A contractor is ready to bid a solid job. The scope fits the crew. The numbers are tight but workable. Then the insurance section of the bid package shows up and stops everything.

It asks for General Liability, then adds Errors & Omissions or Professional Liability. Sometimes it also asks for a COI before work starts, additional insured status, and wording that sounds like it was written for an engineer, not a trade business owner.

That's where a lot of contractors get stuck. They already carry liability coverage. They've handed over COIs before. But now the contract is asking for something that sounds similar and clearly isn't the same thing. The question isn't academic. It affects whether the bid goes out, whether the contract gets signed, and whether the business is properly protected if a claim hits.

This is the practical version of general liability vs professional liability. Not the textbook version. The version that matters when a client asks for proof, when a GC sends over insurance requirements, or when a jobsite mistake turns into a demand letter. Contractors who are still sorting out the basics can start with this guide on what insurance contractors usually need.

Table of Contents

- That Moment on the Bid That Stops You Cold

- The Two Kinds of Trouble a Contractor Can Cause

- General Liability vs Professional Liability Side by Side

- Real Claim Scenarios From the Jobsite

- How These Policies Affect Your Contracts and COIs

- Choosing the Right Coverage for Your Trade

That Moment on the Bid That Stops You Cold

A flooring contractor reviews a school remodel bid. The insurance section starts normally. General liability, workers' comp, auto. Then one more line appears: professional liability required for any contractor providing layout, specification input, design-assist, or project recommendations.

That single line changes the conversation. A lot of trade owners assume liability is liability. If there's already a GL policy in force, that should handle it. But that's not how these claims work, and it's not how contract language is written anymore.

A contractor can be excellent in the field and still get burned by paperwork if the coverage behind the COI doesn't match the work being performed. That happens when the contract treats the business as more than a hands-on installer. If the contractor is advising on system selection, changing specs, reviewing plans, coordinating trades, or making recommendations the owner will rely on, the exposure shifts.

Practical rule: If the client can say, “We relied on your judgment,” the conversation may move beyond general liability.

This is why the general liability vs professional liability question keeps coming up in construction. It isn't just about buying another policy. It's about understanding whether the contract is asking for a box to check, or whether the work itself creates a real professional exposure.

The difference matters most when a claim doesn't start with broken property or a bodily injury. It starts with an allegation that the contractor's judgment, recommendation, or incomplete service cost the client money.

