A lot of electrical contractors hit the same wall at the same point. The estimate is done, the scope looks solid, and the job is worth chasing. Then the contract package shows up with insurance language that can stall the whole thing: additional insured, waiver of subrogation, primary and noncontributory, completed operations, certificate deadlines.

That's usually the moment electrician business insurance stops feeling like a back-office task and starts looking like part of operations. A contractor wiring tenant improvements, troubleshooting service calls, or taking on design-build work isn't just buying policies. That contractor is buying the ability to sign contracts, move onto jobsites, protect cash flow, and keep one claim from turning a profitable quarter into a bad year.

Electrical work creates real exposure. A dropped tool can damage finished floors. A misrouted cord can trip a building manager during a walkthrough. A service van can get rear-ended on the way to a panel replacement. A laptop stolen from a truck can expose customer records and access information. Insurance has to match that reality, not some generic small-business template.

When policy language gets dense, it helps to slow down and read it the same way a contractor reads plans and specifications. For The Public Adjusters' advice on policies is a useful plain-English reference for understanding how insurance wording works before a claim forces the issue.

Table of Contents

- Why Your Electrician Insurance Is More Than Just Paperwork

- The Core Policies Every Electrical Contractor Must Have

- Insuring Your Van Tools and Shop

- Advanced Coverage for Large Jobs and Design Work

- What Drives Your Insurance Premiums and Common Pitfalls

- Managing Subcontractors and Certificates of Insurance

- How to Get the Right Coverage and Compare Quotes

Why Your Electrician Insurance Is More Than Just Paperwork

A commercial fit-out is ready to award. Your price works, your crew is available, and the GC wants to move. Then the contract lands in your inbox: $2 million general liability, additional insured wording, waiver of subrogation, primary and noncontributory language, and proof of completed operations. At that point, the question is no longer whether you can wire the job. It is whether your insurance program is set up well enough to let you start.

That is why electrician business insurance matters on the operations side of the business, not just the compliance side. It helps determine which jobs you can bid, how fast you can turn around paperwork, and whether one claim turns into a temporary headache or a hit to cash flow that wrecks the month.

Insurance affects which jobs you can actually take

A one-van service contractor and a shop chasing ground-up commercial work do not need the same insurance structure. Service work usually brings frequent small exposures. A tech in an occupied home, a ladder in a finished foyer, a shutoff mistake that spoils food in a restaurant cooler. New construction brings a different set of contract demands, higher limits, and tighter certificate requirements. Design-build adds another layer because advice, layouts, load calculations, and recommendations can create professional liability exposure even when no one uses the words "engineering services."

That difference gets missed all the time.

Plenty of contractors buy insurance to keep the license active and satisfy the bare minimum. That can work for a while. It usually stops working when the business moves into schools, tenant improvements, municipal work, medical offices, or negotiated commercial jobs where upstream contracts push risk down to every trade.

If you want better jobs, insurance has to match the work you are pursuing. A basic policy set up for residential service calls can leave gaps on a design-assist project or fail a contract review before the first conduit is run. Contractors who understand general liability insurance for contractors usually make better bidding decisions because they know which jobs fit their current program and which ones require changes before signing.

The right program protects margin and keeps decisions clear

Coverage should be sized to the way the business operates. Buying every endorsement available is one way to waste money. Buying the cheapest certificate-friendly policy is another way to lose money later.

A live remodel makes the trade-off obvious. Your mechanic sets temporary power in an occupied suite. A tenant trips on protection laid across a walkway and files an injury claim. On another job, your foreman recommends a panel configuration for a fast-turn retail build-out, the owner relies on it, and the setup later has to be reworked because the design recommendation did not fit the project conditions. One claim points to general liability. The other may point to professional liability or E&O, which many electricians never add because they assume they only "install." If your shop gives design input, troubleshooting recommendations, load advice, or system layout guidance, that assumption gets expensive.

