A contractor pricing a new hauling contract should usually budget $400 to $1,200+ per month per truck for dump truck insurance in 2026. That cost can go higher for new ventures, tougher classes of work, or accounts with loss issues, so insurance often changes the job math before the first load ever moves.

That's the situation many contractors are in right now. The bid looks good, the truck payment is already part of the overhead, and the route seems straightforward. Then the insurance requirements show up in the subcontract or public works package, and suddenly the critical question isn't just “What does dump truck insurance cost?” It's “Will the current policy effectively let this business win the job, satisfy the contract, and survive a serious claim?”

For trade businesses, dump truck insurance isn't just a paperwork item. It sits right in the middle of bidding, fleet planning, driver management, and cash flow. A sitework contractor hauling stone for a commercial pad job faces a different insurance problem than a groundworks contractor moving topsoil locally or a demolition contractor hauling debris out of a dense urban site. Same basic equipment class. Very different risk.

That's why a smart insurance decision for dump trucks has to go beyond definitions. It has to connect coverage to the actual choices contractors make every week: which jobs to bid, which loads to haul, which limits to carry, and where it's dangerous to save money.

Table of Contents

- Why Your Dump Truck Insurance Matters More Than You Think

- The Core Coverages in Every Dump Truck Policy

- Required Limits FMCSA Minimums vs Jobsite Reality

- What Drives Your Dump Truck Insurance Premiums

- Smart Add-Ons Endorsements and Specialty Policies

- Risk Scenarios How Coverage Responds on a Bad Day

- Getting the Right Program Owner-Operator vs Fleet Operator

Why Your Dump Truck Insurance Matters More Than You Think

The bid looks fine until the insurance terms arrive

A common construction scenario goes like this. An excavation contractor prices a hauling job for a new commercial site, figures the trucking is already handled, and submits the number with confidence. Then the contract package comes back with insurance requirements that the current setup doesn't meet.

The problem usually isn't that the contractor has no insurance. The problem is that the policy was built to stay legal, not to satisfy a general contractor, municipality, or private developer. That gap can knock a good bidder out of the running even when the trucks, drivers, and schedule are ready.

A dump truck used in trade work creates exposure in several places at once. It's on public roads, in tight jobsites, near other trades, around finished property, and often operating in reverse, on uneven ground, or near structures. A basic understanding of what insurance contractors need helps, but dump truck operations usually demand a more specific coverage strategy than a standard contractor account.

Practical rule: If a truck is central to delivering the work, the insurance shouldn't be treated like a generic add-on to the rest of the business policy.

Why project owners care so much about dump trucks

Project owners and GCs push hard on dump truck insurance because the loss potential is obvious. Dump truck risk isn't theoretical. A cited Federal Motor Carrier Safety Administration figure reported 5,483 dump truck accidents involving injuries and 367 fatal dump truck accidents in the same year referenced by this industry summary.

Those numbers help explain why dump truck insurance affects more than compliance. It affects whether the business can absorb a claim, replace damaged equipment, and keep operating after a serious incident.

For a concrete contractor hauling broken slab offsite, one truck backing into another trade's staged materials can trigger a claim. For a paving contractor, a rollover on an uneven shoulder can put a key unit out of service right when the schedule is tightest. For a site contractor, the insurance program becomes part of the production plan, because downtime and rejected certificates can stop work just as fast as a mechanical failure.

A contractor that treats dump truck insurance as a bid qualification tool, an asset protection tool, and a survival tool usually makes better decisions than one that shops only for the cheapest premium.

The Core Coverages in Every Dump Truck Policy

A workable dump truck policy starts with a few core pieces. Some are legal requirements. Others are what it takes to keep a trade business from taking a direct hit when a truck is damaged, a load creates a problem, or an employee gets hurt.

What every policy starts with

The foundation is primary liability. One industry source says it's required in every state and pays for bodily injury and property damage if the driver is at fault in an accident. In contractor terms, that's the coverage that responds if a dump truck backs into a loading dock or hits another vehicle while hauling material, as explained in this overview of primary liability for dump trucks.

