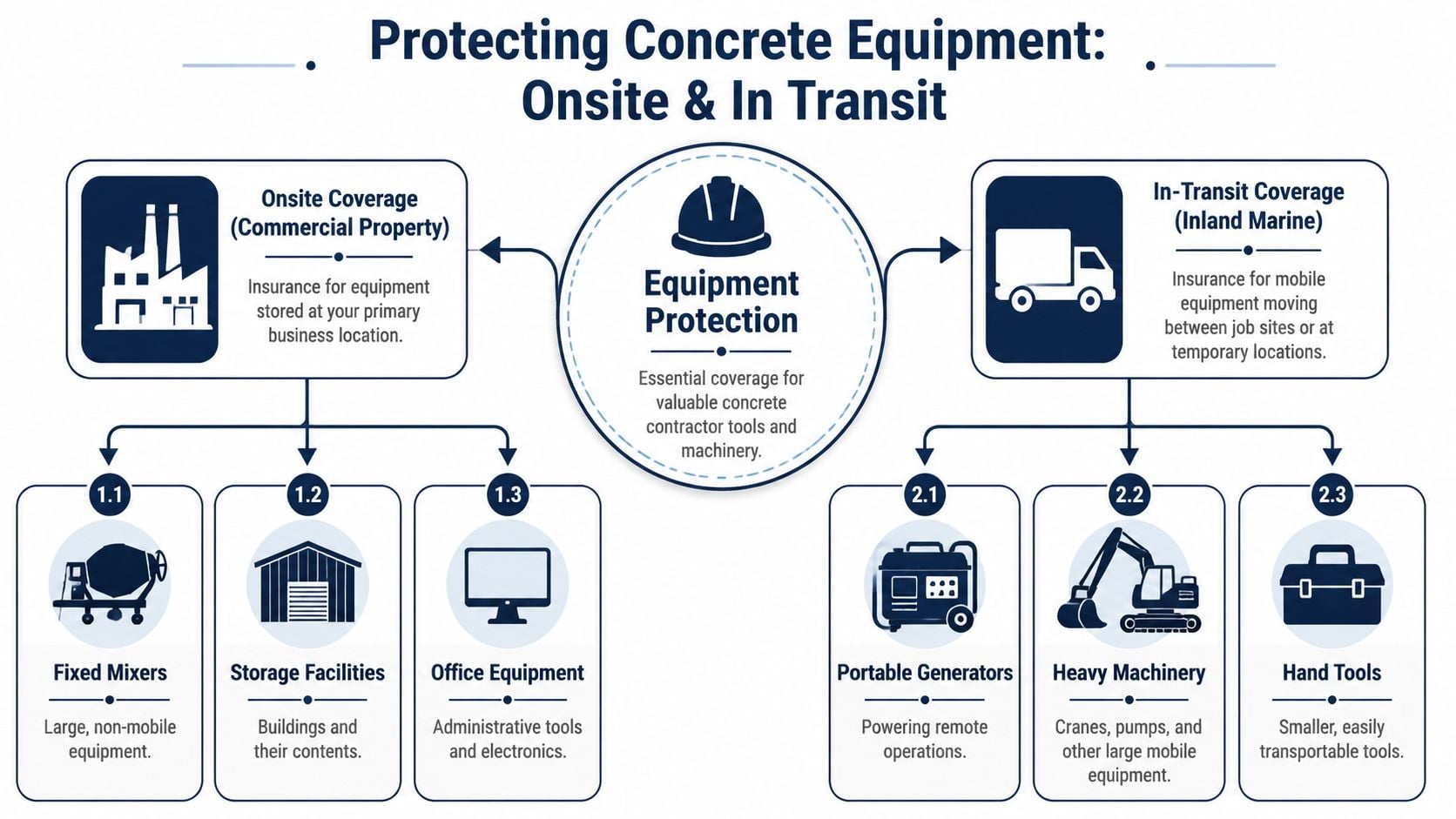

Protecting Your Equipment Onsite and In Transit

Concrete contractors usually feel equipment losses immediately. A stolen hand tool hurts. A missing skid-steer, damaged screed, or vandalized set of forms can shut down production.