Policy language matters too. So do exclusions, sublimits, and who is listed where. Contractors who review forms closely, or use outside guidance like For The Public Adjusters' advice on policies, are usually better at spotting the difference between a policy that only looks acceptable on a certificate and one that can hold up when a claim or contract dispute shows up.

The point is simple. Insurance is part of job costing, contract strategy, and risk control. Electricians who treat it that way tend to keep more options open and make fewer expensive mistakes.

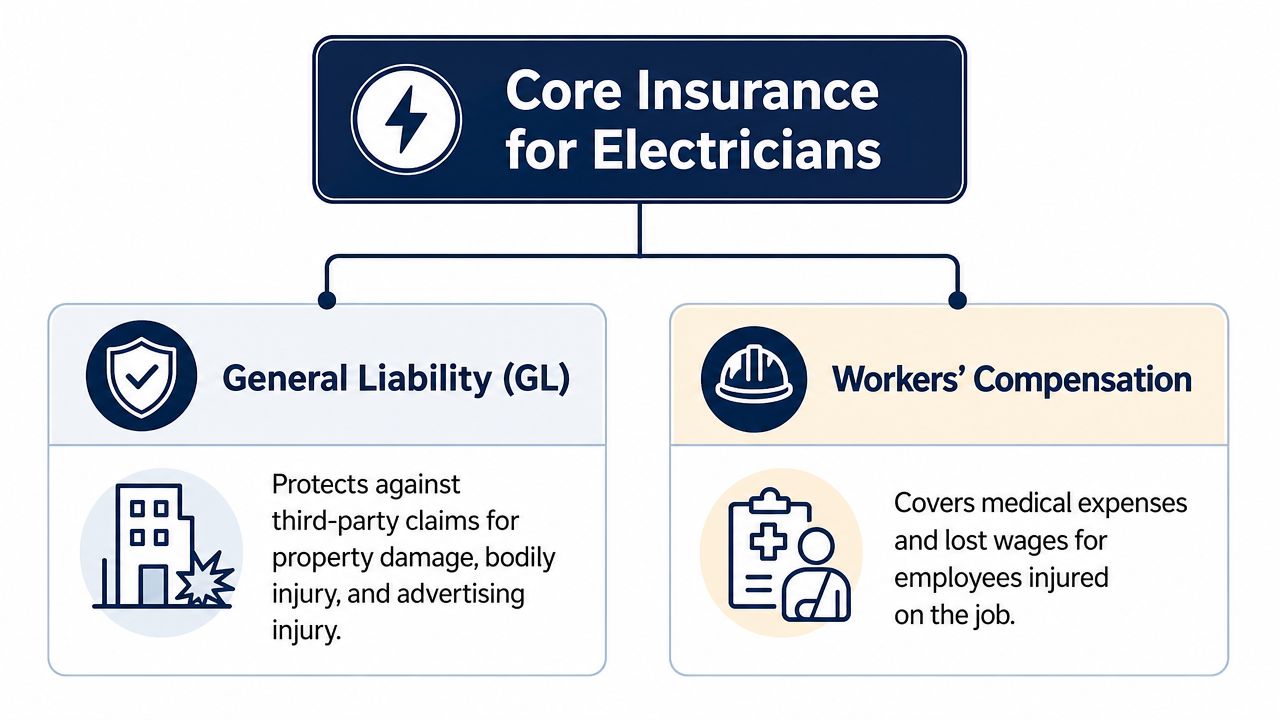

The Core Policies Every Electrical Contractor Must Have

Every electrical business has different exposures, but two coverages are hard to call optional. General liability protects the business from third-party claims. Workers compensation protects the crew when someone gets hurt doing the work.

Those two policies do different jobs. Mixing them up causes bad buying decisions.

General liability is the shield

Think of general liability as the shield around the business. It's there when someone outside the company says the electrician caused bodily injury or property damage.

On an electrical job, that can mean a homeowner trips over a cord during a service upgrade. It can mean a ladder leg cracks tile in a finished foyer. It can mean a panel swap leads to accidental drywall damage in a retail suite. The claim comes from a third party, and the policy is built to address that kind of allegation.

