A drywall subcontractor lands a new job in Portland, adds a helper for demo days, and hires a second crew for a short out-of-state project. The bid looks fine on paper. Then the paperwork starts. The general contractor wants proof of active workers' comp. The carrier asks whether the helper is an employee or an independent contractor. The owner realizes the officer payroll on the quote doesn't match how the business is set up. That's where Oregon workers compensation insurance stops being a simple line item and becomes a compliance issue.

Oregon can look inexpensive at first glance. One 2026 Oregon workers' comp cost analysis estimates an average cost of $104 per month per employee, with rates about 27% lower than the national average. The same analysis also says high-risk operations like Transportation & Logistics can run $316 per month, which is a good reminder that trade classification still drives the bill. Low rates don't protect a contractor who classifies labor wrong, leaves an owner off payroll incorrectly, or sends a crew across state lines without checking how the policy applies.

Contractors that operate in more than one state often run into another problem. Workers' comp is state-based, not one national policy rulebook. Anyone comparing Oregon to nearby markets may find understanding California workers' compensation useful because it explains the same core point from a neighboring state's angle. For Oregon contractors trying to line up licensing, payroll, and field labor, the practical issue isn't just cost. It's getting the structure right before a claim, an audit, or a project award exposes the gap.

For broader risk planning beyond workers' comp alone, Oregon contractors usually need to coordinate it with commercial insurance built for Oregon businesses.

Table of Contents

- Your Guide to Oregon Workers Compensation Insurance

- The Legal Requirement for Contractors in Oregon

- Choosing Your Coverage SAIF vs Private Insurers

- How Workers Comp Rates Are Calculated for Your Trade

- Managing Audits Subcontractors and Certificates

- Claims Handling and Interstate Projects

- Cost-Saving Strategies and Compliance Checklist

Your Guide to Oregon Workers Compensation Insurance

Oregon workers compensation insurance matters most when a contractor is in transition. A solo electrician hires a first apprentice. A roofer turns a casual day labor arrangement into a regular crew. A general contractor starts using a mix of W-2 workers and specialty subs. Those are the moments when a cheap quote can become an expensive mistake.

The state is known for relatively low workers' comp costs, but the contractor problems are rarely about the headline rate. They usually come from classification, ownership status, and who counts as a worker. A flooring contractor may assume a spouse on payroll is treated one way, while the carrier treats that person another way. A framing business may call a laborer a subcontractor, but if that person works under direction, uses company tools, and shows up when told, the label on the invoice won't control the outcome.

Practical rule: If a contractor has to explain why someone isn't a worker, that arrangement deserves a hard review before the policy binds.

A good Oregon workers compensation insurance setup does three things:

- Matches the actual crew structure: Owners, officers, employees, and uninsured subs need to be sorted correctly.

- Fits the trade work being performed: Electrical, roofing, painting, excavation, and delivery exposures don't get treated the same.

- Holds up under audit and claim review: If records fall apart later, the original quote won't matter.

A plumbing contractor with two vans and one helper needs a different approach than a restoration firm running emergency calls with rotating labor. The policy can still be straightforward. The operation usually isn't. That's why the right starting point is not "Who has the lowest rate?" It's "How is the business staffed and where are the workers going?"

The Legal Requirement for Contractors in Oregon

For contractors, the legal question usually isn't whether Oregon cares about workers' comp. It does. Instead, the question is when a person on the job becomes a subject worker and triggers coverage obligations.

Oregon's guidance on workers' comp coverage emphasizes that most employers need it, while also recognizing that some owners may elect out and some independent contractors may qualify only if they meet strict tests. The practical gap for contractors is that many businesses don't stay in one clean category for long. A solo remodeler can become a covered employer fast after adding one helper, a part-time laborer, or a mixed crew that doesn't fit a true subcontractor model. Oregon's overview also notes a 2024 biennial study index rate of 89 cents per $100 of payroll, described as the lowest in the study's history, but low statewide rates don't remove the need for careful worker status analysis under Oregon's workers' compensation insurance overview.