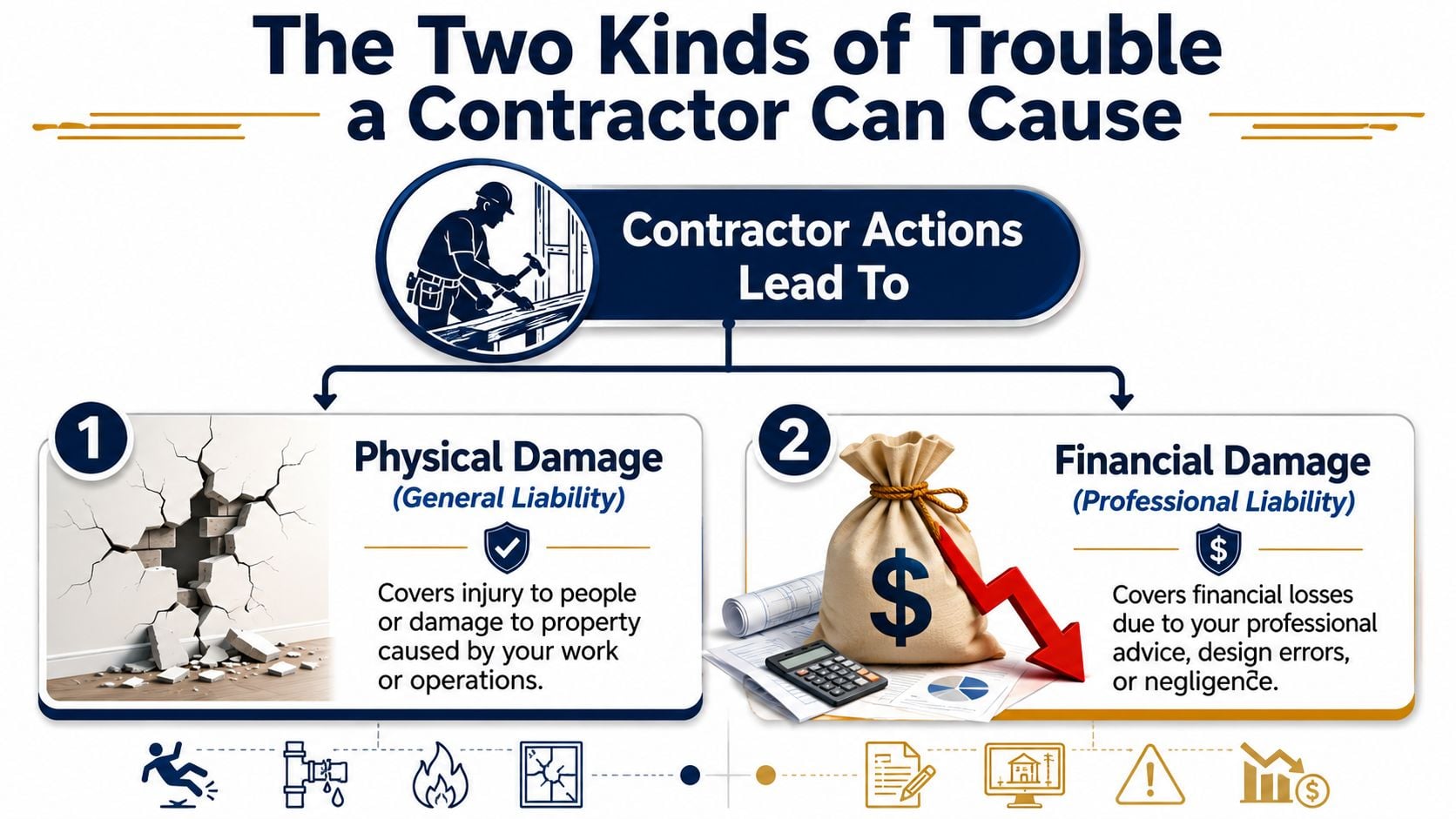

The Two Kinds of Trouble a Contractor Can Cause

The cleanest way to explain general liability vs professional liability is this:

General liability usually deals with physical trouble.

Professional liability usually deals with financial trouble tied to services or advice.

That's the split contractors need to remember when they're reading contract requirements or trying to understand what a claim would look like in practice.

For contractor and service businesses, the key underwriting distinction is that general liability responds to third-party bodily injury, property damage, and advertising or personal injury, while professional liability responds to third-party claims that a service or design mistake caused financial loss, as explained in this contractor insurance comparison. Contractors that perform consultative work can also review how this fits under professional services insurance.

Physical damage claims

Take an electrician working inside a finished office space. A tool slips off a ladder and cracks a stone countertop. Or a customer walks through the work area, trips over materials, and gets hurt.

That's the kind of event contractors usually think about first, because it's visible and immediate. Someone was injured. Something was damaged. There's a direct physical incident, and the claim points back to operations on the job.

A lot of GL claims feel like classic jobsite “oops” situations:

- Dropped material: It damages a client's finished surface.

- Slip and fall: A visitor gets hurt near the work area.

- Accidental damage: A crew member breaks part of the customer's property during installation.

Financial loss claims

Now take that same electrician on a different job. The client asks for guidance on a wiring setup. The contractor recommends a system that later fails inspection or doesn't support the intended equipment. The client has to pay for rework, delay coordination, and replacement decisions.

That's a different type of allegation. The problem isn't a broken countertop or an injured visitor. The claim is that the contractor's recommendation, specification input, or incomplete professional service caused a financial loss.

Many trade businesses often get surprised. They don't think of themselves as “professionals” in the insurance sense. But if the work includes judgment, design input, layout decisions, code interpretation, or system recommendations, a client may frame the loss as professional negligence, an error, or an omission.

Some contractors don't need professional liability for every project. Some absolutely do. The dividing line is whether the job relies only on labor and installation, or on the contractor's technical judgment as well.

