For qualified contractors, surety bond premiums usually cost between 0.5% and 3% of the total bond amount. On a $100,000 performance bond, that often means about $500 to $3,000, while higher-risk applicants can pay more.

That's the number most contractors are hunting for when a bid package lands on the desk and the bonding requirement shows up halfway through the paperwork. However, the concern isn't just price. It's whether that bond cost gets carried into the estimate correctly, whether the surety will support the job in time, and whether the premium ties up margin on a project that was already bid tight.

A lot of search results also muddy the waters by mixing up construction bonding with dental bonding. That's a different topic entirely. This article deals only with commercial surety bonding for contractors, where pricing is usually a percentage of the bond amount tied to the job or license requirement.

Table of Contents

- Your First Look at Bonding Requirements

- What a Contractor Surety Bond Actually Is

- The Main Bond Types You Will Encounter

- How Your Bonding Cost Is Calculated

- Key Factors That Determine Your Bond Rate

- How to Get Bonded and Lower Your Costs

Your First Look at Bonding Requirements

A contractor opens a bid invitation for a school addition, a municipal waterline job, or a commercial tenant build-out. The scope looks solid. The crew can handle it. Then one line in the package changes the whole pricing conversation: bond required.

That moment matters because a bond isn't usually a flat filing fee. For construction, the cost is typically a percentage of the bond amount. For many qualified contractors, commercial surety bond pricing falls in the 1% to 3% project-value range, and that's very different from the unrelated dental use of the word bonding, which is often priced at $100 to $600 per tooth according to Humana's explanation of dental bonding cost. Contractors looking up how much does bonding cost need the construction version, not a dental price chart.

An electrical contractor bidding public work sees this fast. The bid may require a bid bond up front, then performance and payment bonds after award. If those costs aren't understood before the number goes out, the contractor can win the job and still end up squeezing cash flow from day one.

Bond cost isn't just an admin item. It affects bid strategy, working capital, and whether a contractor can take the next job without overextending.

For firms that are actively chasing work, it also helps to keep an eye on where bond-heavy opportunities are showing up. Contractors reviewing UK construction tender opportunities can see how often public and commercial work includes formal tender requirements, including bonding expectations on larger jobs.

A contractor that's new to this process should first pin down exactly what the owner is asking for, then compare it against the state or project-specific rules. A practical starting point is a plain-English guide to contractor bonding requirements so the estimate reflects the actual obligation and not a guess made the night before bid day.

What a Contractor Surety Bond Actually Is

A surety bond is a three-party guarantee. It isn't the same thing as general liability, workers compensation, or builders risk. The bond is there to protect the project owner or the public body that required it.

The three parties on every bond

There are always three sides in the arrangement:

- Principal. The contractor that has to perform the work or meet the license obligation.

- Obligee. The project owner, municipality, or agency requiring the bond.

- Surety. The company backing the contractor's promise.

The cleanest way to explain it is this. The surety acts a lot like a co-signer. The contractor is still the one responsible for performing the contract. The surety just stands behind that promise.

That's why bond underwriting feels different from buying insurance. Insurance transfers risk to the carrier for covered losses. A bond guarantees performance to someone else, and the contractor remains responsible for the obligation.

Why owners ask for bonds

A city awarding a public building contract doesn't want to absorb the cost if the GC defaults halfway through the framing package, electrical rough-in, or finish schedule. The owner wants a financial backstop in place before issuing the notice to proceed.

Take a general contractor on a municipal renovation. If the contractor can't complete the work, the obligee looks to the bond. The bond exists to protect the owner's position and keep the job from collapsing financially. That's why bonded work often opens doors to larger public and institutional projects, but it also brings closer financial scrutiny.

Practical rule: A bond protects the client. It does not function like a policy that protects the contractor's own balance sheet.

Contractors who still hear clients say, “Are you bonded and insured?” should separate the two in conversation. Insurance handles covered accidents and losses. Bonding backs a promise to perform or comply. A quick breakdown of what bonded means for a business helps clear that up when owners or subs lump everything together.

The Main Bond Types You Will Encounter

Most contractors run into three bond types over and over. They show up at different stages of the job and they do different work.

Bid bonds

A bid bond shows the owner that the contractor is submitting a serious number and can provide the required final bonds if awarded the project. In practice, this is the gatekeeper bond. Without it, the bid may not even be considered.

Bid bonds are often issued at no additional charge or under an annual administration fee of $1,500 to $2,500 that covers all bid submissions for the year, according to FCA Insurance's discussion of surety and performance bond cost. That structure matters for general contractors and larger subs who bid often, because it changes the cost from a per-bid expense into more of a yearly overhead item.

