Monday starts with a foreman asking why the renewal jumped again, even though the crew hasn't had a serious driving issue in months. The vans are lettered, the pickups are maintained, and every missed discount goes straight into overhead. For a contractor bidding tight work, commercial auto isn't just another line item. It affects margins, cash flow, and how aggressive a company can be on the next proposal.

That's where the safe driver discount gets attention fast. On paper, it sounds simple. Keep drivers clean, pay less. In practice, contractors run into mixed fleets, shared vehicles, heavier units, and carrier rules built more for personal cars than trade operations. A plumbing shop with three service vans doesn't get judged the same way as a homeowner with one sedan.

This guide is built for contractors, not commuters. It focuses on the part generic insurance articles usually skip. How safe driver discounts work when a business has pickups, vans, dump trucks, trailers, and crews moving between jobs all day.

Table of Contents

- Why Your Good Drivers Still Have High Premiums

- Understanding the Safe Driver Discount

- Why Standard Discounts Often Fail Contractors

- The Contractor Playbook for Qualifying

- Proving Your Safety to Lower Your Rates

- Finding Insurers Who Understand Your Trade

- Take Control of Your Commercial Auto Premiums

Why Your Good Drivers Still Have High Premiums

A small plumbing contractor is a common example. Four service vans, one pickup, the same techs year after year, and a renewal that still comes back higher than expected. The owner knows who speeds, who doesn't, who backs carefully into alleys, and who treats the van like it's their own. Yet the premium doesn't reflect that reality.

That disconnect is why many contractors start asking about a safe driver discount. They're trying to solve a fair question. If the crew drives safely, why isn't the policy rewarding it? The answer usually sits in how commercial auto is rated, not in whether the business deserves a break.

A contractor's policy doesn't look at risk the way a personal auto policy does. Vehicles are used every day, often by multiple employees, under delivery pressure, jobsite conditions, and urban traffic. A service van carrying pipe, ladders, and tools gets treated differently than a family car driving to the grocery store.

Practical rule: A clean crew doesn't automatically create a low premium if the policy structure groups all vehicle and driver exposure together.

That's why it helps to look at the account the same way an underwriter does. Vehicle type, radius of travel, driver mix, claims history, and whether the company can document safe operations all matter. A contractor shopping commercial auto policy options for work vehicles usually gets further by organizing those details before asking for discounts.

What contractors often miss

- Fleet rules matter: One incident can affect the pricing view of the whole account.

- Vehicle use matters: A van used for emergency calls is different from a pickup used by an estimator.

- Proof matters: A carrier can't reward safety it can't see on paper.

A roofing contractor with spotless pickup drivers may still feel the impact of heavier units or prior fleet losses. An electrical contractor may have supervisors with perfect records, but if apprentices rotate through trucks without clear driver assignment, the insurer sees uncertainty. That's the commercial side of the safe driver discount. It isn't impossible to earn, but it takes more than saying the crew drives well.

Understanding the Safe Driver Discount

A safe driver discount is an insurer's pricing credit for lower expected driving risk. In plain language, the carrier believes a driver or vehicle account is less likely to produce accidents, violations, or expensive claims, so the premium may come down.

The broad promise is real. The typical savings range is 20% to 25% for drivers who stay free of accidents and moving violations for three years or more, according to Policygenius on safe-driver savings. That sounds attractive to any contractor trying to control overhead on vans, pickups, or owner-operated trucks.

What the discount really means

For a trade business, the discount usually comes from one of two places. The first is the traditional model, where clean driving records and time without violations support better pricing. The second is usage-based monitoring, where the carrier uses actual driving behavior to set part of the rate.

For owners who want a simple explainer on course-based savings in one state, this guide to Florida insurance savings is a helpful consumer reference. The contractor takeaway is that course completion and clean driving can matter, but commercial fleets usually need stronger documentation and clearer vehicle classifications than personal auto buyers do.

Personal and commercial policies are rated differently

The biggest mistake contractors make is assuming what works on a personal auto policy will transfer neatly to a business policy. It usually doesn't.

| Factor | Personal Auto Policy | Commercial Auto Policy |

|---|---|---|

| Who is rated | Usually a specific household driver setup | Often the business, driver pool, and fleet exposure together |

| Vehicle type | Personal cars and light daily-use vehicles | Vans, pickups, specialty trucks, mixed-use work vehicles |

| Driving pattern | Commuting and personal errands | Jobsites, deliveries, service calls, loaded travel |

| Discount logic | More driver-specific | More account-level and vehicle-class sensitive |

| Proof of safety | Basic record checks or app participation | Record checks, training, maintenance, assignment controls, and sometimes telematics |

A contractor comparing coverage should also understand what sits underneath the discount. Liability limits, hired and non-owned exposure, vehicle schedules, and driver eligibility all affect what a business is buying. This is why a plain-English review of commercial auto liability insurance for contractors matters before chasing the lowest number.