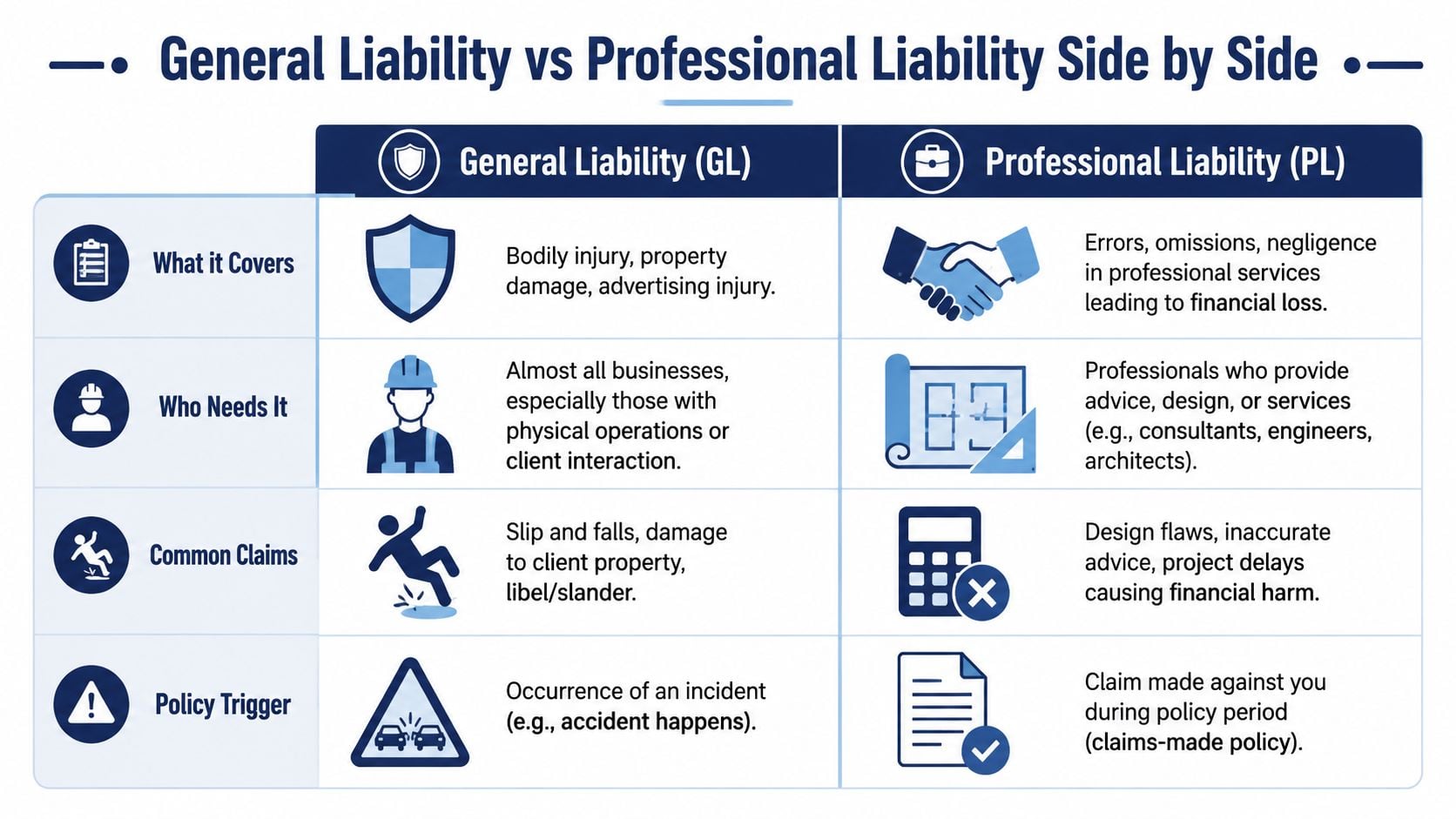

General Liability vs Professional Liability Side by Side

The place contractors usually get tripped up is not the definition. It is the bid package, the insurance exhibit, or the COI request that asks for one policy, the other, or both. If you do not know which problem each policy is built to answer, it is easy to buy coverage that satisfies a checkbox but misses the claim that can hit your business.

General liability and professional liability solve different exposures. General liability is built for third-party bodily injury, property damage, and personal or advertising injury tied to your operations. Professional liability is built for claims that your advice, design input, layout, specification help, or other professional service caused a financial loss, as explained in this breakdown of professional liability versus general liability.