For electricians, general liability is usually the anchor policy because it protects against third-party bodily injury and property damage claims tied to live-wire work. Recent pricing data shows it averages $57 per month or $684 per year in the U.S., while a business owner's policy averages $78 per month and workers' compensation averages $217 per month, according to TechInsurance's electrician insurance cost data.

Contractors who need a plain-English breakdown of this policy can review general liability insurance for contractors.

Workers compensation is the crew safety net

Workers compensation does a different job. It responds when an employee gets hurt on the job. For electrical contractors, that can mean a ladder fall, a hand injury while pulling cable, or an electrical shock while troubleshooting energized equipment.

This is the policy that keeps a crew injury from becoming a direct payroll and medical crisis for the business. It also matters because workers compensation is required in most states when employees are on payroll. A lot of contractors first learn that after they hire helpers and a client asks for proof before site access.

A contractor can survive a lot of small headaches. An uninsured worker injury isn't a small headache.

There's also an operational point here. If a contractor has employees but delays proper workers compensation setup, that problem tends to show up at the worst time, such as during a claim, an audit, or a contract review. It's cheaper to structure it correctly at the start than to fix it after someone gets hurt.

Where the baseline cost starts

The numbers above are useful because they show how quickly a real electrical program becomes a package, not a single line item. A contractor may start by focusing on general liability, but the actual business often needs liability, payroll-driven injury coverage, and then asset protection layered on top.

A one-person residential service electrician has a different risk profile than a multi-crew contractor doing tenant improvements and fleet-based work. But both still need to understand the foundation first. General liability protects the business from claims brought by others. Workers compensation protects employees hurt while doing the work. If those two policies are weak or missing, everything else sits on a shaky base.

Insuring Your Van Tools and Shop

Electrical contractors don't just sell labor. They rely on rolling assets, mobile equipment, stock, and storage. That changes the insurance conversation fast.

A van loaded with ladders, benders, testers, power tools, wire, fittings, and tablets isn't just transportation. It's a mobile work platform. If it's out of service after a crash or theft, jobs can stall before the first task starts.

The van needs business coverage

A personal auto policy usually isn't built for a vehicle used to run service calls, haul materials, or move crews and tools between jobs. If the vehicle is part of business operations, the safer approach is commercial auto.

The practical scenario is easy to see. An electrician is headed to a panel change with conduit and gear in the van, rear-ends another vehicle, and the other driver alleges injury. That's a business-use accident, and the contractor needs coverage written for business use, drivers, and vehicles tied to the company.

For contractors comparing options, commercial auto liability insurance gives a clear overview of what this policy is designed to handle.

Tools move so the coverage has to move too

Tools and equipment coverage matters because electricians rarely keep all critical gear in one fixed place. Meters move from van to jobsite. Thermal imaging equipment gets carried into occupied buildings. Portable threaders, cordless kits, and specialty testers can be stolen from a truck, damaged in transit, or disappear from a partially secured site.

That's why a contractor needs to think beyond “property at the office.” Mobile tools need mobile protection. A policy that only contemplates property inside a fixed building won't line up with how most electrical contractors work.

If a stolen meter, damaged bender, or missing cable locator stops tomorrow's jobs, that's an insurance problem and an operations problem at the same time.

The shop and stored materials need their own protection

Some electrical businesses also have a shop, storage yard, or leased unit where breakers, wire, fittings, reels, and backup tools stay between jobs. That creates a different exposure from tools in transit. Fire, water damage, theft, and vandalism can hit the business where it stores the inventory that keeps jobs moving.

A contractor with a modest service setup may need only limited property protection. A contractor with a stocked shop, office contents, and stored materials has a larger property exposure and should treat it that way.

Technical pricing for electrician business insurance is highly exposure-driven. Premiums scale with payroll, receipts, voltage, fleet size, and liability limits, not just headcount. One industry guide notes service-only electrical shops may pay roughly $1,000 to $3,000 per year for general liability, while adding commercial auto, inland marine, workers' comp, and umbrella can push total annual spend into the $5,000 to $15,000+ range, according to NIP Group's guide for electrical contractor insurance.

