A painting contractor wins a promising job. The scope looks fine, the schedule works, and the price is close. Then the contract turns to insurance. The owner wants a certificate before mobilization, the general contractor wants additional insured status, and the job specs call for limits that don't match the policy already in place. At that point, a lot of painters learn the hard way that having insurance isn't the same as having insurance that fits the work.

That gap shows up in smaller jobs too. A gust pushes overspray onto a parked vehicle. A customer's tenant trips over masking paper near an entry. A crew finishes an exterior repaint, leaves the site clean, and months later the owner claims moisture got behind a failed coating system and damaged the substrate. The policy question isn't just whether painter liability insurance exists. The question is whether the whole insurance setup matches the kind of jobs the business is taking.

For this reason, trade-specific planning is essential. A residential repaint contractor, a school turnover painter, and a commercial new-construction finisher don't carry the same exposures, even if all three buy general liability. The right program has to follow the work.

Table of Contents

- Why Your Current Insurance Might Not Be Enough

- What Painter Liability Insurance Actually Covers

- Beyond the Basics Key Endorsements and Exclusions

- Decoding Policy Limits and Certificates of Insurance

- What Drives Your Painter Insurance Costs

- Smart Risk Control for Painting Contractors

- How to Get the Right Coverage for Your Business

Why Your Current Insurance Might Not Be Enough

A basic policy often works until the work changes. A painter who mostly handles interior residential repaints can usually get by with a simpler setup than a contractor bidding apartment turnovers, schools, retail spaces, or new construction. The trouble starts when the business grows faster than the coverage.

A common example is the first serious commercial bid. The painter opens the insurance requirements and sees requests for additional insured status, waiver wording, specific completed operations protection, and proof of limits that go beyond what the current policy was built for. The contractor thought the business was covered because a policy existed. The contract shows otherwise.

That problem isn't always about buying more insurance. Sometimes it's about buying the right insurance for the way the business operates. A painter doing occupied residential work faces one set of issues. A painter using sprayers around parking lots, storefront glass, HVAC intakes, and pedestrian traffic faces another. A contractor handling new construction may also run into contract transfer language that shifts more risk back downstream than expected.

Practical rule: Insurance should be reviewed any time the business changes job type, starts using subcontractors more heavily, adds vehicles, or begins bidding projects with formal contract exhibits.

Many trade owners first look at coverage as a licensing or bid requirement. That's understandable, but it's too narrow. Painter liability insurance also protects the balance sheet, the ability to stay on schedule after a claim, and the credibility to keep bidding better work.

Contractors that need a broader overview of trade coverage requirements can compare the moving pieces in this contractor insurance guide. The important point is simple. The policy that got a one-crew shop through handyman-style repaint work may not hold up once the business starts taking on higher-limit contracts and higher-consequence jobsite conditions.