A safe driver discount is useful only if the policy still fits the way the business actually uses its vehicles.

A concrete contractor with one owner-operated pickup has a much easier path than a restoration firm dispatching multiple vans around the clock. The phrase is the same. The underwriting reality is not.

Why Standard Discounts Often Fail Contractors

Construction fleets get stuck in a part of the market that personal auto articles rarely address. The company may have good individual drivers and still miss the credit because the carrier prices the account as one operating unit.

The hard data on that problem is clear. 68% of commercial auto policyholders in construction are penalized due to fleet-wide accident rates, and 52% of contractors with 10+ vehicles report no safe driver discounts despite 90% clean individual records because carriers apply fleet average rules, according to Coverage Axis on construction fleet pricing issues.

The fleet average problem

Take a general contractor with superintendent pickups, one dump truck, and a few shared site vehicles. Most of the supervisors may have clean records. One heavy-unit incident, though, can influence how the whole account gets viewed at renewal.

That's the fleet average trap. The carrier isn't always rewarding each clean driver separately. It may be rating the business on aggregate loss experience, driver mix, and the riskiest vehicle classes on the schedule.

Clean individual records can get buried inside a fleet rating model that focuses on total account performance.

For contractors, this feels unfair because it is disconnected from day-to-day management. The owner sees who the reliable drivers are. The carrier may only see one account with mixed exposures and a loss profile that doesn't fit a standard discount box.

Mixed vehicles change the math

A yard maintenance professional with pickups and trailers is one thing. A site contractor with pickups, flatbeds, and heavier hauling equipment is another. Vehicle type changes severity potential, claim cost expectations, and underwriting appetite.

That's why mixed fleets often struggle to qualify for discounts that sound straightforward in consumer advertising. A company can run service vans carefully and still get priced harder because one segment of the fleet creates higher perceived risk. The problem gets worse when different employees share vehicles across crews, or when driver assignment isn't documented well.

A dump truck operation shows this issue quickly. Even if management keeps strong hiring standards, the underwriter will still focus on heavier-unit exposure, use patterns, and claim potential. Contractors dealing with heavier vehicles should review how dump truck insurance is rated for construction businesses before assuming a standard fleet discount will apply.

What doesn't work

- Relying on verbal assurances: Telling a carrier the crew is careful won't move pricing.

- Treating all vehicles the same: Service vans, pickups, and heavier units shouldn't be presented as identical exposures.

- Waiting until renewal week: Discount strategy takes setup, records, and time.

An electrical contractor bidding school work may have better-than-average drivers, but if the account is presented as a generic fleet, the pricing often follows the broadest risk assumptions. That's why standard discounts fail contractors. The issue usually isn't effort. It's how the fleet is classified, segmented, and documented.