Why shop coverage and jobsite coverage are different

This is one of the biggest points contractors miss. Standard commercial property insurance is location-based. It covers tools and equipment at the business address, while contractor's tools and equipment coverage follows items in transit and at the jobsite. For concrete contractors, that matters because the gear is constantly moving, and crews rely on mobile assets such as vibrators, skid-steers, laser screeds, bull floats, form panels, pumps, and mixers that can be stolen, vandalized, or accidentally damaged overnight or while traveling between sites, as noted in this concrete contractor equipment coverage explanation.

If the business stores fixed items at the yard and assumes that same protection automatically applies once the equipment is loaded onto a trailer, that assumption can get expensive fast. The loss often happens away from the premises.

Equipment losses usually hit operations first

Take a real-world style example. A crew leaves a skid-steer and laser screed on a dark site because the next pour starts early. Overnight, one machine is stolen and the other is vandalized. The cost isn't just repair or replacement. The contractor may also lose production time, reschedule labor, and scramble for rental equipment.

That's why storage and transport planning matter alongside insurance. Contractors trying to reduce overnight theft exposure often look at secure offsite options such as Container Self Store business tool solutions when a site has poor lighting or weak perimeter control.

A practical equipment review should include:

- What stays at the yard: Mixers, office contents, and shop property may fit under property coverage.

- What travels daily: Saws, floats, generators, vibrators, and compact equipment usually need coverage that follows them.

- What sits overnight on jobsites: These are often the pieces most exposed to theft and vandalism.

- What rides on company vehicles or trailers: Transit losses need to be addressed clearly, not assumed.

A contractor's property schedule should read like the actual trailer and yard list, not a rough guess from memory.

Contractors that depend heavily on pickups, service bodies, and trailers should also make sure the equipment discussion lines up with the vehicle side of the program. A commercial auto policy quote for contractor fleets is only one piece of that picture. The tools and machines riding with those vehicles need their own review.