Performance bonds

A performance bond kicks in after award. It guarantees that the contractor will complete the work according to the contract terms.

For a GC, that usually means the owner wants assurance that the building, site package, utility work, or tenant improvement will be delivered. For an electrician on a bonded prime contract, it can mean the electrical package sits inside a broader bonded obligation upstream.

Payment bonds

A payment bond protects subcontractors and suppliers by backing the contractor's obligation to pay for labor and materials. Owners care about this because unpaid downstream parties create disruption, claims pressure, and on some jobs, lien exposure.

Performance and payment bonds often travel together. One guarantees completion. The other addresses the money owed down the chain.

On a real job, these bonds aren't paperwork for paperwork's sake. They keep the contract enforceable when money, schedule, and downstream payment start getting tight.

An electrical subcontractor bidding a new commercial building may first deal with a bid bond requirement through the prime contractor's process. If the project is awarded and fully bonded, the project then moves into the performance and payment bond stage at the prime level. Understanding the difference between those stages helps contractors avoid pricing the wrong bond at the wrong time. This side-by-side guide on bid bond vs performance bond is useful when estimating teams need to sort out which obligation is being requested.

How Your Bonding Cost Is Calculated

A bond number can decide whether a bid is still workable before the job even starts. I see that happen with trade contractors all the time. An electrician may be competitive on labor and material, then lose the edge once bond premium gets loaded into the estimate. A GC may win the job, but the premium still hits cash before the first pay app clears.

The pricing formula is simple:

Premium = rate × bond amount

The part that changes from contractor to contractor is the rate.

The basic math

For many contractors, bond premiums are charged as a percentage of the bond amount. The stronger the account, the lower that percentage usually is. Weaker credit, thin financials, or a job that stretches the contractor beyond its normal size can push the cost higher, as reflected in standard surety underwriting guidance published by the Surety & Fidelity Association of America.

That spread matters in the field, not just on paper.

A GC with an established bond program can often carry the premium as another job cost and keep fee intact. A newer plumbing contractor with a higher rate may have to decide whether to raise the bid, cut margin, or pass on the work. For a small electrical shop trying to move from service work into public jobs, that decision affects more than one project. It affects whether the company can build a bonded track record at all.

Here is the practical way to price it:

- Low-rate scenario. The premium fits into the estimate without forcing major changes to overhead or fee.

- Middle-range scenario. The job still works, but the bond starts eating into margin.

- High-rate scenario. The premium changes the bid strategy and may make the job unattractive, even if the contractor is technically bondable.

What the premium does to the job

Contractors should look at bond cost as both a percentage and a timing issue.

On a hard-bid public project, the premium affects how aggressive you can be. If two plumbers carry similar labor burden and material pricing, the one with the stronger bond rate has more room to sharpen the number. On negotiated work, the effect shows up differently. The contractor may stay profitable, but the owner sees a higher total project cost.

Cash flow is the other half of it.

Bond premium often has to be addressed before the project starts producing cash. That creates pressure on smaller firms that are already covering mobilization, early payroll, equipment, deposits, and supplier terms. A contractor can win a good job and still feel squeezed in the first 30 to 60 days if working capital is tight. For smaller firms trying to connect bonding with overall financial planning, this overview of bond insurance for small business is a useful reference.

A plumbing contractor example

A plumbing contractor bidding a bonded job may carry a clean estimate, solid production numbers, and acceptable margin. Then the bond premium gets added. If the owner is slow pay, retainage is heavy, and material pricing is still moving, that premium becomes more than an administrative cost. It directly affects whether the contractor can carry the job without stressing payroll or vendor relationships.

The same pattern shows up in other trades. An electrical contractor trying to break into school work may be approved, but at a rate that makes every bid less competitive. A GC with multiple active jobs may qualify for the next bond, yet the added premium and backlog pressure can still limit how much new work the company should take on at one time.

Getting bonded matters. Getting bonded at a rate that still leaves room for profit, cash flow, and growth matters more.

Key Factors That Determine Your Bond Rate

A bond rate changes fast when a contractor steps outside familiar work. An electrician who has been wiring tenant build-outs can look strong on paper, then get a tougher rate on a school project with phased turnover, public-owner paperwork, and a tighter schedule than the company has ever carried. The same thing happens to plumbers moving from service and small commercial work into larger bonded jobs, and to GCs stacking too many active projects at once.

