A California contractor wins a tenant improvement bid on Friday afternoon. The scope looks solid. The pricing works. Then the project manager sends over the insurance requirements. Suddenly the job isn't about drywall, ducting, concrete, or finish work. It's about terms like $2 million aggregate, additional insured, completed operations, and a certificate deadline that has to be met before anyone steps on site.

That's where a lot of contractors get jammed up. The work is familiar. The paperwork isn't. And in California, insurance paperwork isn't just back-office admin. It affects whether a contractor can keep a license active, satisfy a project owner, hire crews correctly, and avoid paying for someone else's claim out of pocket.

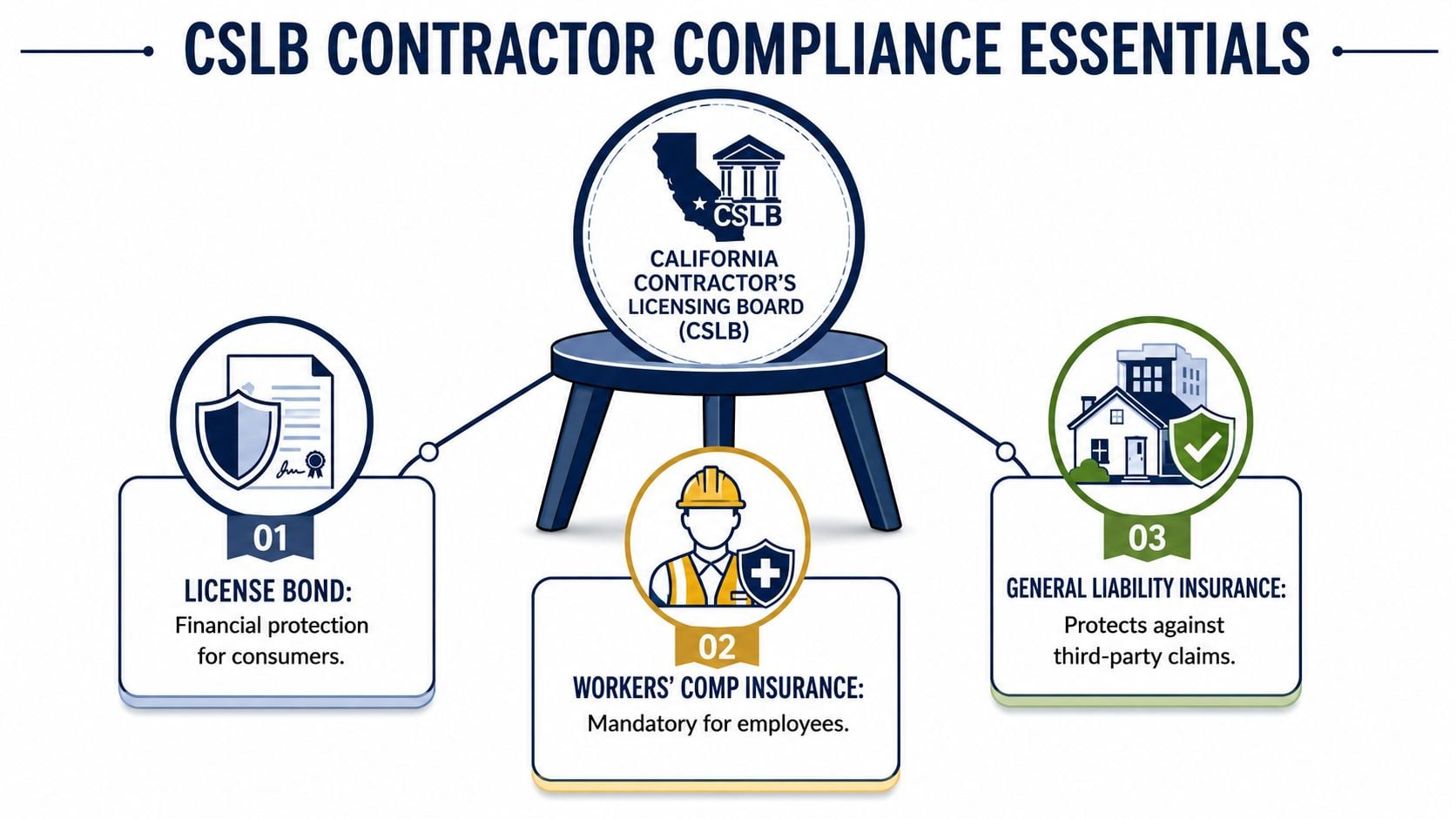

The practical way to think about California contractor insurance is as a three-legged stool. One leg is the license. One leg is the bond. One leg is the insurance program. Take away any leg and the business gets unstable fast. A contractor can be excellent in the field and still lose money, delay a start date, or create a licensing problem because one document is missing or one policy doesn't match the job.

That matters in daily operations. A grounds contractor bidding on a commercial maintenance contract gets asked for a COI before the first mow. A concrete contractor brings on a helper and now workers' comp rules change. A general contractor hires subs and assumes their coverage is fine, only to find out after a loss that the paperwork was stale or incomplete.

California contractor insurance isn't just about checking a legal box. It's part of how a trade business stays bankable, bid-ready, and resilient when jobs go sideways. The contractors who handle it well usually do the same thing they do on site. They keep the process simple, use the right materials, and don't cut corners where failure gets expensive.

Table of Contents

- Introduction

- CSLB Compliance Your License Bond and Insurance Mandates

- General Liability What Your California Policy Must Cover

- Navigating California's Strict Workers Compensation Rules

- What Really Drives Your Contractor Insurance Costs in 2026

- Managing Project Paperwork COIs and Additional Insureds

- How to Compare Policies and Get Coverage Same-Day

Introduction

A lot of contractors are dealing with the same pressure right now. They're trying to keep crews moving, close bids, chase payments, and answer insurance requests that seem written for lawyers. The problem is that California doesn't give much room for guessing. If the business is licensed incorrectly, bonded incorrectly, or insured incorrectly, the issue usually shows up at the worst time. It shows up when a bid is due, when a client asks for proof of coverage, or after a claim.

