A lot of contractors hit the same wall at the same time. The crew is solid, the trade work is clean, the next job is bigger, and then the bid package asks for a bond. Suddenly the question isn't whether the company can build it. The question is whether the company can prove it on paper.

That's where bond insurance for small business changes from an afterthought into a growth tool. For a roofer chasing a school re-roof, an electrician trying to get on municipal work, or a GC stepping into public projects, bonding decides which doors open and which stay shut. A company can be fully insured and still lose the job because the owner wants a bid bond, a performance bond, or a payment bond.

Small contractors often treat bonding like a filing task. The smarter move is to treat it like prequalification. The contractor who understands bonding usually gets to compete for better jobs sooner, with fewer surprises at award time.

Table of Contents

- Why Bonding Stops Good Contractors from Winning Great Jobs

- Surety Bonds vs Insurance What Contractors Must Know

- The Four Key Bond Types for Contractors

- When Are Bonds Required for Your Trade

- How Bond Underwriting Works and What It Costs

- A Step-by-Step Guide to Getting Bonded

- How to Improve Your Bonding Capacity

Why Bonding Stops Good Contractors from Winning Great Jobs

A roofer prices a school re-roof right. An electrician has the crew for a municipal service upgrade. A small GC can handle the site work, concrete, and closeout on a park renovation. The job fits. The bid package does not, because it calls for a bid bond, then performance and payment bonds if awarded.

That requirement knocks good contractors out of contention every week. The problem usually is not field ability. It is timing, financial presentation, and the fact that bonding capacity was never built before the bigger opportunity showed up. By the time the estimator sees the bond form in the instructions to bidders, the clock is already running.

On larger public and commercial work, bonding is often the owner's filter for risk. Owners use it to screen for contractors who can finish the work, pay subs and suppliers, and carry a project when there is pressure on schedule or cash flow. In plain terms, bonding is not just a compliance item. It is a ticket into better work.

That matters most at the step-up point.

A residential electrician can run profitable tenant build-outs for years and still hit a wall on the first city library job. A roofer who has no trouble replacing shingles on private multifamily properties can lose a hospital reroof before bid day because the surety will not support the contract size. A GC may have a strong superintendent and reliable subs, but without bond support, that company stays stuck bidding smaller private jobs while better-margin public work goes to firms that prepared earlier.

Where contractors lose ground

- They wait until the bid is due: That leaves no room to clean up financials, explain job history, or answer underwriting questions.

- They assume insurance solves it: General liability, workers comp, and auto matter, but they do not satisfy a contract bond requirement.

- They chase a larger job before building capacity: A surety wants to see a work program that makes sense, not a sudden jump from small remodels to a large public project.

- They treat bonding as occasional paperwork: Owners and prime contractors often read bond support as a sign of whether a firm is ready for bigger responsibility.

Good production in the field helps, but it does not speak for itself. The file has to show that the company can manage money, manpower, and project size at the same time.

Contractors who understand that point use bonding as a growth tool. They get bond-ready before the right job hits the board. They build a relationship with a surety program that can grow with them. They also know what owners mean when they ask for a bonded contractor, and this plain-English guide on what bonded means for a job gives a useful baseline.

The practical trade-off is simple. Getting bond-ready takes work up front. Better financial records, better job schedules, better communication with your agent or broker. But that work gives a small contractor access to larger jobs, stronger clients, and a path out of the low-bid scramble on small private work.