When a helper becomes more than casual labor

Take a general contractor finishing a kitchen remodel. The GC brings in a helper for debris removal, material handling, and punch work two or three days a week. The helper uses the GC's trailer, takes direction from the GC, and doesn't carry separate insurance. On a jobsite, that person looks like part of the crew. That's the arrangement that creates trouble when a contractor tries to force it into a 1099 box.

A label doesn't decide the issue. The working relationship does.

If the business controls the schedule, directs the work, and folds the person into daily operations, workers' comp exposure usually follows the facts, not the invoice format.

Owner exceptions are narrow, not universal

Sole proprietors, partners, and some business owners may have different treatment than ordinary employees. That's where many small trade firms get overconfident. A solo painter with no employees may have more flexibility. A corporation with officers on payroll, plus a field tech, is a different situation. A landscaping company with family members working part time also needs a careful review, because family or ownership ties don't automatically solve the subject-worker question.

Common contractor trouble spots include:

- One regular helper paid informally: If the person works like an employee, Oregon may view them that way.

- Mixed W-2 and 1099 labor: This often creates the biggest audit disputes.

- Uninsured specialty subs: If they don't stand as true independent businesses, the hiring contractor can inherit the exposure.

- Officer confusion: Businesses often assume an officer is automatically excluded. That assumption can be wrong depending on structure and election.

Contractors that need a clearer framework for role assignment often benefit from reviewing general contractor insurance requirements alongside workers' comp rules, because hiring structure and contract flow usually create the problem together.

What doesn't work

Three approaches tend to fail contractors in Oregon:

- Paying everyone on a 1099 and hoping that solves it

- Assuming part-time means exempt

- Waiting until license renewal or audit season to fix the labor setup

An electrical contractor who hires one apprentice, directs every task, and provides the van and tools shouldn't wait for a claim to find out whether coverage was required. By then, the classification argument is over. The facts are already on record.