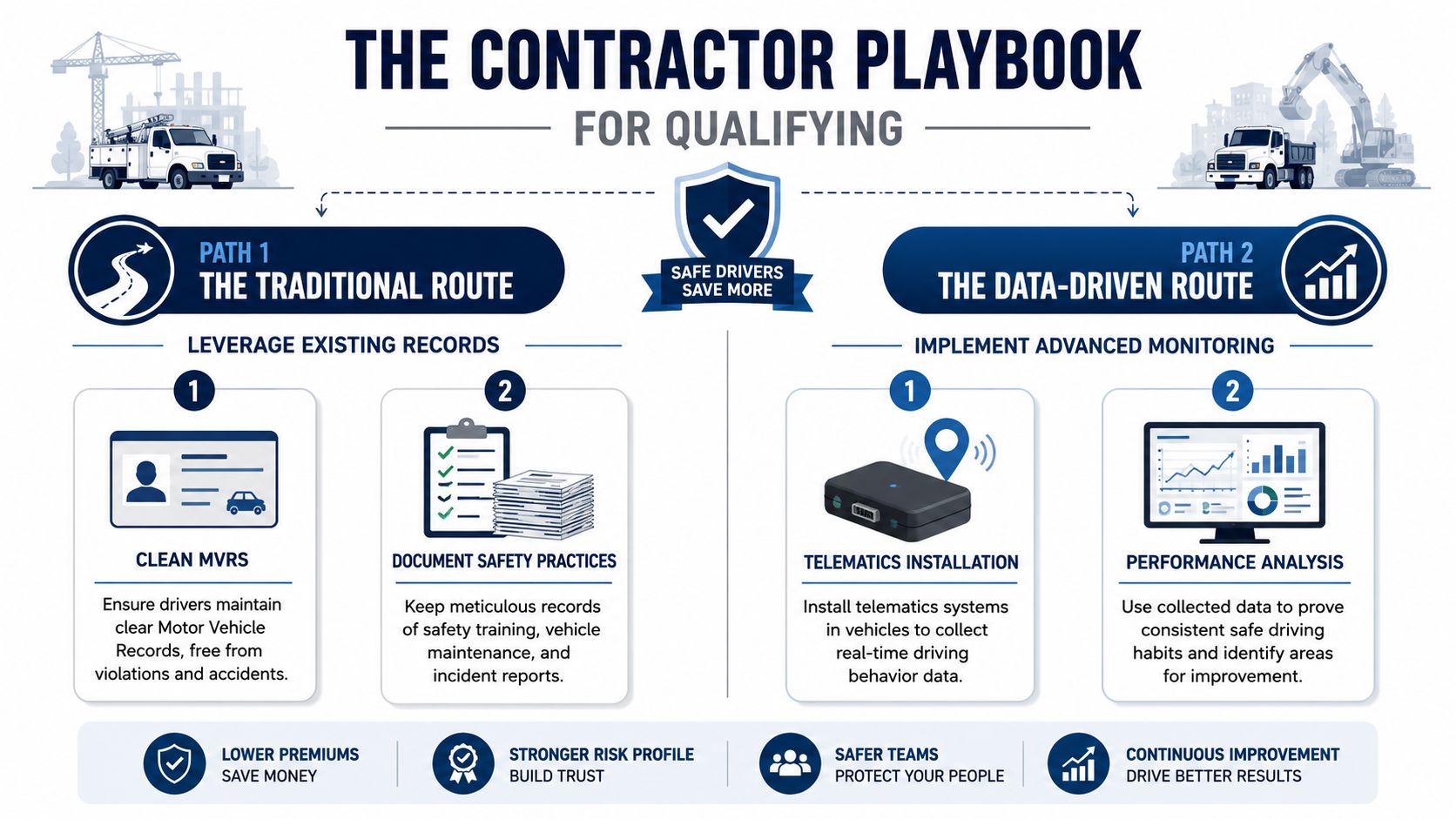

The Contractor Playbook for Qualifying

Contractors usually have two practical paths to a safe driver discount. One relies on records and safety controls that prove the fleet is managed well. The other uses telematics to show actual driving behavior. Both can work. Both come with trade-offs.

The traditional route

Start with the cleanest form of proof. Motor Vehicle Records. If a business wants better pricing, it needs current records on every active driver and a clear hiring rule for who can and can't get behind the wheel.

A roofing contractor is a good example because crews often drive pickups under time pressure, through weather, and with materials in the bed. For that type of operation, qualification may depend on a clean period, often 36 months without at-fault accidents or major violations, with some state variation noted in Travelers' safe driver discount overview. The business lesson is simple. The cleaner and more documented the driver file, the easier it is to ask for credit.

Traditional qualification usually gets stronger when a contractor keeps:

- Current MVRs: Not pulled once and forgotten, but reviewed on a schedule.

- Written driver rules: Seat belts, phone use, backing procedures, and reporting expectations.

- Maintenance logs: Because preventable vehicle issues weaken any safety story.

- Training records: Especially for trades with tougher driving conditions.

High-risk trades have another angle. Some contractors in roofing, excavation, and similar operations may qualify for better treatment when they complete certified driving or safety coursework. Many firms miss that opportunity because generic carriers don't clearly explain tiered approaches for tougher trades.

The best discount conversations happen when the business can show a repeatable safety system, not just a clean month.

A safety program also needs accountability. Assigned vehicles help. So do written corrective actions after violations, even when there's no claim. Underwriters want to see management control.

The telematics route

Telematics can help contractors who want to prove what happens on the road, not just what appears on an MVR. That usually means a mobile app or installed device monitoring behavior like speed, braking, and acceleration.

A practical trade example is an HVAC technician using a monitored driving program. State Farm's Drive Safe & Save offers an initial 10% discount and potential savings up to 30% based on mobile app data, though certain non-standard vehicles may not be eligible, according to State Farm's Drive Safe & Save details. For HVAC fleets, that matters because stop-and-go urban service calls can create the exact braking and acceleration patterns the app is tracking.

Telematics can be useful when a contractor wants to:

- Separate good drivers from fleet assumptions

- Coach drivers with real trip data

- Show an insurer measurable operating discipline

But this route isn't automatic savings. Privacy concerns come up fast. So does driver resistance. A company also needs to read the program terms carefully, especially if vehicles are shared or if some units fall outside eligibility rules.

For contractors building a stronger fleet safety process before renewal, loss control support for growing crews can matter just as much as the insurance application. Stronger controls make either discount path easier to support.

Proving Your Safety to Lower Your Rates

Being safe helps. Proving it is what changes renewal conversations.