Contractors that want a better grasp of how this works in a trade setting should understand commercial auto liability for contractors, because this is the line that usually gets checked first in a contract review.

From there, most dump truck accounts need more than one coverage line:

- Physical damage: This handles repair or replacement of the truck after a covered loss. For a trade example, if a tri-axle rolls on an unpaved access road, physical damage is what deals with the truck itself.

- General liability: This addresses business liability that isn't tied directly to an auto accident. If a problem happens around operations rather than from driving, this may be the relevant policy.

- Cargo coverage: This can matter when the material being hauled becomes part of the loss.

- Workers' compensation: If the business has employees, this is what responds when a driver or crew member is hurt on the job.

What keeps one bad incident from becoming a business problem

A lot of contractors make the mistake of asking whether a coverage is “required.” The better question is whether the business can afford the loss without it.

Here's the plain-English version of the core stack:

| Coverage | What it does on a real job |

|---|---|

| Primary liability | Pays for injury or property damage caused to others by the truck |

| Physical damage | Fixes or replaces the insured truck after covered damage |

| General liability | Handles certain non-auto business claims tied to operations |

| Cargo | Helps when the hauled material is part of the loss situation |

| Workers' compensation | Covers employee job injuries |

A legal minimum policy may keep a truck on the road. It may not keep a contractor in business after a serious jobsite incident.

A landscaping contractor provides a good example. Hauling mulch locally may look simple, but the exposure changes fast if the truck operates in residential neighborhoods, backs into driveways, or runs through tight subdivisions all week. The same applies to excavation, paving, utility, and demo work. The truck is only one part of the risk. The way it's used is what shapes the insurance decision.

Required Limits FMCSA Minimums vs Jobsite Reality

The biggest misunderstanding in dump truck insurance is the belief that legal minimums are enough. They might be enough to operate. They often aren't enough to get awarded the work.

Legal minimums are not the same as bid-ready limits

Federal trucking rules set minimum liability limits that matter for many dump truck operations. The general baseline is $750,000 for most motor carriers, while specific cargo-based thresholds rise to $1 million for private oil hauling and $5 million for hazardous materials other than oil. Those minimums were originally established in 1980, according to this summary of federal truck insurance minimums.

That sounds straightforward until the contractor starts bidding real jobs.

For Class 8 dump truck fleets hauling aggregate as for-hire interstate carriers, FMCSA-mandated minimums of $750,000 combined single limit shape the legal baseline. But many general contractors and public works departments now require $1M CSL or higher as a standard condition of contract, even where FMCSA only mandates $750,000, as outlined in this review of dump truck liability limit expectations.

That's why a contractor can be fully compliant and still be unable to provide an acceptable certificate. A useful reference point for understanding this contract language is combined single limit coverage, because that's often the wording sitting in the subcontract.

How to match limits to the work being pursued

For many contractors, the right limit is a business decision before it's an insurance decision. The key question is not “What is the minimum allowed?” It's “What limit keeps this company eligible for the jobs it wants?”

A simple way to understand this:

- Local private work: The contract may be lighter, but certificates still need to match the agreement exactly.

- General contractor sub work: Insurance requirements usually tighten fast, especially for hauling heavy material into active projects.

- Municipal or public works bids: These often come with strict insurance language, and missing the required limit can make the bid unusable.

A utility contractor hauling spoil from trench work runs into this all the time. The trucks may operate on short local routes, but the contract owner still wants stronger liability protection because the exposure involves public roads, active crews, and third-party property.

Being legal is one standard. Being bid-ready is another.

Some contractors solve this by building the primary auto program around the kind of work they pursue. Others use higher-level liability structures to align with larger projects. The wrong approach is waiting until award week to find out the current policy doesn't fit the contract.