A practical insurance setup starts with understanding what each piece is supposed to do. The license gives legal authority to operate. The bond backs up certain obligations to the public and the state. The insurance responds to specific risks tied to the work, the crew, and the vehicles. They work together, but they don't replace each other.

Practical rule: If a contractor treats the bond like insurance or assumes a COI means every requirement is satisfied, that contractor is already exposed.

A trade example makes the point. Take a flooring contractor who lands a commercial suite remodel. The owner wants proof of general liability. The state requires the contractor's bond. If the flooring installer uses helpers, workers' comp comes into play. If materials and labor put the project over the licensing threshold, operating casually isn't an option. One missing leg on that stool can turn a profitable job into a contract dispute or a compliance problem.

The good news is that most of this gets easier once the terms are translated into field language. Liability limits work like the budget available for covered claims. Bonds work like a financial backstop for licensing obligations. COIs work like a snapshot of what's in force today. Additional insured status works like extending part of the policy's protective umbrella to another party for the contractor's work.

Contractors don't need a lecture. They need clean answers to practical questions. What has to be in place before bidding? What limits are clients asking for? Which trades have stricter workers' comp rules? What paperwork should be collected from subs before they create a problem? Those are the issues that decide whether California contractor insurance helps the business or slows it down.

CSLB Compliance Your License Bond and Insurance Mandates

California's compliance framework is simple in concept and unforgiving in practice. The contractor needs the right license status, the right bond filed correctly, and the right insurance where the law or the contract requires it. If one piece drops, the rest of the system gets shaky.

The three non-negotiables

California requires some hard numbers that every contractor should know. Every active contractor must hold a $25,000 Contractor's License Bond filed with the CSLB, LLC-licensed contractors must also carry a $100,000 LLC Employee/Worker Bond plus at least $1 million in General Liability coverage for businesses with five or fewer personnel, and work valued at $500 or more including labor and materials requires a CSLB license according to California contractor bond and insurance requirements by trade.