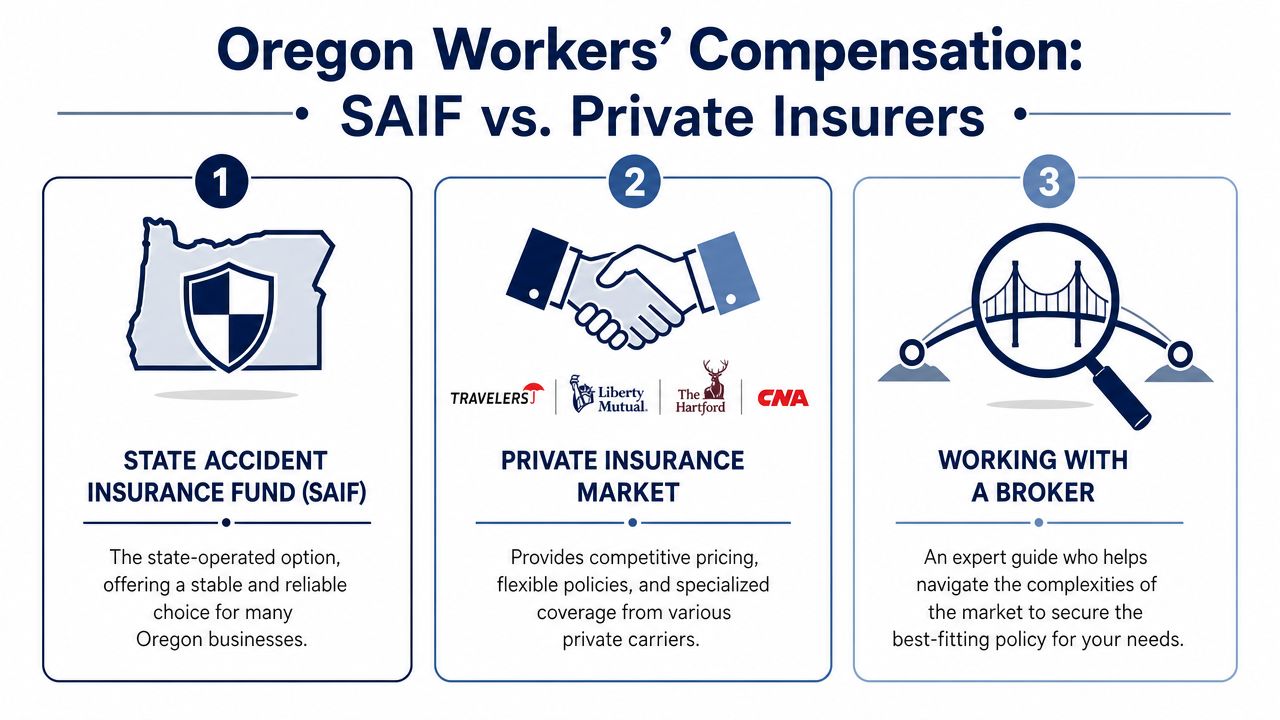

Choosing Your Coverage SAIF vs Private Insurers

Contractors shopping Oregon workers compensation insurance usually end up looking at three paths. The state fund, the private market, or an assigned risk option if regular placement gets difficult. Each path can work. The fit depends on trade, claims history, crew size, and how clean the operation looks on paper.

To understand why this market has long been shaped by both the state fund and private carriers, Oregon's workers' compensation market report shows $766.7 million in direct written premium in 2009, with SAIF posting an 88.6 loss ratio and Liberty Northwest leading private carriers at $74.9 million in direct premium written according to the Oregon Department of Consumer and Business Services market reporting page.

Three paths contractors usually consider

| Coverage path | Best fit | What contractors usually like | What can frustrate them |

|---|---|---|---|

| SAIF | Newer firms, steady operations, many standard trade risks | Stable option, familiar Oregon presence, often a practical place to start | May not always be the best fit for every account profile |

| Private insurers | Contractors with clean records, specific trade niches, or stronger submission quality | More room for policy flexibility and underwriting variation | Appetite can change by trade and loss history |

| Assigned risk | Businesses that can't place coverage in the regular market | Access to required coverage when other doors close | Usually a last-resort path, not a strategy for long-term cost control |

A new painting contractor is a good example. If the business has one owner, one employee, solid payroll records, and no unusual exposure, either SAIF or a private carrier could make sense. If the same contractor has frequent turnover, no clear subcontractor controls, and inconsistent job descriptions, the options narrow quickly.

Contractors looking at entry-level placement questions often need the same plain-English guidance found in workers' comp planning for small businesses, especially when the operation is growing faster than the paperwork.

How trade type changes the decision

A residential electrician and a commercial roofer don't present the same risk profile. Even when both are well run, carriers react differently to fall exposure, fleet use, subcontracted labor, and claim history. That's why shopping by price alone usually produces a bad result.

A few practical trade examples show the difference:

- Electrician: Often easier to place if payroll is clean, ownership is documented, and the operation doesn't blur into general contracting.

- Roofer: More likely to face tighter underwriting scrutiny. Claims handling and appetite matter as much as the quoted number.

- Remodeling GC: Usually lives or dies by subcontractor controls and whether uninsured labor can spill back onto the policy.

- Outdoor services contractor with irrigation crews: Multi-state travel, vehicle use, and seasonal labor can create questions a simple online quote won't catch.

The best policy choice is usually the one that still makes sense at audit time, not the one that looked cheapest on the first proposal.

Self-insurance exists within the broader workers' comp system, but for most trade contractors it isn't a practical near-term option. The practical decision is almost always between a state fund path, private-market placement, or assigned risk if the account has become hard to place.

How Workers Comp Rates Are Calculated for Your Trade

Premium starts with payroll and classification, but that's only the surface. Oregon workers compensation insurance for contractors gets priced based on what work the crew performs, who is included, and how well the records support those decisions.