Surety Bonds vs Insurance What Contractors Must Know

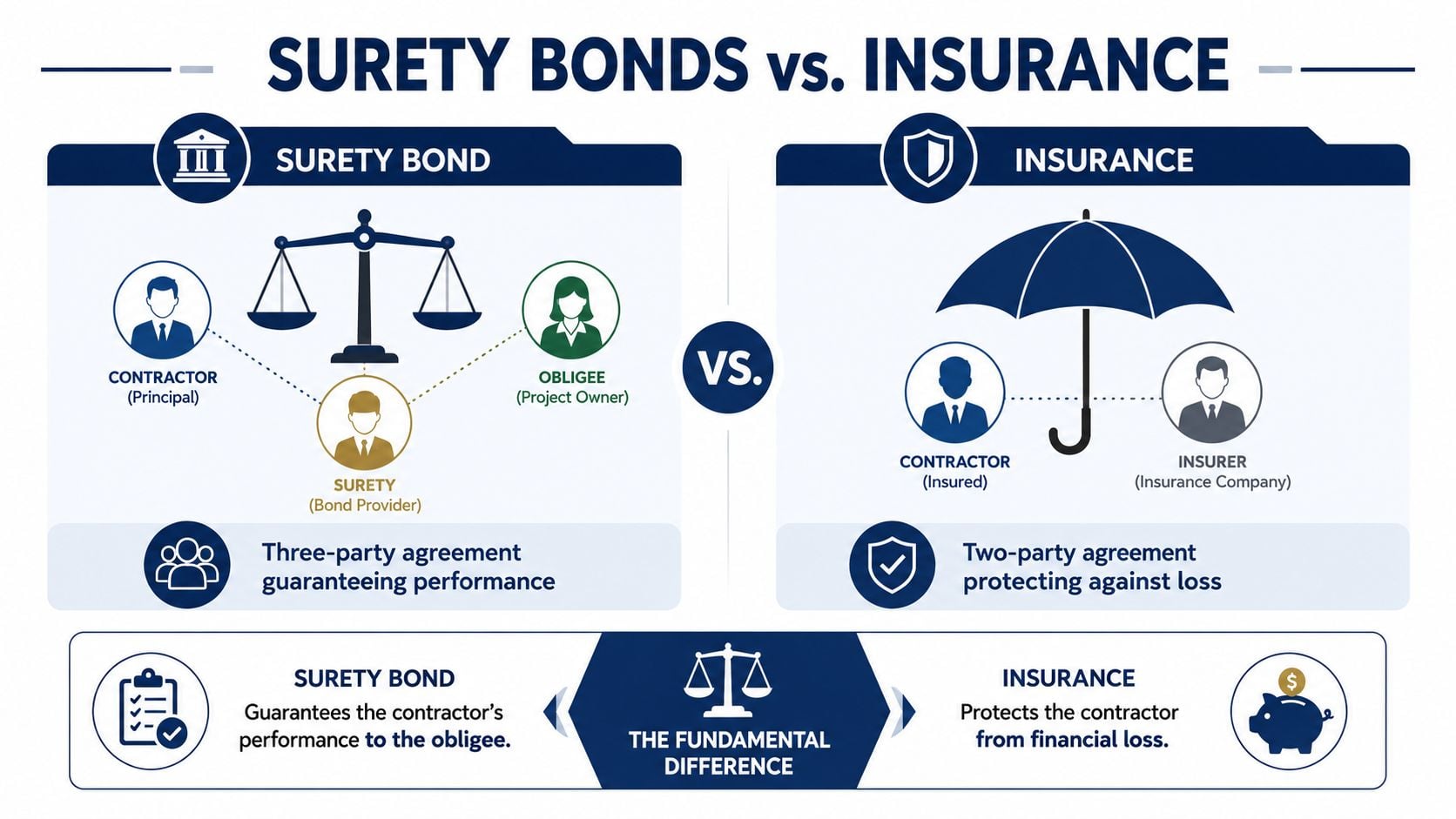

The biggest misunderstanding is simple. A surety bond isn't the same thing as insurance.

Insurance protects the policyholder against covered loss. A surety bond protects the project owner or licensing authority if the contractor fails to meet an obligation. That difference changes everything about how the product works and how it gets underwritten.

The three parties on a surety bond

A surety bond is a three-party credit instrument involving the principal (the contractor), the obligee (the owner or licensing authority), and the surety. If the contractor fails to meet contract terms, the obligee can be compensated, and the surety can seek reimbursement from the principal, which is why underwriting focuses heavily on credit, capacity, and character, as explained in this overview of how surety bonds differ from insurance.

A simple job-site analogy helps. Insurance acts more like a protective shield around the business. A surety bond acts more like a financially strong co-signer standing behind the contractor's promise to perform.