That's the baseline. It doesn't matter whether the contractor is doing tenant improvements, service calls, resurfacing, fencing, or finish carpentry. If the legal threshold is met, the paperwork has to match the operation.

For contractors getting set up for the first time, a plain-English guide to getting bonded and insured for contractor work helps sort out the sequence.

A flooring contractor gives a good real-world example. If that contractor installs a project over the licensing threshold without the proper license and bond in place, the risk isn't just administrative. Payment disputes get harder. Project owners hold a stronger position. Insurance complications can follow if the contractor was operating outside the required framework.

How the bond and liability policy do different jobs

The bond and the liability policy are often confused, but they do two different jobs.

- The license bond protects consumers and the licensing system. It's tied to statutory obligations and claims tied to violations of state law.

- General liability protects against covered third-party injury or property damage claims. It's the policy that usually gets reviewed in bid packages and owner contracts.

- The license itself is the gatekeeper. Without it, the rest of the paperwork won't fix the underlying compliance problem.

A contractor can't patch a license problem with a good insurance certificate. That's like trying to fix failed substrate with a premium finish coat.

There's also a practical project analogy that helps with liability limits. Per occurrence is the amount available for one covered incident. Aggregate is the total budget available across covered claims during the policy term. On a construction job, that's the difference between the allowance for one problem and the total allowance for the whole run of work.

Contractors who keep these roles separate usually make better decisions. They don't underbuy liability because they already have a bond, and they don't assume a bond satisfies an owner's insurance requirements.