That spread is why electricians should match coverage to operations instead of buying whatever package looks cheapest. A contractor with one van and light hand tools doesn't need the same structure as a company with multiple vehicles, stocked storage, and crews spread across jobsites. The right move is to insure the things that keep work moving: the vehicle, the mobile tools, and the place where the business stores its working assets.

Advanced Coverage for Large Jobs and Design Work

As electrical contractors grow, the exposures change. The company may start bidding larger commercial work, taking on design-build responsibilities, or signing contracts that demand more than the basics. That's where umbrella, professional liability, and bonding start to matter.

A contractor doing straightforward service replacements may not need the same structure as a contractor laying out power distribution for a build-out or advising on system design. The insurance program has to follow the work, not the company's old habits.

Umbrella coverage matters when one loss can punch through base limits

Commercial umbrella insurance adds an extra layer above underlying liability policies. It becomes relevant when a contractor looks at a serious accident and realizes the base policy may not be enough.

Consider a van accident involving injuries, or a jobsite incident that triggers a large third-party claim. The contractor doesn't buy umbrella because losses are expected every day. The contractor buys it because one unusually severe claim can be financially disruptive in a way that standard limits may not absorb comfortably.

Umbrella also shows up in contract requirements. Larger owners, GCs, and institutional clients often expect higher total liability capacity than a small service contractor carries by default.

E and O matters when the electrician gives advice not just labor

This is the most commonly missed gap for growing electrical firms. Professional liability, often called errors and omissions, is for the contractor who does more than install according to a clean set of plans.

A frequently underexplained issue is that electricians who design, specify, or consult can face claims based on financial loss even when nobody is physically injured and no property is damaged. Mainstream coverage discussions often focus on general liability, workers' comp, commercial auto, tools, and BOPs, but they rarely explain that a wrong load calculation, code interpretation, panel schedule, or design recommendation can create this kind of claim, as explained in Levelset's discussion of electrical contractors insurance.

That matters in the field. An electrical contractor may recommend EV charging layout, advise on service capacity, coordinate lighting controls, or create a panel schedule for a tenant build-out. If that advice is wrong and the client suffers delay, rework, or other financial harm, general liability may not be the policy meant to answer that type of allegation.

An electrician who only installs to plan has one risk profile. An electrician who advises, designs, or specifies has another.

A useful rule is simple. If the contractor's judgment is part of what the client is buying, E&O deserves a serious review.

Bonds help qualify for work

Surety bonds are often lumped into the insurance conversation, but they serve a different purpose. They function as a guarantee tied to contract performance, licensing, or project obligations.

For many public jobs and some larger private projects, bonding isn't optional. No bond, no bid. That makes bonding part of growth planning, not just paperwork after award.

Contractors moving into that market can review bond insurance for small business for a practical explanation of how bonds fit project qualification. The important point is that a growing electrical contractor often needs all three layers working together: liability capacity for bigger claims, E&O for advisory exposure, and bonding for project access.

What Drives Your Insurance Premiums and Common Pitfalls

Two electricians can look similar from the outside and still get priced very differently. One runs a single service van and handles residential troubleshooting. Another has multiple crews, does commercial tenant improvements, and works on higher-voltage systems. The difference in premium usually comes from exposure, not from a carrier being arbitrary.

One industry pricing study reported a national average of $379 per month for a standard $1 million per occurrence / $2 million aggregate general liability policy for electrical contractors, with state pricing ranging from $230 per month in West Virginia to $671 per month in California, a 191% spread between the lowest and highest markets, according to MoneyGeek's electrical contractor insurance cost analysis.

Why one electrician pays more than another

Several operational factors tend to move pricing up or down:

- Payroll and receipts: More payroll and more revenue usually mean more exposure. More work means more chances for injury, property damage, driving losses, and contract disputes.