Quick comparison table

| Coverage point | General Liability | Professional Liability |

|---|---|---|

| Main purpose | Pays for claims involving bodily injury, property damage, and related defense costs tied to operations | Pays for claims alleging an error, omission, negligent advice, or other professional mistake caused financial harm |

| Typical trigger | A physical incident on or from the job | A dispute over judgment, recommendations, plans, layout, code interpretation, or project advice |

| Common contractor example | Your crew cracks a finished lobby floor while moving material | Your recommended system or layout leads to rework, delay costs, or performance complaints |

| How it is usually bought | Standard core coverage for most contractors | Added based on trade scope, contract terms, and how much technical judgment you take on |

| Why contracts ask for it | To protect against jobsite injury and property damage claims | To protect against design-assist, consulting, or professional error allegations |

Owners, GCs, and lenders ask for these coverages because they worry about two separate ways a contractor can cost them money. One is the obvious jobsite loss. The other is a decision problem. A bad recommendation, a missed detail, or a scope gap can turn into change order fights, delay claims, and backcharges long after the crew is gone.

That distinction also affects how you review limits, not just whether you have the policy. Contractors who want a practical read on how general liability coverage limits work should compare those limits against contract indemnity language, additional insured requirements, and the size of loss a single incident could create on a live job.

A property owner dealing with an injury claim may also be sorting out premises exposure tied to site conditions. For that side of the issue, this overview of your Hawaii premises liability rights gives useful context on how those claims can develop.

Why policy form matters

The policy title does not tell the whole story.

General liability is commonly written on an occurrence form. Professional liability is commonly written on a claims-made form. That difference matters in construction because many professional allegations show up after closeout, after occupancy, or after the owner starts pressing on performance.

Here is the practical version. If drywall gets damaged during the job, the date of damage usually drives the GL response. If a client later alleges your design-assist input caused rework, the date the claim is made can drive the professional liability response. Drop that policy, switch carriers carelessly, or miss a retroactive date issue, and you can create a gap you do not see until the demand letter shows up.

I tell contractors to read past the declarations page. Check the form, the retro date, the reporting terms, and any professional services exclusion on the GL policy. A COI can help you get through prequal, but it does not fix a coverage hole.

Real Claim Scenarios From the Jobsite

The easiest way to understand general liability vs professional liability is to test it against real trade situations.

Plumber and water damage

A plumber installs a water heater in a tenant space. A connection fails later, water runs overnight, and the unit below suffers damage to ceilings, flooring, and contents.

That scenario points toward general liability because the claim starts with physical damage to someone else's property. The loss is visible. The allegation is tied to operations and resulting property damage.

What usually confuses contractors is that the same job can produce a second layer of argument. If the owner also claims the plumber gave faulty guidance on the type of equipment or setup and that recommendation created added costs, the facts need a closer review. One event can create more than one theory of liability.

HVAC sizing recommendation

An HVAC contractor reviews a commercial buildout and recommends a unit size for the space. After occupancy, the client says the system can't maintain conditions, usage costs are wrong for the building, and the unit has to be replaced.

That's the kind of claim that often points toward professional liability. The core allegation isn't that a technician smashed a window or flooded a mechanical room. It's that the contractor's judgment, recommendation, or technical service caused downstream financial harm.

This is one reason field documentation matters. Good notes, approval trails, and photos can help show what was recommended, what was installed, and what changed during the job. Teams that want tighter records can look at how stronger documentation practices can boost profits through photo management, especially when disputes start with “that's not what was discussed.”

General contractor oversight

A general contractor coordinates several trades on a tenant improvement project. A subcontractor's work creates a structural issue, and the owner alleges the GC failed in project oversight, coordination, and management.

That scenario can move toward professional liability if the allegation is framed around negligent supervision, project management, or a failure in professional services. The GC may not have physically performed the faulty work, but the claim may still target decision-making, oversight, and responsibility for how the work was directed.

A contractor doesn't need to draw stamped plans to face a professional liability allegation. Coordination, recommendations, and management decisions can be enough.

When neither policy solves the whole problem

Some jobsite losses don't fit cleanly into either bucket. Pollution conditions are a common example. If a contractor disturbs contaminants, releases fumes, or creates an environmental issue during operations, the claim may require a separate policy entirely. Contractors with that exposure should review how contractors pollution liability insurance fills a gap that standard liability policies often leave behind.