What Painter Liability Insurance Actually Covers

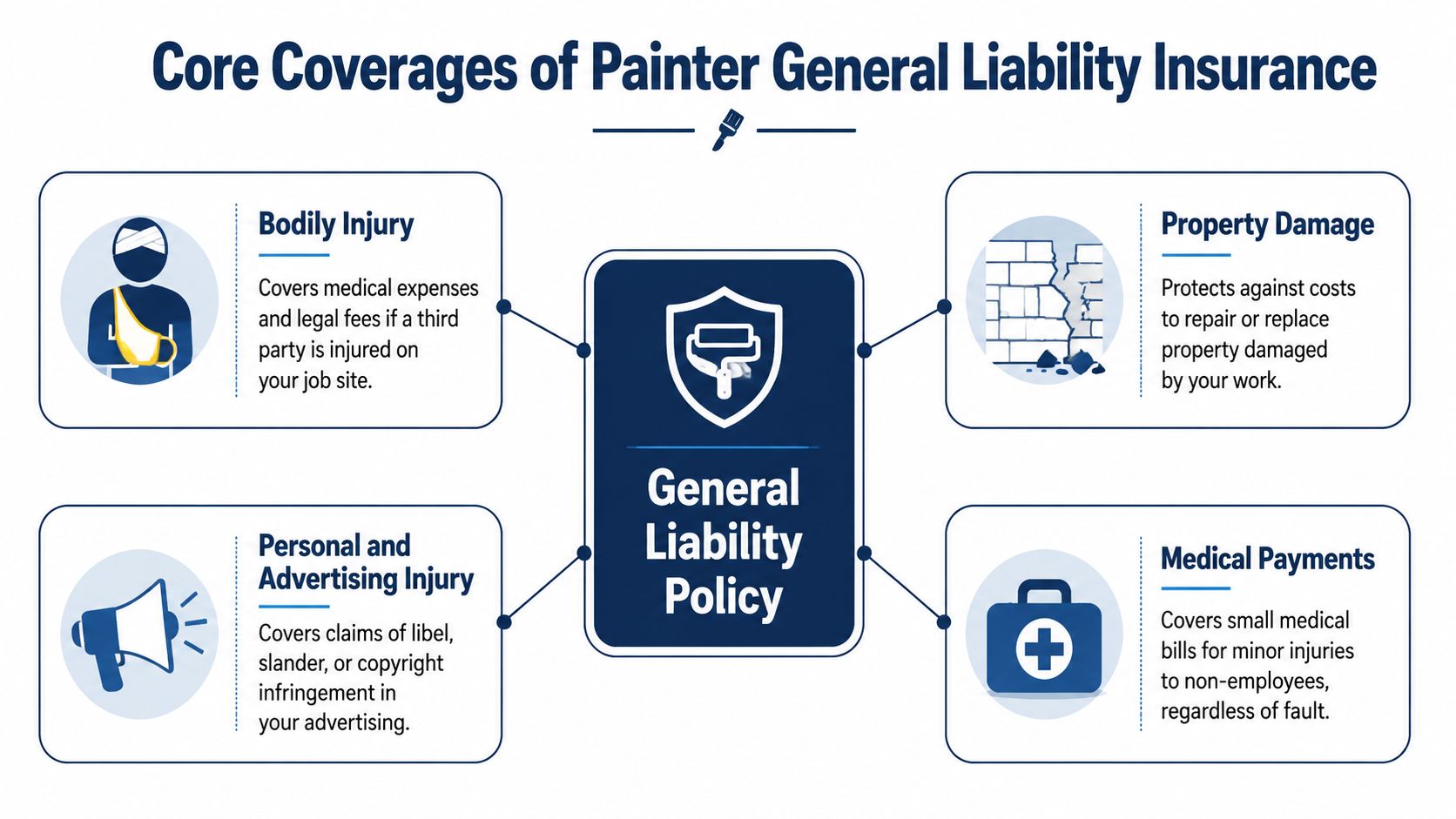

General liability is the foundation of painter liability insurance because painters regularly create third-party bodily injury and third-party property damage exposure. For this trade, that usually means the public, the client, tenants, visitors, or neighboring property. It does not mean injuries to employees, and it does not mean every mistake made to the painter's own work.

For painters, this core policy is usually the starting point because bodily injury and property damage are the main third-party claim drivers. Pricing benchmarks for painters also show that general liability averages about $59 per month, while workers' compensation averages about $239 per month and commercial auto averages about $139 per month, which highlights that employee and vehicle exposure often cost more than the base liability policy itself, according to painting contractor insurance benchmarks.

The core claim paths painters face

The easiest way to understand general liability is to tie it to jobsite events.

A bodily injury claim can start with something as ordinary as a walkway. A crew leaves drop cloths, masking material, or hoses in a path of travel, and a tenant or customer trips. If that injured person isn't an employee, general liability is the policy that may respond.

A property damage claim is just as familiar. Overspray hits a vehicle. A ladder damages a window frame. Paint or solvent gets onto finished flooring, stone, landscaping, signage, or storefront glass. If the painter's operations damage someone else's property, that usually falls into general liability territory.

A standard policy can also include medical payments for minor injuries to non-employees regardless of fault, and personal and advertising injury for issues tied to things like slander, libel, or certain advertising claims. Those aren't usually the first concern for painters, but they're still part of the core policy structure.

For contractors who want a plain-English breakdown of how this policy works in the trades, this overview of general liability insurance for contractors is a useful reference.