Why that distinction matters on real jobs

Take a roofing contractor on a commercial reroof. If a wind event damages stored material, an insurance policy may respond if the loss fits the policy terms. If the roofer fails to complete the project according to contract, a performance bond addresses a different problem entirely. It protects the owner, not the roofer.

That's why a contractor can't approach bond insurance for small business the same way as buying general liability. The surety wants to know whether the company can carry the work, manage crews, handle subs, and finish the contract. Loss history still matters in the broader account, but it isn't the whole story.

Practical rule: If the product protects your customer from your failure to perform, it's operating like a bond, not like standard insurance.

Don't mix up surety bonds and fidelity bonds

Contractors also confuse contract surety with employee dishonesty protection. They're not interchangeable.

- Surety bonds: Used to support licensing or contract obligations.

- Fidelity or business service bonds: Used in theft-related situations involving employees or client property.

- Contract bonds: Common on public work and larger private jobs where owners want performance assurance.

A residential electrician expanding into light commercial work should keep those buckets separate. The company may need liability, auto, workers comp, and a contract bond package for one job. It might also consider employee dishonesty protection for service work. Different exposures. Different purpose.

Contractors sorting out the full insurance side of the equation can compare the usual coverage stack in this guide to insurance contractors need.

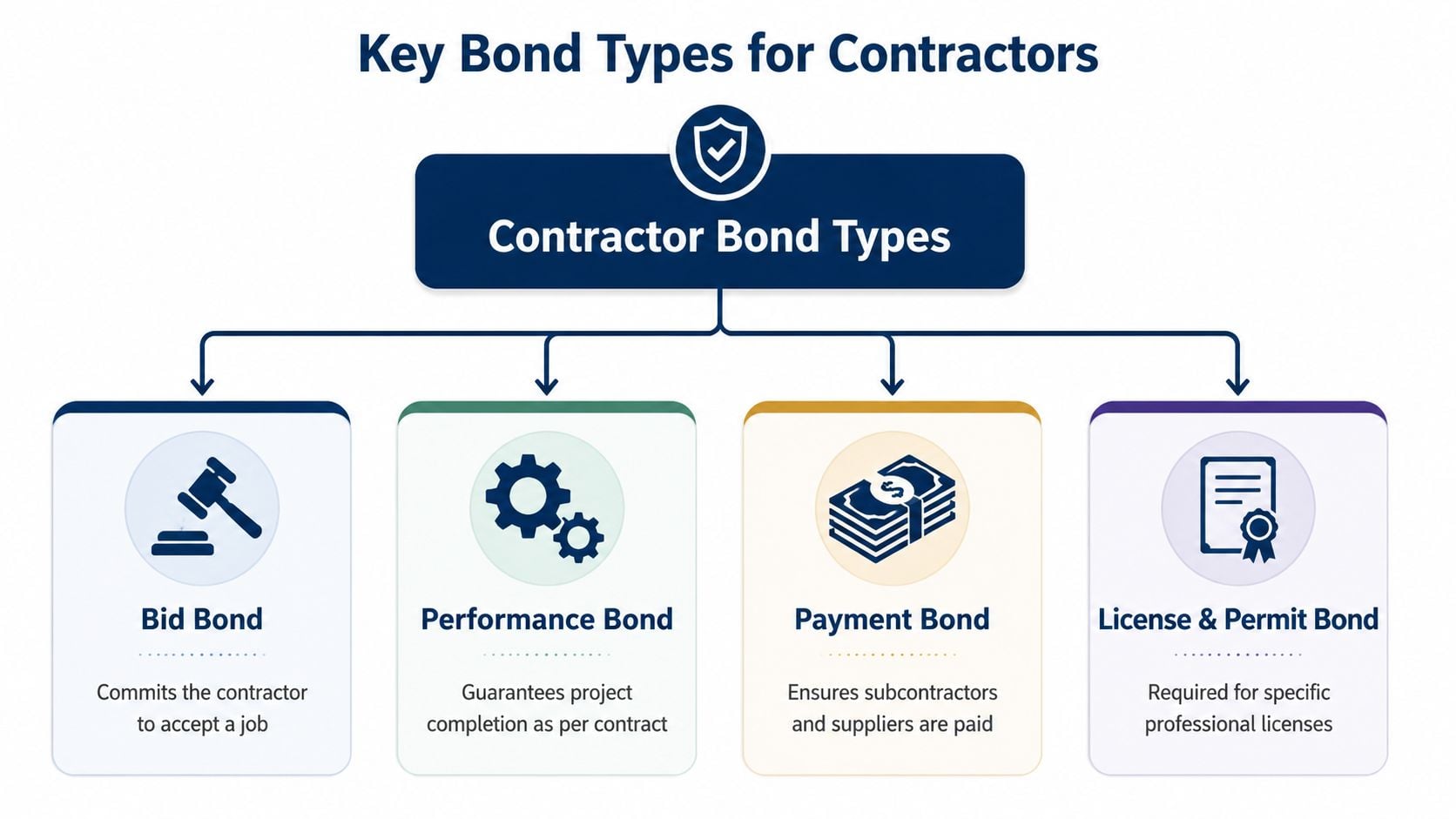

The Four Key Bond Types for Contractors

Most contractors don't need every bond on every job. They need the right bond for the stage they're in, the trade they work in, and the project owner asking for it.

The cleanest way to think about it is this. Some bonds help a company get legally set up. Others help it pursue and secure contract work. The bond requirement can also shift by jurisdiction and by owner. The SBA notes that surety bonds can guarantee bid, performance, payment, and maintenance obligations, while state and local regulators may impose separate requirements, as discussed in this guide to small business bond categories.

License and permit bonds

A license and permit bond usually ties to a legal or regulatory requirement. It's often the bond that lets a contractor operate or pull permits in a given area.