- Type of work performed: Service calls, tract residential, tenant improvements, industrial work, and design-build work don't present the same hazards.

- Fleet size and driving activity: More vehicles and more miles create more chances for claims.

- Limits requested: Higher liability limits and added umbrella capacity cost more, but they may be necessary for the work pursued.

- Claims history: A contractor with prior losses is a different underwriting profile than one with a cleaner record.

A shop owner looking at premium only through the lens of headcount usually misses the bigger picture. Exposure follows operations. If the company adds apprentices, more vans, more design responsibility, or more demanding contracts, pricing tends to reflect that.

Typical Insurance Limits for Electrical Contractors by Job Type

| Job Type | General Liability (Per Occurrence/Aggregate) | Commercial Umbrella | Common Risks |

|---|---|---|---|

| Residential service | Standard limits often satisfy smaller homeowner-facing work | Often not required, but may be considered based on exposure | Slip hazards, incidental property damage, vehicle accidents |

| Commercial tenant improvement | Contracts often call for stronger baseline liability limits | Common on larger or more demanding projects | Damage to finished interiors, third-party injury, subcontractor issues |

| Design-build or advisory-heavy electrical work | Liability limits still matter, but professional exposure also needs review | Often considered where contract size or client requirements increase | Design recommendations, layout errors, financial-loss allegations |

| Public or institutional work | Limits are often tied to bid and contract requirements | More common when owners require higher total liability capacity | Strict contract compliance, jobsite injury allegations, larger claim severity |

A separate cost issue is tax treatment. Insurance premiums are part of the operating picture, so contractors reviewing overhead with an accountant may also want guidance on how to maximize business tax savings while keeping records clean.

Common gaps that cause trouble

A cheap quote can still be expensive if it leaves out the exposures the contractor has.

Watch for issues like these:

- Work-class mismatch: A policy written for lighter operations can create trouble if the company performs broader or higher-hazard electrical work.

- Faulty workmanship confusion: Many contractors assume the policy pays to redo bad work. Often, the primary concern is whether resulting damage is covered while the cost to replace the contractor's own work is treated differently.

- Residential or commercial mismatch: A contractor who shifts between project types needs the policy to reflect that reality.

- Contract endorsements missing: If the contract requires additional insured status, waiver of subrogation, or completed operations wording, the base policy alone may not solve the problem.

Contractors trying to understand pricing logic in more detail can review electrical contractor insurance cost. The better question isn't just “How much is the premium?” It's “What exactly is being insured, and what isn't?”

Managing Subcontractors and Certificates of Insurance

Your helper sub lands a ladder on a finished floor, opens a panel, and a wiring mistake knocks out power to a tenant space. The property manager calls you, not the sub. That is how subcontractor risk usually works in electrical contracting. The hiring contractor gets pulled into the claim first, then sorts out whose insurance should respond.

That is why subcontractor control is an operations issue, not just an admin task. If you use subs for service overflow, trenching, low-voltage cabling, or portions of a larger commercial build, the insurance side needs to be checked before anyone shows up on site. A verbal “we're covered” does nothing when there is a loss.

A simple subcontractor control process

The best process is usually boring and consistent.

- Get the COI before mobilization. If the sub is already on site, you have lost your advantage.

- Match the certificate to the subcontract. Required limits, additional insured wording, waiver of subrogation, and completed operations terms should line up with the agreement.

- Verify the scope fits the work. A subcontractor insured for low-hazard handyman work is a bad fit if they are doing energized troubleshooting, service upgrades, or commercial rough-in.

- Track renewals until the job is done. A policy that expires mid-project can leave a gap right when a claim happens.

This matters even more on larger jobs. General contractors and project owners often require you to carry the paper correctly downstream. If your subcontractor setup is loose, you can meet your own insurance requirements and still create a claim problem for your company.

What to review on every COI

A certificate is only a snapshot. Read it like someone who may have to defend the file later.

Focus on these items:

- Named insured: Confirm it matches the legal business name on the subcontract, not a trade name or related company.

