A lot of contractors are sitting in this exact spot right now. The bid is good, the scope is clear, the crew is ready, and then the contract stalls because the general contractor wants to be added as an additional insured. For an electrician on a commercial fit-out, that request can feel like paperwork that slows down work and ties up the office.

It isn't just paperwork.

An additional insured endorsement is often the pass that gets a subcontractor onto better jobs with larger builders, stricter owners, and tighter contract terms. In plain language, it lets another party use part of the contractor's liability protection for claims tied to that contractor's work. The easiest way to think about it is borrowed insurance. If a plumbing sub causes a loss, the GC wants the plumbing sub's policy involved first for that job-related exposure.

That matters for three reasons. It affects whether the contract gets signed. It affects how much protection the contractor is giving away. And it affects whether a certificate on file matches what the policy really says when a claim lands.

Busy trade business owners don't need theory. They need to know what this endorsement means for liability, what it costs, what forms matter, and where the traps are hiding. The biggest trap is simple. A certificate can suggest comfort, while the actual endorsement may be much narrower than the contractor, owner, or GC expects.

Table of Contents

- Introduction What This Endorsement Means for Your Next Bid

- What Is an Additional Insured Endorsement

- The Most Common Endorsement Forms for Contractors

- Ongoing vs Completed Operations A Tale of Two Risks

- Understanding Your Coverage Limits and Priority

- How to Get and Verify an Endorsement

- The Real Costs and Risk Management Benefits

- Conclusion Protect Your Business and Win More Work

Introduction What This Endorsement Means for Your Next Bid

A skilled electrician wins a commercial tenant improvement project. The pricing is tight but workable. Then the GC sends over insurance requirements asking for additional insured status, completed operations, primary and noncontributory wording, and a waiver of subrogation. The work doesn't move until that insurance package lines up.

That moment decides a lot more than compliance.

For contractors and trade business owners, an additional insured endorsement is one of the most common contract requirements on private work, municipal jobs, and multi-trade commercial projects. It's a tool for risk transfer. The party hiring the contractor wants claims arising out of that contractor's work to hit the contractor's policy, not their own, when possible.

A job site analogy makes it simple. If a contractor brings a lift onto a site, that lift supports the contractor's work, not everyone's work on the project. An additional insured endorsement works in a similar way. It extends the contractor's liability protection to another party, but only within the boundaries of the endorsement and the policy.

Practical rule: If the contract requires additional insured status, the contractor should treat the endorsement as a bid qualification item, not an afterthought.

For electricians, plumbers, roofers, and other trades, understanding this endorsement helps with three daily business problems. It keeps contracts from stalling. It prevents false confidence based on a certificate alone. And it helps the contractor decide whether the requested wording is reasonable or whether it gives away more protection than the job is worth.