A plumbing contractor is a good example. The company may do clean work and carry proper insurance, but the city or state may still require a license bond before the plumber can legally perform work under that credential. This bond isn't about one single project. It's about compliance with the rules attached to the trade.

A few practical points matter here:

- Check the exact jurisdiction: State, county, and city rules may differ.

- Match the bond form: Some authorities require their own wording and filing process.

- Renew on time: A lapsed bond can create licensing headaches fast.

Bid bonds

A bid bond shows the owner that the contractor is serious. It backs up the proposal by indicating the bidder will accept the contract and provide any required follow-up bonds if awarded the job.

A landscaping contractor bidding on a city athletic field upgrade sees this often. The company submits a price, but the city doesn't want bidders walking away after award because they underpriced labor or material. The bid bond helps screen that out.

Owners use bid bonds to separate real bidders from hopeful bidders.

Performance bonds

A performance bond is the one owners focus on for critical projects. It guarantees the contractor will complete the work according to the contract.

A roofer installing a new roof system on a warehouse is a straightforward trade example. The owner wants assurance that the roof will be installed to spec, not abandoned halfway through or delivered with major contract failure. For contractors stepping into larger jobs, this is often the bond that moves them from “small crew” status into serious contention.

Payment bonds

Payment bonds protect the owner from the fallout of unpaid subs and suppliers. If the GC doesn't pay downstream parties as required, the owner gets protection against that exposure.

This matters most on multi-party jobs. A general contractor building out a retail shell may hire electrical, framing, glazing, and site subs. If those parties don't get paid, the owner may face liens, disputes, and project interruption. The payment bond is there to reduce that risk.

A simple comparison helps:

| Bond type | Common use | Trade example |

|---|---|---|

| License and permit bond | Meets licensing or permit rules | Electrician obtaining or maintaining a trade license |

| Bid bond | Supports a bid submission | Landscaper bidding a city park project |

| Performance bond | Guarantees contract completion | Roofer on a commercial reroof |

| Payment bond | Protects against nonpayment to subs and suppliers | GC managing multiple subcontractors |

Contractors who need help sorting out the difference between two of the most commonly confused forms can review bid bond vs performance bond.

