A roofing contractor often feels the insurance problem before any claim happens. A general contractor sends over a subcontract agreement. The job looks good. The margins work. Then the paperwork shows up and stalls everything. The roofer needs higher limits, additional insured status, and proof that the policy fits roofing operations instead of a generic contractor form.

That's the moment when general liability insurance for roofers stops being abstract. It becomes the difference between getting on the roof or getting screened out before work starts. It also becomes painfully real when a shingle bundle slides off a steep pitch and crushes a customer's car, or when a property owner calls back months later because water is showing up around a vent penetration and the finger is pointed at the last roofer on site.

Table of Contents

- Why Your Roofing Insurance Is More Than a Piece of Paper

- What General Liability Actually Covers on the Jobsite

- The Fine Print That Can Make or Break Your Roofing Policy

- What Roofers Should Expect to Pay for Liability Insurance

- Using Your Insurance to Win More Commercial Bids

- Protecting Your Business from Subcontractor Mistakes

- Your Checklist for Getting the Right Roofer Liability Policy

Why Your Roofing Insurance Is More Than a Piece of Paper

A roofer lands a chance to bid a retail center reroof. The scope is solid. The crew can handle it. Then the insurance requirements come in. The owner wants higher liability limits, the general contractor wants additional insured wording, and the certificate has to match the contract exactly. If the paperwork is wrong, the roofer doesn't get to mobilize.

That paperwork issue isn't separate from the inherent risk. It's tied directly to the kind of losses roofers create when something goes wrong. A pallet shifts during material staging. A ladder swings into custom siding. A laborer drops debris and it lands on a parked car. Roofing puts people, property, and expensive contracts in the same place at the same time.

Some of the toughest claims also arrive after everyone thinks the job is over. A church calls back after the next heavy storm. Water has made its way into insulation and down an interior wall. The owner doesn't care whether the issue came from flashing, sequencing, or another trade. The roofer is still in the line of fire.

Practical rule: Insurance for a roofer isn't just for lawsuits. It's also a qualification tool for bigger jobs and a shield between one bad loss and the owner's personal balance sheet.

Storm-chasing seasons make this even sharper. Contractors that handle hail and wind work often move fast, deal with stressed property owners, and juggle urgent timelines. Anyone involved in managing storm damage and claims already knows how quickly small documentation mistakes turn into payment disputes and insurance headaches.

Commercial clients usually judge professionalism long before the first tear-off starts. They look at the contract package, the endorsements, and the certificate request. A roofer that can respond cleanly and accurately is easier to trust. A roofer that can't may lose the job to someone with the same craftsmanship but better insurance readiness. For contractors that need to understand the paperwork side, a solid certificate of insurance template helps clarify what project owners are asking for.

What General Liability Actually Covers on the Jobsite

General liability insurance for roofers is built for claims involving third-party bodily injury and third-party property damage. In plain English, that means it responds when someone outside the roofing company says the roofer caused injury or damaged their property.

The core jobsite claims GL is built for

A few roofing examples make this easier to pin down:

- Pedestrian injury: A delivery driver walks past the house, trips over a hose or safety cone near the work area, and breaks a wrist.

- Damage to someone else's property: A bundle slides off the roof and dents the homeowner's car in the driveway.

- Accidental damage during setup: A ladder shifts while being moved and scratches new siding on the elevation.

- Debris-related damage: Tear-off material gets loose in the wind and breaks a neighbor's window.

Those are classic GL scenarios. The policy is there because roofers work above occupied homes, near vehicles, around walkways, and on buildings that often stay in use while work is happening.

That's also why limit selection matters. A roofing contractor may think of a damaged gutter or broken window as the typical claim. But a single falling object can injure a bystander, trigger a legal defense bill, and pull the property owner, general contractor, and roofer into the same dispute.

A good GL policy doesn't just answer, “Is there liability?” It also answers, “Who's defending the roofer when several parties start pointing at each other?”

Roofers that track storm-driven demand also see how exposure changes when crews are stretched thin and jobs stack up quickly. During high-volume seasons, operational discipline matters as much as coverage. Contractors planning around surge periods may find a report on 2026 storm opportunities useful for the business side of that cycle.

Where roofers get tripped up

The biggest misunderstanding is thinking GL is the entire roofing insurance package. It isn't. Even roofers shopping for one policy often find out after a claim or certificate request that major gaps still exist. As noted in this explanation of roofing insurance gaps, GL doesn't cover employee injuries, vehicle accidents, or stolen equipment.

That means these common losses go elsewhere:

- An employee falls off the roof: That belongs under workers' compensation, not GL.