That's why a smart insurance program isn't built by asking, “What policy is cheapest?” The better question is, “What kind of claim can this trade trigger?”

How These Policies Affect Your Contracts and COIs

Insurance requirements in construction rarely show up by accident. If a contract asks for both GL and professional liability, the upstream party is trying to transfer two different categories of risk.

Why contracts ask for both

Owners, property managers, and general contractors know that contractors can cause direct jobsite damage. They also know that contractors often influence outcomes through recommendations, sequencing decisions, layout input, and technical judgment.

So the contract may ask for:

- General liability for bodily injury and property damage exposures tied to operations

- Professional liability for service-related or advice-related allegations

- Additional insured wording so the hiring party has rights tied to the contractor's policy, depending on the contract and endorsement structure

Contractors dealing with upstream requirements should understand how an additional insured endorsement changes the risk transfer conversation. A COI alone doesn't rewrite the policy.

This is also why “the client only wants a certificate” can be misleading. The COI is just the summary the client asks to see. The important question is whether the actual coverage behind it matches the contract and the work.

What to check on the COI

A COI should be read like a compliance document, not just proof that insurance exists.

Check these points first:

- Named insured: Does it match the legal entity signing the contract?

- Policy types listed: Does the certificate show the exact coverages the bid package requires?

- Dates: Will the policy be active through the project period?

- Endorsement needs: If the contract asks for additional insured, waiver language, or primary and noncontributory wording, has that been addressed?

A contractor can hand over a clean COI and still have a problem if the policy behind it doesn't support the operations described in the contract.

There's another practical issue. Both GL and professional liability generally exclude employee injuries, owned business property, and vehicle accidents, so contractors often need separate workers' compensation, commercial property, and commercial auto coverage to close those gaps, as summarized in this guidance on what these liability policies don't cover.

That matters during contract review because one certificate may not be enough. A solid subcontractor package often includes multiple policies, each solving a different part of the risk.