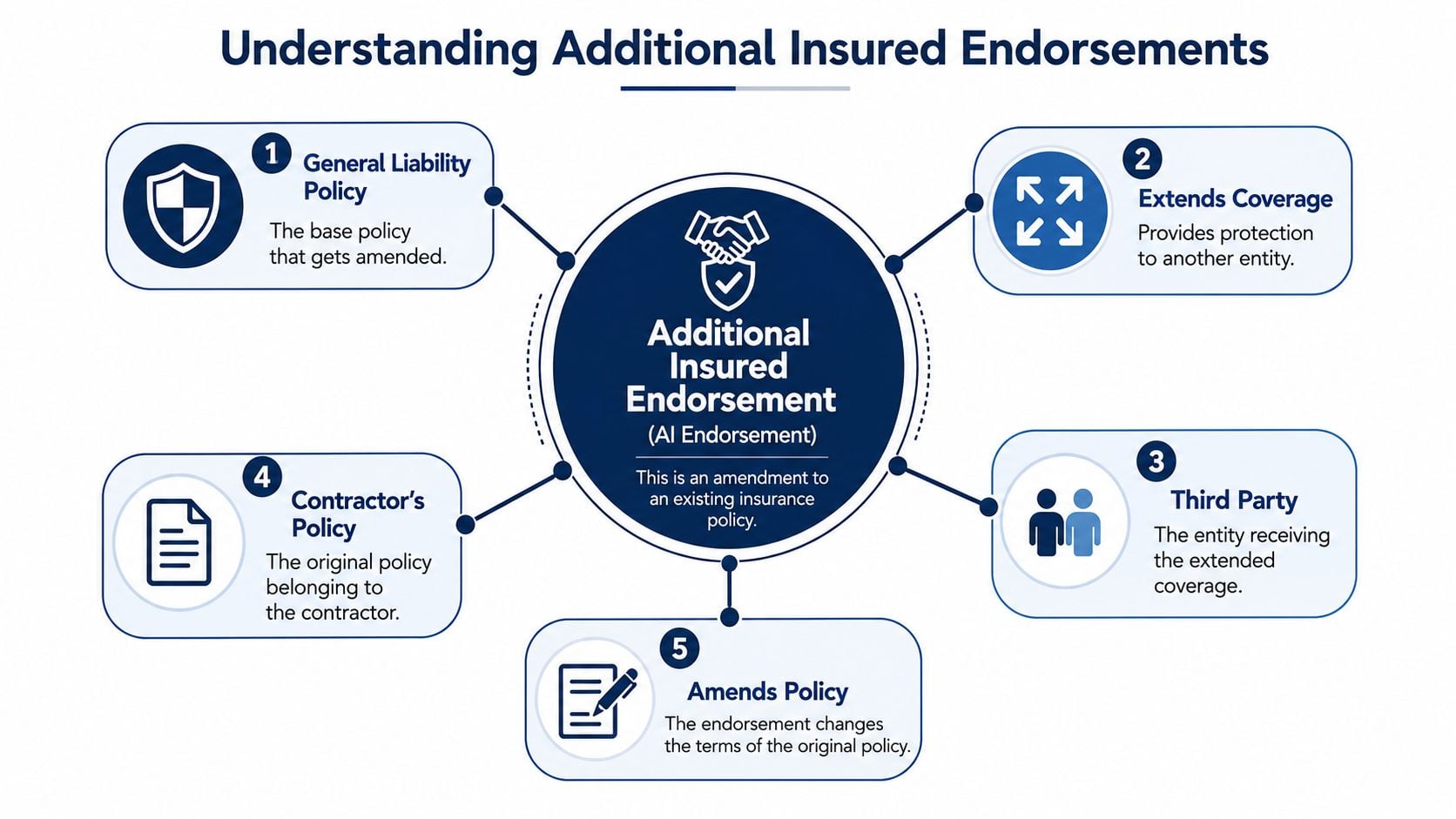

What Is an Additional Insured Endorsement

An additional insured endorsement is an amendment to a liability policy that extends some coverage to another party, usually a general contractor, property owner, landlord, or project manager. The named insured still owns the policy. The added party doesn't become a full policyholder. They receive limited, derivative coverage tied to the named insured's work.

Why contractors get asked for it

The purpose is usually risk shifting, not risk sharing. One verified analysis explains that additional insured endorsements transfer financial responsibility for specific losses from one party to another's insurer and that all parties still share the same total policy limits available under the policy, not a separate new limit pool, in this discussion of modern risk management and common AI forms. That's why GCs ask for it so often in construction and specialty trade contracts.

A plumbing example shows how this works in the field. A plumber roughs in a line on a retail build-out. A leak later damages finished flooring and a wall below. The owner sues the GC and the plumbing sub. The GC wants access to the plumbing contractor's liability policy for the portion of the claim arising from the plumber's work.

Contractors who need a refresher on the base policy behind these endorsements should understand how general liability insurance for contractors responds before they agree to contract language.

What it does not do

A common pitfall for many contractors relates to this point: Additional insured status doesn't usually mean full policy protection for the added party's own mistakes. One verified source states: “This means that the additional insured endorsement would not likely afford any coverage for a claim brought against the Additional Insured for its own act (or failure to act)” in this white paper on additional insured limitations.

That matters on real jobs.

- Electrician example: If the claim arises from the electrician's temporary power setup, the GC may have access to the electrician's policy as an additional insured.

- Roofer example: If the building owner independently ignored known drainage problems unrelated to the roofer's work, the owner shouldn't assume the roofer's endorsement fixes that exposure.

- Plumber example: If the GC's superintendent directs work unsafely and creates a separate loss, the plumber's endorsement may not protect the GC for that independent act.

A certificate may show “AI” in a box or description line. That still doesn't answer the key question. What exactly did the endorsement add, and how narrowly was it written?

The Most Common Endorsement Forms for Contractors

Not all additional insured endorsements do the same job. The form number matters because it determines when coverage applies and how broad the extension is. Contractors who skip that detail often assume they've met the contract when they've only met part of it.

A roofer job from start to finish

A roofer starts a re-cover project on a commercial building. On day three, a crew member leaves part of the roof exposed before weather rolls in. Water enters the building and damages ceiling tiles and inventory. That's an ongoing operations scenario because the work is still underway.

Months later, the project is complete. Then another problem surfaces. Water intrusion appears around penetrations, and the owner alleges the completed roofing work failed. That's a completed operations issue because the claim arises after the roofer finished the job.