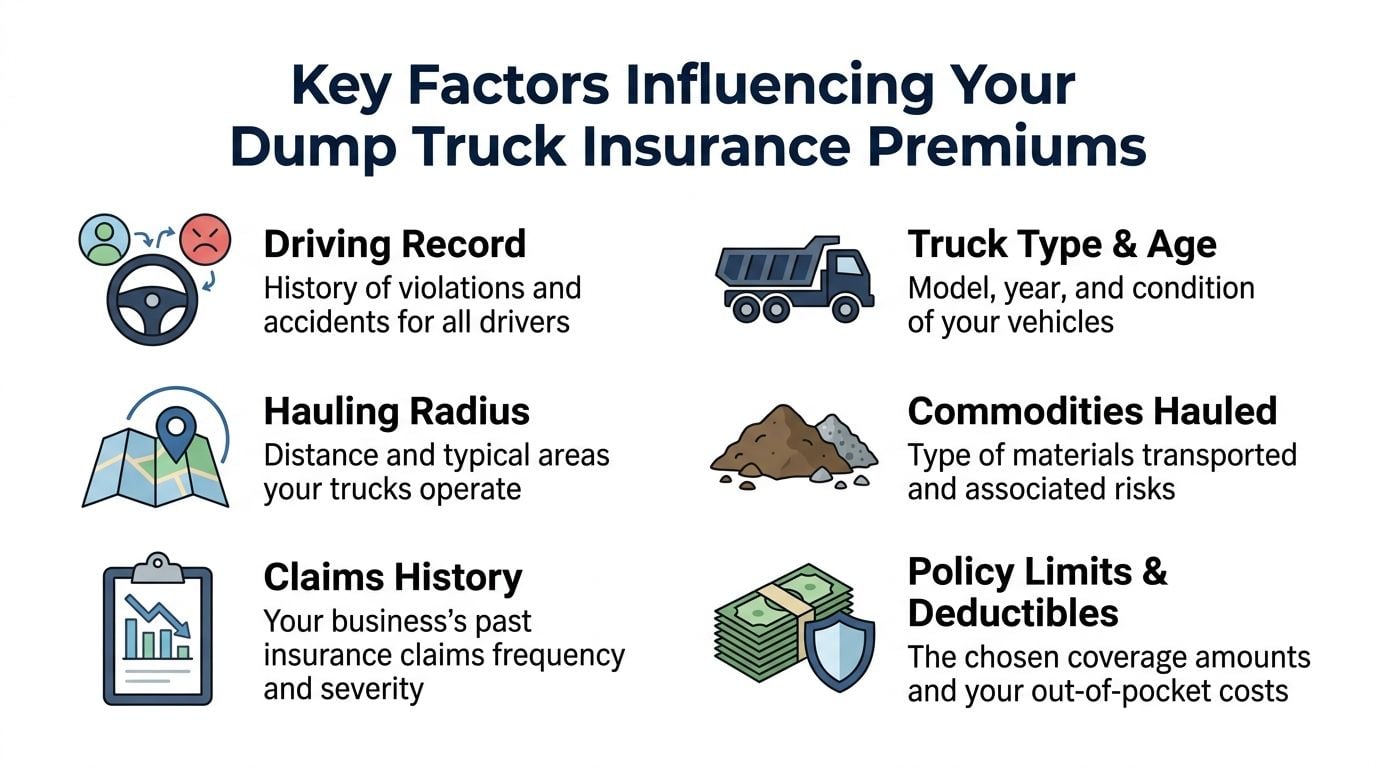

What Drives Your Dump Truck Insurance Premiums

Most contractors don't object to paying for insurance. They object to paying for a number they don't understand. Dump truck insurance gets easier to manage once the premium is viewed the way an underwriter views it, as a risk dashboard.

Commercial dump truck insurance is commonly budgeted at $400 to $1,200+ per month per truck in 2026 for many owner-operators and small fleets, with pricing driven by state, garaging ZIP code, driver experience, job type, operating radius, and claims history from the last 3–5 years, according to this breakdown of 2026 dump truck insurance pricing factors.

How underwriters read a dump truck account

Underwriters usually focus on exposure, not just equipment.

A concrete contractor gives a clear example. Hauling clean aggregate into a site is one kind of risk. Hauling broken concrete and debris out of a demolition-heavy environment is another. The truck may be similar, but the use class changes the claim picture.

The main rating factors usually include:

- Driver quality: A cleaner record and stronger experience profile generally make an account easier to place.