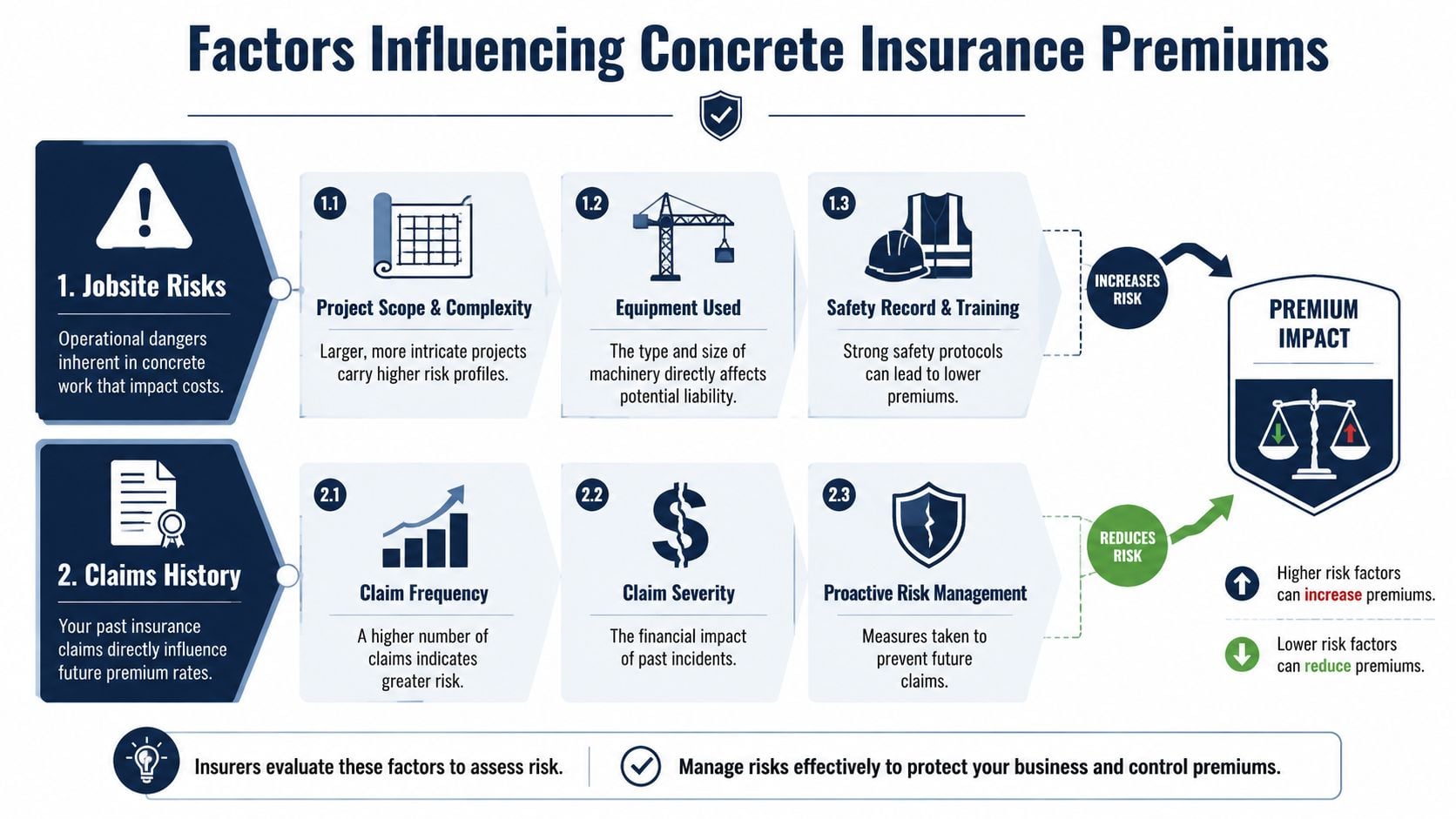

How Jobsite Risks and Past Work Affect Your Premiums

Premiums don't come out of thin air. Carriers price what the contractor does, where the work happens, what the crew uses, and how the company has handled losses before. A concrete business that places patios and sidewalks presents one kind of exposure. A contractor doing deeper structural work, more traffic-heavy jobs, or more complicated placements presents another.

Underwriters price what the crew actually does

Underwriters usually pay close attention to a few practical items:

- Project type: Flatwork, foundations, walls, and other scopes don't all carry the same downstream risk.

- Jobsite conditions: Congested sites, public access, nearby structures, and tight staging areas create more chances for damage or injury.

- Vehicle and equipment use: More road time and heavier gear mean more ways for claims to happen.

- Claims history: Frequency matters, but so does severity. One ugly loss can change how a carrier views the account.

A lot of contractors focus on payroll and revenue because those are obvious underwriting inputs. The less obvious factor is operational discipline. Clear jobsite controls, driver screening, equipment handling standards, and documented safety practices often make the account easier to place.

For employers watching labor-related costs, understanding workers comp experience modification helps connect claim performance to future pricing pressure.

Completed operations is where concrete gets tricky

This is the part many concrete businesses don't hear enough about. A major underserved issue is completed-operations risk. Concrete defects such as cracking or settling can show up well after the pour, and those claims can be costly to defend. Some public discussions of contractor insurance mention general liability, workers' comp, and equipment, but don't spend enough time on post-job failures, policy duration, claims-made versus occurrence structure, or whether subcontracted work is protected, even though those details can decide whether a later claim is covered, as explained in this discussion of concrete completed-operations exposure.

A simple trade example makes the point. A contractor pours a residential foundation or a commercial slab, closes out the job, and moves on. Later, the owner alleges cracking, movement, or damage tied to the original work. By then, the project file may be archived, the superintendent may be on other jobs, and the contractor may not even have the same insurance setup if the business changed carriers or bought a bare-bones renewal.

The cheapest liability policy can be the wrong policy if the claim arrives after the dust settles.

That long-tail exposure is why concrete contractor insurance should be reviewed with the completed-work timeline in mind, not just the immediate site hazards. A policy has to make sense for the active phase of the work and for the period after the contractor leaves.