Those are different risk periods. One endorsement may address the first and miss the second.

How the common forms differ

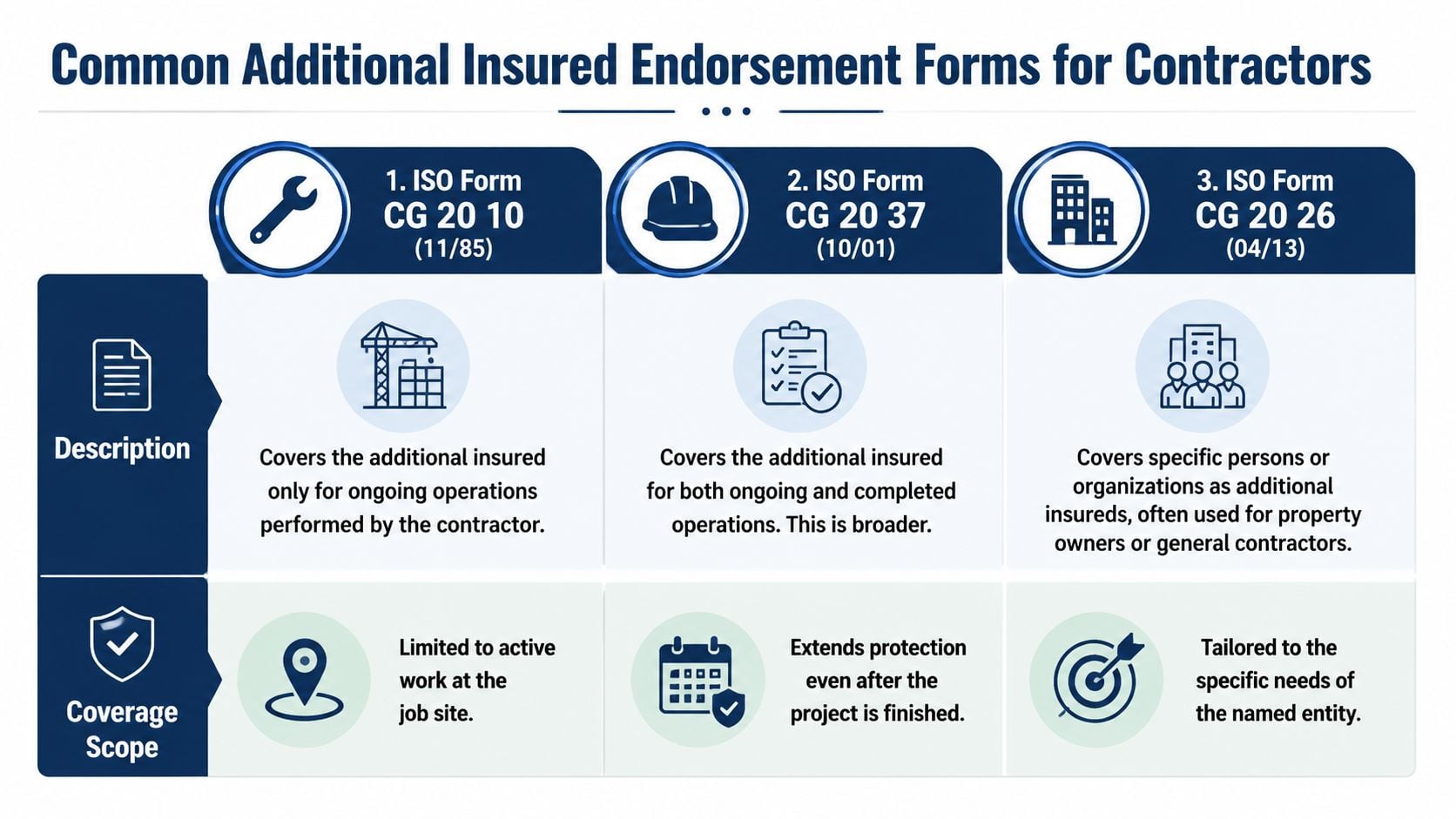

Three forms show up often in contractor conversations:

| Form | What it generally does | Trade example |

|---|---|---|

| CG 20 10 | Extends coverage for liability tied to ongoing operations | An electrician drops conduit from a lift during active work and damage follows |

| CG 20 37 | Extends coverage for completed operations exposures | A plumbing installation later fails after turnover and causes property damage |

| CG 20 33 | Provides blanket ongoing operations coverage when a written contract requires AI status | A GC's subcontract requires AI status before a framing crew starts work |

A verified construction advisory states that CG2010 4/13 and CG2037 4/13 are required together to cover both ongoing and completed operations, and that without CG2037 a contractor's liability policy may not protect a project owner for claims arising years after project completion, as explained in this client advisory on additional insureds.