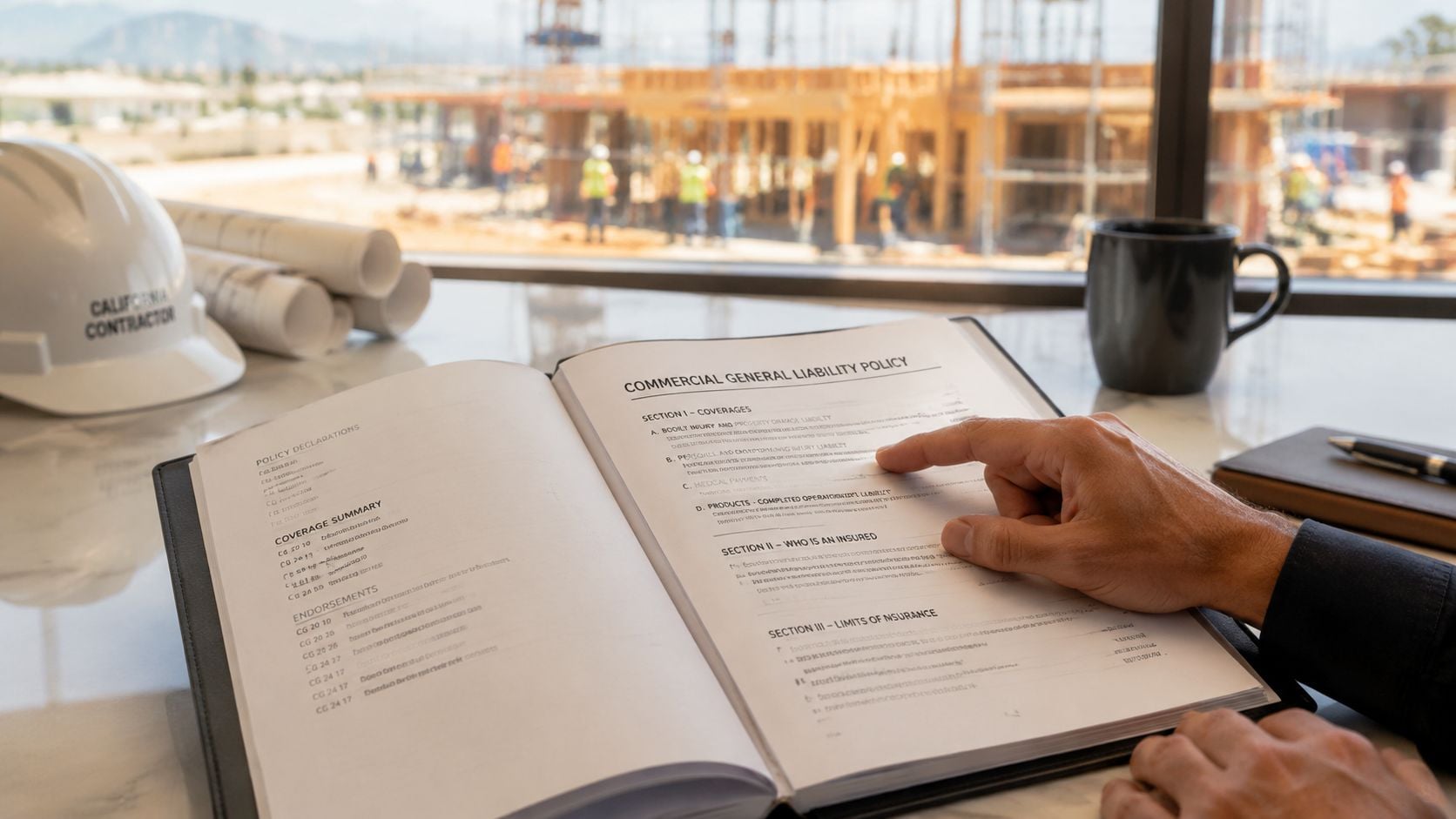

General Liability What Your California Policy Must Cover

General liability is the policy most contractors get asked for first because it speaks directly to common jobsite losses. Someone gets hurt. A customer's property gets damaged. A claim shows up after the work is done. That's why this coverage keeps appearing in bid specs, subcontracts, and owner onboarding packets.

How to read the limit language

For California general contractors, the standard market benchmark for Commercial General Liability is $1 million per occurrence with a $2 million aggregate limit, most project owners and government contracts demand that $2 million aggregate, and completed operations should remain in place for at least three years after project completion based on California general liability benchmarks for contractors.

Those numbers matter because many contractors only look at the premium and ignore the structure. But the structure is what the client is usually checking.

Think of it this way:

| Liability term | Plain-language meaning | Trade example |

|---|---|---|

| Per occurrence | The most the policy pays for one covered incident | A ladder falls onto a parked vehicle during an HVAC install |

| Aggregate | The most the policy pays for all covered claims in the policy period | Several unrelated claims hit during the same year across different jobs |

| Completed operations | Protection for claims that show up after the work is finished | A defect tied to earlier work causes property damage months later |

A contractor who does electrical tenant improvements can see this clearly. If wiring work later contributes to a fire after final completion, the issue isn't whether the crew is still on site. The issue is whether completed operations protection is still standing behind that work.

For contractors reviewing policy options, a practical reference on general liability insurance for contractors can help sort the language that tends to show up in project requirements.

Why completed operations matters after the crew leaves

This part gets overlooked because there's no visible problem on the day the invoice is paid. But finished work can still create a claim later. Concrete can crack and shift. Improper flashing can allow water intrusion. Mechanical work can fail after turnover and damage surrounding property.

Field takeaway: The end of the job isn't the end of liability exposure.

Clients ask for stronger liability limits because they know construction claims don't always arrive during active work. They also know one project can produce more than one incident. That's why a contractor shouldn't read a request for a $2 million aggregate as boilerplate. It's an owner trying to make sure one claim doesn't wipe out the policy for the rest of the project period.

California contractor insurance becomes operational, not theoretical. The contractor who understands the limit language can answer bid questions faster, submit cleaner paperwork, and avoid buying a policy that looks cheap but doesn't fit the contract.

Navigating California's Strict Workers Compensation Rules

Workers' comp is where many California contractors get tripped up because the answer changes based on license class, employee status, and how the business is set up. Some contractors still assume workers' comp only matters once payroll is on the books. In California, that assumption can create a licensing issue.

Solo operator versus licensed trade mandate

California already requires certain license classifications, including C-8 Concrete and C-20 HVAC, to carry workers' compensation insurance even when they have no employees, and that requirement expands to all licensed contractors by January 2028 regardless of employee status according to California contractor workers' compensation requirements for 2025 and the 2028 mandate.