When Are Bonds Required for Your Trade

A lot of contractors find out they need a bond at the worst possible time. The bid is due Friday, the owner wants a bond letter in the package, and the company has never gone through underwriting before.

That happens when the field side outgrows the office side. A roofer may spend years doing residential tear-offs and small commercial repairs with no bond requirement at all. Then a hospital reroof or school project hits the board, and bonding becomes the line between staying in the small-job lane and getting a shot at larger work.

Bond requirements usually come from three places. Public work rules, state or local licensing rules, and private contract terms.

Federal work

Federal construction is one of the clearest triggers. On many federal jobs, performance and payment bonds are part of the contract requirement. For a small GC chasing its first federal renovation, or an electrical subcontractor trying to move from tenant improvements into government work, that means bond readiness has to be in place before the bid goes in.

The practical issue is simple. A contractor can have the crew, equipment, and trade skill to do the work and still miss the job because the surety will not support the bond in time.

That is why bonding is a growth issue, not just a compliance item.

State and local licensing rules

Licensing is the other common trigger, especially for specialty trades. Electricians, plumbers, HVAC contractors, and other licensed firms often need a bond to get licensed, renew a license, pull permits, or work in a specific city.

A contractor who crosses municipal lines sees this fast. An electrician may be properly set up in one county and then learn the next city wants a different bond amount or a different bond form before issuing permits. A license bond, permit bond, and contract bond may sound close in conversation, but they solve different problems and are not interchangeable on paper.

That mistake costs time. On a live job, it can also cost the start date.

Private project owners and lenders

Private work brings its own bond triggers. Owners on larger commercial projects often require bonds because they want protection if the contractor defaults or if subs and suppliers go unpaid. Lenders may also require stronger bonding on financed jobs, especially when the project budget is tight and the schedule leaves little room for replacement contractors.

This shows up on real jobs every week. A GC building a small retail center may not need bonds on one negotiated project, then get asked for performance and payment bonds on the next job because the owner has bank financing. A framing contractor or site contractor stepping onto that project needs to understand those requirements early, because bond terms affect pricing, cash flow, and who can realistically bid the work.

Contractors trying to sort out what applies by license, project type, or public versus private work can review these contractor bonding requirements by trade and job type.

Bonding also connects to working capital. If a contractor is lining up a larger bonded job, it helps to review cash needs, retainage pressure, and pay cycle gaps at the same time. This guide on how to finance your construction project is a useful companion resource.