That's why many GCs ask for both forms or equivalent wording. One form handles the active phase. The other handles the tail risk after the tools are back in the truck.

The endorsement request isn't complete until the contractor knows whether the job requires protection during the work, after the work, or both.

For roofers, this distinction is obvious once a leak shows up after final payment. For electricians, it can be a failed connection discovered after occupancy. For plumbers, it can be a hidden fitting issue that doesn't surface until walls are closed and operations resume. The endorsement form decides whether the claim period matches the contract requirement.

Ongoing vs Completed Operations A Tale of Two Risks

An HVAC contractor installs rooftop units and interior controls on a commercial renovation. Midway through the project, a worker moves equipment through the building and cracks an expensive glass panel near the entrance. The owner looks to the GC. The GC looks to the HVAC sub. That's the first bucket of risk.

During the job

Claims that happen while the contractor is still performing the work usually fall into the ongoing operations category. The project is active. The crew is still on site. The punch list hasn't closed out.

This category catches the losses many contractors think about first because they're visible and immediate.

- Broken property on site: damaged finishes, storefront glass, doors, or tenant improvements

- Job-related injury allegations: someone says the trade's active work created a hazardous condition

- Site disruption losses: a mistake during installation causes a shutdown, water release, or unsafe condition

After the crew leaves

A year later, the same HVAC project has a different problem. A faulty connection in the installed system is blamed for a fire loss. The owner and GC still face the claim, but now the work is complete. The exposure didn't disappear when the contractor demobilized.

That's the second bucket. Completed operations applies after the work has been finished and put to use.

For electricians, this can be a wiring defect discovered after occupancy. For plumbers, it can be a concealed leak. For roofers, it can be water intrusion after several storms. Contractors who only think about active job site accidents often miss the longer tail.

Two contract terms that affect the bill

Additional insured requests often arrive with two related terms.

One is primary and noncontributory. In practical terms, that usually means the contractor's policy should respond first for covered claims tied to that contractor's work, without asking the GC's policy to share at the front end.

The other is waiver of subrogation. That usually means the contractor's insurer agrees not to turn around after payment and pursue recovery against the GC if the contract requires that waiver.

Contractors reviewing these requirements should also understand the contract-side promise behind them. A plain-English breakdown of contractual liability in construction agreements helps connect the endorsement request to the indemnity language in the subcontract.

If the subcontract pushes broad transfer obligations onto the trade contractor, the insurance wording needs to be checked line by line. Otherwise the contract may promise more than the policy delivers.

Understanding Your Coverage Limits and Priority

Many contractors assume that once a party is added as an additional insured, that party gets the same full protection as the named insured. That's not always how the endorsement works. The added party may share the policy limit, and the endorsement may cap or narrow what they can access.

One policy limit shared by more than one party

A verified example shows the issue clearly. Under a $2 million general liability policy, an additional insured may receive only $1 million in coverage if the endorsement limits their protection, even though the primary contractor retains the full $2 million, as described in this explanation of additional insured endorsements and policy limits. The lesson is simple. AI coverage can be partial, not equal.

That matters on larger losses because defense costs and indemnity obligations can burn through the same policy faster when more than one party is seeking protection.

Primary noncontributory and defense obligations

A flooring contractor provides AI status to a GC on a retail interior project. During installation, adhesive overspray damages nearby finishes and a dispute follows. The GC wants the flooring contractor's policy to defend first. That's the practical effect of primary and noncontributory wording when it applies.

Defense and indemnity are not the same thing.

- Defense: who pays for lawyers and claim handling

- Indemnity: who pays the settlement or judgment

- Priority: which policy is expected to respond first

If a contractor only looks at the certificate summary, those details can stay hidden. That's why policy wording matters more than the box checked on a form. Contractors comparing limit options should also understand how general liability coverage limits affect bidding requirements and loss scenarios.

A fast verification checklist

When reviewing an endorsement request, contractors should confirm these points:

- Correct legal entities. The named insured and the added party must match the contract exactly.

- Correct form type. Ongoing operations alone may not satisfy a project that also requires completed operations.

- Priority wording. If the contract calls for primary and noncontributory treatment, the policy documents should support it.

- Defense access. The contractor should confirm whether the additional insured receives defense, not just indemnity.

- Limit sharing. The added party is usually drawing from the contractor's policy, not a separate stack of insurance.