That changes how a solo operator should think about compliance. A solo HVAC technician and a solo concrete contractor may both consider themselves owner-only businesses, but the legal treatment of their workers' comp obligation isn't identical under current California rules. By January 2028, the state moves to universal coverage for all licensed contractors regardless of employee status.

That's stricter than what many contractors see elsewhere. For readers who want a side-by-side contrast with another state model, this overview of understanding Florida workers' compensation rules is useful because it shows how state-specific these requirements can be.

What changes in day-to-day operations

The practical impact shows up in ordinary business decisions:

- Hiring a helper changes exposure immediately. Once labor enters the picture, injury risk isn't theoretical anymore.

- Using subcontractors doesn't remove the need for review. A contractor still needs to know whether those subs carry proper coverage and whether contract terms push risk back upstream.

- License renewals and project onboarding can stall. Missing workers' comp documents often surface when a contractor is trying to move quickly.

A concrete contractor is a strong example because the work itself carries obvious physical risk. Crew members handle heavy material, uneven surfaces, and equipment in changing site conditions. If someone gets hurt and the contractor assumed owner-only status meant no policy was needed, the financial exposure can shift directly onto the business.

Workers' comp pricing also follows risk. Carriers look closely at the trade, the type of labor being performed, crew size, payroll, and claims history. A high-hazard trade won't be priced like a low-hazard trade. A contractor with a clean operation and disciplined jobsite process usually presents differently from one with frequent injury issues or sloppy payroll classification.

For state-by-state context on how these rules vary and why California stands apart, contractors can review workers comp requirements by state for trade businesses.

Coverage questions around workers' comp are rarely solved by guessing who counts as a helper, who counts as a sub, or which license class gets special treatment. The paperwork has to match the real operation.

What Really Drives Your Contractor Insurance Costs in 2026

Contractors often ask for “the price” as if there's one standard number. There isn't. Insurance pricing works more like estimating a job. The trade, the exposure, the crew size, the vehicles, the loss history, and the contract requirements all affect the final number.

What the premium ranges actually tell a contractor

In California, general liability for a solo operator ranges from $700 to $1,400 annually, a business with 2 to 5 employees typically pays $1,400 to $4,000, and roofers often fall between $3,000 and $8,800 because of the higher risk profile according to California contractor general liability cost ranges.

Those ranges tell a contractor two useful things. First, crew size matters. Second, trade class matters a lot. A roofer and a painting contractor aren't bringing the same exposure to the market. Neither are a handyman and a general contractor managing multiple trades and subs.

Here's a clean budgeting view:

| Trade | Solo Operator (1 Person) | Small Crew (2-5 Employees) |

|---|---|---|

| General contractor | Varies by operation and job type | Varies by operation and job type |

| Roofer | $3,000 to $8,800 annual GL range applies by trade class via the cited source | Higher-risk trade exposure typically places pricing above lower-hazard trades |

| Contractor, broad California benchmark | $700 to $1,400 | $1,400 to $4,000 |

A quote that lands at the high end doesn't automatically mean it's overpriced. It may reflect a tougher trade class, larger contracts, more subcontractor exposure, or prior claims. The better question is whether the quote matches the work being performed.

For contractors evaluating budget benchmarks, this guide to general liability insurance cost for contractors can help frame what to ask when reviewing pricing.

When a client asks for a COI during bidding

A request for a COI during bidding usually means the client wants proof that the contractor is insurable before awarding the job. That request shouldn't slow things down if the policy setup is clean.

When the COI request lands, the contractor should:

- Confirm the named insured matches the business entity on the contract.

- Check the policy dates so coverage won't expire at project start.

- Review the limits against the bid requirements.

- Ask whether additional insured status is required so endorsements can be addressed early.

A grounds maintenance contractor bidding on a commercial account sees this all the time. The property manager isn't asking for a COI out of curiosity. The manager wants proof that if a third party gets injured or property is damaged during the work, there's a live policy behind the contractor.