- A company truck rear-ends another vehicle: That belongs under commercial auto.

- Tools are stolen from a trailer or jobsite: That usually points to inland marine or equipment coverage.

- Damage to the roofer's own truck or owned equipment: GL isn't built for that either.

For contractors trying to choose the right structure, it helps to start with the exposure and then match the policy. That's the same reason many roofers compare general liability coverage limits against the rest of the insurance stack instead of treating GL as a stand-alone purchase.

Roofing incident vs. the right insurance policy

| Jobsite Incident | What It Damages | Correct Insurance Policy |

|---|---|---|

| A pedestrian trips near the work area | Third-party bodily injury | General liability |

| A shingle bundle falls on a customer's car | Third-party property damage | General liability |

| A roofer tears a knee stepping off a ladder | Employee injury | Workers' compensation |

| A company pickup causes a road accident | Vehicle liability and auto damage exposure | Commercial auto |

| Nail guns and compressors are stolen from the trailer | Contractor's movable equipment | Inland marine |

| A leak claim shows up after the job is finished | Post-completion liability allegation | General liability with completed operations provisions |

The Fine Print That Can Make or Break Your Roofing Policy

A roofer can buy a policy that looks fine on the certificate and still have real coverage trouble when a claim lands. Roofing is one of those trades where the wording matters almost as much as the limit. If the operations description is wrong, if key endorsements are missing, or if the policy carries exclusions that don't match the work, the paper can look compliant while the actual protection is thin.

Completed operations is where roofing gets expensive

Roofing claims don't always happen during tear-off or install. Some of the most painful ones come later. The building owner notices staining around skylights months after completion. A property manager alleges the flashing failed. A tenant says inventory was damaged because water entered after the roofer signed off the job.

That's where completed operations becomes central. As discussed in this breakdown of roofers general liability coverage, completed-operations exposure is a major issue for roofers because leak or faulty-installation allegations can surface long after the crew has left. The same discussion points to specialized roofing programs that include features like per-project aggregates and broad acceptance for subcontracted work, which signals how often a basic form falls short on contract-driven jobs.

A few details matter more than many buyers realize:

- Per-project aggregate wording: On larger jobs, this can help prevent one claim from eating up the full aggregate available to all projects.

- Subcontracted work treatment: If a roofer subs out part of the install, the policy language needs to fit that operating model.

- Contract wording: A promise in the subcontract can be broader than the policy the roofer bought.

A leak claim six months later is still a roofing claim. The fact that the crew is gone doesn't make the exposure disappear.

Endorsements and exclusions that deserve real attention

Roofers should read the exclusions with the same care they give the declarations page. A cheap policy can still be the wrong buy if it cuts out the kind of work the contractor performs.

Important review points include:

- Heat or torch work: If the roofer uses processes involving heat, that needs to line up with the policy.

- Open-roof exposure: Some carriers narrow or scrutinize projects where the structure is exposed during active work.

- Residential versus commercial scope: A contractor rated one way can hit trouble if operations drift into work the carrier didn't price for.

- Subcontractor conditions: Some policies expect strict certificates and written agreements before coverage lines up the way the roofer assumes.

- Additional insured wording: Commercial jobs often require it, and many contractors don't verify the exact endorsement until the GC rejects the certificate.

For project paperwork, additional insured status isn't just contract jargon. It changes how protection is extended to upstream parties on the job. Roofers that need a plain-English explanation can review an additional insured endorsement guide before the next subcontract lands in the inbox.

What Roofers Should Expect to Pay for Liability Insurance

Pricing for general liability insurance for roofers doesn't move in a straight line. Two contractors doing similar work can see very different premiums because carriers care about the full exposure picture, not just the class code. Roof pitch, building type, loss history, subcontracting habits, geography, and contract demands all push the number around.

Typical limits and when they need to go higher

For many roofers, a common market benchmark for general liability is $1 million per occurrence and $2 million aggregate, and some commercial roofing jobs require $3 million to $5 million with umbrella coverage added, as noted in this roofing operations market overview. That same market example also references roofing GL being offered at $1M/$2M with $5M excess or umbrella authority and additional insured wording available for contract compliance.

Those bigger limits usually show up when the roofer is dealing with:

- Large commercial properties: Shopping centers, industrial roofs, multifamily complexes, and occupied facilities create broader exposure.

- Demanding upstream contracts: Some owners and general contractors set their insurance requirements before bid selection.

- Higher consequence locations: A mistake over a storefront, medical office, or busy access point can create a much larger claim than the same mistake on a detached shed.