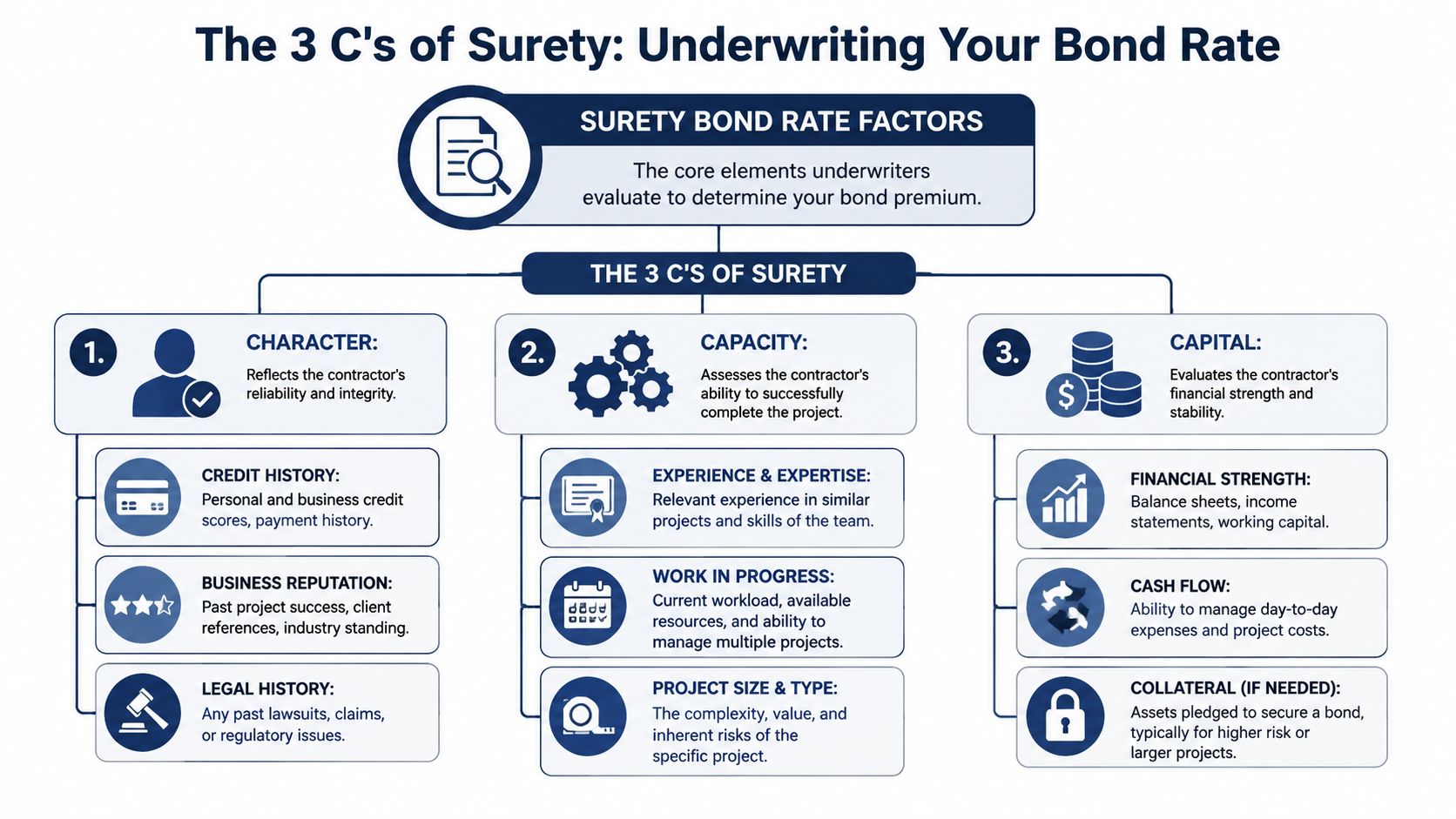

Underwriters usually sort that risk into the 3 C's of surety.

Character

Character is about trust. It covers personal and business credit, tax history, payment habits, claims history, legal issues, and whether the contractor does what they say they will do.

Sureties pay close attention to late pays, unresolved disputes, bounced vendor checks, and old tax problems because those issues often show up on the jobsite later. A small electrical contractor with clean books, steady supplier terms, and a track record of closing jobs without drama usually presents better than a contractor with the same revenue but constant collections pressure. Better character often means better pricing, but it also means fewer surprises when bid time gets tight.

Capacity

Capacity answers a simple question. Can this company perform this job with its current people, systems, and backlog?

That review goes beyond headcount. Underwriters look at field supervision, PM strength, equipment, subcontractor dependence, schedule pressure, and experience with similar contract sizes and scopes. A plumber may be profitable on restaurant remodels and medical office finish-outs, but a larger public job with multiple inspections, long material lead times, and strict closeout requirements is a different test. A GC can also get squeezed here if current backlog already has the superintendent team and office staff fully stretched.