Why completed operations matters after the crew leaves

Completed operations is where many painters get tripped up. Damage that happens while the crew is actively working is one thing. Damage that shows up after the work is finished is another.

Take an exterior repaint on a multi-unit property. The job closes out, the owner signs off, and everyone moves on. Later, coating failure, preparation issues, or moisture intrusion are alleged to have caused damage beyond the painted surface. That's no longer a live-job incident. It's a completed operations issue.

A useful way to think about it is timing. If the ladder scratches a parked car during the project, that's an operations claim. If the owner later claims the finished work led to damage after turnover, that's where completed operations becomes important.

The liability tail on a painting job doesn't end when the crew pulls the masking and leaves the site.

This matters even more on commercial work, where owners, property managers, and general contractors often expect the painter's policy to support claims tied to work after completion. Residential repaint work can create this exposure too, but larger projects tend to make the distinction much more consequential because more parties are involved and contract language is tighter.

Beyond the Basics Key Endorsements and Exclusions

A painter wins a commercial interior job, sends over the certificate, and still gets pushed back by the GC. The problem usually is not the base general liability policy. The problem is that the job requires specific endorsements, and the contract shifts obligations the policy may not match.

That is where painters get caught. A residential repaint can often run on a simpler setup. A school project, tenant improvement, or new construction job usually cannot. The right insurance program changes with the work. General liability is the foundation, but completed operations, inland marine, and a few contract-driven endorsements often decide whether the coverage holds up on a real claim.

Where general liability stops

General liability is built for third-party bodily injury and property damage. It is not a warranty for the painter's own work.

The clearest example is care, custody, and control. If the crew is spraying cabinet doors, refinishing trim, or coating a steel door package and damages the very surface being worked on, the policy may not treat that as covered third-party damage. In many claims, the cost to repair or redo the painter's own work stays with the contractor.

That line matters on fine-finish work and new construction punch work, where one bad application can mean expensive rework but not an insured loss.

The exposure can widen when the painter is doing more than application. Recommending a coating system for a high-moisture space, choosing products for an exterior with substrate issues, or advising on prep for an industrial environment can create a services exposure that does not fit neatly inside standard liability coverage. Not every painter needs professional liability, but shops that spec products, advise owners, or take on finish-system decisions should review it.

Endorsements that matter on real painting jobs

The endorsement package should match the job type, not just the business class code.

Additional insured status: Commercial owners and general contractors often require the painter to extend liability protection to them for claims tied to the painter's ongoing or completed work. The wording matters. Some endorsements are narrow, some are broad, and some only apply when a written contract is in place before the loss. Painters who want the plain-English version should review how an additional insured endorsement works before signing.

Pollution limitations and exclusions: Spray application, solvents, coatings with stronger chemical content, and work around HVAC returns or occupied interiors can create claims that run into pollution exclusions. On a house repaint, that issue may be limited. On a hospital renovation, office build-out, or enclosed commercial project, it deserves a close review before work starts.

Inland marine for mobile tools and equipment: General liability does not insure sprayers, scaffolding, ladders, dust-control gear, or other equipment that moves from the shop to the truck to the jobsite. Inland marine is usually the policy that picks up that property exposure. For a residential repaint crew, that may mean protecting a few key sprayers and sanders. For a commercial crew, it may mean protecting a much larger block of mobile equipment across multiple jobs at once.

Waiver of subrogation and primary and noncontributory wording: These are common on commercial contracts and public work. They do not change every claim outcome, but they can affect how the policy responds and whether the certificate request can be met cleanly.

Contract transfer terms: Indemnity language often reaches further than the insurance. Before agreeing to broad hold harmless language, review what the contract is asking the painter to assume. This indemnification guide for South Florida businesses gives a practical legal primer on how that language works.

A painter can meet the bid requirement and still carry a gap if the contract promises protection the policy does not provide.

That risk shows up more often on commercial new construction than on residential repaint work. Residential jobs usually need a tighter, cleaner package with strong general liability, completed operations, and inland marine for tools. Commercial work often needs those same core coverages plus endorsement wording that matches the subcontract, the certificate requirements, and the way the job will be performed.