A contractor shouldn't assume the standard limit is automatically enough. The right question is whether the limit matches the projects being pursued.

Why one roofer pays far more than another

MoneyGeek found roofing business insurance averaging $329 per month or $3,944 annually, and reported general liability premiums ranging from $396 per month in West Virginia to $1,158 per month in California, which is nearly a 3x spread for similar work, according to its roofing insurance cost analysis.

That kind of variation tells roofers something important. Premium isn't only about the individual business. It's also about where the work happens and how the market views that risk.

Common pricing drivers include:

- Type of roofing work: Residential repair, replacement, commercial flat work, and specialized systems don't all get viewed the same way.

- Crew size and payroll: More people on more roofs means more chances for a claim.

- Use of subcontractors: Heavy subcontracting can increase scrutiny if insurance controls are weak.

- Claims history: A contractor with prior losses will usually face tougher pricing or tighter terms.

- Geographic claim environment: Some states and territories price harder than others.

Workers' comp also affects the total insurance budget, especially for a growing roofer with a larger field crew. A contractor that wants to understand how past losses influence that line should review how a workers' comp experience modification can shape costs beyond GL.

Low premium by itself doesn't mean low cost. A policy that misses the operation, carries the wrong exclusions, or can't satisfy contract language often becomes more expensive when the job starts.

Using Your Insurance to Win More Commercial Bids

Insurance can block a commercial job, but it can also help win one. Many owners and general contractors won't even finish reviewing a roofing bid until the insurance side looks clean. That means the certificate, endorsements, and named parties need to be right early, not after award.

Why the COI matters before work starts

The certificate of insurance, or COI, is the document that proves the roofer carries the requested coverage. It doesn't replace the policy, but it acts like a gate pass. If the certificate doesn't show the right entities, limits, or endorsements, the contract can stall.

That matters most on work such as retail centers, apartment complexes, schools, and industrial sites. A roofing company may have the right crew and equipment, but if the GC needs proof by end of day and the insurance package isn't ready, another bidder can move ahead.

Commercial readiness also supports the marketing side of growth. Contractors focused on boosting roofing company leads often concentrate on ad spend and follow-up speed, but bigger opportunities also depend on being administratively ready when the serious buyer asks for insurance documentation.

Additional insured status in plain English

Additional insured status means the roofer extends certain liability protection to another party named in the contract, usually the owner or general contractor, when the claim arises out of the roofer's work. On commercial projects, that request is routine.

A practical example makes it clear. A roofer bids on a new shopping center. The developer's rep wants the proposal, safety plan, and COI package up front. The subcontract requires the GC to be added as an additional insured. If the roofer can provide that cleanly and quickly, it reduces friction. The GC sees a contractor that understands commercial process, not just installation.

Some insurance advisors build their workflow around that need. Coverage Axis, for example, states that it handles market outreach through licensed advisors and provides 24-hour COI turnaround for contractor accounts. That kind of process matters because insurance responsiveness often becomes part of the contractor's sales process, whether the roofer planned it that way or not.

Protecting Your Business from Subcontractor Mistakes

Many roofers carry solid liability coverage and still leave one major hole open. They hire subs without checking whether those subs are properly insured. When that happens, the hiring contractor can end up absorbing a claim that should have been pushed downstream.

Why the claim can come back to the hiring roofer

Take a common setup. A roofing company hires a gutter crew or siding sub to finish related exterior work. The sub shows up, starts fast, and no one asks for current certificates. Then a worker drops material onto a storefront awning, or a laborer falls and the injury story gets messy. The property owner doesn't care how the internal subcontract chain worked. The hiring roofer is still the name on the prime contract.

That's the practical side of vicarious liability. If the sub doesn't have the right insurance, the upstream contractor's policy is often where people turn first. Even when coverage exists, the roofer may still deal with the reporting burden, defense issues, and future premium pressure.

Hiring a subcontractor doesn't transfer risk by itself. Documentation transfers risk.

A simple risk transfer routine

Roofers don't need a complicated system. They need a disciplined one.

- Collect the certificate before work starts: No certificate, no mobilization. It's that simple.

- Verify the policies match the exposure: The sub should carry its own general liability and workers' compensation where applicable.

- Use a written subcontract agreement: Responsibilities, hold harmless language, and insurance requirements should be documented before the first day on site.

- Watch expiration dates: A certificate that was valid at bid time may not be valid halfway through the project.

This matters even more when labor is fluid and crews change during storm seasons or fast-growth periods. A roofer that regularly hires labor-only or specialty subs should understand when workers' comp for subcontractors becomes a direct business issue instead of just an HR detail.