Bond cost starts affecting growth directly. If the surety sees a jump in job size or complexity, the contractor may still get approved, but at a rate that makes the bid harder to carry.

Capital

Capital is the balance sheet side of the file. Sureties want to see enough working capital and cash to absorb ordinary project problems without missing payroll, delaying suppliers, or falling behind in the field.

That matters more than many contractors expect. A job can be estimated correctly and still create stress if receivables lag, retainage builds up, or a change order sits unsigned for weeks. For an electrician, that may mean carrying material and labor before draws catch up. For a plumbing contractor, it may mean funding rough-in labor while waiting on owner approvals. For a GC, it may mean fronting early project costs across several jobs at the same time.

Some bond costs are fixed by state rule instead of individual underwriting. In Virginia, the state requires certain Class A and Class B contractors to carry a $50,000 license bond with a set premium for the term, so the price is driven by the licensing requirement rather than the contractor's credit profile. Bonds tied to project performance and payment are different. Those rates move with the contractor's financial strength, experience, and current workload.

Contractors who are new to this process can get the basics in this guide on how to get bonded and insured for contractor work.

A roofer, electrician, plumber, and sitework GC can post similar annual revenue and still land very different bond rates. Trade exposure, job size, owner type, backlog, and cash position all change the surety's view of risk. The rate is not just a percentage on paper. It affects whether you can bid the work, carry the job through the first billing cycle, and keep growing without outrunning your balance sheet.

How to Get Bonded and Lower Your Costs

A contractor who waits until the day before bid close usually pays for it somewhere. Sometimes the price shows up in a higher bond rate. Sometimes it shows up in a missed bid, a smaller single-job limit, or a surety that will issue the bond but only after tying up more indemnity than the contractor expected. For an electrician chasing school work, a plumber stepping into municipal jobs, or a GC trying to keep several public bids in play at once, that delay can slow growth fast.

What to gather before applying

Sureties price and approve bonds off the file in front of them. If the file is thin, unclear, or rushed, the underwriter fills that gap with caution.

Have these items ready before you ask for a bond:

- Current financial statements with a clear balance sheet, income statement, and enough detail to show working capital and cash position.

- Project information including contract amount, scope, owner type, start date, completion timeline, and which trade scopes your company will self-perform.

- Work history that shows similar job sizes, past bonded projects, and whether the company has handled this kind of schedule and owner before.

- Ownership and entity details so the surety can review who is signing, who is indemnifying, and how the company is structured.

- Lead time before bid day because a file submitted early gives the underwriter time to ask questions before the deadline becomes the problem.

If bonding, licensing, general liability, workers comp, and auto are all hitting at once, this guide on how to get bonded and insured for contractor work helps line up the pieces in the right order.

What actually lowers bond cost

Lower bond cost usually follows stronger underwriting, cleaner execution, and better financial control. It is not just about shaving a rate. It affects how much work you can bid, how much backlog you can carry, and whether cash gets tight while you are waiting on the first draw.

A small contractor with limited bonded history will often pay more on an early bonded job than a peer with stronger statements and a clean track record. That first bond can still make sense if it opens the door to public work or larger private contracts. The mistake is treating the premium as the only cost. If the bond strains working capital or caps your next bid, the actual cost is bigger than the invoice.

Here is what improves terms over time:

- Keep personal and business credit clean because late payments still raise concerns about how bills and subs get managed on active jobs.

- Produce financial statements that make sense so the underwriter can see liquidity, debt load, and job performance without chasing missing details.

- Step up in job size in a controlled way instead of jumping from small service calls to a contract that is several times larger than anything on the completed-work list.

- Manage cash tightly because underbillings, slow receivables, and thin cash reserves are common reasons a surety gets cautious.

- Finish jobs without claims or payment issues since unpaid suppliers, tax problems, and disputes with owners damage future bond terms quickly.

The trade-offs are real. An electrician moving from tenant improvement work into public school projects may need to show stronger statements before the surety is comfortable with larger performance and payment bonds. A plumbing contractor that takes on a labor-heavy project with slow billing terms may get approved, but the bond cost and indemnity requirements can stay higher until cash flow stabilizes. A GC with solid profits can still run into resistance if backlog is stacked too high for the current balance sheet.

Contractors who need a bond quote, license review, or a full insurance checkup can get help from Coverage Axis. A free quote or coverage review can help sort out bond requirements, GL, workers comp, auto, and the insurance pieces that need to line up before the next bid goes out.