- Garaging location: Where the truck is based affects theft, traffic, road conditions, and claim frequency.

- Operating radius: A truck running farther and in more varied conditions creates a broader exposure.

- Commodity and job type: Sand, gravel, dirt, asphalt, debris, and demolition material don't all underwrite the same way.

- Loss history: Prior claims matter because they show how the account has performed in actual operations.

A truck's prior condition also matters when insurers assess risk and value. For contractors buying used units, how vehicle history affects insurance is worth reviewing because accident history, title issues, and repair records can influence how an asset is viewed before it ever reaches the schedule.

The cost levers contractors can actually influence

Not everything is controllable. A business can't easily move its yard to a new ZIP code just to chase premium savings. But several cost drivers are manageable.

| Factor | Fixed or controllable | Practical move |

|---|---|---|

| Garaging area | Mostly fixed | Make sure the insurer has the correct operating details |

| Driver experience | Controllable over time | Use stricter hiring and retention standards |

| Claims history | Controllable over time | Improve reporting, maintenance, and site procedures |

| Job classification | Controllable | Describe operations accurately instead of using broad labels |

| Radius | Sometimes controllable | Keep listed operating territory aligned with real work |

Field insight: A sloppy application often costs more than a risky one that's documented well.

What doesn't work is hiding exposure. If a contractor says the operation is local aggregate hauling but regularly takes demolition debris to distant disposal sites, the quote may come in wrong and the account may face trouble later. Accurate classifications, clean driver information, and realistic operating details usually produce better results than trying to shave premium with incomplete descriptions.

Smart Add-Ons Endorsements and Specialty Policies

A standard dump truck policy rarely covers every issue that shows up in construction and trade work. The biggest coverage problems usually come from assumptions. A contractor assumes the rented truck is covered. Assumes a spill is covered. Assumes the project owner's endorsement request is minor. Then a claim or certificate request exposes the gap.

Common gaps in a basic policy

One of the most common trouble spots is hired and non-owned auto liability. A paving contractor may rent an extra dump truck during a busy stretch or have an employee use a personal vehicle for business errands tied to the operation. If the policy doesn't address that exposure, the business may be carrying liability it didn't mean to retain.

Another frequent issue is pollution liability. Contractors hauling soil, asphalt grindings, debris, or material from messy sites often assume any fluid leak or contaminated release is just another claim under the auto policy. It often isn't that simple. If a release triggers cleanup, disposal, or third-party contamination allegations, standard policies may not respond the way the contractor expects.

The phrase “we thought that was covered” usually shows up after the expensive part.

Add-ons that make sense for trade contractors

The right add-ons depend on the work, but several come up often in dump truck operations:

- Hired and non-owned auto liability: Useful when the business rents, borrows, or relies on vehicles it doesn't title itself.

- Pollution liability: Important for contractors that could create a cleanup event from fuel, hydraulic fluid, contaminated material, or runoff.

- Additional insured endorsements: These matter when a GC, municipality, or owner requires status under the contract. Contractors dealing with upstream parties should understand the role of an additional insured endorsement, because the wording affects whether the certificate matches the agreement.

- Gap-related protection for financed or leased equipment: This can matter when loan balances and equipment values don't line up after a major loss.

A demolition contractor is a strong example. The truck may spend part of the week hauling concrete, part hauling mixed debris, and part moving in and out of sites controlled by different upstream parties. That operation often needs more than a bare auto policy because the contractual and environmental exposure shifts from job to job.

What works is adding endorsements that solve a known operational problem. What doesn't work is collecting every optional coverage without tying it back to a real exposure. Dump truck insurance should be built around how the trucks are used, who hires the business, and what can go wrong between loading, transport, unloading, and site access.

Risk Scenarios How Coverage Responds on a Bad Day

Insurance becomes real when a bad day hits at the same time as a tight schedule. Dump truck operations create that kind of pressure because one incident can damage property, injure a worker, and sideline the truck all at once.

Scenario one property damage during site access

A site contractor sends a dump truck into a commercial project with limited maneuvering room. The driver misjudges the backing angle and damages a newly installed fence near the access route.