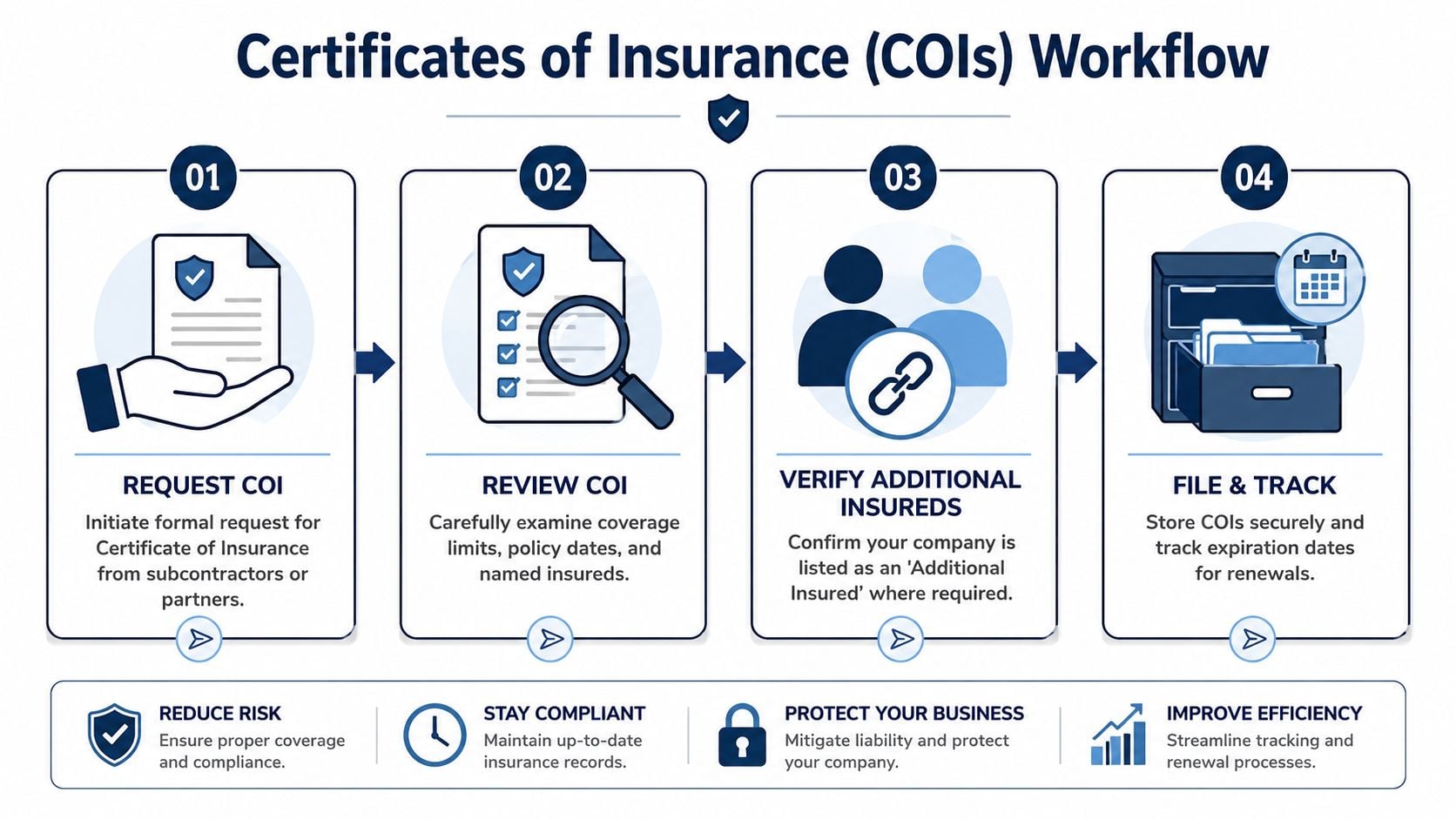

Managing Project Paperwork COIs and Additional Insureds

Insurance problems don't always come from a denied claim. Sometimes they come from a job that can't start because the paperwork is late, incomplete, or inconsistent with the contract. That's why contractors who manage documents well tend to keep projects moving more smoothly.