A COI can start this review. It can't finish it.

How to Get and Verify an Endorsement

The cleanest time to deal with an additional insured endorsement is before the contract is signed and before the crew is scheduled. Waiting until mobilization week creates the worst version of this problem. The office scrambles, the GC pushes for revised paperwork, and the contractor may accept wording without understanding what it does.

What to send the agent or broker

A grounds maintenance contractor working for a property management company is a good example. The grounds maintenance contractor gets a contract requiring AI status for the management company, the property owner, and possibly affiliates. If the request sent to the agent is vague, the paperwork often comes back wrong.

The contractor should send:

- The contract requirement page so the insurance request matches the actual obligation

- The full legal name of every party that needs status

- The job description and project dates so the policy timing makes sense

- Any required wording for ongoing operations, completed operations, primary and noncontributory, or waiver of subrogation

Why the certificate is not enough

This is the gap that causes real trouble. Recent court rulings have invalidated blanket additional insured coverage for parties not explicitly named in writing. To avoid non-coverage, construction contracts must require a direct written agreement with each proposed additional insured or expressly name each AI in the policy itself, not just rely on certificates, which are informational only, as outlined in this legal analysis of additional insured status and written agreement requirements.

That rule hits electricians, plumbers, and roofers hard because those trades often work under layered contracts where several upstream parties expect to be protected.

A certificate helps show what was issued at that point in time. It does not replace the endorsement itself. Contractors who need a reference for the document side of this process can review a certificate of insurance template to understand what the certificate does and does not prove.

A practical review process

A contractor doesn't need to become a coverage lawyer to verify this correctly. A simple office process works.

Ask for the actual endorsement form, not just the certificate. Then match the form language and named parties against the subcontract before work starts.

A workable review flow looks like this:

- Step one: confirm the party names exactly match the contract

- Step two: confirm the endorsement form is attached, not merely referenced

- Step three: check whether the form covers ongoing operations, completed operations, or only one

- Step four: confirm any blanket wording still ties back to a written contract requirement

- Step five: save the endorsement with the job file, not just the COI

This takes a little more office discipline. It also avoids the ugly version of the claim where everyone thought the paperwork was fine until coverage counsel starts reading the forms.

The Real Costs and Risk Management Benefits

Contractors usually ask two questions once they understand the endorsement. What does it cost, and is it worth it?

What the endorsement can cost

There is a direct out-of-pocket cost. Verified data shows that additional insured endorsements in construction and specialty contracts typically cost contractors between $82 and $142 for agents or brokers to issue, while some insurers charge $25 to $150 per endorsement annually, according to this breakdown of named insured versus additional insured costs and fee ranges.

That fee isn't the whole picture. The named insured carries the financial burden. The added party doesn't pay premium for the protection it receives, and broader risk on the policy can affect premium and claims history over time. For contractors running multiple jobs with multiple upstream parties, these small administrative charges can pile up.

Why good contractors still buy it

Even with that cost, serious contractors treat the endorsement as part of doing business on larger or better-run jobs. It helps the contractor qualify for project work that won't move forward without formal risk transfer. It protects the relationship with the GC because the insurance structure matches the subcontract. And it can keep a single claim from landing entirely on the wrong balance sheet.

For electricians, plumbers, and roofers, this is similar to tightening warranty language before handing over a job. The contractor wants scope and responsibility defined before a dispute starts. Shops that need a plain-language framework for service promises can also look at how to create your own warranty policy. The principle is the same. Clear documents reduce avoidable fights.

Some contractors also need more ceiling above the liability policy when project size grows. In those cases, commercial umbrella insurance may matter as much as the AI wording itself.

The wrong approach is treating the endorsement as a nuisance fee. The better approach is treating it like bid compliance, contract hygiene, and loss control bundled into one line item.

Conclusion Protect Your Business and Win More Work

An additional insured endorsement isn't just another insurance form in a project folder. It's a contract tool that can help a contractor win the job, protect the GC relationship, and direct claims to the right policy when the loss comes out of the contractor's work. The key points are straightforward. The endorsement form matters. Ongoing and completed operations aren't the same. And a certificate alone doesn't prove the coverage the contract requires.

Contractors who also manage equipment movement and site logistics know that paperwork and operations go together. The same discipline that applies when choosing equipment hauling trailers should apply to insurance documents. The right setup prevents expensive problems later.

If current contracts require additional insured status, completed operations wording, or tighter COI compliance, get a free quote or coverage review from Coverage Axis. A licensed advisor can review the subcontract requirements, check whether the policy forms match the job, and help build coverage that fits the trade, crew, and project type.