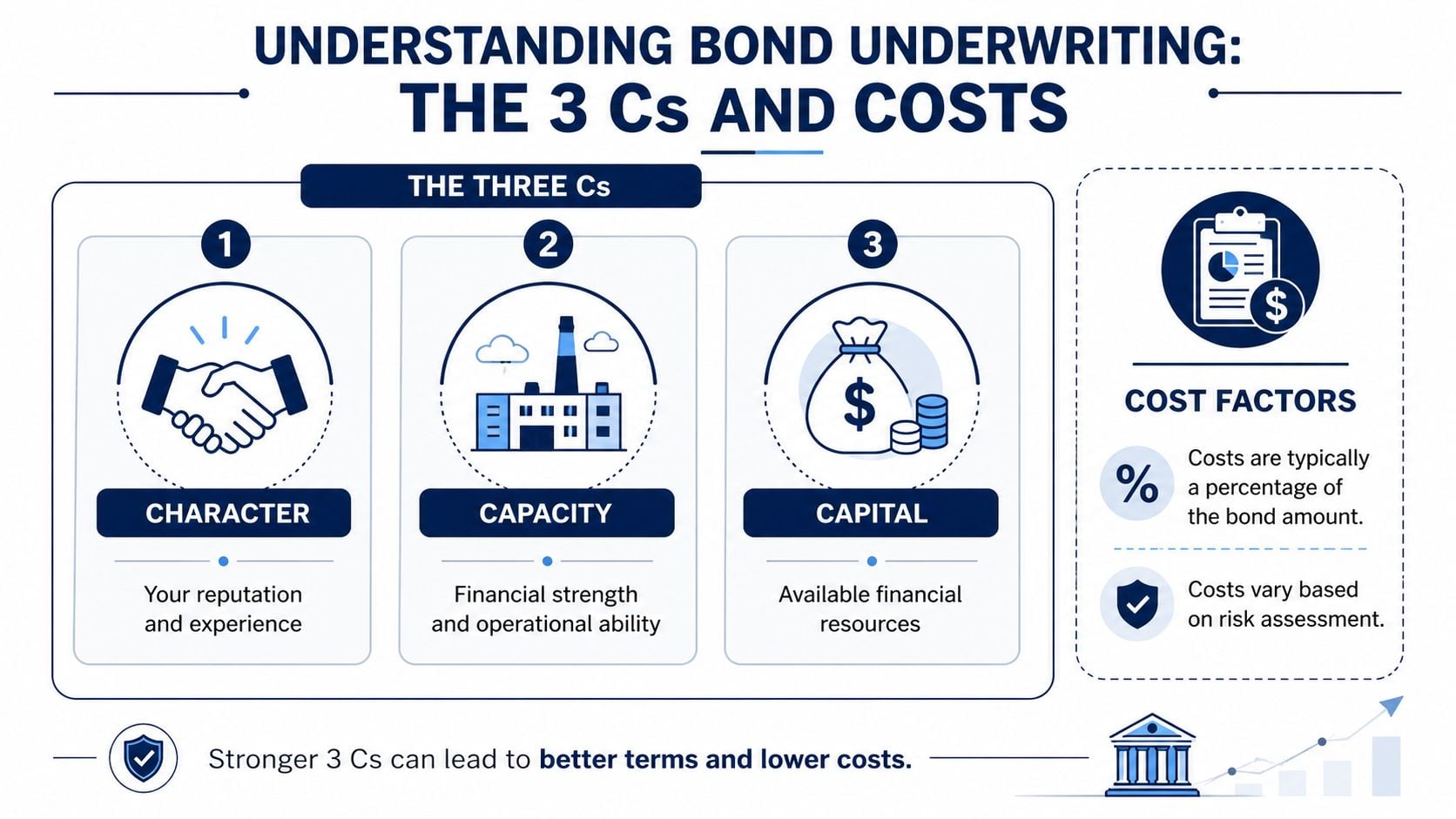

How Bond Underwriting Works and What It Costs

Underwriting is where the surety decides whether the contractor looks dependable enough to back. On the ground, that decision usually comes down to three things. Character, capacity, and capital.

A lot of owners hear those words and think they sound vague. They're not vague once they're tied to a live project.

Character

Character is about trust. Does the contractor have a record of honoring obligations, finishing jobs, handling disputes reasonably, and paying bills on time?

For a small electrical contractor, character shows up in credit quality, owner reputation, and the overall story the file tells. If the application says the company can handle institutional work but the project history only shows small residential service calls, the surety will ask hard questions.

Capacity

Capacity is the company's ability to perform the work being requested. Crew depth matters. Field supervision matters. Equipment matters. So does experience with similar job size and complexity.

A concrete contractor may be excellent at sidewalks and driveways but not yet ready for a larger structural package with schedule pressure and multiple inspections. That doesn't make the company bad. It just means the surety wants to see a sensible progression in project size.

Capital

Capital is the financial side. Working capital, cash position, business financials, and overall balance sheet strength all shape the decision.

Two plumbing contractors can look similar from the outside and still get very different results. One keeps clean books, has better cash discipline, and can show stable finances. The other may do decent field work but runs thin, carries old payables, or mixes personal and business finances. The surety notices.

Clean financial statements don't win the job by themselves, but messy ones can definitely lose it.

What bond costs look like

For small businesses, bond pricing is typically quoted as a percentage of the bond amount. A common range is 1% to 3% for applicants with strong credit, while poor-credit applicants may pay up to 10%. For SBA-backed performance and payment bond guarantees, the guarantee fee is 0.6% of the contract price, according to this breakdown of surety bond pricing for small businesses.

A few practical cost drivers show up again and again:

- Credit strength: Better credit usually opens better pricing.

- Financial quality: Reviewed, organized statements help.