Decoding Policy Limits and Certificates of Insurance

Policy paperwork can look abstract until a job can't start without it. For painters, the most important pieces are the liability limits and the certificate of insurance. One tells the market how much protection exists. The other proves the policy is in force and shows whether the contract requests were handled.

What the limit language actually means

A common benchmark for painter liability coverage is $1 million per occurrence and $2 million aggregate, according to guidance on liability limits for painting contractors. The cleanest way to explain it is with buckets.

The per occurrence limit is the bucket for one covered incident. If one overspray event, one trip-and-fall, or one property damage loss turns into a covered claim, that bucket applies to that event.

The aggregate limit is the total bucket for covered claims over the policy term. If several covered claims hit during the year, they draw against that larger total. Once that total is exhausted, the policy won't keep paying forever.

That same guidance notes that commercial umbrella insurance for painters averages $59 per month, or $707 per year. For painters stepping into larger commercial work, umbrella coverage can be a practical way to add capacity when the contract or project size makes the base limits feel thin.

On a small residential repaint, the base limit may feel comfortable. On a multi-unit project with public traffic, vehicles, and schedule pressure, the same limit can feel much smaller.

What clients are really checking on a COI

A certificate of insurance, or COI, is the document most clients ask for before work starts. It's the jobsite passport. But clients usually aren't just checking whether insurance exists. They're checking whether the document matches the contract.

They often look for a short list of details:

| Contract item | Why it matters to the client |

|---|---|

| Named insured | Confirms the legal business on the policy matches the contracting party |

| Effective dates | Shows the policy will still be active during the job |

| Policy types | Verifies general liability, auto, workers' compensation, or umbrella when required |

| Limits shown | Confirms the policy meets the minimum threshold in the contract |

| Special wording | Signals whether endorsements such as additional insured status have been issued |

Painters also run into waiver of subrogation language. In plain English, that's a request that the insurer give up certain recovery rights against the party named in the waiver, subject to the policy and endorsement terms. It's common in construction contracts and shouldn't be treated as routine paperwork.

Homeowners and small property owners can also struggle to read insurance language. While it addresses a different policy type, this consumer-friendly article on decoding your Arizona home insurance is a good reminder that policy wording often sounds simple until the exclusions and endorsements start changing the result.

A painter that regularly issues certificates should also understand the document format itself. This walkthrough of a certificate of insurance template helps clarify what each field is trying to show and what a certificate does not guarantee by itself.