That distinction matters more now because telematics has moved into the mainstream. Over 20% of new auto insurance enrollments now use tracking technology, some carriers advertise discounts up to 40%, the typical realized discount is closer to 10%, and drivers under 45 see median annual savings of around $145, according to Damoov's review of U.S. telematics discount programs. The lesson for contractors isn't that every fleet should enroll. It's that insurers increasingly expect better evidence.

Documentation that actually helps at renewal

An electrical contractor bidding institutional work can't walk into renewal with scattered files and hope the underwriter notices the company is disciplined. The file needs to be organized and easy to audit.

A useful checklist includes:

- Driver qualification files: MVRs, license checks, and signed driver policies

- Safety meeting notes: Short records showing recurring vehicle topics

- Maintenance logs: Oil service, tire checks, brake work, and repair records

- Incident reviews: What happened, what changed, and who was retrained

- Telematics summaries: Not every trip, just readable trend reports if the company uses them

The carrier doesn't need a speech. It needs a file that shows the business controls its fleet.

Short, repeatable documentation usually works better than a thick manual nobody follows. A one-page backing policy that every driver signs has more value than a generic handbook copied from somewhere else.

Safety records can help win work

This part gets overlooked. The same fleet documentation that supports a safe driver discount can also help a contractor look stronger to a general contractor, property manager, or project owner.

An electrical subcontractor chasing a hospital project may need to satisfy stricter insurance and compliance review before getting mobilized. If the company can show a written fleet safety policy, current driver records, and vehicle oversight, it signals professionalism. It can also make certificate requests cleaner and faster when the GC wants proof of compliant coverage. Contractors that need better paperwork discipline should understand how a certificate of insurance template is used in project compliance.

That matters to the bottom line because bids aren't won on price alone. Buyers look for contractors who seem controllable, insurable, and less likely to create downstream problems.

Finding Insurers Who Understand Your Trade

A contractor doesn't just need a carrier that offers a safe driver discount. The business needs one that understands what a construction fleet looks like in practice.

Generic underwriting often treats trade fleets too broadly. A landscaping company with trucks and trailers, an HVAC service fleet, and a concrete operation with heavier units can all end up pushed through the same simplified logic. That's where discounts get missed, or offered in ways that don't reflect actual safety practices.

What to ask before moving a fleet

The right questions expose whether an insurer understands the trade or is just quoting vehicle counts.

- How do they handle mixed fleets: Ask whether pickups, vans, trailers, and heavier units are segmented or blended.

- Do they reward documented training: Some carriers care about formal driver management. Others barely ask.

- Can clean drivers get credit inside a broader fleet: This is critical when one part of the operation carries more exposure than another.

- How do they view high-risk trades: Roofing, excavation, and similar work often need more specialized underwriting judgment.

A 2026 survey found 78% of contractors in high-risk trades are unaware that completing certified defensive driving courses can qualify them for tiered discounts such as 10% for standard and 20% for their trade, a framework many generic carriers lack. Contractors should use that insight as a screening tool when interviewing brokers and carriers, even where those discount structures aren't explained clearly in marketing materials.

Why specialist underwriting matters

A specialist underwriter is more likely to ask useful questions. Who drives the trucks. Whether vehicles are assigned. Whether trailers are attached daily. Whether crews cross state lines. Whether heavier units are occasional or central to the operation.

Those details affect pricing and discount eligibility. A specialist is also more likely to understand that an estimator's pickup shouldn't always be rated like a fully loaded field truck, and that a disciplined service fleet may deserve better treatment than a mixed account presented without detail.

A contractor gets better pricing when the insurer sees the business as a managed operation, not just a list of VINs.

The safe driver discount works best when the carrier's model matches the trade. If that fit isn't there, a clean fleet can still get priced like a problem account.

Take Control of Your Commercial Auto Premiums

Commercial auto premiums aren't fixed overhead that a contractor has to accept. They respond to how the fleet is built, how drivers are managed, how safety is documented, and whether the insurer understands the trade.

For contractors, the safe driver discount is less about chasing a consumer-style coupon and more about controlling presentation. Clean MVRs, written driver rules, documented maintenance, and selective telematics use can all strengthen the file. Better files often mean better pricing discussions. They can also support stronger bid positioning when owners and general contractors want confidence that the company is organized.

For companies that want one more practical consumer-oriented read on course-based savings, this overview of defensive driving for lower premiums is useful background. The commercial takeaway is to ask whether the carrier applies that logic to the actual trade, not just to private passenger vehicles.

A contractor with safe crews, clear records, and the right underwriting partner has more control than most owners think. That control shows up in margins, in COIs, and in how confidently the business can bid the next job.

Coverage Axis offers a free commercial insurance quote and coverage review for contractors who want to lower fleet costs without cutting protection. A licensed advisor can review vehicle mix, driver setup, current pricing issues, and trade-specific options to see whether a better safe driver discount strategy is available.