A COI proves coverage but it isn't the policy

A Certificate of Insurance, or COI, is proof that a policy exists on the date it's issued. It isn't the full policy. It doesn't rewrite exclusions. It doesn't create extra coverage by itself. It's a snapshot.

A grounds contractor bidding on a commercial maintenance contract can use a simple process:

- Request the right certificate early. Don't wait until the day before the scheduled start.

- Match the business name carefully. The insured name on the COI should line up with the contracting entity.

- Review dates and limits. Expired coverage or weak limits can stop access to the site.

- Ask for endorsements when required. Additional insured status usually isn't something to assume.

If a project owner or GC asks to be listed as an additional insured, the easiest analogy is an umbrella. The contractor owns the umbrella, but for liability arising out of the contractor's work on that job, another party is being allowed under part of that protection. That's why owners and upstream contractors ask for it. They want a layer of defense tied to the subcontractor's operations.

A practical template for handling these requests is available in this certificate of insurance template for contractor workflows.

How to manage subcontractor paperwork without slowing the job

Subcontractor insurance management is where many avoidable problems begin. A GC assumes the sub has coverage. The COI arrives. Nobody checks expiration dates, entity names, or whether additional insured wording was handled. Then a claim hits.

The fastest way to inherit someone else's problem is to let them onto the job with unchecked paperwork.

A cleaner process looks like this:

| Step | What to verify | Why it matters |

|---|---|---|

| Request | Coverage before mobilization | Prevents last-minute scrambling |

| Review | Limits, dates, named insured | Catches obvious mismatches |

| Confirm | Additional insured requirement | Aligns with contract transfer language |

| Track | Renewal and expiration | Keeps coverage from lapsing mid-project |

Contractors trying to do all of this alone often end up wasting time chasing documents from subs, owners, and agents while the job clock is already running. A more efficient approach is using a process that standardizes requests, checks details quickly, and keeps expiration tracking organized instead of buried in email threads.

That's especially important on multi-trade jobs where one weak subcontractor file can create a chain reaction across the whole project.

How to Compare Policies and Get Coverage Same-Day

Shopping contractor insurance without a framework usually produces a stack of quotes that don't match each other. One has lower limits. One strips out terms the contract expects. One looks cheaper because the scope was classified differently. On paper they all look close. In practice they're not the same product.

Compare the parts that affect claims

A contractor comparing policies should focus on what changes claim performance and contract compliance:

- Limits that fit the work. Cheap doesn't help if the project requires stronger liability terms.

- Coverage language that matches operations. The policy should fit the trade, not a generic business description.

- Exclusions that can block common contractor losses. The fine print matters when a claim occurs.

- Carrier quality and responsiveness. Fast COIs and clear underwriting matter when jobs move quickly.

A plumbing contractor bidding several service agreements may need quick certificates, contract review support, and policy language that fits both residential and light commercial work. A stripped-down quote might satisfy none of those needs even if it wins on premium.

Why speed matters when the start date is close

The old way is still common. A contractor calls around, repeats the same intake details several times, waits for callbacks, and then tries to compare quotes that weren't built on the same assumptions. That process burns time and often produces confusion instead of clarity.

A better approach is working through an independent advisor who can shop the market broadly, translate the differences into plain language, and move quickly when the insured needs to bind and issue paperwork. Coverage Axis does exactly that for contractors by shopping 50+ A-rated carriers, building right-sized programs for the trade and operation, and helping secure same-day binding when timing is tight.

For a contractor staring at a contract deadline, that difference matters. The goal isn't just to get a policy. The goal is to get the right policy in force, with the right documents, before the job stalls.

Contractors who need a fast quote, a same-day bind option, or a practical review of their current California contractor insurance program can get a free coverage review from Coverage Axis. A licensed advisor can help compare policies, sort out CSLB-related requirements, and assemble coverage that fits the trade, crew size, and project demands without the usual back-and-forth.