What Drives Your Painter Insurance Costs

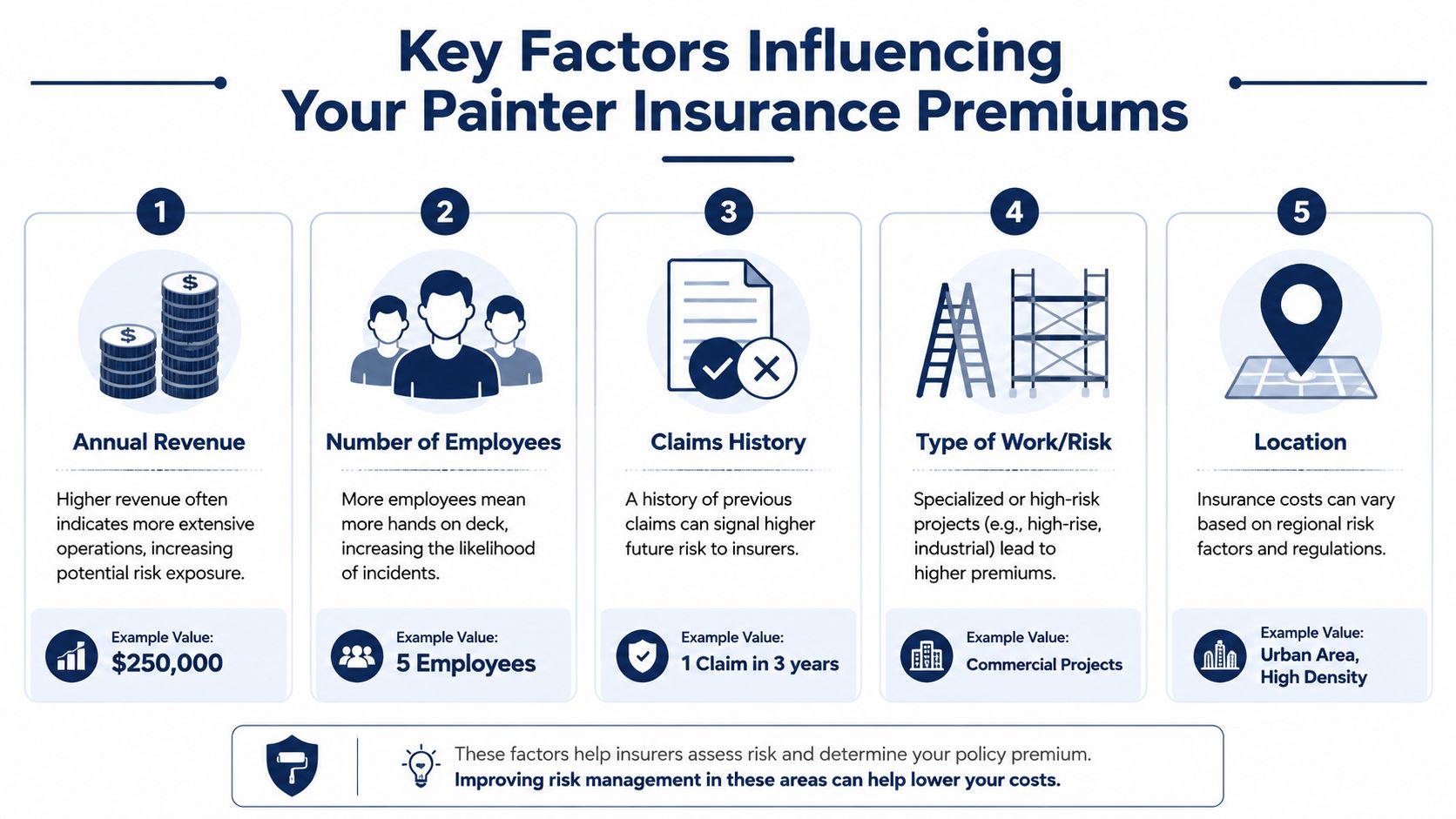

The total cost of a painter's insurance program rarely comes from general liability alone. That's why some contractors underestimate their true insurance spend when they focus only on the liability line needed for a certificate.

For painting businesses, benchmark pricing shows general liability averages $59 per month ($704 per year) and a business owner's policy averages $84 per month ($1,002 per year). The larger cost drivers are often workers' compensation at $239 per month ($2,871 per year) and commercial auto at $139 per month ($1,673 per year), based on 2026 painter insurance cost data. That pattern tells a practical story. Payroll and vehicles usually move the budget more than the base liability form.

The cost drivers that matter most

A painter's premium is usually shaped by a handful of operational facts.

- Payroll size: Once a contractor adds helpers, foremen, or multiple crews, workers' compensation becomes a much larger part of the insurance picture.

- Vehicles on the road: Vans, pickups, trailers, and regular jobsite driving add commercial auto exposure quickly.

- Claims history: Carriers pay close attention to prior losses, especially preventable vehicle incidents, falls, and property damage claims.

- Scope of operations: Interior repainting in occupied homes doesn't look the same as exterior spray work, high-reach work, or large commercial projects.

- Business structure and packaging: Some painters buy monoline policies. Others place property and liability together in a business owner's policy when that structure fits.

A contractor trying to control workers' compensation costs should also pay attention to how loss history affects the rating side of the policy. This overview of workers comp experience modification is worth reviewing because repeated injury claims can shape future pricing long after one bad year.

Why job type changes the conversation

A residential repaint business usually has different insurance pressure points than a commercial painter.

Residential work tends to center on customer property, occupied homes, surface protection, and reputation-sensitive disputes. Commercial work adds formal contracts, site rules, public exposure, additional insured requirements, and more layered responsibility between trades.

A new-construction painter may have lower public foot traffic than a repaint contractor in an occupied retail center, but much heavier contract risk. A maintenance repaint contractor may have lighter contract language but much more exposure to pedestrian claims, parked vehicles, and complaints from tenants or neighboring units.