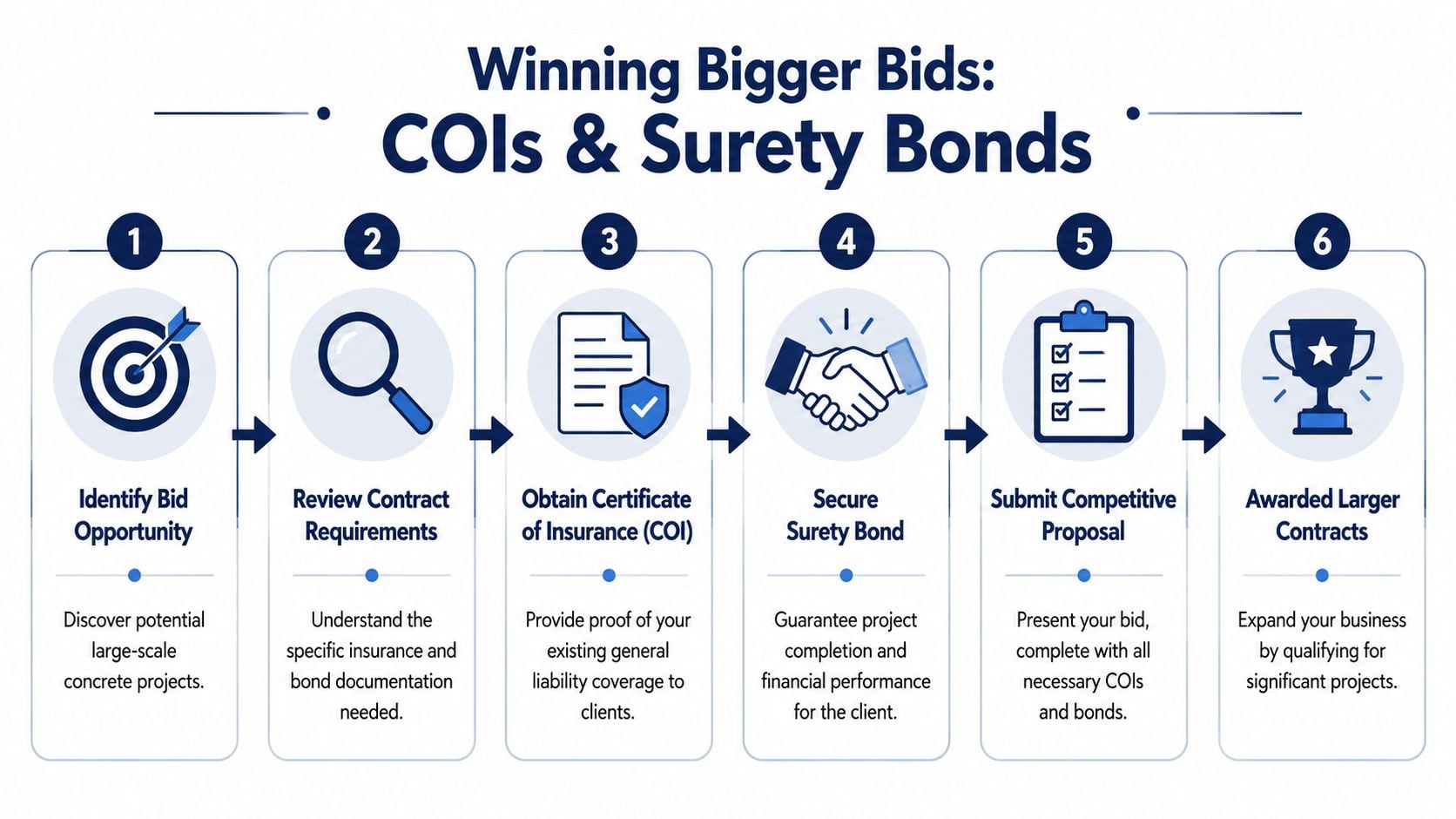

Winning Bigger Bids with COIs and Surety Bonds

A lot of contractors think insurance starts protecting the business only after a loss. On bigger jobs, it starts working much earlier than that. It helps the business qualify.

Paperwork qualifies the contractor before the work does

Owners, public entities, and general contractors often ask for proof before they care about production capacity. That means certificates of insurance, endorsements, and sometimes bond documents have to be ready and accurate.

A public-contract example from Louisiana requires commercial general liability at $1,000,000 per occurrence and $3,000,000 aggregate, workers' compensation with statutory limits plus $1,000,000 employers' liability, and commercial auto with a $1,000,000 combined single limit when vehicles are used on the job, according to these contractor insurance requirements. Those aren't abstract numbers on a form. They can decide whether a concrete contractor can even submit a compliant package.