- Job fit: A project that aligns with the contractor's track record is easier to support.

- Business stability: Sureties prefer contractors who don't look stretched thin.

Contractors should also remember that a high bond cost doesn't only hurt profit. It can also hurt bid competitiveness if the company is already operating on a tight margin.

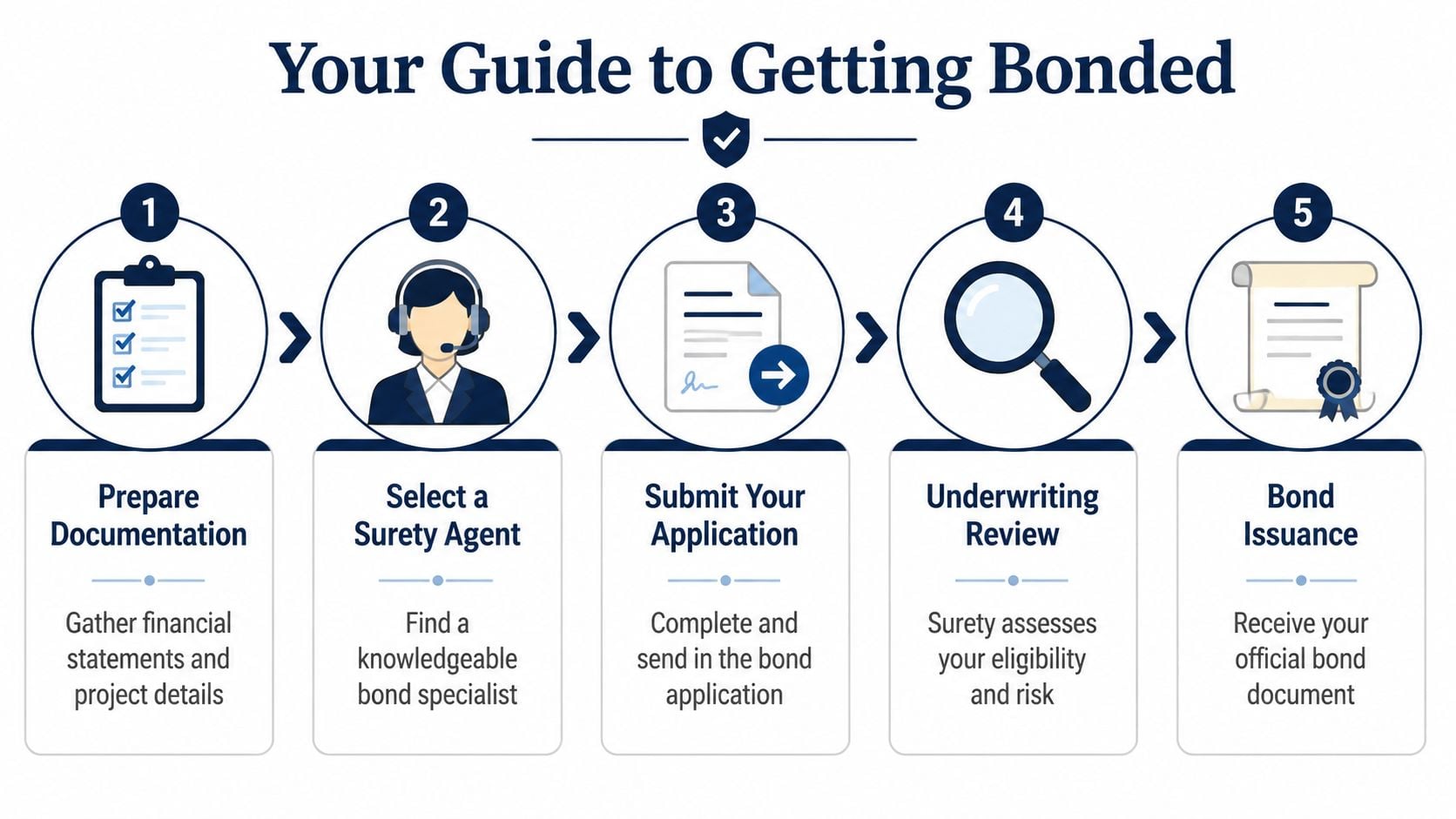

A Step-by-Step Guide to Getting Bonded

Getting bonded feels complicated until the process is broken into pieces. Most delays come from missing information, sloppy financial records, or waiting until the owner needs the bond immediately.