That's why price shopping without matching the operations often backfires. Two painters can pay very different premiums because they're not really doing the same kind of work, even if both describe themselves as painting contractors.

Smart Risk Control for Painting Contractors

A painter wins a commercial bid on Monday and gets hit with an overspray complaint on Wednesday. Those two problems look unrelated, but they usually trace back to the same issue. The field controls did not match the job.

Risk control for painters works best when it follows the type of work being performed. A residential repaint crew in occupied homes needs tight protection for floors, fixtures, and customer property. A commercial new-construction crew needs stronger subcontractor controls, site-specific safety procedures, and records that hold up when the GC starts sorting out responsibility after a claim.

The habits that prevent the avoidable claims

Start with subcontractors if you use them. If a sub causes property damage or injures someone, the hiring painter is often the first name pulled into the claim. Collect current certificates before work starts, confirm the legal business name matches the contract, and make sure the sub's coverage fits the work being handed off. A sub hired for basic prep work creates a different exposure than a crew spraying exterior façades near parked cars and pedestrian traffic.

Containment deserves the same job-by-job approach. Overspray claims rarely come out of nowhere. They usually follow rushed masking, weak barriers, poor ventilation planning, or a bad decision to spray when site conditions say no. Exterior work near storefronts, vehicles, rooftop air intakes, or neighboring buildings needs a firmer stop-work standard than an interior residential repaint with brush and roller application.

Documentation changes the claim outcome too. Before photos, daily job logs, signed change orders, and stage-completion signoffs can keep a finish dispute from turning into an allegation that the painter damaged the whole project. If siding was already chalking, drywall already had water marks, or trim was already failing before prep began, the file should show it clearly.

The same goes for material selection. On residential jobs, a written approval for color, sheen, and product choice helps prevent the classic “this isn't what I expected” dispute. On commercial work, it also helps show whether the painter followed spec, proposed a substitution, or applied a product outside the original scope.

A practical checklist helps:

- Photograph the work area: Capture floors, windows, fixtures, landscaping, nearby vehicles, and visible pre-existing damage before setup starts.

- Confirm the go-or-no-go conditions for spray work: Wind, ventilation, adjacent trades, open intakes, and public access should be checked before spraying begins.

- Use written material approvals: If the owner, tenant, or GC approves a color, sheen, or coating system, get that approval in writing.

- Train on access and cleanup: Ladder handling, hose placement, cord routing, and end-of-day housekeeping prevent many injury and property-damage claims.

- Keep equipment accountability tight: Track sprayers, hoses, and ladders by crew and job so missing or damaged equipment does not turn into delays, disputes, or preventable inland marine claims.

Clean files and clean jobsites usually go together. Contractors that document well also tend to manage risk better in the field.

How to Get the Right Coverage for Your Business

Most painters don't need a more complicated insurance program. They need a more accurate one. The fastest way to get there is to build coverage around the actual work, not around a generic description of the trade.

A simple way to build a better insurance submission

First, gather the operating details that drive underwriting. That includes payroll by role, vehicle information, loss runs if available, subcontractor use, and a clear description of the jobs being performed. A painter who does mostly brush-and-roll residential repaints should say that. A contractor doing commercial spray applications, tenant improvements, and coating recommendations should say that too.

Second, separate the jobs by exposure. Residential interiors, occupied exteriors, apartment turnovers, schools, retail, industrial coatings, and new construction don't create the same contract requirements or the same claim pattern. The policy should reflect where risk sits.

Third, compare the contract requirements to the policy structure before the next bid goes out. Additional insured wording, waiver requests, completed operations expectations, equipment exposure, and the need for umbrella limits should be reviewed before the owner asks for a certificate at the last minute.

This kind of review gets easier when the coverage discussion is tied to actual jobs instead of abstract insurance terms.

A painter bidding higher-value work, adding employees, or taking on more commercial contracts should treat that review as part of normal business planning. The right painter liability insurance program supports the bid, protects the operation during the job, and still holds up when a claim shows up after completion.

If the current policy feels generic, or if upcoming jobs come with tougher insurance requirements, Coverage Axis can provide a free quote or coverage review for painting contractors who want a program built around the work they perform.