A concrete contractor may have one class of field labor, one clerical employee, and an owner who occasionally runs a crew. A plumbing shop may have service techs, apprentice labor, warehouse support, and an officer doing sales. If all of that gets thrown into the same bucket, the quote may look clean and still be wrong.

What actually drives the premium

The pieces that usually matter most are:

- Class code assignment: A framing crew doesn't carry the same exposure as office staff or a light service trade.

- Payroll by role: The cleaner the payroll split, the cleaner the premium basis.

- Loss history: Frequent or severe claims can change how an account is priced or whether it gets regular market access at all.

- Operational mix: Shop work, road work, installation, hauling, and subcontracted labor all affect how underwriters view the account.

A contractor doesn't need to memorize class manuals to make better decisions. The useful question is simpler. "Does the payroll breakdown match what people do all day?" If not, the number is unstable.

Owner payroll is where many quotes go wrong

Oregon is unusually specific about payroll treatment for owners. For 2024, sole proprietors, partners, and LLC members who elect coverage must be assigned $67,400 in annual payroll, while covered corporate officers must be written on payroll of at least $67,600 and no more than $270,400, as summarized in this Oregon workers' compensation state rule guide.

That matters in real jobs.

A small electrical contractor organized as an LLC might tell the agent, "The owner only takes draws." For workers' comp, that doesn't end the discussion if the owner elects coverage. A corporation with two officers can't just pick a low number because cash flow is tight. The state payroll basis still applies. When a quote ignores that, the audit later corrects it.

Field note: Owner classification errors usually don't show up when the policy is issued. They show up when payroll records, tax forms, and job duties get compared side by side.

For contractors trying to control long-term cost, claim history also feeds into the experience side of pricing. A business that understands how workers' comp experience modification works is usually better positioned to connect safety performance with premium results.

A trade example that causes audit pain

Consider a siding contractor with:

- one owner who works in the field,

- one office spouse handling invoices,

- two installers on payroll,

- and one "subcontractor" crew used on overflow.

The likely trouble points are obvious. Is the owner included correctly. Is the office role separated properly. Is the overflow crew insured and operating independently. Those questions have more impact on the final premium than most contractors expect.

What works is disciplined setup on the front end. Separate duties clearly. Keep payroll by role. Document owner elections. Verify outside labor before the policy starts, not after the audit request arrives.