- Policy dates: The coverage period should include the actual dates the subcontractor will be working.

- Coverage shown: General liability is standard. Workers compensation and commercial auto may matter too, depending on the work and who is bringing vehicles to the site.

- Limits listed: Check that the numbers satisfy the contract. Do not assume “insured” means “insured at the level your project requires.”

- Description of operations or notes: If the certificate language looks generic or unrelated to the job, ask questions.

- Endorsements: The COI may reference additional insured status, but the endorsement is what matters if a dispute comes up.

For design-build or design-assist electrical work, review subcontractor insurance even more carefully. If a lighting controls consultant, fire alarm designer, or engineering sub gives advice that leads to rework or a system performance problem, general liability may not address the full loss. That is where professional liability can become part of the subcontractor review. Many contractors miss this because the certificate looks fine at a glance.

One practical rule helps here. If the subcontractor is only supplying labor, the review is usually centered on bodily injury, property damage, and workers compensation. If the subcontractor is making layout decisions, calculations, drawings, programming decisions, or system recommendations, review whether professional liability should also be part of the requirement.

Contractors who want a practical reference can review this certificate of insurance template for contractors. It helps to know what a proper COI should contain before relying on one.

How to Get the Right Coverage and Compare Quotes

The fastest way to get a bad insurance program is to shop only by price and rush through the application details. Electrician business insurance works best when the quote reflects the actual operation. If the business performs service calls, tenant improvements, design-assist work, or multi-vehicle operations, the submission needs to say so clearly.

Good quoting starts with clean information. If the contractor understates payroll, leaves out a vehicle, forgets to mention subcontracted labor, or glosses over design-related services, the quote may look attractive up front and become a problem later.

What to gather before asking for quotes

A contractor usually gets a better result when these details are organized in advance:

- Business operations summary: Describe the actual work. Residential service, commercial build-outs, industrial troubleshooting, low-voltage work, design-assist, and EV charging aren't the same thing.

- Payroll and revenue estimates: These affect several lines of coverage.

- Vehicle list: Include who drives what and how the vehicles are used.

- Tool and equipment overview: Especially important when gear regularly moves between vans and jobsites.

- Contract requirements: If clients ask for specific endorsements or limits, that should shape the quote request from the start.

How to compare more than price

A lower premium doesn't always mean better value. Two quotes can look similar until the contractor checks the details that control claim response and job qualification.

Compare these items line by line:

- Coverage limits: Are the liability limits enough for the jobs being pursued?

- Deductibles: A lower premium paired with a painful deductible may not help cash flow.

- Exclusions: Exclusions can hide gaps.

- Endorsements: Additional insured, waiver of subrogation, and related wording matter for contract compliance.

- Fit with operations: The policy should reflect the work performed, not a cleaner version of the business on paper.

Why cyber now belongs in the conversation

Many electricians still think cyber coverage is only for tech companies. That view is outdated.

The FBI's IC3 recorded 859,532 cybercrime complaints in 2024, with reported losses above $16 billion, showing that cyber incidents remain a large business risk. For electricians, if a laptop with customer addresses and billing data is stolen from a truck, cyber insurance is what covers the fallout, according to biBERK's article on electrician insurance policies.

That matters because many electrical contractors now store schedules, invoices, payment records, property access details, and customer contact data on phones, tablets, and laptops used in the field. A standard package may not address the downstream fallout from that kind of loss.

The smartest way to compare quotes is to treat the process like estimating a job. Check scope. Check assumptions. Check what's included, what's excluded, and what has to happen after award. Contractors who want a faster path can start with Coverage Axis, where licensed advisors shop 50+ A-rated carriers and build right-sized programs for trade and specialty contractors based on crew size, project type, and operational risk.

Need a clearer read on electrician business insurance before the next bid goes out? Contact Coverage Axis for a free quote or coverage review. A licensed advisor can help compare current policies, spot gaps, and build a program that fits the work instead of forcing the business into a generic package.