A well-run subcontractor file won't prevent every dispute. It will, however, give the roofer a much better shot at pushing the claim to the right policy and keeping one sub's mistake from distorting the roofer's own loss record.

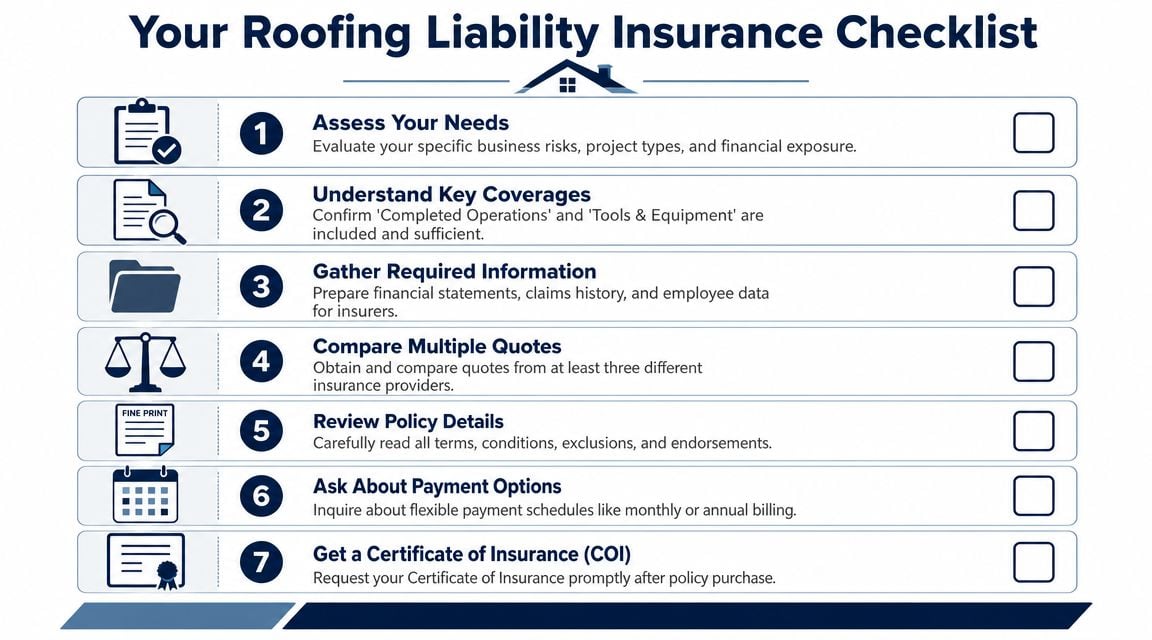

Your Checklist for Getting the Right Roofer Liability Policy

The right policy starts before the quote request. A roofing contractor that gives vague information usually gets vague coverage back. The cleaner the submission, the more accurate the terms, exclusions, and pricing tend to be.

What to gather before asking for quotes

Before shopping, roofers should pin down the facts of their operation:

List the actual work performed

Note whether the company handles residential, commercial, repair, replacement, coatings, tear-off, or specialty systems. Include whether heat is used and how much work is subcontracted.Pull contract insurance requirements

A roofer chasing commercial work should gather sample GC and owner requirements first. That's how higher limits, additional insured wording, waiver requests, and umbrella needs show up before the quote comes back.Review the current policy for gaps

Look closely at exclusions, completed-operations wording, and any mismatch between the policy description and the real work being done.

The best time to find a roofing exclusion is before the first loss, not during a reservation-of-rights letter.

How to compare policies without getting fooled by price

Once quotes arrive, roofers should compare more than premium.

- Check the operations description: If the insurer classified the business too narrowly, the price may look good for the wrong reason.

- Read endorsements and exclusions: A lower premium can hide restrictions that remove value where the roofer needs it most.

- Confirm certificate support: Fast COI handling matters for bid work and contract compliance.

- Ask direct questions about subcontracted work and post-completion claims: If the advisor can't answer clearly, the roofer should keep digging.

A strong general liability insurance program for roofers is built around the work they do, the contracts they sign, and the losses that happen in roofing. Cheap paper that won't stand up to a leak allegation, a dropped bundle, or a strict commercial contract isn't a bargain.

Coverage Axis offers free quotes and no-obligation coverage reviews for contractors that need trade-specific guidance on general liability, workers' comp, commercial auto, inland marine, and umbrella coverage. Roofers that want a plain-English review of limits, exclusions, completed-operations exposure, and contract requirements can request a free coverage review through Coverage Axis.