That's the kind of claim that typically points first to auto liability for damage caused to someone else's property by the insured truck. If the contract also creates downstream obligations, the claim handling may involve more than just the repair bill. Certificate wording and contract status can matter too.

The trade lesson is simple. Tight sites create expensive low-speed claims. Contractors often focus on highway exposure, but many dump truck losses start with backing, turning, and positioning around other people's property.

Scenario two injury and truck damage during dumping

A gravel hauler raises the bed at a rough jobsite while unloading. The truck makes contact with an overhead line area or unstable ground condition, the driver is injured, and the truck suffers major damage.

In that situation, two different coverage lines may come into play. Workers' compensation is the coverage that generally responds to an employee injury tied to the job. Physical damage is the part that addresses the insured truck itself, assuming the loss falls within the policy terms.

A utility contractor sees versions of this risk often. Dumping on uneven shoulders, temporary haul roads, and active site pads creates a mechanical and bodily injury exposure at the same time.

Scenario three fluid release on finished pavement

A dump truck develops a hydraulic leak while crossing a finished asphalt lot at a project closeout stage. The pavement is stained, cleanup is needed, and the owner wants immediate remediation.

That's where pollution liability can become the difference between a manageable claim and a disputed mess. A contractor that assumed every leak was automatically part of ordinary auto coverage may find out too late that cleanup-related expenses follow different rules.

Good dump truck insurance doesn't work as one policy. It works as a coordinated set of responses.

These scenarios matter because they show the trade-off in buying cheap coverage. A stripped-down policy may keep monthly cost down. It may also leave the business paying out of pocket when a claim involves the truck, the employee, the site owner, and environmental cleanup at the same time.

Getting the Right Program Owner-Operator vs Fleet Operator

The right insurance program depends on whether the business is one truck and one decision-maker, or several trucks with multiple drivers, job locations, and certificate requests moving at once.

What an owner-operator should have ready

An owner-operator usually needs efficiency. The insurance has to satisfy legal requirements, match contract language, and stay affordable enough that the truck can still make money.

For solo operators, the best quoting preparation usually includes:

- Vehicle details: VINs, unit descriptions, and whether the truck is financed or leased

- Driver information: License details, experience, and a clean account of prior issues

- Operating profile: Radius, garaging location, and the actual materials hauled

- Target work: Contract requirements, requested limits, and any special certificate language

For drivers comparing business models, this owner operator driver comparison is a useful outside read because it helps frame what changes when a driver moves from employment into ownership. Insurance responsibility is one of those changes, and it's often bigger than expected.

A landscaping contractor with one dump truck is a good example. If that business only buys to the legal minimum but starts taking larger commercial site jobs, the policy can become obsolete before the truck changes.

What changes when the fleet starts growing

A fleet operator's challenge is different. The issue isn't just buying a policy. It's controlling variation across drivers, trucks, contracts, and jobs.

A growing operation usually needs to tighten these areas:

Driver onboarding and safety procedures

One weak driver can affect the whole account. Hiring standards, internal training, and documented expectations matter.Certificate management

If several jobs are active at once, certificate requests need to be accurate and fast. Missed wording can delay work.Maintenance and claim reporting discipline

Faster reporting and stronger equipment controls help keep small losses from becoming account-wide problems.Market fit for difficult risks

New ventures, unusual operations, or loss-heavy accounts sometimes need excess and surplus insurance solutions when standard placements won't fit the exposure cleanly.

A practical quoting checklist for any contractor seeking dump truck insurance should include the truck schedule, driver list, business description, hauling radius, garaging address, prior insurance details, and copies of any job contracts that specify limits or endorsements. The more precise the information, the more useful the quote.

What works is building the program around the work the business wants next, not just the work it did last year. What doesn't work is waiting until a certificate is rejected to find out the policy was designed for a smaller operation than the business has become.

Contractors that need dump truck insurance that fits real construction work can get a free quote or coverage review from Coverage Axis. A licensed advisor can review current limits, contract requirements, vehicle schedules, and coverage gaps, then help build a right-sized program for owner-operators, small fleets, and growing trade businesses.