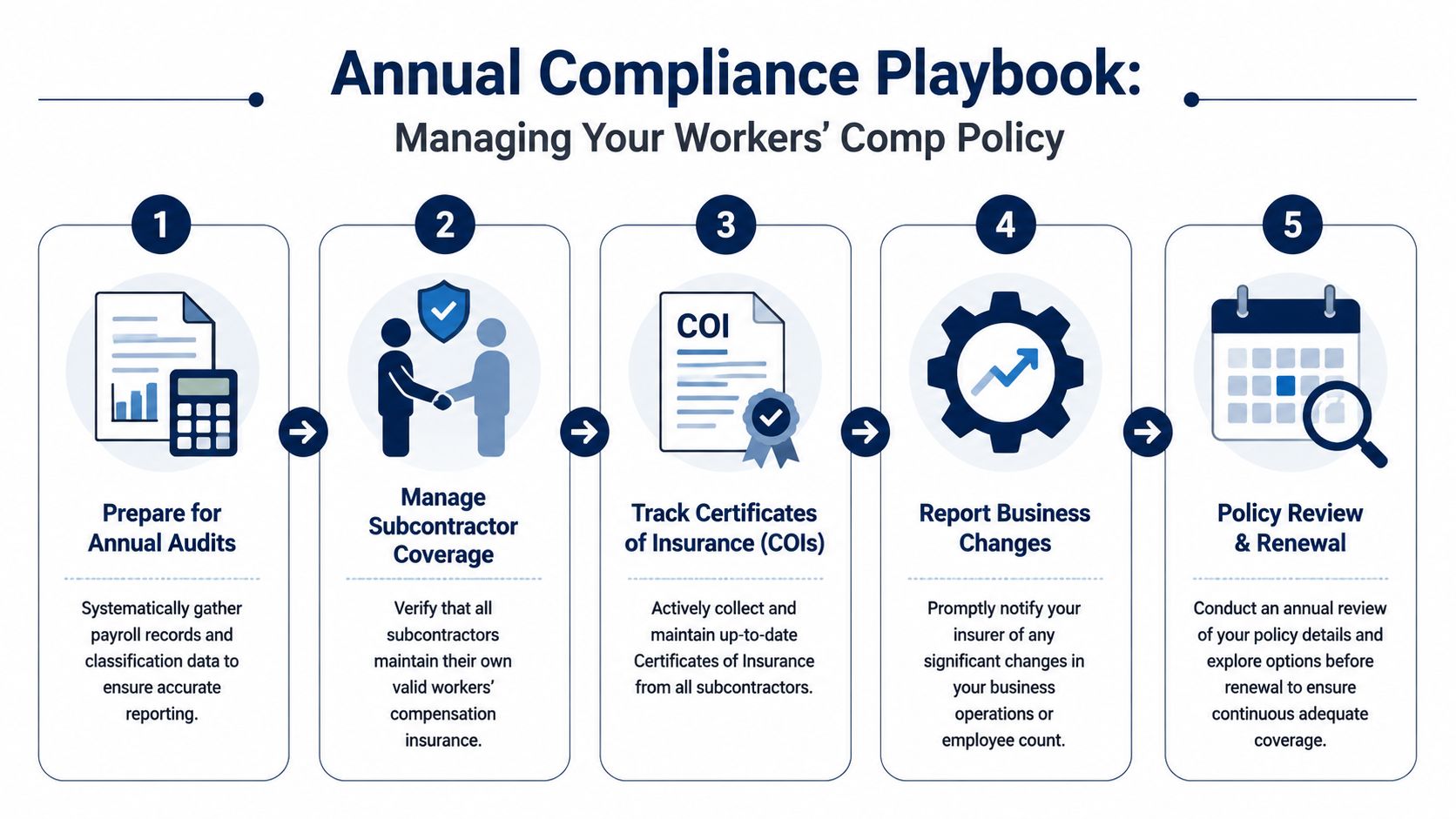

Managing Audits Subcontractors and Certificates

Most workers' comp problems don't start with a claim. They start with sloppy records that get exposed in an audit. A remodeling GC may run clean jobs all year, then get hit with extra premium because payroll wasn't separated, owner treatment wasn't documented, or subcontractor coverage wasn't verified.

In Oregon, proof of coverage is tied to the state's electronic reporting system. Insurers report coverage electronically, and the state defines proof of coverage as that electronic record for a specific employer, which allows real-time verification by business name or FEIN through Oregon's proof of coverage system. For contractors hiring subs, that record is more reliable than taking someone's word for it.

What an audit usually looks for

An auditor usually wants to connect a few basic dots. Who was paid. What work they performed. Whether uninsured labor should be included. Whether payroll was assigned to the right buckets.

For a contractor, the cleanest audit file usually includes:

- Payroll records by job role: Field labor, clerical, and executive duties shouldn't be mixed casually.

- Owner documents: Entity type, officer status, and elections should be easy to produce.

- Subcontractor files: Current certificates plus independent verification matter.

- Job descriptions: These help support class assignment if duties get questioned.

A masonry contractor that keeps one spreadsheet for everyone and pays overflow labor from miscellaneous expense accounts is asking for a fight. A contractor that keeps payroll organized by function usually gets through audit with far less friction.

How a GC should handle subcontractor paperwork

A certificate of insurance is useful, but it shouldn't be the only checkpoint. A residential GC using tile setters, drywall crews, and short-term labor should verify that the subcontractor's workers' comp is active before work begins and again if the project stretches on.