For a first-time contractor, the path usually runs best when it's handled in order.

Get the paperwork together

Start with the documents the surety will want to review. That usually includes business financial statements, owner financial information, company background, and project history. For a GC, a current work-on-hand schedule is often part of the story because it shows what the company is already carrying.

A specialty trade contractor should also gather resumes or summaries for key managers, lists of completed projects, and details on the job that needs the bond. The cleaner the package, the easier it is for an underwriter to follow.

Many contractors lose time here because receipts, job cost backup, and expense records are scattered across trucks, inboxes, and file folders. Better recordkeeping helps the bond file and the broader insurance file. For that side of the operation, Simplified receipt management for contractors can help keep documentation from turning into a scramble.

Work with a bond-focused advisor

Not every insurance conversation is a bonding conversation. A contractor needs someone who understands surety submissions, underwriter expectations, and what to present upfront versus what to clean up first.

That matters a lot for a roofer or electrician chasing a larger contract for the first time. A well-prepared submission can frame the company as moving up responsibly. A weak one can make the same contractor look unready.

Complete the application carefully

Applications should be complete, consistent, and honest. If the contract amount, business history, and job description don't line up, the surety will dig deeper.

Three habits help:

- Answer directly: Don't leave obvious blanks.

- Match supporting documents: Revenue, project size, and ownership details should agree across the file.

- Flag unusual items early: Prior disputes, older credit issues, or rapid growth are easier to explain upfront than after an underwriter discovers them.

Expect questions before approval

Underwriting often comes back with follow-up questions. That's normal. A surety may ask about backlog, subcontractor controls, banking relationships, or prior jobs similar to the one being proposed.

An HVAC contractor stepping from residential replacement into school work should expect that. The surety isn't trying to make the process harder. It's trying to see whether the company can carry the jump without creating project trouble.

The fastest bonding process usually belongs to the contractor whose documents already make sense before the first underwriter review.

Contractors who want a fuller overview of the process can review how to get bonded and insured.

How to Improve Your Bonding Capacity

Bonding capacity isn't just a surety term. It's a business health test.

Project owners use bonds because they want confidence in delivery, and there's a real financial reason for that. A 2023 analysis from the Surety & Fidelity Association of America found that on a representative $35 million bonded project, net savings from bonding were about $140,000 (0.4%) even with no default, and about $8.0 million (23%) if the project defaulted, as shown in this report on the project savings value of surety bonding.

That's why improving bondability is worth the effort. It isn't about satisfying paperwork for its own sake. It's about becoming the kind of contractor owners trust with larger obligations.

What actually helps

- Keep credit clean: Personal and business credit still matter because the surety is backing the contractor's promise.

- Tighten financial reporting: A construction-focused CPA can make the financial story clearer and more credible.

- Build in steps: A mason who completes smaller bonded jobs successfully has a stronger case for larger work later.

- Separate business from personal spending: Mixed accounts create confusion and weaken the file.

- Develop banking relationships: A supportive bank relationship helps show stability.

- Track job performance: Clean closeouts, margin discipline, and orderly records all strengthen future submissions.

What usually doesn't work

Some contractors try to solve a bonding problem at the last minute with explanations instead of preparation. That rarely lands well. Sureties prefer a company that grew in a controlled way over one that appears to be jumping several job sizes at once with thin support behind it.

A better approach is steady progression. A trade business that improves books, controls receivables, documents successful projects, and manages growth usually becomes more bondable over time. That same discipline tends to improve the rest of the insurance account too.

If a contractor is trying to qualify for bigger jobs, clean up a bond submission, or review whether the current insurance and bonding setup fits the work being pursued, Coverage Axis offers free quotes and coverage reviews built for contractors and trade businesses.