A practical bid issue looks like this:

- The estimator prices the work correctly

- The contract requires higher limits or specific endorsements

- The contractor can't produce the COI package in time

- The opportunity stalls before the field team gets a chance

That's why insurance administration matters. A slow certificate process can cost real work even when the contractor is otherwise qualified.

Bonding affects both eligibility and cash flow

Surety bonds are different from insurance, but they live in the same conversation because they enable work. Washington requires contractors to register with L&I and carry a $12,000 surety bond, and many project owners or municipalities also require payment and performance bonds. One industry source notes those bonds may be priced at about 3% of the contract price for jobs under $400,000 when credit is strong, which means credit quality and bonding capacity can directly change the cost of chasing work, as noted in the same contractor bonding requirements reference.

That has two practical consequences. First, a contractor may be technically capable of doing the work but still unable to qualify if the bond program is too limited. Second, a contractor with weak bonding terms can win a job and still feel pressure on margins and cash flow from the bond cost.

Bigger bids don't just require better estimating. They require paperwork capacity, carrier support, and enough financial credibility to satisfy bond underwriters.

For concrete contractors trying to move from smaller private jobs into public or larger commercial work, this is often the point where insurance shifts from expense to growth tool.

When to Add an Umbrella Policy for Ultimate Protection

At a certain size, primary liability limits stop feeling comfortable. The contractor may own more vehicles, work on larger sites, or has more at risk if one severe claim gets out of hand.

A severe loss can outrun a primary policy

A straightforward example is a company truck causing a major multi-vehicle accident while heading to a site with employees, tools, or materials. The commercial auto policy responds first, but severe injury allegations and legal costs can climb fast. If the claim blows through the underlying limit, the contractor can end up facing the excess without another layer in place.

That's where umbrella coverage comes in. It sits over certain primary liability policies and provides additional protection when a covered claim exhausts the underlying limit. It doesn't replace general liability or auto. It extends the protection above them.

Contractors comparing options usually benefit from understanding how commercial umbrella insurance fits over the rest of the liability tower before a contract requires it or a severe loss tests it.

When an umbrella starts making sense

An umbrella often becomes worth serious consideration when the business starts checking boxes like these:

- Larger contracts: Bigger jobs tend to come with stricter insurance expectations.

- More vehicles on the road: More road exposure means more chances for a serious auto claim.

- Higher asset value: As the company builds trucks, equipment, receivables, and retained earnings, it has more worth protecting.

- Broader public exposure: More activity around occupied sites, traffic areas, or larger commercial work increases liability stakes.

A small contractor doing tightly controlled local work may not need to rush into an umbrella immediately. A growing concrete company with multiple crews, public-facing operations, or larger commercial contracts usually shouldn't wait too long. The umbrella is there for the bad day that doesn't fit inside ordinary limits.

How to Get the Right Insurance Program for Your Business

The best insurance program usually starts with better information, not faster shopping. A contractor that hands over clean details gets cleaner quotes and fewer surprises later.

A practical checklist before requesting quotes

Start with the operating facts the carrier will ask for anyway:

- Payroll details: Separate field labor from office staff as clearly as possible.

- Revenue by operation: Break out the kind of work performed, such as flatwork, foundations, or other concrete scope.

- Vehicle list: Include who drives what and how each unit is used.

- Equipment inventory: List the tools and machines that move between jobs.

- Loss history and current policy copies: These help show what has been happening and what the business carries now.

Contracts should be reviewed before the quote process is done, not after. If a customer needs additional insured wording, waiver language, bond support, or higher limits, those items should be part of the discussion up front.

What to ask before binding coverage

The smartest questions are practical ones:

- Does the policy fit the actual jobs the company performs?

- How does it handle mobile equipment and overnight jobsite exposure?

- What does the liability structure look like for completed work?

- How quickly can certificates and endorsements be issued when a bid turns hot?

For contractors trying to streamline paperwork after coverage is selected, resources on automating insurance document signing can help reduce delays in getting forms executed and returned.

One option in the market is Coverage Axis, which works with construction and trade businesses by shopping multiple carriers and helping organize coverage lines such as general liability, workers' comp, auto, inland marine, umbrella, and surety support around the contractor's actual operations.

If a concrete business needs a program that fits the work, protects equipment, and holds up when completed-work claims show up later, request a free quote or no-obligation coverage review from Coverage Axis.