A disciplined process looks like this:

- Collect the certificate before mobilization

- Verify the business in the state's proof-of-coverage system

- Match the legal business name to the hiring contract

- Track expiration dates

- Pause work if coverage can't be confirmed

Contractors that regularly hire outside labor often need stronger procedures around workers' comp requirements for subcontractors, because uninsured subs can become the hiring contractor's premium problem later.

A certificate in a file cabinet doesn't help much if the policy canceled weeks before the worker showed up on the job.

A restoration contractor is a good example. Emergency jobs move fast. Crews get called in after hours. That speed is exactly when verification gets skipped. The safest habit is simple. No active coverage confirmation, no work start.

Claims Handling and Interstate Projects

A claim tests whether the policy was set up correctly. Interstate work tests whether the contractor understood where the policy applies. Oregon contractors run into both problems more often than they expect.

A landscaping crew working in Eugene may have a routine strain injury one week and a temporary project across the river the next. The first issue is claims handling. The second is state exposure. Both need quick decisions, not guesswork.

What to do after a jobsite injury

When a framer twists a knee carrying sheets upstairs or a plumber gets hurt lifting water heaters, the contractor's first move should be practical and documented.

- Get medical attention: Immediate care comes first.

- Report the injury promptly: Delays create confusion and can complicate claim handling.

- Document the facts: Time, task, location, witnesses, and what equipment was involved.

- Keep communication clear: The injured worker needs to know what happens next.

- Use modified duty if appropriate: Return-to-work planning often helps both the worker and the business.

For contractors trying to understand wage-replacement concepts that can come up during a claim, Bell Law's guide to Oregon TTD is a useful plain-English reference on temporary total disability.

When Oregon crews cross state lines

Traveling crews create a different kind of risk. An Oregon-based contractor may assume an Oregon policy automatically follows the employee everywhere. That's not always how it works.

A legal explainer on Oregon reciprocity notes that the state has agreements that can sometimes remove the need for an out-of-state contractor to buy an Oregon policy for temporary work, and that the answer depends on the worker's home state, the duration of work, and whether the employer has extraterritorial coverage under the home policy, as discussed in this Oregon reciprocity and extraterritorial coverage article.

That creates real trade decisions:

- Oregon electrician taking a short Washington job: The policy should be reviewed before mobilization, not after payroll is posted there.

- Out-of-state specialty crew entering Oregon temporarily: Reciprocity may help, but only if the home-state setup meets the requirements.

- GC with rotating crews across western states: Payroll allocation and state-specific coverage need active management.

Multi-state work is where many otherwise solid contractors discover they bought a local policy for a regional operation.

A contractor doesn't need to panic every time a crew crosses a border. But they do need to ask the right questions early. Which state employs the worker. How long will the work last. Does the policy extend properly. If those answers aren't clear, the exposure isn't under control.

Cost-Saving Strategies and Compliance Checklist

The cheapest Oregon workers compensation insurance strategy is usually the one that avoids correction later. Audit charges, uninsured-sub issues, and misclassified owner payroll cost more than careful setup ever will.

A practical checklist for contractors:

- Review worker status: Make sure helpers, part-time labor, and 1099 crews are classified based on how they work.

- Confirm owner treatment: Entity structure and payroll basis should match the policy.

- Separate payroll clearly: Field, office, and executive duties need clean records.

- Verify every subcontractor: Collect certificates and confirm active coverage before work starts.

- Report operational changes early: New trade work, new states, and bigger crews should be disclosed before renewal.

- Support return to work: A documented modified-duty approach can help keep claims from dragging out.

- Shop the market periodically: A well-organized account is easier to place and easier to compare.

For a roofer, that may mean tightening subcontractor controls. For an HVAC contractor, it may mean cleaning up officer payroll. For a GC, it often means building a repeatable paperwork process that the office can maintain.

Contractors that want a second set of eyes on owner classification, subcontractor exposure, or multi-state crew issues can get a free quote or coverage review through Coverage Axis. A plain-English review can help identify whether the current workers' comp setup matches the way the business really operates before an audit, claim, or project requirement exposes the gap.