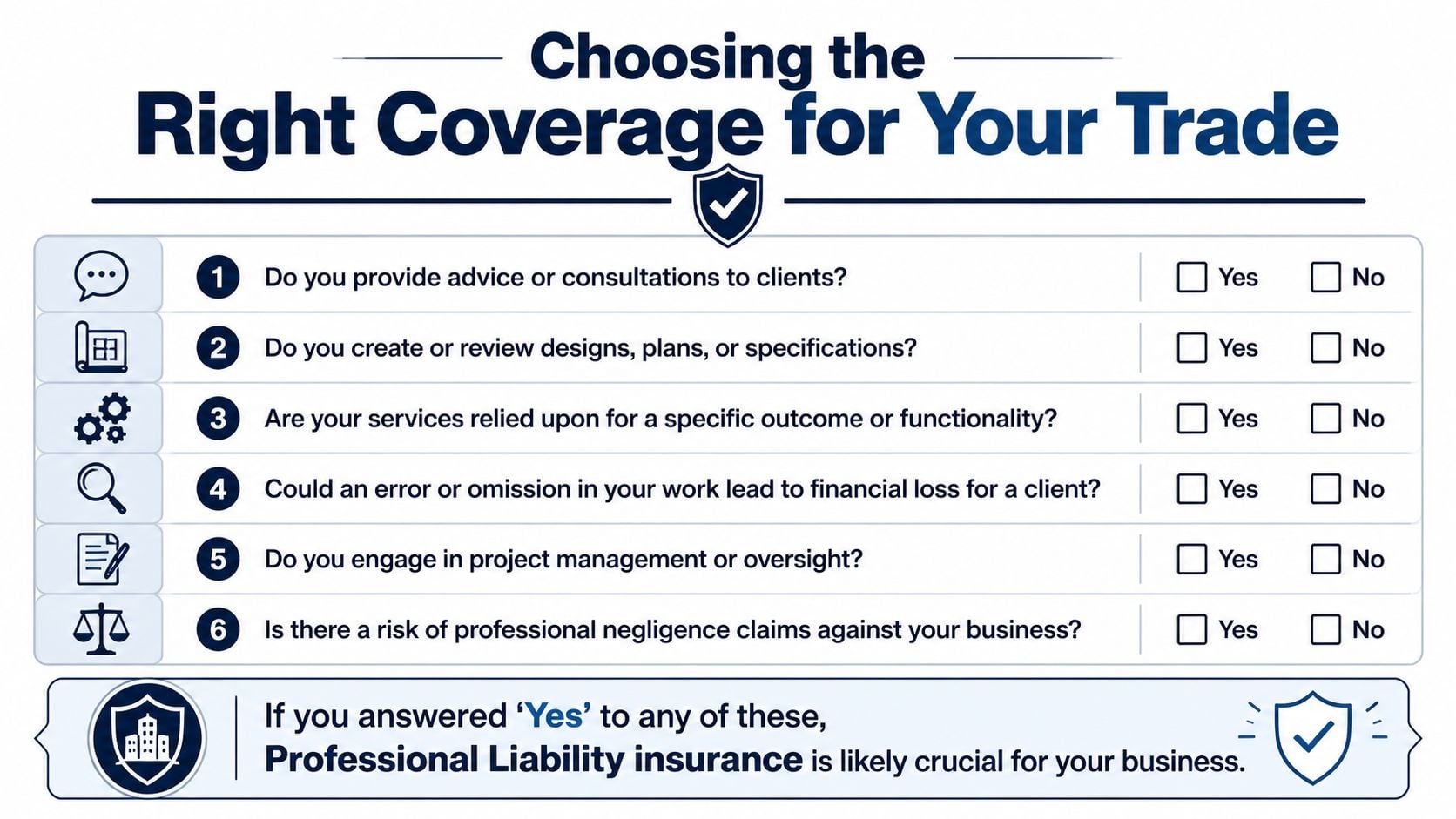

Choosing the Right Coverage for Your Trade

A lot of contractors find out what coverage they need only after the bid package lands on the desk. The specs call for GL. The owner or GC asks for a COI. Then a line buried in the insurance requirements mentions professional liability, design-assist, or errors and omissions. That is usually the point where the central question emerges. Is this just a contract compliance issue, or does the work create that exposure?

A simple self-check

Professional liability starts to matter when your value is more than labor and materials.

Use these questions to size it up:

- Client guidance: Do customers rely on your recommendations before the crew starts work?

- Plan involvement: Do you review, interpret, revise, or influence plans, specs, layouts, or equipment selections?

- Outcome responsibility: Are you selling a performance result, not just installation?

- Coordination role: Do you manage subs, sequencing, trade coordination, or design-assist scope?

- Financial exposure: Could a judgment call by your team trigger rework, delay costs, lost use, or other financial loss without any direct property damage?

A residential painter doing straightforward prep and coating work may not have much professional liability exposure on a typical job. A design-build electrical contractor, an HVAC firm recommending system sizing and controls, or a GC taking responsibility for coordination usually does.

What usually drives the decision

The buying decision usually comes down to how you get work, what the contract says, and how much judgment your company puts into the job.

General liability is standard for almost every contractor because it answers the claims that show up most often on jobsites: bodily injury, property damage, and the slip, trip, and damage-to-someone-else's-property problems that can put a project sideways fast. Professional liability is different. It comes into play when your advice, interpretation, or design-related decisions can cause financial harm, rework, or delay even if nobody gets hurt and nothing is broken in the usual sense.

That distinction affects both coverage and administration. Professional liability is often written on a claims-made form, which means timing, retro dates, and keeping the policy in force matter a lot. General liability is usually more familiar to contractors and easier to line up with routine COI requests.

A few practical triggers usually settle the issue:

- Trade scope: Pure install work has a different profile than work involving design input, recommendations, or delegated engineering.

- Contract language: Some contracts require professional liability whether you expected to buy it or not.

- Project type: Schools, hospitals, public work, and larger commercial jobs tend to ask for tighter insurance terms.

- Company role: An installer following plans exactly has one exposure. A contractor responsible for system performance or coordination has another.

The cleanest answer for a lot of trades is not choosing one policy over the other. It is matching the insurance program to the way the company operates. Buy GL because the jobsite requires it. Add professional liability when your contract, your scope, or your decision-making creates a gap GL will not pick up.

A contractor that wants a free, plain-English quote or coverage review can talk with Coverage Axis. A licensed advisor can review current policies, check contract requirements, shop the market, and help build a right-sized insurance program that fits the trade, crew, and project mix without loading the business up with coverage it doesn't need.